Taxation and Residency for Jack Jones

VerifiedAdded on 2020/10/04

|7

|1672

|33

AI Summary

This assignment involves applying tax legislation to determine the taxable income of Jack Jones, a Canadian resident, for the year ended June 30, 2016. It requires consideration of section 6 of the Income Tax Assessment Act (1936) and the 180-days test to establish residency status. The assignment also involves identifying allowable deductions and taxable expenses, resulting in a total taxable income of $250,900.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Taxation Law

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Advising Jack about his residency status.....................................................................................3

Calculating taxable income of Jack for the year ended on 30 June 2016....................................5

CONCLUSION................................................................................................................................6

INTRODUCTION...........................................................................................................................3

Advising Jack about his residency status.....................................................................................3

Calculating taxable income of Jack for the year ended on 30 June 2016....................................5

CONCLUSION................................................................................................................................6

INTRODUCTION

Taxation may be served as a way through which government authorities’ finances their

expenditure through imposing charges on citizens. With the motive to encourage or discourage

certain economic decisions government use taxation as a tool. For this purpose ITAA 1936 has

been introduced which in turn clearly entails the rules and regulations that helps individuals in

determining their tax liability or obligations. The present report is based on the case situation of

Jack which will provide deeper insight about the conditions needs to fulfill for showing the

residency status. Besides this, it also depicts the extent to which Jack is liable to pay tax in

against to the income earned during the financial year.

Advising Jack about his residency status

Issue: On the basis of cited case situation, the main issue is to assess the residency status

of Jack. Moreover, as per the given case Jack Jones hold a Canadian passport as well as visa

which allows him to work in Australia from 2 December 2012 to 30th June 2016. Further, within

visa period Jack had done contract with Peterson Marine Industries Pty Ltd, an Australian

company. Hence, after some time period on 1st August 2015 Jack left America and started to

work in Canada. Given case situation clearly presents that approximately 9 months from August

2015 to April 2016 Jack worked in Canada. Thereafter, he returned to Australia for the rest of

income tax year ended on June 2016. Thus, as per the movement of Jack from Australia to

Canada and vice versa the main issue is to ascertain the residency status of Jack from the purpose

of taxation.

Laws: In order to resolve the concerned issue section and case law pertaining to

residential status has been considered. Section 6 and 183 day test as per ITAA (1936) has been

applied. Further, case law of FC of T v Jenkins82 ATC 4098 has also undertaken to determine

the extent to which Jack is considered as an Australian resident for tax purpose1.

Application: From assessment, it has been identified that if an individual actually present

in Australia more than 6 months of financial whether continuously or in breaks. Thus, individual

1 Income tax: residency - permanent place of abode outside Australia

Taxation may be served as a way through which government authorities’ finances their

expenditure through imposing charges on citizens. With the motive to encourage or discourage

certain economic decisions government use taxation as a tool. For this purpose ITAA 1936 has

been introduced which in turn clearly entails the rules and regulations that helps individuals in

determining their tax liability or obligations. The present report is based on the case situation of

Jack which will provide deeper insight about the conditions needs to fulfill for showing the

residency status. Besides this, it also depicts the extent to which Jack is liable to pay tax in

against to the income earned during the financial year.

Advising Jack about his residency status

Issue: On the basis of cited case situation, the main issue is to assess the residency status

of Jack. Moreover, as per the given case Jack Jones hold a Canadian passport as well as visa

which allows him to work in Australia from 2 December 2012 to 30th June 2016. Further, within

visa period Jack had done contract with Peterson Marine Industries Pty Ltd, an Australian

company. Hence, after some time period on 1st August 2015 Jack left America and started to

work in Canada. Given case situation clearly presents that approximately 9 months from August

2015 to April 2016 Jack worked in Canada. Thereafter, he returned to Australia for the rest of

income tax year ended on June 2016. Thus, as per the movement of Jack from Australia to

Canada and vice versa the main issue is to ascertain the residency status of Jack from the purpose

of taxation.

Laws: In order to resolve the concerned issue section and case law pertaining to

residential status has been considered. Section 6 and 183 day test as per ITAA (1936) has been

applied. Further, case law of FC of T v Jenkins82 ATC 4098 has also undertaken to determine

the extent to which Jack is considered as an Australian resident for tax purpose1.

