Taxation Law: Residency and Tax Liability

VerifiedAdded on 2023/02/01

|10

|2575

|96

AI Summary

This document discusses the tests to determine tax residency for individuals in Australia, including the domicile test, Commonwealth Superannuation test, 183 day test, and ordinary 'residency' test. It also explains the tax liability for foreign tax residents and Australian tax residents. Additionally, it explores the factors that differentiate between a hobby and a business and the taxation treatment of the sale of different components of a business.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION LAW

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Case Study One

a) The issue of residency has been dealt with as per ss. 6-1 ITAA 1936. With regards to the

various tests that can be used to determine tax residency for individual taxpayers, the relevant

tax ruling is TR 98/17. As per this ruling, there are four tests that may be applicable which

are briefly described below (Woellner, 2015).

Domicile Test – In order to pass this test, it is essential that the underlying taxpayer should be

a domicile holder as per Domicile Act 1981. Additionally, it is also imperative that the

permanent abode of the concerned taxpayer during the year under consideration must lie in

Australian territory only (Krever, 2016).

Commonwealth Superannuation Test –This test is a specific test which is valid only for

Federal government employees who have been serving abroad. The criterion to determine tax

residency is to highlight if the underlying employee makes contribution to specified

superannuation schemes or not.

183 day test – This is used to test if the underlying foreign resident is a tax resident of

Australia or not. The primary condition that ought to be fulfilled for passing this test is that

the underlying taxpayer should have been physically present during the concerned tax year

in Australia for a minimum period of 183 days. Also, it is imperative that the Tax

Commissioner should have not suspicion in regards to intention on the part of the taxpayer to

settle in Australia over the long term.

Ordinary ‘residency’ test- Owing to the lack of clarity with regards to meaning of “reside” in

the Australian statute, the key parameters for this test have been outlined from the various

legal cases that act as precedents. These factors as summarized in TR 98/17 are indicated

below.

1) Purpose of visit to Australia – Typically Australian tax residency could potentially arise in

cases where the reason to visit is significant such as employment or study. In this regards, it

is noteworthy that visit to Australia for a short duration (such as 1 or 2 months) for

employment would not result in Australian tax residency as indicated in FC of T v. Pechey 75

ATC 4083.

2) Extent of personal and professional ties – The existence of strong personal and professional

ties with Australia in comparison to country of origin would make a valid case for Australian

2

a) The issue of residency has been dealt with as per ss. 6-1 ITAA 1936. With regards to the

various tests that can be used to determine tax residency for individual taxpayers, the relevant

tax ruling is TR 98/17. As per this ruling, there are four tests that may be applicable which

are briefly described below (Woellner, 2015).

Domicile Test – In order to pass this test, it is essential that the underlying taxpayer should be

a domicile holder as per Domicile Act 1981. Additionally, it is also imperative that the

permanent abode of the concerned taxpayer during the year under consideration must lie in

Australian territory only (Krever, 2016).

Commonwealth Superannuation Test –This test is a specific test which is valid only for

Federal government employees who have been serving abroad. The criterion to determine tax

residency is to highlight if the underlying employee makes contribution to specified

superannuation schemes or not.

183 day test – This is used to test if the underlying foreign resident is a tax resident of

Australia or not. The primary condition that ought to be fulfilled for passing this test is that

the underlying taxpayer should have been physically present during the concerned tax year

in Australia for a minimum period of 183 days. Also, it is imperative that the Tax

Commissioner should have not suspicion in regards to intention on the part of the taxpayer to

settle in Australia over the long term.

Ordinary ‘residency’ test- Owing to the lack of clarity with regards to meaning of “reside” in

the Australian statute, the key parameters for this test have been outlined from the various

legal cases that act as precedents. These factors as summarized in TR 98/17 are indicated

below.

1) Purpose of visit to Australia – Typically Australian tax residency could potentially arise in

cases where the reason to visit is significant such as employment or study. In this regards, it

is noteworthy that visit to Australia for a short duration (such as 1 or 2 months) for

employment would not result in Australian tax residency as indicated in FC of T v. Pechey 75

ATC 4083.

