HA3042 Taxation Law Assignment: FBT, CGT and Tax Implications

VerifiedAdded on 2023/03/31

|9

|2024

|436

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, focusing on Fringe Benefit Tax (FBT) and Capital Gains Tax (CGT) implications. The first part of the assignment addresses the FBT liability of Spiceco Pty Ltd, calculating depreciation, interest, total operating costs, taxable value (using both cost basis and statutory formula), and the final FBT liability arising from providing a company car to an employee. The second part delves into Capital Gains Tax consequences for Daniel, analyzing the sale of a house, painting, luxury yacht, and shares. The analysis includes determining capital gains or losses, applying relevant CGT rules, and considering the discount method for long-term capital gains and the treatment of capital losses. The assignment covers various aspects of tax law, including relevant sections of the FBTAA 1986 and ITAA 1997, and provides detailed calculations and explanations to support the conclusions.

TAXATION LAW

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

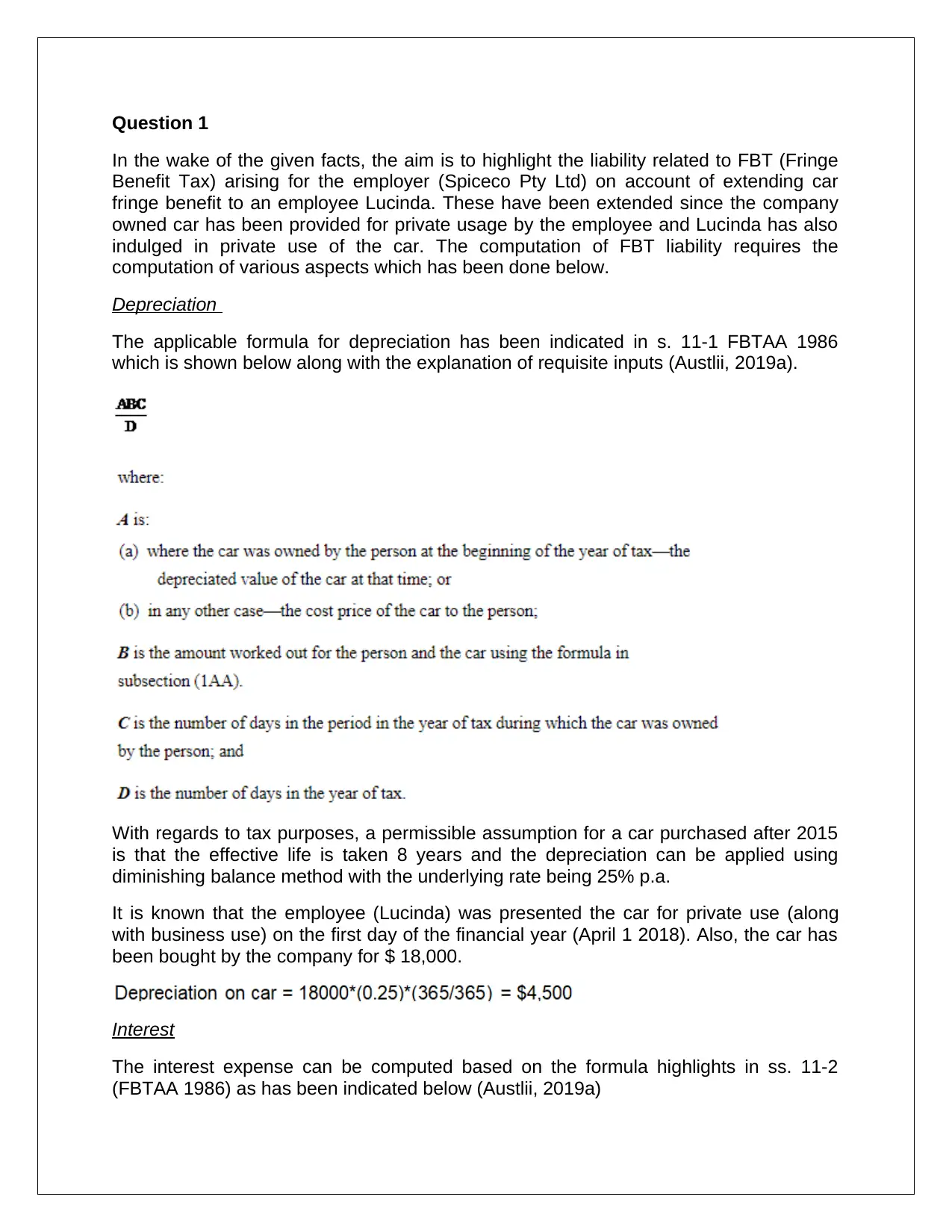

In the wake of the given facts, the aim is to highlight the liability related to FBT (Fringe

Benefit Tax) arising for the employer (Spiceco Pty Ltd) on account of extending car

fringe benefit to an employee Lucinda. These have been extended since the company

owned car has been provided for private usage by the employee and Lucinda has also

indulged in private use of the car. The computation of FBT liability requires the

computation of various aspects which has been done below.

Depreciation

The applicable formula for depreciation has been indicated in s. 11-1 FBTAA 1986

which is shown below along with the explanation of requisite inputs (Austlii, 2019a).

With regards to tax purposes, a permissible assumption for a car purchased after 2015

is that the effective life is taken 8 years and the depreciation can be applied using

diminishing balance method with the underlying rate being 25% p.a.

It is known that the employee (Lucinda) was presented the car for private use (along

with business use) on the first day of the financial year (April 1 2018). Also, the car has

been bought by the company for $ 18,000.

