TAXATION LAW. STUDENT ID:. [Pick the date]. Question 1.

VerifiedAdded on 2022/11/13

|7

|2668

|2

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION LAW

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 1

Issue

In wake of the given facts, the objective is to provide legal advice to taxpayer Helen

in the context of CGT liability that could potential arise on account of the various sale

transactions that have occurred during 2017-2018.

Law

The relevant aspects to be considered are highlighted below.

Concept of Pre-CGT asset

This is a crucial aspect as in accordance with ss. 149-10 (ITAA 1997), it has been

indicated that a pre-CGT asset would not attract any CGT liability irrespective of the

holding period and the extent of capital gains or losses. It is essential to note that the

classification of these assets is done on the date of purchase. Since capital gains

regime was made enforceable on September 20, 1985, hence any assets purchased

before this date would be termed as pre-CGT asset and would not attract any tax on

account of capital gains or losses (Coleman, 2016).

Asset Class - Collectibles

A particular capital asset class which has a statutory definition is collectible as

indicated in ss. 108-15 (Austlii, n.d.). This includes various items such as antique,

artwork (painting, sculpture, picture) etc. The following are two key asp3cts related to

this asset class (Deutsch et. al., 2016).

As per s. 108-10(1), the capital losses arising from this class of assets must

be necessarily adjusted against capital gains of this asset class only.

As per s. 118-10, CGT would not apply for any capital gains or loss that arise

from collectibles having cost base less than $ 500.

Computation of Capital gains

As collectible belong to CGT asset, hence their disposal would trigger a A1 CGT

event. Under this event, there is a need to compute the capital gains by referring to

the formula which has been given in ss. 104-10. This formula advocates that asset

cost base ought to be deducted from the liquidation proceeds of the underlying asset

(Gilders et. al., 2016).

Taxable Capital Gains

There are two ways in which the tax liability could be reduced namely discount

method and cost indexation method. Discount method as described in Division 115

allows for 50% exemption on the capital gains for individual taxpayers provided the

asset is a long term asset (i.e. holding period of atleast one year).Cost indexation

method allows for inflation adjustment in the cost base which increases the same

and reduction of capital gains (Barkoczy,2018).

Application

Based on the given rules, the appropriate result for each of the transactions is as

highlighted below.

2

Issue

In wake of the given facts, the objective is to provide legal advice to taxpayer Helen

in the context of CGT liability that could potential arise on account of the various sale

transactions that have occurred during 2017-2018.

Law

The relevant aspects to be considered are highlighted below.

Concept of Pre-CGT asset

This is a crucial aspect as in accordance with ss. 149-10 (ITAA 1997), it has been

indicated that a pre-CGT asset would not attract any CGT liability irrespective of the

holding period and the extent of capital gains or losses. It is essential to note that the

classification of these assets is done on the date of purchase. Since capital gains

regime was made enforceable on September 20, 1985, hence any assets purchased

before this date would be termed as pre-CGT asset and would not attract any tax on

account of capital gains or losses (Coleman, 2016).

Asset Class - Collectibles

A particular capital asset class which has a statutory definition is collectible as

indicated in ss. 108-15 (Austlii, n.d.). This includes various items such as antique,

artwork (painting, sculpture, picture) etc. The following are two key asp3cts related to

this asset class (Deutsch et. al., 2016).

As per s. 108-10(1), the capital losses arising from this class of assets must

be necessarily adjusted against capital gains of this asset class only.

As per s. 118-10, CGT would not apply for any capital gains or loss that arise

from collectibles having cost base less than $ 500.

Computation of Capital gains

As collectible belong to CGT asset, hence their disposal would trigger a A1 CGT

event. Under this event, there is a need to compute the capital gains by referring to

the formula which has been given in ss. 104-10. This formula advocates that asset

cost base ought to be deducted from the liquidation proceeds of the underlying asset

(Gilders et. al., 2016).