Application: From assessment, it has been identified that if an individual actually present

in Australia more than 6 months of financial whether continuously or in breaks. Thus, individual

1 Income tax: residency - permanent place of abode outside Australia

who completed 183 days in Australia considered as resident. Along with this, there is a condition

that place of adobe of the candidate is outside Australia and having no intention to taking up

residence there. In the cited case such aspect is applied to a great extent because place of adobe

of Jack is Australia. Further, as per 183-residency test Jack considered an Australian resident for

the purpose of tax pertaining to the financial years 2012-13, 2013-14 and 2014-15. Moreover,

during such periods Jack Jones spent more than 6 years. Thus, Jack Jones obliged to fulfill tax

liability in against to the income generated during such periods. However, in the financial year

2015-16, Jack Jones worked for only 3 years in Australia (Residency – the resides test, 2017). By

considering this, it can be stated that for the financial year 2015-16 Jack Jones was not

considered as an Australian resident. In addition to this, case of FC of T v Jenkins82 ATC 4098

clearly entails that IT 2650 furnishes information about whether or not a taxpayer has a

permanent place of adobe outside Australia or not (King, 2016). In this case, commissioner

presented that at the time of determining residential status following factors need to be

considered:

183-days test2

Intention and time-period of an individual in relation to staying in overseas country

Having intention in relation to returning in Australia or travelling in another country

Durability of association: This aspect can be assessed or evaluated through the aspects

such as maintaining bank accounts in Australia

Presented case summary of Jack Jones clearly presents that he had bank account in Australia

which in turn shows the level of association. Along with this, commissioner said that an

individual is a resident of Australia if the concerned one has actually been in Australia during

more than one-half of the year of income. Further, as per section 6 (1) (a) (ii) commissioner

satisfaction is highly required that place of adobe of individual is outside Australia and the he has

no intention to take up residence in Australia (Reinhardt & Steel, 2016). Thus, by taking into

account the case laws and section 6 (1) it can be stated that Jack Jones is resident for taxation

purpose pertaining to financial year 2012-13, 14 & 15.

Conclusion: It can be concluded from overall evaluation that in the year of 2013, 2014 and

2015 Jack Jones was resided in Australia more than 6 months. Further, it can be seen in the

2 Residency test

that place of adobe of the candidate is outside Australia and having no intention to taking up

residence there. In the cited case such aspect is applied to a great extent because place of adobe

of Jack is Australia. Further, as per 183-residency test Jack considered an Australian resident for

the purpose of tax pertaining to the financial years 2012-13, 2013-14 and 2014-15. Moreover,

during such periods Jack Jones spent more than 6 years. Thus, Jack Jones obliged to fulfill tax

liability in against to the income generated during such periods. However, in the financial year

2015-16, Jack Jones worked for only 3 years in Australia (Residency – the resides test, 2017). By

considering this, it can be stated that for the financial year 2015-16 Jack Jones was not

considered as an Australian resident. In addition to this, case of FC of T v Jenkins82 ATC 4098

clearly entails that IT 2650 furnishes information about whether or not a taxpayer has a

permanent place of adobe outside Australia or not (King, 2016). In this case, commissioner

presented that at the time of determining residential status following factors need to be

considered:

183-days test2

Intention and time-period of an individual in relation to staying in overseas country

Having intention in relation to returning in Australia or travelling in another country

Durability of association: This aspect can be assessed or evaluated through the aspects

such as maintaining bank accounts in Australia

Presented case summary of Jack Jones clearly presents that he had bank account in Australia

which in turn shows the level of association. Along with this, commissioner said that an

individual is a resident of Australia if the concerned one has actually been in Australia during

more than one-half of the year of income. Further, as per section 6 (1) (a) (ii) commissioner

satisfaction is highly required that place of adobe of individual is outside Australia and the he has

no intention to take up residence in Australia (Reinhardt & Steel, 2016). Thus, by taking into

account the case laws and section 6 (1) it can be stated that Jack Jones is resident for taxation

purpose pertaining to financial year 2012-13, 14 & 15.

Conclusion: It can be concluded from overall evaluation that in the year of 2013, 2014 and

2015 Jack Jones was resided in Australia more than 6 months. Further, it can be seen in the

2 Residency test

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

report that during the income year ended on June 2016 Jack was in Australia for only 3 months.

By considering this, it can be presented that as per Sec 6 and 180 days – resident test referring

ITAA (1936) Jack was not recognized as an Australian resident for the purpose of taxation.

Calculating taxable income of Jack for the year ended on 30 June 2016

Issue: In accordance with the given case situation Jack Jones is considered as an

Australian resident for tax purpose. Thus, in this, main issue is to assess the taxable income of

him related to income tax year ended on 30th June 2016.