Interest

The interest expense can be computed based on the formula highlights in ss. 11-2

(FBTAA 1986) as has been indicated below (Austlii, 2019a)

In the wake of the given facts, the aim is to highlight the liability related to FBT (Fringe

Benefit Tax) arising for the employer (Spiceco Pty Ltd) on account of extending car

fringe benefit to an employee Lucinda. These have been extended since the company

owned car has been provided for private usage by the employee and Lucinda has also

indulged in private use of the car. The computation of FBT liability requires the

computation of various aspects which has been done below.

Depreciation

The applicable formula for depreciation has been indicated in s. 11-1 FBTAA 1986

which is shown below along with the explanation of requisite inputs (Austlii, 2019a).

With regards to tax purposes, a permissible assumption for a car purchased after 2015

is that the effective life is taken 8 years and the depreciation can be applied using

diminishing balance method with the underlying rate being 25% p.a.

It is known that the employee (Lucinda) was presented the car for private use (along

with business use) on the first day of the financial year (April 1 2018). Also, the car has

been bought by the company for $ 18,000.

Interest

The interest expense can be computed based on the formula highlights in ss. 11-2

(FBTAA 1986) as has been indicated below (Austlii, 2019a)

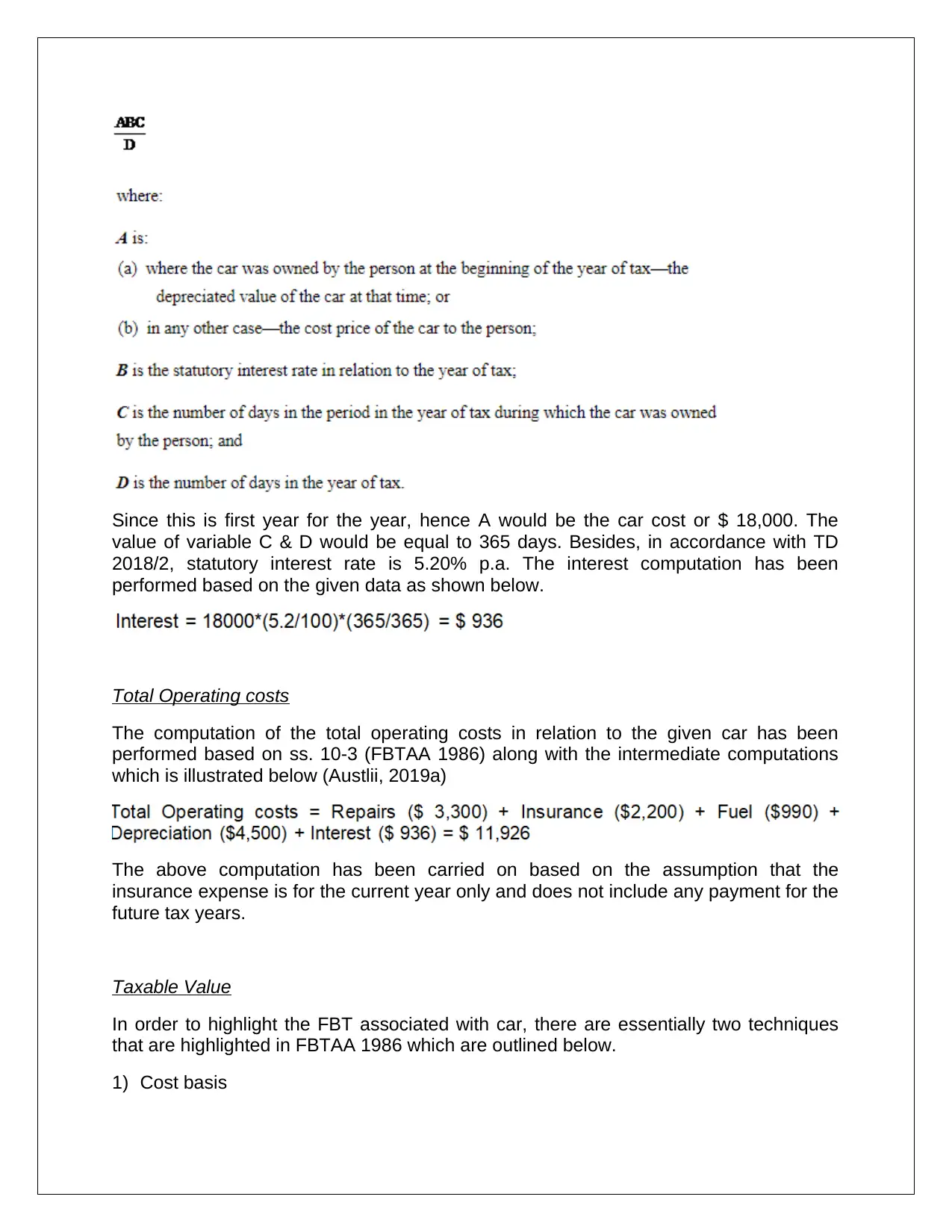

Since this is first year for the year, hence A would be the car cost or $ 18,000. The

value of variable C & D would be equal to 365 days. Besides, in accordance with TD

2018/2, statutory interest rate is 5.20% p.a. The interest computation has been

performed based on the given data as shown below.

Total Operating costs

The computation of the total operating costs in relation to the given car has been

performed based on ss. 10-3 (FBTAA 1986) along with the intermediate computations

which is illustrated below (Austlii, 2019a)

The above computation has been carried on based on the assumption that the

insurance expense is for the current year only and does not include any payment for the

future tax years.