2) Extent of personal and professional ties – The existence of strong personal and professional

ties with Australia in comparison to country of origin would make a valid case for Australian

2

tax residency. The relevant case indicating the same is Peel v. The Commissioners of Inland

Revenue (1927) 13 TC 443 (Barkoczy, 2017).

3) Location of Assets – If the underlying taxpayer has significant assets (especially immovable)

located in Australia, it would potentially strength the case for Australian tax residency as the

taxpayer might stay for a long time (Reuters, 2017).

4) Living arrangement while in Australia – If the taxpayer tends to socially have a life in

Australia which is comparable to that in Australia, then the chances of Australian tax

residency would be enhanced (Woellner, 2015).

In wake of the above tests, the tax residency status of Sue needs to be determined who is a UK

resident. Clearly, the domicile test would be irrelevant for her as she does not hold Australian

domicile. Also, since she is not employed by the Federal government, hence the Commonwealth

superannuation test would not apply. The applicability of the other two tests for Sue based on the

given information is carried below.

1) 183 day test – It is evident that Sue arrived in Australia on August 1, 2018 and left Australia

on December 31, 2018. The total number of days of stay in Australia is less than 183 days

and hence she fails to pass this test.

2) Ordinary “Resides” Test – It is evident that Sue has come for employment which is a full

time position for a period of 4 months. Also, she has migrated to Australia with all her family

and hence has significant ties with Australia both professionally and personally. Based on the

above factors, she would be considered as Australian tax resident despite not having any

fixed assets in Australia.

For an Australian tax resident as per ss. 6-5(2)ITAA 1997, all sources of income would be taxed

irrespective of their geographical location. Hence, income for Sue would include the following

(Wilmot, 2016).

Interest on bank account in London – Ordinary Income (s. 6-5 ITAA 1997)

Salary and wages earned in London– Ordinary Income (s. 6-5 ITAA 1997)

Salary and wages earned from BHP while in Australia– Ordinary Income (s. 6-5 ITAA

1997)

3

Revenue (1927) 13 TC 443 (Barkoczy, 2017).

3) Location of Assets – If the underlying taxpayer has significant assets (especially immovable)

located in Australia, it would potentially strength the case for Australian tax residency as the

taxpayer might stay for a long time (Reuters, 2017).

4) Living arrangement while in Australia – If the taxpayer tends to socially have a life in

Australia which is comparable to that in Australia, then the chances of Australian tax

residency would be enhanced (Woellner, 2015).

In wake of the above tests, the tax residency status of Sue needs to be determined who is a UK

resident. Clearly, the domicile test would be irrelevant for her as she does not hold Australian

domicile. Also, since she is not employed by the Federal government, hence the Commonwealth

superannuation test would not apply. The applicability of the other two tests for Sue based on the

given information is carried below.

1) 183 day test – It is evident that Sue arrived in Australia on August 1, 2018 and left Australia

on December 31, 2018. The total number of days of stay in Australia is less than 183 days

and hence she fails to pass this test.

2) Ordinary “Resides” Test – It is evident that Sue has come for employment which is a full

time position for a period of 4 months. Also, she has migrated to Australia with all her family

and hence has significant ties with Australia both professionally and personally. Based on the

above factors, she would be considered as Australian tax resident despite not having any

fixed assets in Australia.

For an Australian tax resident as per ss. 6-5(2)ITAA 1997, all sources of income would be taxed

irrespective of their geographical location. Hence, income for Sue would include the following

(Wilmot, 2016).