Taxable Capital Gains

There are two ways in which the tax liability could be reduced namely discount

method and cost indexation method. Discount method as described in Division 115

allows for 50% exemption on the capital gains for individual taxpayers provided the

asset is a long term asset (i.e. holding period of atleast one year).Cost indexation

method allows for inflation adjustment in the cost base which increases the same

and reduction of capital gains (Barkoczy,2018).

Application

Based on the given rules, the appropriate result for each of the transactions is as

highlighted below.

2

Asset 1: Antique painting

The underlying painting was bought by taxpayer’s father in the pre-CGT era. This

can be established owing to the month of purchase being February 1985 which lies

before September 20, 1985. As a result, the given asset would be labelled as a pre-

CGT asset and thereby no CGT would be paid by Helen on any capital gains made

on this asset.

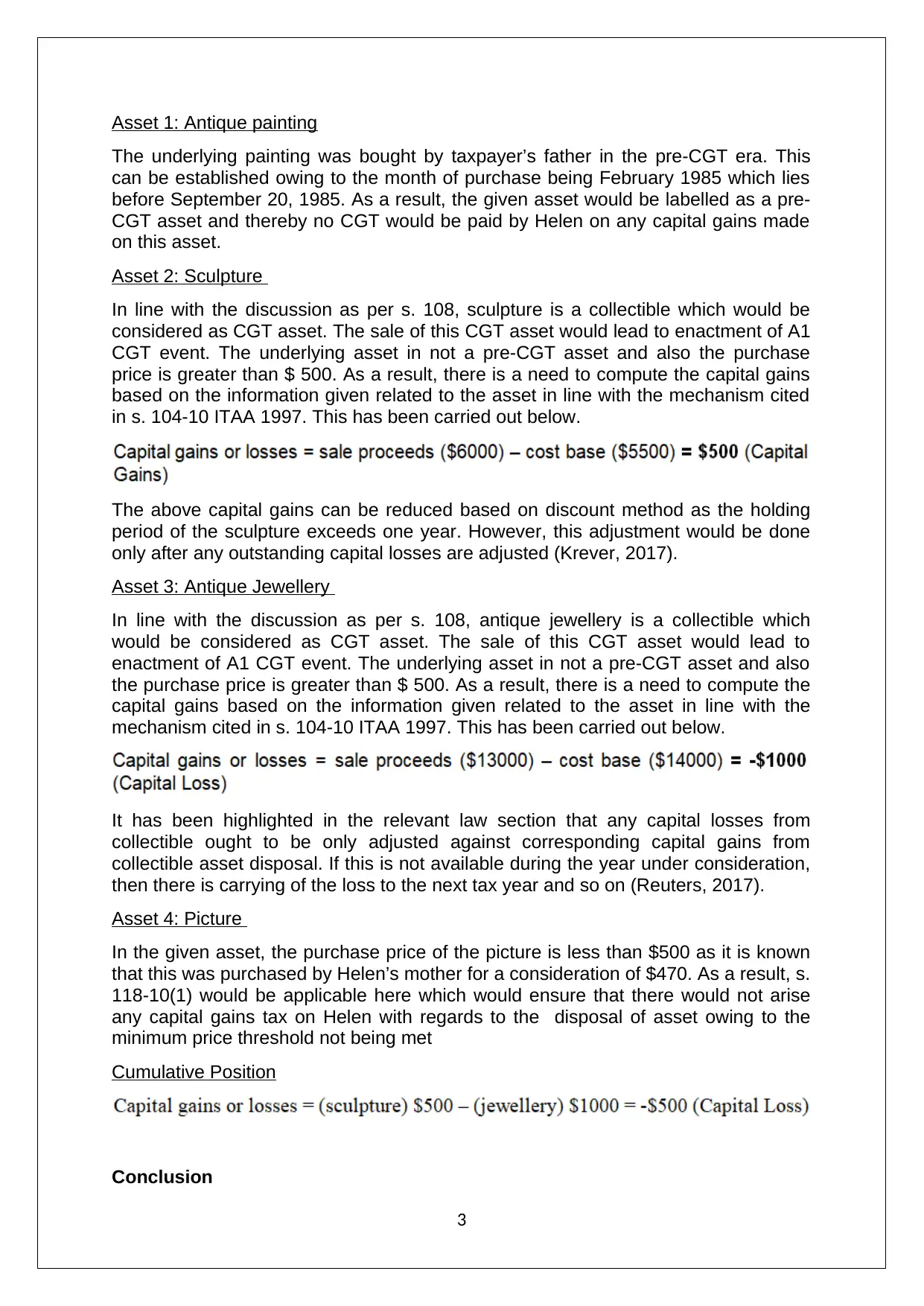

Asset 2: Sculpture

In line with the discussion as per s. 108, sculpture is a collectible which would be

considered as CGT asset. The sale of this CGT asset would lead to enactment of A1

CGT event. The underlying asset in not a pre-CGT asset and also the purchase

price is greater than $ 500. As a result, there is a need to compute the capital gains

based on the information given related to the asset in line with the mechanism cited

in s. 104-10 ITAA 1997. This has been carried out below.

The above capital gains can be reduced based on discount method as the holding

period of the sculpture exceeds one year. However, this adjustment would be done

only after any outstanding capital losses are adjusted (Krever, 2017).

Asset 3: Antique Jewellery

In line with the discussion as per s. 108, antique jewellery is a collectible which

would be considered as CGT asset. The sale of this CGT asset would lead to

enactment of A1 CGT event. The underlying asset in not a pre-CGT asset and also

the purchase price is greater than $ 500. As a result, there is a need to compute the

capital gains based on the information given related to the asset in line with the

mechanism cited in s. 104-10 ITAA 1997. This has been carried out below.

It has been highlighted in the relevant law section that any capital losses from