Taxable Value

In order to highlight the FBT associated with car, there are essentially two techniques

that are highlighted in FBTAA 1986 which are outlined below.

1) Cost basis

value of variable C & D would be equal to 365 days. Besides, in accordance with TD

2018/2, statutory interest rate is 5.20% p.a. The interest computation has been

performed based on the given data as shown below.

Total Operating costs

The computation of the total operating costs in relation to the given car has been

performed based on ss. 10-3 (FBTAA 1986) along with the intermediate computations

which is illustrated below (Austlii, 2019a)

The above computation has been carried on based on the assumption that the

insurance expense is for the current year only and does not include any payment for the

future tax years.

Taxable Value

In order to highlight the FBT associated with car, there are essentially two techniques

that are highlighted in FBTAA 1986 which are outlined below.

1) Cost basis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

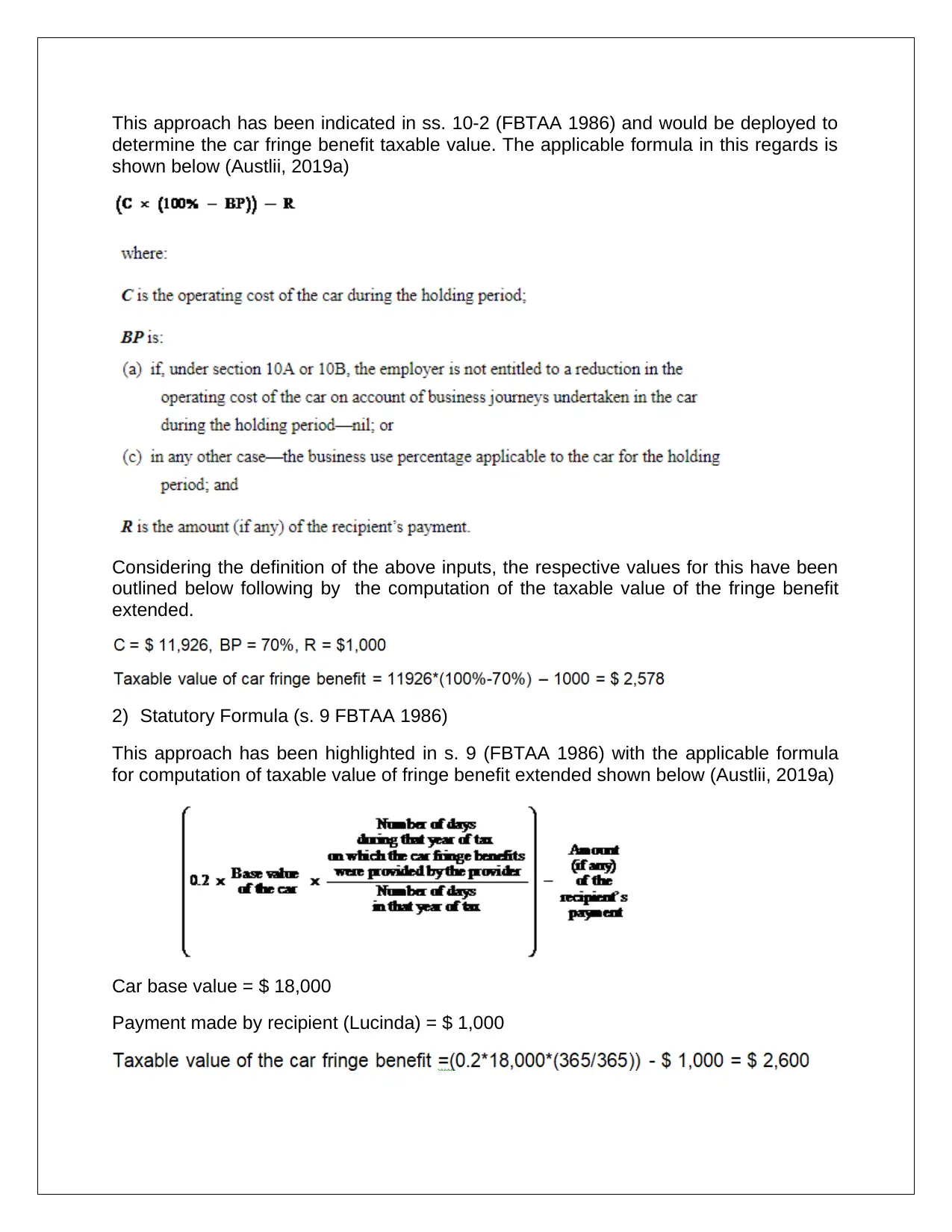

This approach has been indicated in ss. 10-2 (FBTAA 1986) and would be deployed to

determine the car fringe benefit taxable value. The applicable formula in this regards is

shown below (Austlii, 2019a)

Considering the definition of the above inputs, the respective values for this have been

outlined below following by the computation of the taxable value of the fringe benefit

extended.

2) Statutory Formula (s. 9 FBTAA 1986)

This approach has been highlighted in s. 9 (FBTAA 1986) with the applicable formula

for computation of taxable value of fringe benefit extended shown below (Austlii, 2019a)

Car base value = $ 18,000

Payment made by recipient (Lucinda) = $ 1,000

determine the car fringe benefit taxable value. The applicable formula in this regards is

shown below (Austlii, 2019a)

Considering the definition of the above inputs, the respective values for this have been

outlined below following by the computation of the taxable value of the fringe benefit

extended.