Interest on bank account in London – Ordinary Income (s. 6-5 ITAA 1997)

Salary and wages earned in London– Ordinary Income (s. 6-5 ITAA 1997)

Salary and wages earned from BHP while in Australia– Ordinary Income (s. 6-5 ITAA

1997)

3

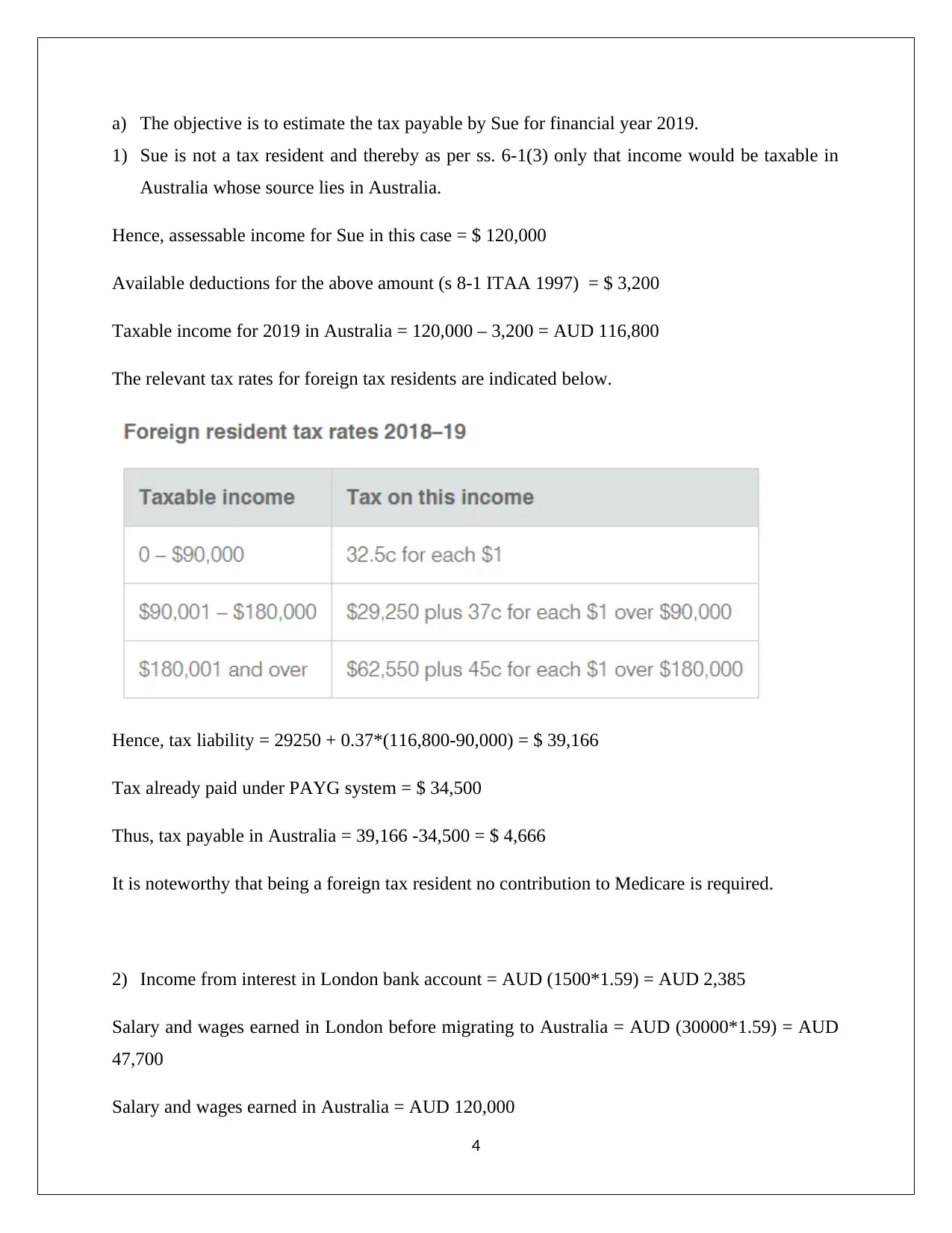

a) The objective is to estimate the tax payable by Sue for financial year 2019.