collectible ought to be only adjusted against corresponding capital gains from

collectible asset disposal. If this is not available during the year under consideration,

then there is carrying of the loss to the next tax year and so on (Reuters, 2017).

Asset 4: Picture

In the given asset, the purchase price of the picture is less than $500 as it is known

that this was purchased by Helen’s mother for a consideration of $470. As a result, s.

118-10(1) would be applicable here which would ensure that there would not arise

any capital gains tax on Helen with regards to the disposal of asset owing to the

minimum price threshold not being met

Cumulative Position

Conclusion

3

The underlying painting was bought by taxpayer’s father in the pre-CGT era. This

can be established owing to the month of purchase being February 1985 which lies

before September 20, 1985. As a result, the given asset would be labelled as a pre-

CGT asset and thereby no CGT would be paid by Helen on any capital gains made

on this asset.

Asset 2: Sculpture

In line with the discussion as per s. 108, sculpture is a collectible which would be

considered as CGT asset. The sale of this CGT asset would lead to enactment of A1

CGT event. The underlying asset in not a pre-CGT asset and also the purchase

price is greater than $ 500. As a result, there is a need to compute the capital gains

based on the information given related to the asset in line with the mechanism cited

in s. 104-10 ITAA 1997. This has been carried out below.

The above capital gains can be reduced based on discount method as the holding

period of the sculpture exceeds one year. However, this adjustment would be done

only after any outstanding capital losses are adjusted (Krever, 2017).

Asset 3: Antique Jewellery

In line with the discussion as per s. 108, antique jewellery is a collectible which

would be considered as CGT asset. The sale of this CGT asset would lead to

enactment of A1 CGT event. The underlying asset in not a pre-CGT asset and also

the purchase price is greater than $ 500. As a result, there is a need to compute the

capital gains based on the information given related to the asset in line with the

mechanism cited in s. 104-10 ITAA 1997. This has been carried out below.