2) Statutory Formula (s. 9 FBTAA 1986)

This approach has been highlighted in s. 9 (FBTAA 1986) with the applicable formula

for computation of taxable value of fringe benefit extended shown below (Austlii, 2019a)

Car base value = $ 18,000

Payment made by recipient (Lucinda) = $ 1,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

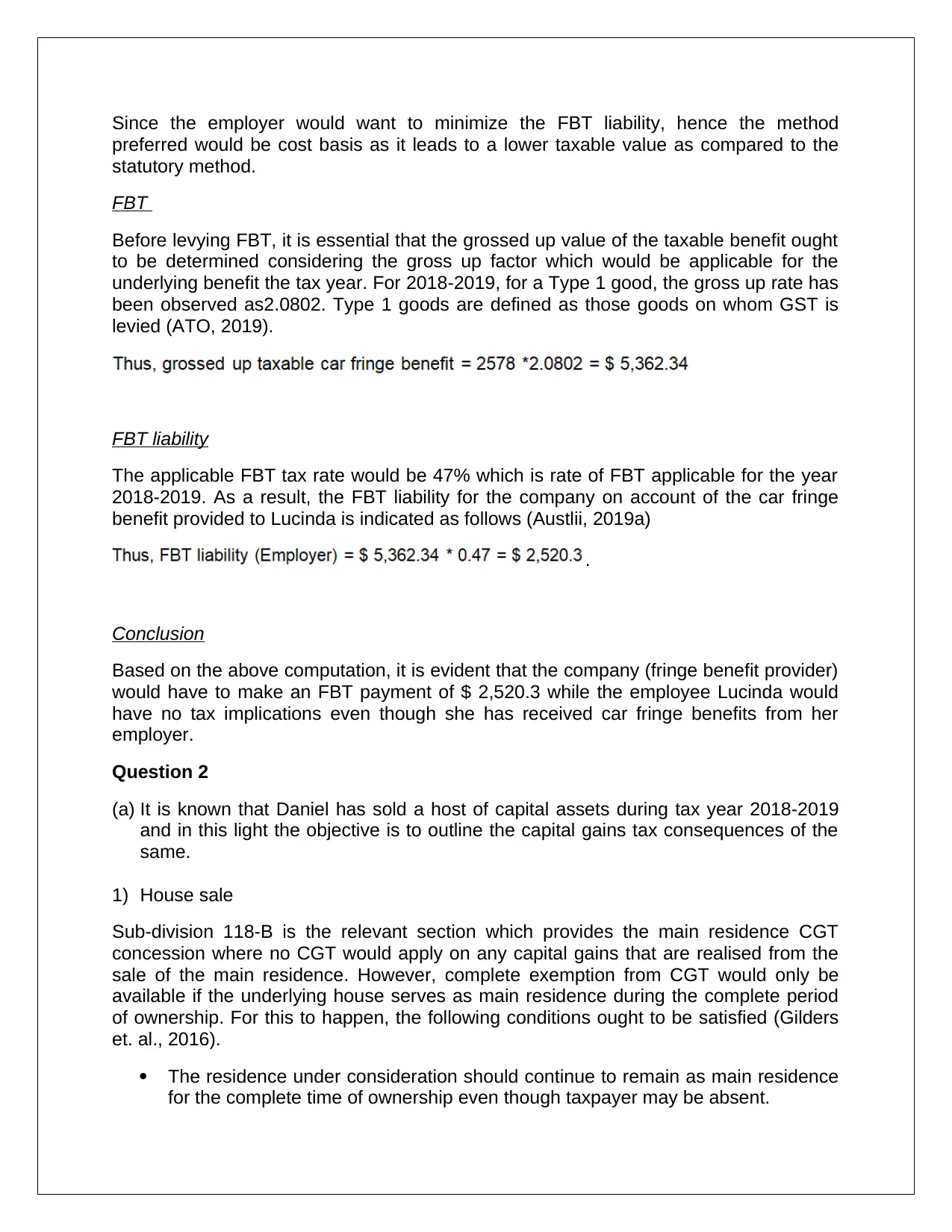

Since the employer would want to minimize the FBT liability, hence the method

preferred would be cost basis as it leads to a lower taxable value as compared to the

statutory method.

FBT

Before levying FBT, it is essential that the grossed up value of the taxable benefit ought

to be determined considering the gross up factor which would be applicable for the

underlying benefit the tax year. For 2018-2019, for a Type 1 good, the gross up rate has

been observed as2.0802. Type 1 goods are defined as those goods on whom GST is

levied (ATO, 2019).

FBT liability

The applicable FBT tax rate would be 47% which is rate of FBT applicable for the year

2018-2019. As a result, the FBT liability for the company on account of the car fringe

benefit provided to Lucinda is indicated as follows (Austlii, 2019a)

.

Conclusion

Based on the above computation, it is evident that the company (fringe benefit provider)

would have to make an FBT payment of $ 2,520.3 while the employee Lucinda would

have no tax implications even though she has received car fringe benefits from her

employer.

Question 2

(a) It is known that Daniel has sold a host of capital assets during tax year 2018-2019

and in this light the objective is to outline the capital gains tax consequences of the

same.

1) House sale

Sub-division 118-B is the relevant section which provides the main residence CGT

concession where no CGT would apply on any capital gains that are realised from the

sale of the main residence. However, complete exemption from CGT would only be

available if the underlying house serves as main residence during the complete period

of ownership. For this to happen, the following conditions ought to be satisfied (Gilders

et. al., 2016).