1) Sue is not a tax resident and thereby as per ss. 6-1(3) only that income would be taxable in

Australia whose source lies in Australia.

Hence, assessable income for Sue in this case = $ 120,000

Available deductions for the above amount (s 8-1 ITAA 1997) = $ 3,200

Taxable income for 2019 in Australia = 120,000 – 3,200 = AUD 116,800

The relevant tax rates for foreign tax residents are indicated below.

Hence, tax liability = 29250 + 0.37*(116,800-90,000) = $ 39,166

Tax already paid under PAYG system = $ 34,500

Thus, tax payable in Australia = 39,166 -34,500 = $ 4,666

It is noteworthy that being a foreign tax resident no contribution to Medicare is required.

2) Income from interest in London bank account = AUD (1500*1.59) = AUD 2,385

Salary and wages earned in London before migrating to Australia = AUD (30000*1.59) = AUD

47,700

Salary and wages earned in Australia = AUD 120,000

4

1) Sue is not a tax resident and thereby as per ss. 6-1(3) only that income would be taxable in

Australia whose source lies in Australia.

Hence, assessable income for Sue in this case = $ 120,000

Available deductions for the above amount (s 8-1 ITAA 1997) = $ 3,200

Taxable income for 2019 in Australia = 120,000 – 3,200 = AUD 116,800

The relevant tax rates for foreign tax residents are indicated below.

Hence, tax liability = 29250 + 0.37*(116,800-90,000) = $ 39,166

Tax already paid under PAYG system = $ 34,500

Thus, tax payable in Australia = 39,166 -34,500 = $ 4,666

It is noteworthy that being a foreign tax resident no contribution to Medicare is required.

2) Income from interest in London bank account = AUD (1500*1.59) = AUD 2,385

Salary and wages earned in London before migrating to Australia = AUD (30000*1.59) = AUD