It has been highlighted in the relevant law section that any capital losses from

collectible ought to be only adjusted against corresponding capital gains from

collectible asset disposal. If this is not available during the year under consideration,

then there is carrying of the loss to the next tax year and so on (Reuters, 2017).

Asset 4: Picture

In the given asset, the purchase price of the picture is less than $500 as it is known

that this was purchased by Helen’s mother for a consideration of $470. As a result, s.

118-10(1) would be applicable here which would ensure that there would not arise

any capital gains tax on Helen with regards to the disposal of asset owing to the

minimum price threshold not being met

Cumulative Position

Conclusion

3

Based on the cumulative position, it is evident that the net capital loss of $ 500 has

been made by Helen which cannot be offset against any revenue receipts and must

be necessarily adjusted against collectible based capital gains which may be done in

the existing year or in future years.

Question 2

Issue

Barbara (taxpayer) has received several payments in relation to a book on

economics which has written. This book results in several proceeds and the

objective is to outline if any of these would be personal exertion linked income.

Further, alternative scenario where Barbara wrote the book in spare time and later

only decided to sell the same would be considered. It would be indicated if any

change in classification of proceeds happens or not.

Law

Income from personal exertion has been highlighted under s. 6 ITAA 1997. It

requires that the taxpayer must use his/her skills in order to produce commercial

value based on the activity undertaken and the effort taken therein. Indulgence in

activity alone would not lead to personal exertion related income if there is no

commercial value derived on account of activity (Barkoczy, 2018). Further, there are

scenarios and circumstances in which even though effort is involved in activity and

commercial proceeds are also derived, these are not for the activity as the activity

facilitates the transfer of the asset having real commercial value. A case which

demonstrates the same is Brent vs Federal Commissioner of Taxation (1971) 125

CLR. Here, the interview was given by the taxpayer but it was a means for providing

information which had commercial value and thereby the proceeds were treated to

be capital and non-taxable (Woellner, 2014).

Application

Some key facts related to the given situation are highlighted below.

Barbara has no experience in writing a book.

She is not famous for her literary skills.

She has knowledge of economics and also conducting research.

In wake of the above facts, the obtaining of offer from publisher would imply that the

book is a means to obtain access to the knowledge which Barbara has acquired over

the years. The act of writing does not lead to any commercial value since Barbara

does not have writing skills. It is only a means to express the knowledge which is the

key asset, The copyright also relates to this very asset as literary skills lack any

commercial worth. Hence, these proceeds would not be categorised as income on

account of personal exertion.

Further, the manuscript also derives value on account of knowledge being the key

asset. If Barbara has used her literary skills to write a book pertaining to a topic not

related to economics, hence the manuscript would not have any value. Thereby it is

is knowledge which provides worth and not the writing effort and hence these

proceeds also would not be categorised as income on account of personal exertion.

However, an exception to this classification trend is in the form of proceeds based on

4

been made by Helen which cannot be offset against any revenue receipts and must

be necessarily adjusted against collectible based capital gains which may be done in

the existing year or in future years.

Question 2

Issue

Barbara (taxpayer) has received several payments in relation to a book on

economics which has written. This book results in several proceeds and the

objective is to outline if any of these would be personal exertion linked income.

Further, alternative scenario where Barbara wrote the book in spare time and later

only decided to sell the same would be considered. It would be indicated if any

change in classification of proceeds happens or not.

Law

Income from personal exertion has been highlighted under s. 6 ITAA 1997. It

requires that the taxpayer must use his/her skills in order to produce commercial

value based on the activity undertaken and the effort taken therein. Indulgence in

activity alone would not lead to personal exertion related income if there is no

commercial value derived on account of activity (Barkoczy, 2018). Further, there are

scenarios and circumstances in which even though effort is involved in activity and

commercial proceeds are also derived, these are not for the activity as the activity

facilitates the transfer of the asset having real commercial value. A case which

demonstrates the same is Brent vs Federal Commissioner of Taxation (1971) 125

CLR. Here, the interview was given by the taxpayer but it was a means for providing

information which had commercial value and thereby the proceeds were treated to

be capital and non-taxable (Woellner, 2014).