The residence under consideration should continue to remain as main residence

for the complete time of ownership even though taxpayer may be absent.

preferred would be cost basis as it leads to a lower taxable value as compared to the

statutory method.

FBT

Before levying FBT, it is essential that the grossed up value of the taxable benefit ought

to be determined considering the gross up factor which would be applicable for the

underlying benefit the tax year. For 2018-2019, for a Type 1 good, the gross up rate has

been observed as2.0802. Type 1 goods are defined as those goods on whom GST is

levied (ATO, 2019).

FBT liability

The applicable FBT tax rate would be 47% which is rate of FBT applicable for the year

2018-2019. As a result, the FBT liability for the company on account of the car fringe

benefit provided to Lucinda is indicated as follows (Austlii, 2019a)

.

Conclusion

Based on the above computation, it is evident that the company (fringe benefit provider)

would have to make an FBT payment of $ 2,520.3 while the employee Lucinda would

have no tax implications even though she has received car fringe benefits from her

employer.

Question 2

(a) It is known that Daniel has sold a host of capital assets during tax year 2018-2019

and in this light the objective is to outline the capital gains tax consequences of the

same.

1) House sale

Sub-division 118-B is the relevant section which provides the main residence CGT

concession where no CGT would apply on any capital gains that are realised from the

sale of the main residence. However, complete exemption from CGT would only be

available if the underlying house serves as main residence during the complete period

of ownership. For this to happen, the following conditions ought to be satisfied (Gilders

et. al., 2016).

The residence under consideration should continue to remain as main residence

for the complete time of ownership even though taxpayer may be absent.

No assessable income has been produced from the house.

For the house sold by Daniel, it would be fair to categorise this has main residence

since for the complete ownership period, Daniel has resided in the house and has not

used the same for earning any assessable income. Hence, any capital gains realised

from the sale of the house would not attract any CGT. In relation to the advance of $

85,000 made by the previous buyer, the same would also be capital gains related to the

house which would be discarded for CGT purpose (Nethercott, Richardson and Devos,

2016).

2) Painting Sale

The painting as a asset belongs to a specific asset class known as collectibles which is

outlined in ss. 108-10 ITAA 1997. Considering that these assets are CGT assets, hence

the sale of this asset would lead to A1 CGT event as per ss. 104-5 ITAA 1997. Owing to

this event, there is a need to determine the capital gains/(losses) as per the formula

stated in ss. 104-10 ITAA 1997. This is illustrated as follows (CCH, 2013).

With regards to application of CGT, it is noteworthy that the current CGT regime came

on force on September 20, 1985 and hence any capital assets which the taxpayers

purchased before this date are termed as pre-CGT assets as indicated in ss. 149-10

ITAA 1997. This classification becomes vital considering that any capital gains are

exempt from CGT in case of pre-CGT asset (Deutsch et. al., 2016).

The painting has been purchased on the cutoff date (I,e, September 20, 1985) and

hence is not a CGT exempt asset. Thereby, using the information provided, the capital

gains realised by Daniel on the sale of painting has been computed below.

Sale price = $ 125,000

Price of purchase = $ 15,000

It is critical to note that all the above capital gains would not be taxable. This is because

relief in taxable amount would be provided under the discount method (s. 115-25

ITAA1997) as per which a 50% rebate is available for individual payments when the

capital gains are long term. These capital gains arise on assets whose holding period

for the taxpayer is atleast one year (Austlii, 2019b).

3) Luxury yacht sale

The relevant facts clearly indicate that the yacht that has been sold was not used to

derive business income but essentially was meant for personal enjoyment and usage.

Thus, in accordance with ss. 108-20(2), the given asset would be termed as an asset

for personal use (Nethercott, Richardson and Devos, 2016). In regards to this particular

For the house sold by Daniel, it would be fair to categorise this has main residence

since for the complete ownership period, Daniel has resided in the house and has not

used the same for earning any assessable income. Hence, any capital gains realised

from the sale of the house would not attract any CGT. In relation to the advance of $

85,000 made by the previous buyer, the same would also be capital gains related to the

house which would be discarded for CGT purpose (Nethercott, Richardson and Devos,

2016).

2) Painting Sale

The painting as a asset belongs to a specific asset class known as collectibles which is

outlined in ss. 108-10 ITAA 1997. Considering that these assets are CGT assets, hence

the sale of this asset would lead to A1 CGT event as per ss. 104-5 ITAA 1997. Owing to

this event, there is a need to determine the capital gains/(losses) as per the formula

stated in ss. 104-10 ITAA 1997. This is illustrated as follows (CCH, 2013).

With regards to application of CGT, it is noteworthy that the current CGT regime came

on force on September 20, 1985 and hence any capital assets which the taxpayers

purchased before this date are termed as pre-CGT assets as indicated in ss. 149-10

ITAA 1997. This classification becomes vital considering that any capital gains are

exempt from CGT in case of pre-CGT asset (Deutsch et. al., 2016).

The painting has been purchased on the cutoff date (I,e, September 20, 1985) and

hence is not a CGT exempt asset. Thereby, using the information provided, the capital

gains realised by Daniel on the sale of painting has been computed below.

Sale price = $ 125,000

Price of purchase = $ 15,000

It is critical to note that all the above capital gains would not be taxable. This is because

relief in taxable amount would be provided under the discount method (s. 115-25

ITAA1997) as per which a 50% rebate is available for individual payments when the

capital gains are long term. These capital gains arise on assets whose holding period

for the taxpayer is atleast one year (Austlii, 2019b).

