Taxation Law Assignment: CGT, Income from Personal Exertion, Loans

VerifiedAdded on 2023/01/18

|7

|2678

|39

Homework Assignment

AI Summary

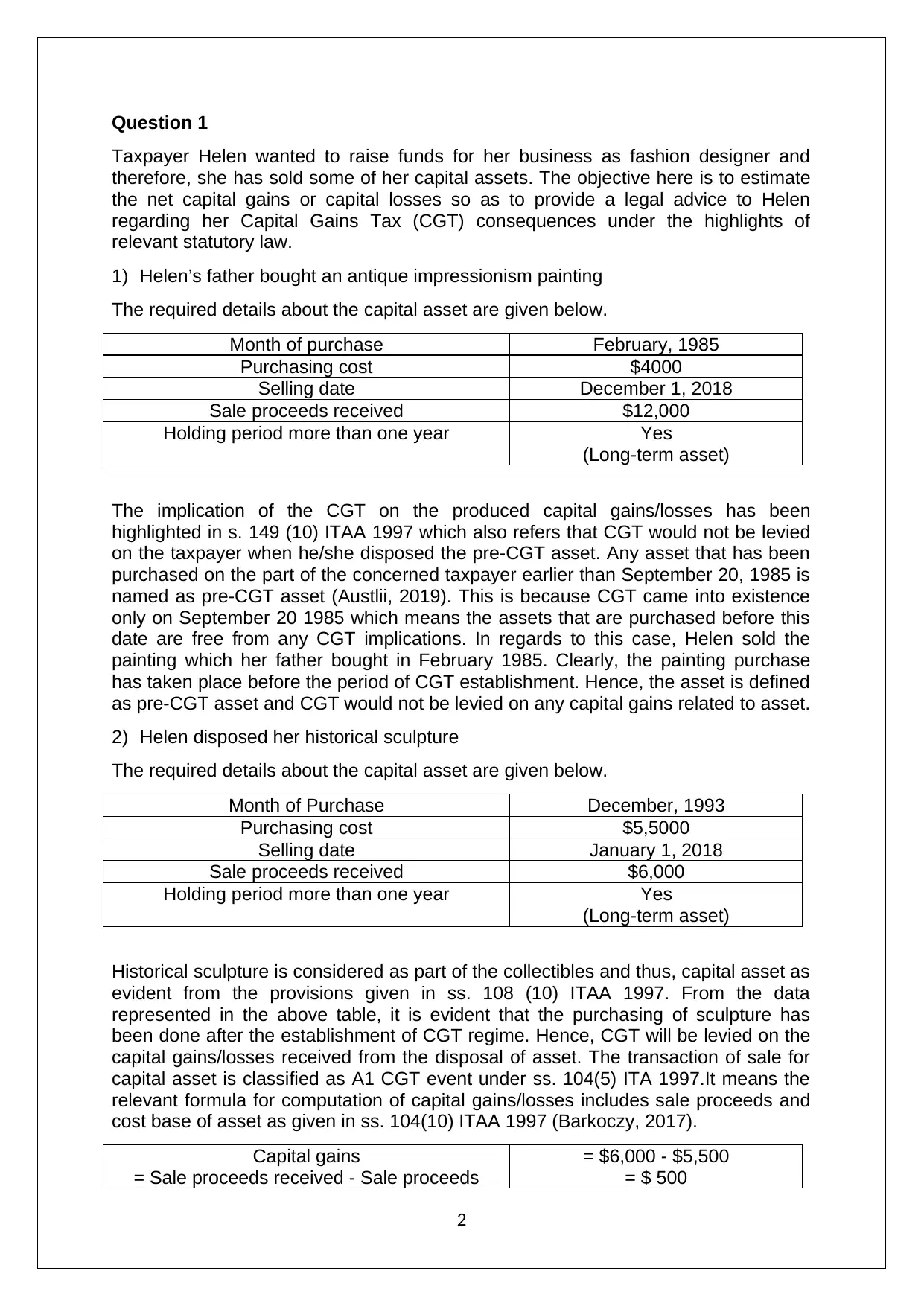

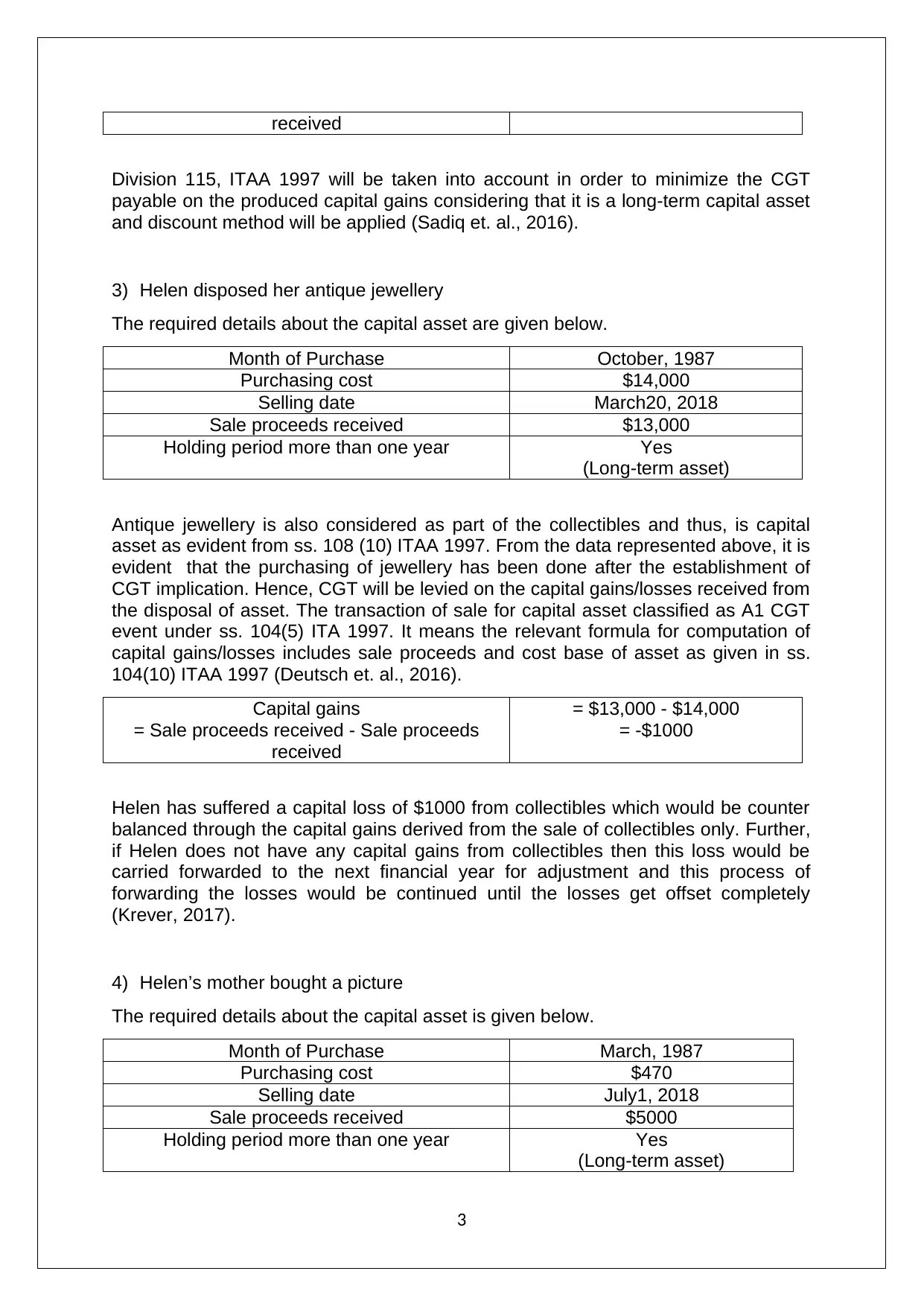

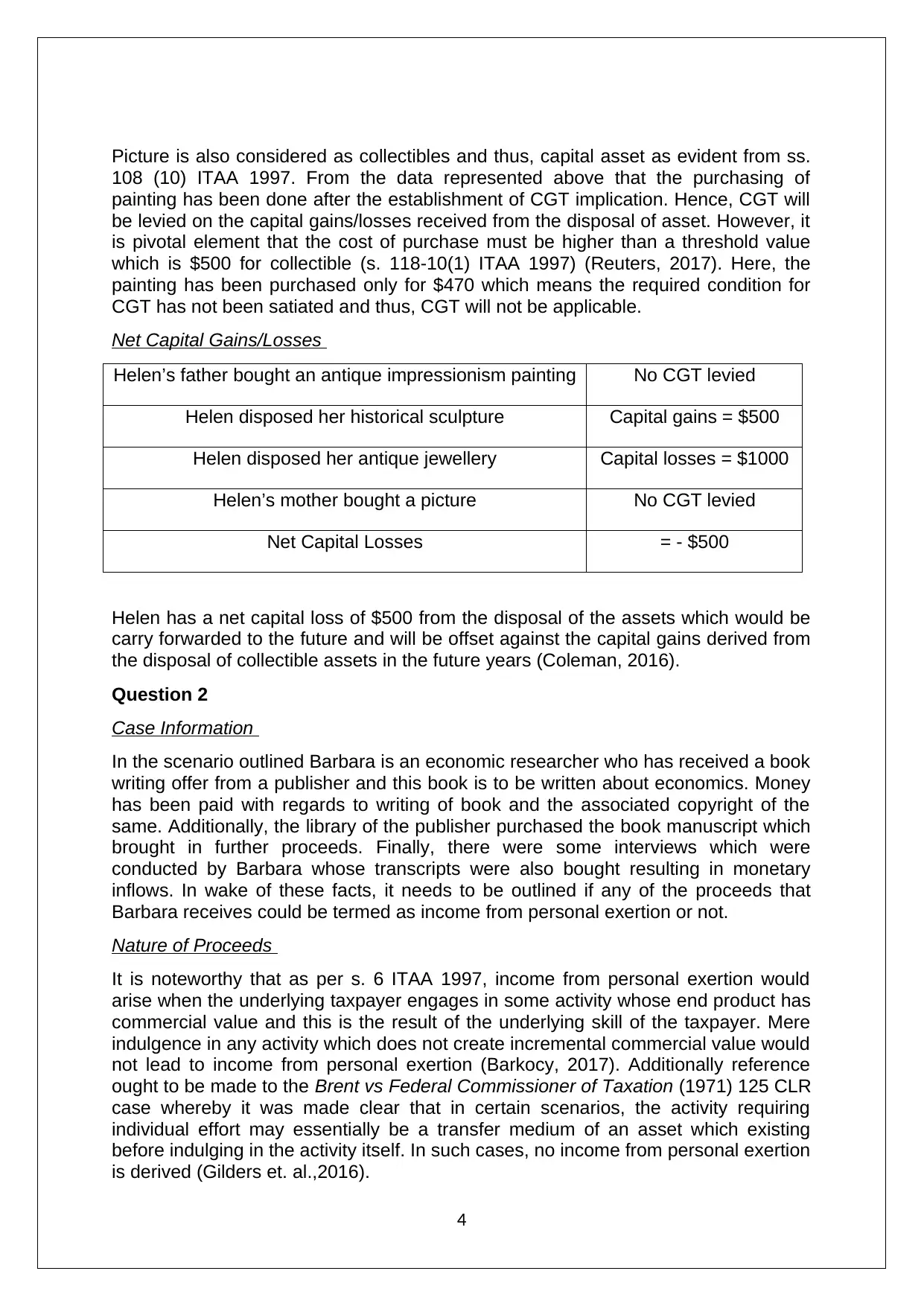

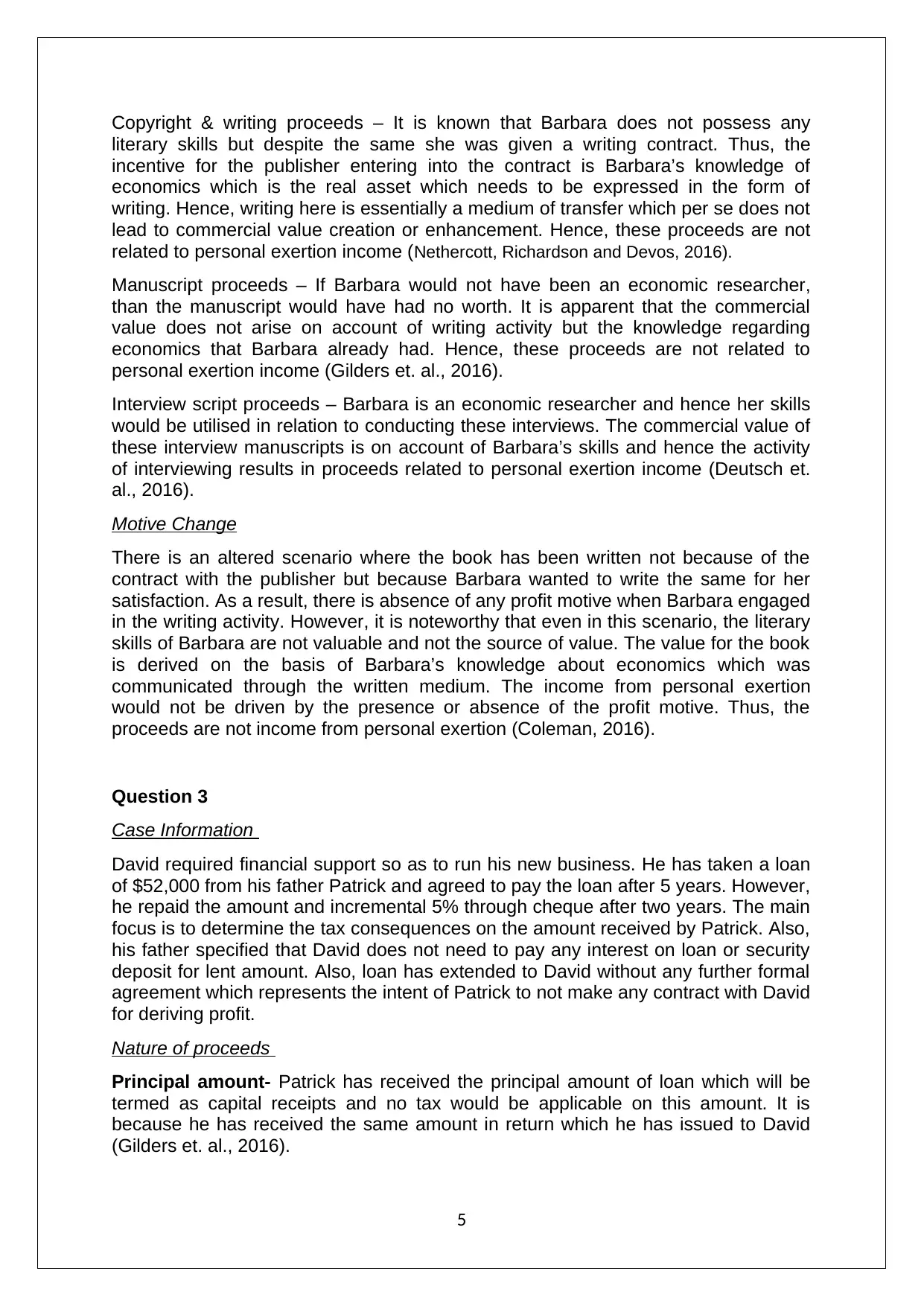

This document provides a comprehensive solution to a taxation law assignment, addressing three key questions. Question 1 analyzes the capital gains tax (CGT) implications for a fashion designer, Helen, who sold various assets, including a pre-CGT painting, a historical sculpture, antique jewelry, and a picture. The analysis determines CGT liabilities based on purchase and sale dates, cost bases, and relevant legislation. Question 2 examines whether proceeds received by an economic researcher, Barbara, from writing a book, manuscript sales, and interview transcripts constitute income from personal exertion, considering factors like the source of value and profit motive. Question 3 explores the tax consequences for David and his father Patrick, involving a loan provided by Patrick to David and the subsequent repayment with interest. The analysis determines whether the interest received by Patrick is assessable income or non-assessable income, considering the nature of the loan and the absence of a money-lending business or profit motive. The solution incorporates relevant Australian tax law, including ITAA 1997 sections and case law, to provide a detailed and legally sound analysis of each scenario.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.