47,700

Salary and wages earned in Australia = AUD 120,000

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

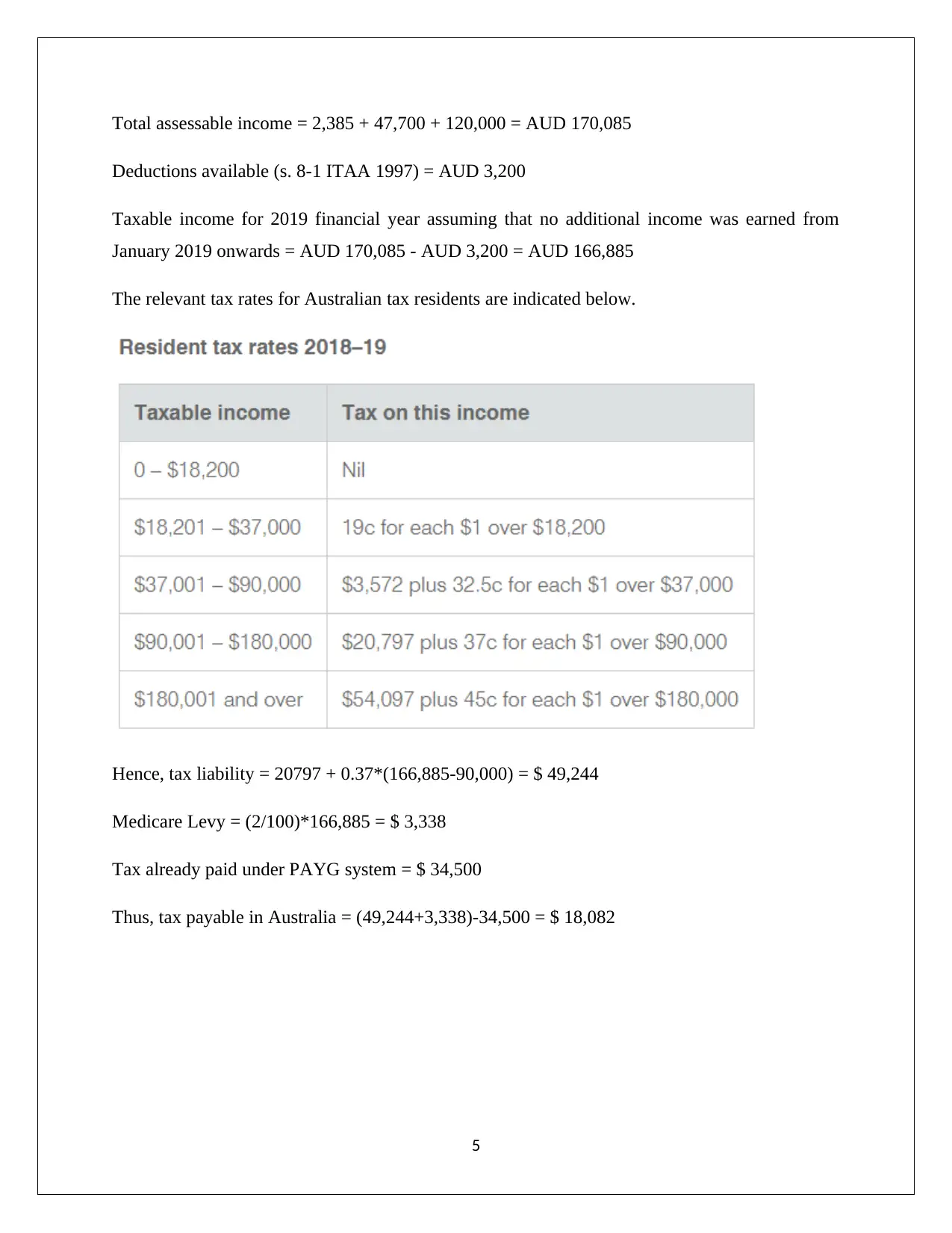

Total assessable income = 2,385 + 47,700 + 120,000 = AUD 170,085

Deductions available (s. 8-1 ITAA 1997) = AUD 3,200

Taxable income for 2019 financial year assuming that no additional income was earned from

January 2019 onwards = AUD 170,085 - AUD 3,200 = AUD 166,885

The relevant tax rates for Australian tax residents are indicated below.

Hence, tax liability = 20797 + 0.37*(166,885-90,000) = $ 49,244

Medicare Levy = (2/100)*166,885 = $ 3,338

Tax already paid under PAYG system = $ 34,500

Thus, tax payable in Australia = (49,244+3,338)-34,500 = $ 18,082

5

Deductions available (s. 8-1 ITAA 1997) = AUD 3,200

Taxable income for 2019 financial year assuming that no additional income was earned from

January 2019 onwards = AUD 170,085 - AUD 3,200 = AUD 166,885

The relevant tax rates for Australian tax residents are indicated below.

Hence, tax liability = 20797 + 0.37*(166,885-90,000) = $ 49,244

Medicare Levy = (2/100)*166,885 = $ 3,338

Tax already paid under PAYG system = $ 34,500

Thus, tax payable in Australia = (49,244+3,338)-34,500 = $ 18,082

5

Case Study 2

The various factors which distinguish between a carrying on an activity as hobby or business

have been highlighted in TR 97/11. One of the relevant factors in this regards is the underlying

intention of the taxpayer whose importance has been indicated in the Inglis v. FC of T (1979) 10

ATR 493 (Krever, 2016). However, the judge in this case also indicated that the activity level

also indicated the difference between the two i.e. hobby and business. As per Case H11 76

ATC 59 at 61, the pivotal factor which helps differentiating between hobby and business is the

presence of profit motive. Further, Smith v. Anderson (1880) 15 Ch D 247 defines business as an

activity which is done with profit intention. As per the verdict in Tweddle v. FC of T (1942) 7

ATD 186, the presence of current profits is not necessary for an activity to be labeled as business

but profit prospect must exist as per as the taxpayer (Coleman, 2015). Additionally, business

activities tend to be recurring unlike hobby which is done in leisure time and is often

intermittent.