3) Luxury yacht sale

The relevant facts clearly indicate that the yacht that has been sold was not used to

derive business income but essentially was meant for personal enjoyment and usage.

Thus, in accordance with ss. 108-20(2), the given asset would be termed as an asset

for personal use (Nethercott, Richardson and Devos, 2016). In regards to this particular

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

asset, certain special rules with regards to capital gains/(loss) treatment tend to arise.

For these assets, the capital gains would be taxable under CGT regime only if the cost

base of the asset is higher than $ 10,000. Additionally, ss. 108-20 ITAA 1997 clearly

highlights that any losses made on these assets is discarded from the CGT perspective

without any adjustment or offsetting available (Barkoczy, 2018).

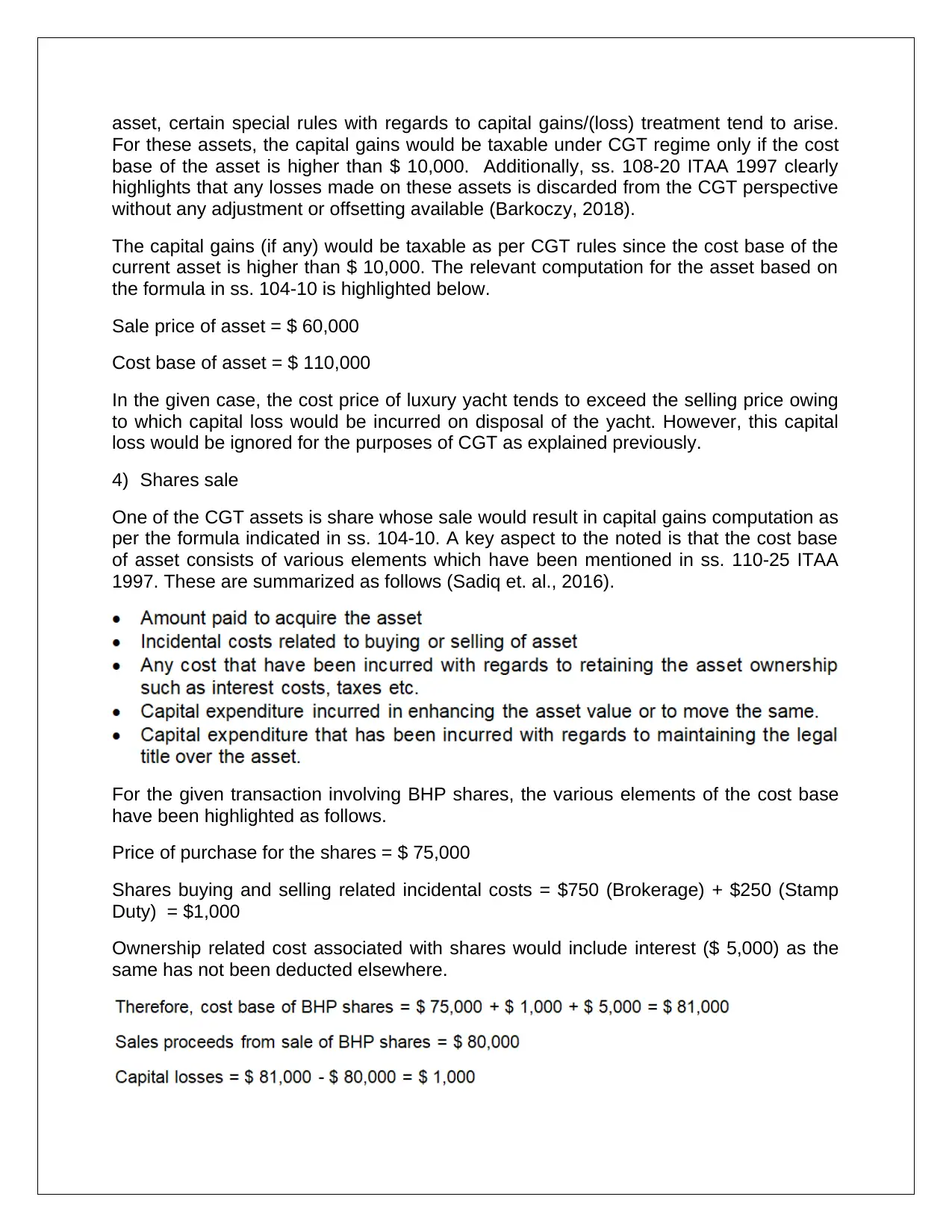

The capital gains (if any) would be taxable as per CGT rules since the cost base of the

current asset is higher than $ 10,000. The relevant computation for the asset based on

the formula in ss. 104-10 is highlighted below.

Sale price of asset = $ 60,000

Cost base of asset = $ 110,000

In the given case, the cost price of luxury yacht tends to exceed the selling price owing

to which capital loss would be incurred on disposal of the yacht. However, this capital

loss would be ignored for the purposes of CGT as explained previously.

4) Shares sale

One of the CGT assets is share whose sale would result in capital gains computation as

per the formula indicated in ss. 104-10. A key aspect to the noted is that the cost base

of asset consists of various elements which have been mentioned in ss. 110-25 ITAA

1997. These are summarized as follows (Sadiq et. al., 2016).

For the given transaction involving BHP shares, the various elements of the cost base

have been highlighted as follows.

Price of purchase for the shares = $ 75,000

Shares buying and selling related incidental costs = $750 (Brokerage) + $250 (Stamp

Duty) = $1,000

Ownership related cost associated with shares would include interest ($ 5,000) as the

same has not been deducted elsewhere.