Application

Some key facts related to the given situation are highlighted below.

Barbara has no experience in writing a book.

She is not famous for her literary skills.

She has knowledge of economics and also conducting research.

In wake of the above facts, the obtaining of offer from publisher would imply that the

book is a means to obtain access to the knowledge which Barbara has acquired over

the years. The act of writing does not lead to any commercial value since Barbara

does not have writing skills. It is only a means to express the knowledge which is the

key asset, The copyright also relates to this very asset as literary skills lack any

commercial worth. Hence, these proceeds would not be categorised as income on

account of personal exertion.

Further, the manuscript also derives value on account of knowledge being the key

asset. If Barbara has used her literary skills to write a book pertaining to a topic not

related to economics, hence the manuscript would not have any value. Thereby it is

is knowledge which provides worth and not the writing effort and hence these

proceeds also would not be categorised as income on account of personal exertion.

However, an exception to this classification trend is in the form of proceeds based on

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

sale of interview transcript. These did not exist previously and were conducted while

the book writing was being carried on. Also, Barbara is a researcher in economics

and thereby has the right skills for interviews and related research. Hence, these

proceeds are categorised as income from personal exertion.

Alternative motive for book writing

As per the altered facts, now the book has been written in Barbara’s spare time

without any specific intention to publish. Only after it was completed did Barbara

decide to publish the same. A significant change in this circumstance when

compared with the previous circumstance is that while engaging in the activity profit

motive is absent. However, it does not alter the fact that literary skills of Barbara

would not be valued in this case also. Further, when a publisher does show interest

in paying for the book, essentially the proceeds are for the knowledge regarding

economics that Barbara has. No new commercial value is created by the act of

writing, hence the proceeds from book sale would not lead to income being obtained

from personal exertion (Nethercott, Richardson and Devos, 2016).

Question 3

Issue

The aim is to analyse the given facts and determine the tax liabilities that could be

potentially levied on Patrick owing to the lending arrangement with his son David. As

per this, an interest free loan to the tune of $ 52,000 was offered to David with the

promise that the same would be paid after five years. However, David paid this

money only after two years but besides principal repayment also gave extra amount

to the tune of 5% of the principal lent.

Rule

Whenever proceeds are received by any taxpayer that seeks to discharge a loan

obligation, then there would be typically two kind of payment. One would be principal

repayment which the taxpayer would receive as the principal amount was lent. Since

this amounts to repayment of the amount already lent, hence this would be capital

proceeds. On the other hand, it is possible that over and above the principal amount,

some incremental amount is also provided which may be assessable at the end of

the taxpayer. The various possible outcomes are outlined below.

1) Declared as assessable income – The assessable income declaration is

linked to the intention of deriving profit. The extra payment may be income as

per ordinary concepts (s. 6-5 ITAA 1997) if it can be proved that the taxpayer

enters such transactions on a regular basis and thereby this is essentially a

commercial transaction. The manner of conduct on part of taxpayer would

assume significance as it would indicate the commercial element of the

transaction. Also, another alternative may arise even though such

transactions are not conducted regularly. In this scenario, the taxpayer

conducts an isolated (not regular) transaction with the motive of earning profit

and thereby income derived would be assessable (s. 15-15 ITAA 1997)

(Gilders et. al., 2016).

2) Declared as non-assessable income – The declaration of proceeds as non-

assessable income would happen only when the amount is considered gift.

5

the book writing was being carried on. Also, Barbara is a researcher in economics

and thereby has the right skills for interviews and related research. Hence, these

proceeds are categorised as income from personal exertion.