The given situation needs to be analysed in the wake of the above discussion. It is apparent that

the amount of investment is zero as the account was free. Also, Sally is selling only second hand

goods that too below cost. Further, these are personal items only and are being sold once their

use is over. Also, during one year the turnover is quite low at $ 4,200. Based on the given

evidence it is evident that profit motive is lacking and it is a hobby whereby Sally is trying to

dispose all unwanted personal items. However, this opinion may change if she actively starts

purchasing second hand goods for selling on eBay wth the objective of making money.

Case Study 3

It is noteworthy that if the receipts received are on account of liquidation of capital assets, then

these would be termed as capital receipts and not subject to income tax. However, any capital

gains derived in the process may be subject to CGT (Capital Gains Tax). The relevant taxation

treatment of the sale of the various components of business is discussed below (Hodgson,

Mortimer & Butler, 2016).

6

The various factors which distinguish between a carrying on an activity as hobby or business

have been highlighted in TR 97/11. One of the relevant factors in this regards is the underlying

intention of the taxpayer whose importance has been indicated in the Inglis v. FC of T (1979) 10

ATR 493 (Krever, 2016). However, the judge in this case also indicated that the activity level

also indicated the difference between the two i.e. hobby and business. As per Case H11 76

ATC 59 at 61, the pivotal factor which helps differentiating between hobby and business is the

presence of profit motive. Further, Smith v. Anderson (1880) 15 Ch D 247 defines business as an

activity which is done with profit intention. As per the verdict in Tweddle v. FC of T (1942) 7

ATD 186, the presence of current profits is not necessary for an activity to be labeled as business

but profit prospect must exist as per as the taxpayer (Coleman, 2015). Additionally, business

activities tend to be recurring unlike hobby which is done in leisure time and is often

intermittent.

The given situation needs to be analysed in the wake of the above discussion. It is apparent that

the amount of investment is zero as the account was free. Also, Sally is selling only second hand

goods that too below cost. Further, these are personal items only and are being sold once their

use is over. Also, during one year the turnover is quite low at $ 4,200. Based on the given

evidence it is evident that profit motive is lacking and it is a hobby whereby Sally is trying to

dispose all unwanted personal items. However, this opinion may change if she actively starts

purchasing second hand goods for selling on eBay wth the objective of making money.

Case Study 3

It is noteworthy that if the receipts received are on account of liquidation of capital assets, then

these would be termed as capital receipts and not subject to income tax. However, any capital

gains derived in the process may be subject to CGT (Capital Gains Tax). The relevant taxation

treatment of the sale of the various components of business is discussed below (Hodgson,

Mortimer & Butler, 2016).

6

1) Goodwill – As per s. 108-5 ITAA 1997, goodwill is an example of a CGT asset. As a result,

any proceeds from the liquidation of this asset would not be taxed as these would be capital

receipts and not revenue receipts. However, CGT may be applicable on the underlying

taxpayer. The sale of a CGT asset triggers an A1 CGT event for which the capital would be

computed by subtracting the cost base of the asset from the sales proceeds (Coleman, 2015).

Sales proceeds of goodwill = $ 200,000

The cost base for goodwill would be zero since it is internally generated and not acquired as

part of any acquisition.

Hence, gross capital gains = $ 200,000 - $ 0 = $ 200,000

Considering that the business was started in 2005, hence the asset is long term owing to

which discount method rebate under s. 115-5 ITAA 1997 would be available.

Thus, taxable capital gains on account of goodwill sale = 0.5*(200,000) = $100,000

It is noteworthy that small business CGT concessions would be available on the goodwill

which is an active asset. Thereby, capital gains subject to CGT = 0.5*100,000 = $50,000

2) Furniture and fixtures are depreciating capital assets whose sale would lead to non-taxable

capital receipts. However, capital gains can potentially arise on which CGT would be

payable. The sale of a CGT asset triggers an A1 CGT event for which the capital would be

computed by subtracting the cost base of the asset from the sales proceeds (Hodgson,

Mortimer & Butler, 2016).