For these assets, the capital gains would be taxable under CGT regime only if the cost

base of the asset is higher than $ 10,000. Additionally, ss. 108-20 ITAA 1997 clearly

highlights that any losses made on these assets is discarded from the CGT perspective

without any adjustment or offsetting available (Barkoczy, 2018).

The capital gains (if any) would be taxable as per CGT rules since the cost base of the

current asset is higher than $ 10,000. The relevant computation for the asset based on

the formula in ss. 104-10 is highlighted below.

Sale price of asset = $ 60,000

Cost base of asset = $ 110,000

In the given case, the cost price of luxury yacht tends to exceed the selling price owing

to which capital loss would be incurred on disposal of the yacht. However, this capital

loss would be ignored for the purposes of CGT as explained previously.

4) Shares sale

One of the CGT assets is share whose sale would result in capital gains computation as

per the formula indicated in ss. 104-10. A key aspect to the noted is that the cost base

of asset consists of various elements which have been mentioned in ss. 110-25 ITAA

1997. These are summarized as follows (Sadiq et. al., 2016).

For the given transaction involving BHP shares, the various elements of the cost base

have been highlighted as follows.

Price of purchase for the shares = $ 75,000

Shares buying and selling related incidental costs = $750 (Brokerage) + $250 (Stamp

Duty) = $1,000

Ownership related cost associated with shares would include interest ($ 5,000) as the

same has not been deducted elsewhere.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

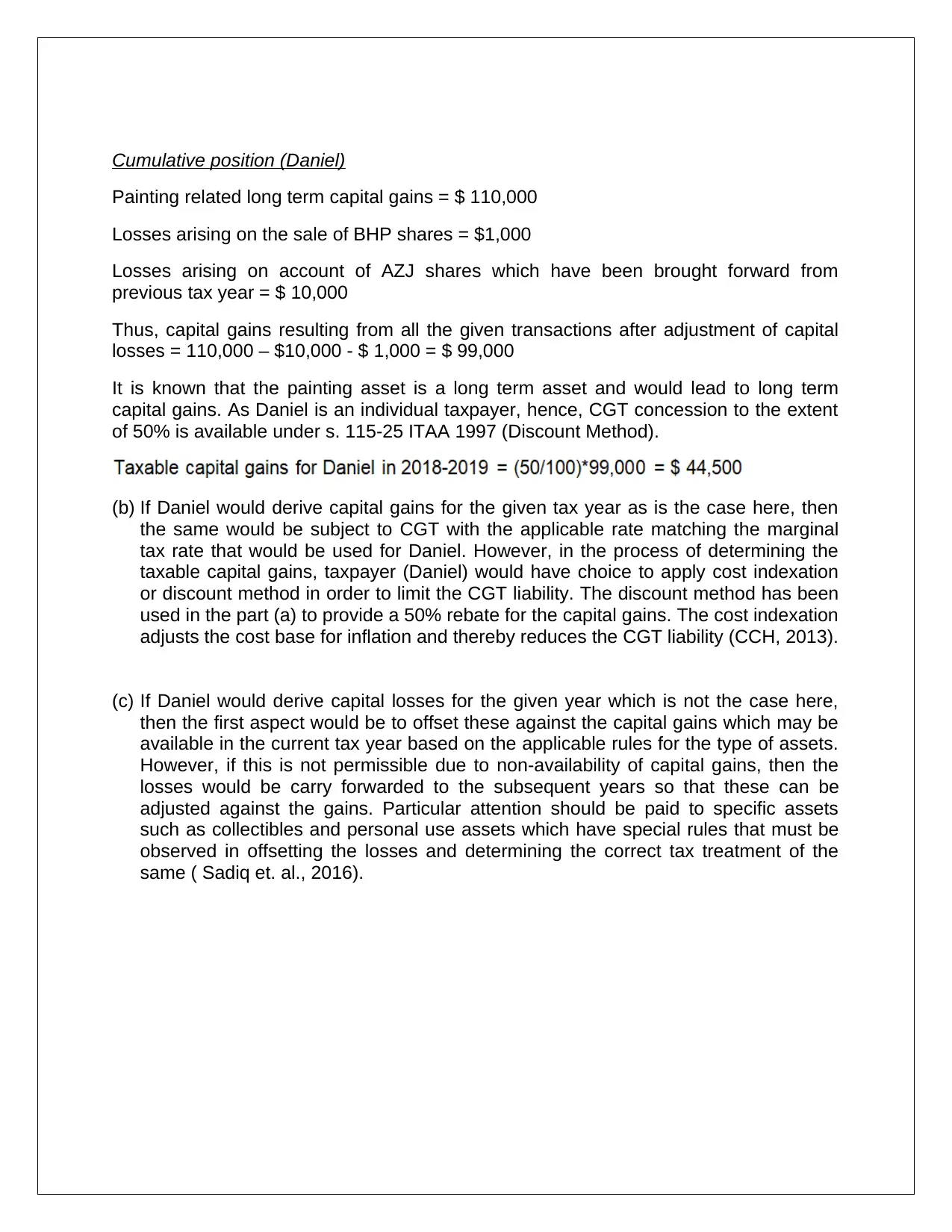

Cumulative position (Daniel)

Painting related long term capital gains = $ 110,000

Losses arising on the sale of BHP shares = $1,000

Losses arising on account of AZJ shares which have been brought forward from

previous tax year = $ 10,000

Thus, capital gains resulting from all the given transactions after adjustment of capital

losses = 110,000 – $10,000 - $ 1,000 = $ 99,000

It is known that the painting asset is a long term asset and would lead to long term

capital gains. As Daniel is an individual taxpayer, hence, CGT concession to the extent

of 50% is available under s. 115-25 ITAA 1997 (Discount Method).