Alternative motive for book writing

As per the altered facts, now the book has been written in Barbara’s spare time

without any specific intention to publish. Only after it was completed did Barbara

decide to publish the same. A significant change in this circumstance when

compared with the previous circumstance is that while engaging in the activity profit

motive is absent. However, it does not alter the fact that literary skills of Barbara

would not be valued in this case also. Further, when a publisher does show interest

in paying for the book, essentially the proceeds are for the knowledge regarding

economics that Barbara has. No new commercial value is created by the act of

writing, hence the proceeds from book sale would not lead to income being obtained

from personal exertion (Nethercott, Richardson and Devos, 2016).

Question 3

Issue

The aim is to analyse the given facts and determine the tax liabilities that could be

potentially levied on Patrick owing to the lending arrangement with his son David. As

per this, an interest free loan to the tune of $ 52,000 was offered to David with the

promise that the same would be paid after five years. However, David paid this

money only after two years but besides principal repayment also gave extra amount

to the tune of 5% of the principal lent.

Rule

Whenever proceeds are received by any taxpayer that seeks to discharge a loan

obligation, then there would be typically two kind of payment. One would be principal

repayment which the taxpayer would receive as the principal amount was lent. Since

this amounts to repayment of the amount already lent, hence this would be capital

proceeds. On the other hand, it is possible that over and above the principal amount,

some incremental amount is also provided which may be assessable at the end of

the taxpayer. The various possible outcomes are outlined below.

1) Declared as assessable income – The assessable income declaration is

linked to the intention of deriving profit. The extra payment may be income as

per ordinary concepts (s. 6-5 ITAA 1997) if it can be proved that the taxpayer

enters such transactions on a regular basis and thereby this is essentially a

commercial transaction. The manner of conduct on part of taxpayer would

assume significance as it would indicate the commercial element of the

transaction. Also, another alternative may arise even though such

transactions are not conducted regularly. In this scenario, the taxpayer

conducts an isolated (not regular) transaction with the motive of earning profit

and thereby income derived would be assessable (s. 15-15 ITAA 1997)

(Gilders et. al., 2016).

2) Declared as non-assessable income – The declaration of proceeds as non-

assessable income would happen only when the amount is considered gift.

5

For this, the legal precedents indicate that normal characteristics of gift ought

to be existing based on the conduct of the parties and the circumstances. Tax

ruling TR 2005/13 indicates the applicable conditions for gift below (Coleman,

2016).

The gift should be transferred to the transferee.

The gift should not be driven by reciprocal expectations in present or future.

The gift should be given voluntarily without force or asking.

The gift should benefit the transferee and should not cause harm.

Application

In regards to the payment given by David, it would be noted that the amount of $

52,000 from the receipts would go towards repayment of loan. As a result, these

would be capital proceeds for Patrick on which he would not have to bear any tax.

Now the issue arises with regards to the 5% of the principal paid extra by David.

This is not assessable as per section 6-5 ITAA 1997 as the transaction is not

commercial. This is evident from the conduct of the two parties. If Patrick was

engaged in money lending transactions on a regular basis, he would have asked for

some collateral and would have enacted as a formal agreement which could serve

as a proof for future. Also, he mentioned no intention for interest which clearly

indicates non-commercial transaction where repayment was dependent on the

goodwill of the son. Lack of intention to take interest payment would imply that

section 15-15 cannot be applied here and the additional proceeds would not be

assessable under either s. 6-5 or s. 15-15 ITAA 1997.

The incremental amount is therefore gift and would not attract tax liability for Patrick.

This may be proved on the basis of following aspects.

1) Through the means of the cheque, there has been actual transfer of extra

payment from David to Patrick.

2) In lieu or exchange of the payment given to his father, he does not have any

incremental expectations (present or future).

3) The payment was voluntary as Patrick indicated non-requirement of any

interest payment.

4) Extra payment would make Patrick economically better off and hence is

beneficial for him.