Sales proceeds from sale of furniture and fixtures = $ 125,000

Written down value for tax purposes =$ 120,000

Hence, capital gains on sale of furniture and fittings = 125,000 – 120,000 = $ 5,000

Considering that the business was started in 2005, hence the asset is long term owing to which

discount method rebate under s. 115-5 ITAA 1997 would be available (Krever, 2016).

Thus, taxable capital gains on account of furniture and fixtures sale = 0.5*(5,000) = $2,500

7

any proceeds from the liquidation of this asset would not be taxed as these would be capital

receipts and not revenue receipts. However, CGT may be applicable on the underlying

taxpayer. The sale of a CGT asset triggers an A1 CGT event for which the capital would be

computed by subtracting the cost base of the asset from the sales proceeds (Coleman, 2015).

Sales proceeds of goodwill = $ 200,000

The cost base for goodwill would be zero since it is internally generated and not acquired as

part of any acquisition.

Hence, gross capital gains = $ 200,000 - $ 0 = $ 200,000

Considering that the business was started in 2005, hence the asset is long term owing to

which discount method rebate under s. 115-5 ITAA 1997 would be available.

Thus, taxable capital gains on account of goodwill sale = 0.5*(200,000) = $100,000

It is noteworthy that small business CGT concessions would be available on the goodwill

which is an active asset. Thereby, capital gains subject to CGT = 0.5*100,000 = $50,000

2) Furniture and fixtures are depreciating capital assets whose sale would lead to non-taxable

capital receipts. However, capital gains can potentially arise on which CGT would be

payable. The sale of a CGT asset triggers an A1 CGT event for which the capital would be

computed by subtracting the cost base of the asset from the sales proceeds (Hodgson,

Mortimer & Butler, 2016).

Sales proceeds from sale of furniture and fixtures = $ 125,000

Written down value for tax purposes =$ 120,000

Hence, capital gains on sale of furniture and fittings = 125,000 – 120,000 = $ 5,000

Considering that the business was started in 2005, hence the asset is long term owing to which

discount method rebate under s. 115-5 ITAA 1997 would be available (Krever, 2016).

Thus, taxable capital gains on account of furniture and fixtures sale = 0.5*(5,000) = $2,500

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is noteworthy that small business CGT concessions would be available on the furniture and

fixtures which is an active asset. Thereby, capital gains subject to CGT = 0.5*2,500 = $1,250

3) Building premises is an immovable asset which is also a CGT asset as per s. 108-5 ITAA

1997. As a result, any proceeds from the liquidation of this asset would not be taxed as these

would be capital receipts and not revenue receipts (Woellner, 2015). However, CGT may be

applicable on the underlying taxpayer. The sale of a CGT asset triggers an A1 CGT event for

which the capital would be computed by subtracting the cost base of the asset from the sales

proceeds (Barkoczy, 2017).

Sales proceeds obtained from building premises = $ 500,000

Tax adjusted value of building premises = $ 350,000

Capital gains derived = $500,000 - $350,000 = $150,000

Considering that the business was started in 2005, hence the asset is long term owing to which

discount method rebate under s. 115-5 ITAA 1997 would be available.

Thus, taxable capital gains on account of building premises sale = 0.5*(150,000) = $75,000

It is noteworthy that small business CGT concessions would be available on the building premise

which is an active asset. Thereby, capital gains subject to CGT = 0.5*75,000 = $37,500

4) With regards to trading stock, it is noteworthy that in accordance with s. 118-25 ITAA 1997,

any capital gains or losses made are disregarded (Reuters, 2017). One of the key reasons for

the same is that trading stock would not lead to capital receipts but essentially revenue

receipts as the business involved regular and continuous selling of the trading stock with the

objective to make profit. As a result, the difference between the cost price trading stock and

existing market value of trading stock would lead to ordinary income as per s. 6-5 ITAA