(b) If Daniel would derive capital gains for the given tax year as is the case here, then

the same would be subject to CGT with the applicable rate matching the marginal

tax rate that would be used for Daniel. However, in the process of determining the

taxable capital gains, taxpayer (Daniel) would have choice to apply cost indexation

or discount method in order to limit the CGT liability. The discount method has been

used in the part (a) to provide a 50% rebate for the capital gains. The cost indexation

adjusts the cost base for inflation and thereby reduces the CGT liability (CCH, 2013).

(c) If Daniel would derive capital losses for the given year which is not the case here,

then the first aspect would be to offset these against the capital gains which may be

available in the current tax year based on the applicable rules for the type of assets.

However, if this is not permissible due to non-availability of capital gains, then the

losses would be carry forwarded to the subsequent years so that these can be

adjusted against the gains. Particular attention should be paid to specific assets

such as collectibles and personal use assets which have special rules that must be

observed in offsetting the losses and determining the correct tax treatment of the

same ( Sadiq et. al., 2016).

Painting related long term capital gains = $ 110,000

Losses arising on the sale of BHP shares = $1,000

Losses arising on account of AZJ shares which have been brought forward from

previous tax year = $ 10,000

Thus, capital gains resulting from all the given transactions after adjustment of capital

losses = 110,000 – $10,000 - $ 1,000 = $ 99,000

It is known that the painting asset is a long term asset and would lead to long term

capital gains. As Daniel is an individual taxpayer, hence, CGT concession to the extent

of 50% is available under s. 115-25 ITAA 1997 (Discount Method).

(b) If Daniel would derive capital gains for the given tax year as is the case here, then

the same would be subject to CGT with the applicable rate matching the marginal

tax rate that would be used for Daniel. However, in the process of determining the

taxable capital gains, taxpayer (Daniel) would have choice to apply cost indexation

or discount method in order to limit the CGT liability. The discount method has been

used in the part (a) to provide a 50% rebate for the capital gains. The cost indexation

adjusts the cost base for inflation and thereby reduces the CGT liability (CCH, 2013).

(c) If Daniel would derive capital losses for the given year which is not the case here,

then the first aspect would be to offset these against the capital gains which may be

available in the current tax year based on the applicable rules for the type of assets.

However, if this is not permissible due to non-availability of capital gains, then the

losses would be carry forwarded to the subsequent years so that these can be

adjusted against the gains. Particular attention should be paid to specific assets

such as collectibles and personal use assets which have special rules that must be

observed in offsetting the losses and determining the correct tax treatment of the

same ( Sadiq et. al., 2016).

References

ATO (2019) Fringe benefits tax – rates and thresholds, [online] Available at

https://www.ato.gov.au/Rates/FBT/ [Assessed May 31, 2019]

Austlii (2019a) FRINGE BENEFITS TAX ASSESSMENT ACT 1986, [online] Available at

http://classic.austlii.edu.au/au/legis/cth/consol_act/fbtaa1986312/ [Assessed May 31,

2019]

Austlii (2019b) INCOME TAX ASSESSMENT ACT 1997 - SECT 115.25, [online]

Available at http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s115.25.html [Assessed May 31, 2019]

Barkoczy, S. (2018), Foundation of Taxation Law 2018, 9thed.,NorthRyde: CCH

Publications,

CCH (2013), Australian Master Tax Guide 2013, 51st ed., Sydney: Wolters Kluwer,

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016), Australian tax

handbook 8th ed., Pymont: Thomson Reuters,

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016), Understanding

taxation law 2016, 9th ed., Sydney: LexisNexis/Butterworths,

Nethercott, L., Richardson, G. and Devos, K. (2016), Australian Taxation Study Manual

2016, 4th ed., Sydney: Oxford University Press,

Sadiq, K, Coleman, C, Hanegbi, R, Jogarajan, S, Krever, R, Obst, W, and Ting, A

(2016) , Principles of Taxation Law 2016, 8th ed., Pymont:Thomson Reuters,

ATO (2019) Fringe benefits tax – rates and thresholds, [online] Available at

https://www.ato.gov.au/Rates/FBT/ [Assessed May 31, 2019]

Austlii (2019a) FRINGE BENEFITS TAX ASSESSMENT ACT 1986, [online] Available at

http://classic.austlii.edu.au/au/legis/cth/consol_act/fbtaa1986312/ [Assessed May 31,

2019]

Austlii (2019b) INCOME TAX ASSESSMENT ACT 1997 - SECT 115.25, [online]

Available at http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s115.25.html [Assessed May 31, 2019]

Barkoczy, S. (2018), Foundation of Taxation Law 2018, 9thed.,NorthRyde: CCH

Publications,

CCH (2013), Australian Master Tax Guide 2013, 51st ed., Sydney: Wolters Kluwer,

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016), Australian tax

handbook 8th ed., Pymont: Thomson Reuters,

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016), Understanding

taxation law 2016, 9th ed., Sydney: LexisNexis/Butterworths,

Nethercott, L., Richardson, G. and Devos, K. (2016), Australian Taxation Study Manual

2016, 4th ed., Sydney: Oxford University Press,

Sadiq, K, Coleman, C, Hanegbi, R, Jogarajan, S, Krever, R, Obst, W, and Ting, A

(2016) , Principles of Taxation Law 2016, 8th ed., Pymont:Thomson Reuters,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9