Conclusion

In line with the discussion above, it would be correct to conclude that for the existing

loan arrangement between Patrick and his son David, Patrick would not have to pay

any tax despite deriving economic benefit.

6

to be existing based on the conduct of the parties and the circumstances. Tax

ruling TR 2005/13 indicates the applicable conditions for gift below (Coleman,

2016).

The gift should be transferred to the transferee.

The gift should not be driven by reciprocal expectations in present or future.

The gift should be given voluntarily without force or asking.

The gift should benefit the transferee and should not cause harm.

Application

In regards to the payment given by David, it would be noted that the amount of $

52,000 from the receipts would go towards repayment of loan. As a result, these

would be capital proceeds for Patrick on which he would not have to bear any tax.

Now the issue arises with regards to the 5% of the principal paid extra by David.

This is not assessable as per section 6-5 ITAA 1997 as the transaction is not

commercial. This is evident from the conduct of the two parties. If Patrick was

engaged in money lending transactions on a regular basis, he would have asked for

some collateral and would have enacted as a formal agreement which could serve

as a proof for future. Also, he mentioned no intention for interest which clearly

indicates non-commercial transaction where repayment was dependent on the

goodwill of the son. Lack of intention to take interest payment would imply that

section 15-15 cannot be applied here and the additional proceeds would not be

assessable under either s. 6-5 or s. 15-15 ITAA 1997.

The incremental amount is therefore gift and would not attract tax liability for Patrick.

This may be proved on the basis of following aspects.

1) Through the means of the cheque, there has been actual transfer of extra

payment from David to Patrick.

2) In lieu or exchange of the payment given to his father, he does not have any

incremental expectations (present or future).

3) The payment was voluntary as Patrick indicated non-requirement of any

interest payment.

4) Extra payment would make Patrick economically better off and hence is

beneficial for him.

Conclusion

In line with the discussion above, it would be correct to conclude that for the existing

loan arrangement between Patrick and his son David, Patrick would not have to pay

any tax despite deriving economic benefit.

6

References

Austlii (n.d.) , INCOME TAX ASSESSMENT ACT 1997 - SECT 108.15, [online]

available at http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s108.15.html [Accessed May 28, 2019]

Barkoczy, S. (2018), Foundation of Taxation Law 2018, 9thed.,NorthRyde: CCH

Publications,

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters

(Professional) Australia,

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016), Australian

tax handbook 8th ed., Pymont: Thomson Reuters,

Nethercott, L., Richardson, G. and Devos, K. (2016), Australian Taxation Study

Manual 2016, 4th ed., Sydney: Oxford University Press,

Krever, R. (2017) Australian Taxation Law Cases 2017.2nd ed. Brisbane: THOMSON

LAWBOOK Company,

Reuters, T. (2017) Australian Tax Legislation (2017).4th ed. Sydney.THOMSON

REUTERS,

Woellner, R (2014), Australian taxation law 2014, 7th ed., North Ryde: CCH Australia,

7

Austlii (n.d.) , INCOME TAX ASSESSMENT ACT 1997 - SECT 108.15, [online]

available at http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s108.15.html [Accessed May 28, 2019]

Barkoczy, S. (2018), Foundation of Taxation Law 2018, 9thed.,NorthRyde: CCH

Publications,

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters

(Professional) Australia,

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016), Australian

tax handbook 8th ed., Pymont: Thomson Reuters,

Nethercott, L., Richardson, G. and Devos, K. (2016), Australian Taxation Study

Manual 2016, 4th ed., Sydney: Oxford University Press,

Krever, R. (2017) Australian Taxation Law Cases 2017.2nd ed. Brisbane: THOMSON

LAWBOOK Company,

Reuters, T. (2017) Australian Tax Legislation (2017).4th ed. Sydney.THOMSON

REUTERS,

Woellner, R (2014), Australian taxation law 2014, 7th ed., North Ryde: CCH Australia,

7

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.