1997. This would be assessable at the end of the taxpayer (Barkoczy, 2017).

Hence, taxable income = $295,000 -$ 150,000 =$145,000

8

fixtures which is an active asset. Thereby, capital gains subject to CGT = 0.5*2,500 = $1,250

3) Building premises is an immovable asset which is also a CGT asset as per s. 108-5 ITAA

1997. As a result, any proceeds from the liquidation of this asset would not be taxed as these

would be capital receipts and not revenue receipts (Woellner, 2015). However, CGT may be

applicable on the underlying taxpayer. The sale of a CGT asset triggers an A1 CGT event for

which the capital would be computed by subtracting the cost base of the asset from the sales

proceeds (Barkoczy, 2017).

Sales proceeds obtained from building premises = $ 500,000

Tax adjusted value of building premises = $ 350,000

Capital gains derived = $500,000 - $350,000 = $150,000

Considering that the business was started in 2005, hence the asset is long term owing to which

discount method rebate under s. 115-5 ITAA 1997 would be available.

Thus, taxable capital gains on account of building premises sale = 0.5*(150,000) = $75,000

It is noteworthy that small business CGT concessions would be available on the building premise

which is an active asset. Thereby, capital gains subject to CGT = 0.5*75,000 = $37,500

4) With regards to trading stock, it is noteworthy that in accordance with s. 118-25 ITAA 1997,

any capital gains or losses made are disregarded (Reuters, 2017). One of the key reasons for

the same is that trading stock would not lead to capital receipts but essentially revenue

receipts as the business involved regular and continuous selling of the trading stock with the

objective to make profit. As a result, the difference between the cost price trading stock and

existing market value of trading stock would lead to ordinary income as per s. 6-5 ITAA

1997. This would be assessable at the end of the taxpayer (Barkoczy, 2017).

Hence, taxable income = $295,000 -$ 150,000 =$145,000

8

Therefore, based on the above discussion, it can be concluded that the sale of business would

result in ordinary income of $ 145,000 and taxable capital gains to the tune of $88,750.

9

result in ordinary income of $ 145,000 and taxable capital gains to the tune of $88,750.

9

References

Barkoczy, S. (2017). Foundation of Taxation Law 2017 (9th ed.). North Ryde: CCH Publications.

Coleman, C. (2015). Australian Tax Analysis (4th ed.). Sydney: Thomson Reuters (Professional)

Australia.

Hodgson, H., Mortimer, C. & Butler, J. (2016). Tax Questions and Answers 2016 (6th ed.).

Sydney: Thomson Reuters.

Krever, R. (2016). Australian Taxation Law Cases 2017 (2nd ed.). Brisbane: THOMSON

LAWBOOK Company.

Reuters, T. (2017). Australian Tax Legislation 2017 (4th ed.). Sydney. THOMSON REUTERS.

Wilmot, C. (2016). FBT Compliance guide (6th ed.). North Ryde: CCH Australia Limited.

Woellner, R. (2015). Australian taxation law 2014 (8th ed.). North Ryde: CCH Australia.

10

Barkoczy, S. (2017). Foundation of Taxation Law 2017 (9th ed.). North Ryde: CCH Publications.

Coleman, C. (2015). Australian Tax Analysis (4th ed.). Sydney: Thomson Reuters (Professional)

Australia.

Hodgson, H., Mortimer, C. & Butler, J. (2016). Tax Questions and Answers 2016 (6th ed.).

Sydney: Thomson Reuters.

Krever, R. (2016). Australian Taxation Law Cases 2017 (2nd ed.). Brisbane: THOMSON

LAWBOOK Company.

Reuters, T. (2017). Australian Tax Legislation 2017 (4th ed.). Sydney. THOMSON REUTERS.

Wilmot, C. (2016). FBT Compliance guide (6th ed.). North Ryde: CCH Australia Limited.

Woellner, R. (2015). Australian taxation law 2014 (8th ed.). North Ryde: CCH Australia.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.