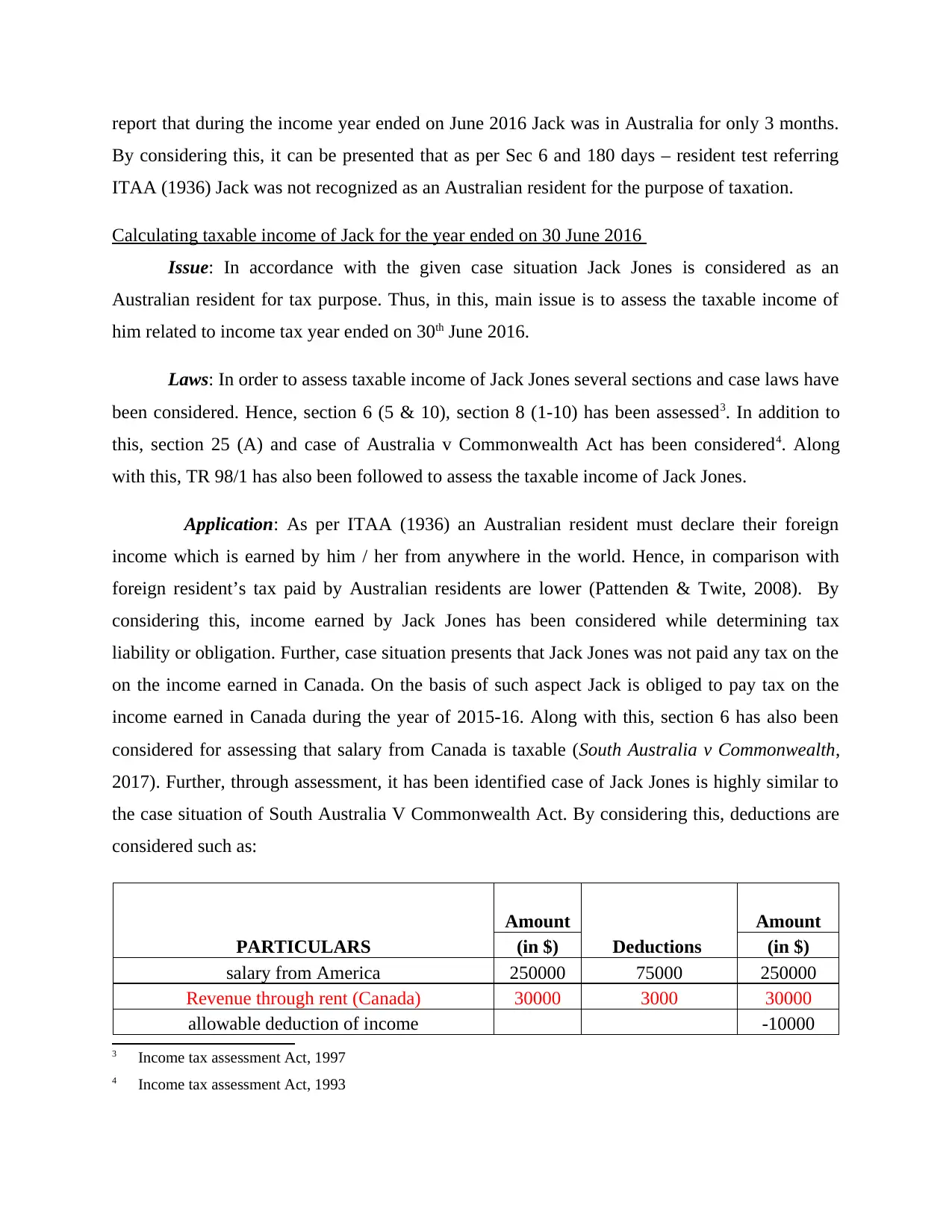

Laws: In order to assess taxable income of Jack Jones several sections and case laws have

been considered. Hence, section 6 (5 & 10), section 8 (1-10) has been assessed3. In addition to

this, section 25 (A) and case of Australia v Commonwealth Act has been considered4. Along

with this, TR 98/1 has also been followed to assess the taxable income of Jack Jones.

Application: As per ITAA (1936) an Australian resident must declare their foreign

income which is earned by him / her from anywhere in the world. Hence, in comparison with

foreign resident’s tax paid by Australian residents are lower (Pattenden & Twite, 2008). By

considering this, income earned by Jack Jones has been considered while determining tax

liability or obligation. Further, case situation presents that Jack Jones was not paid any tax on the

on the income earned in Canada. On the basis of such aspect Jack is obliged to pay tax on the

income earned in Canada during the year of 2015-16. Along with this, section 6 has also been

considered for assessing that salary from Canada is taxable (South Australia v Commonwealth,

2017). Further, through assessment, it has been identified case of Jack Jones is highly similar to

the case situation of South Australia V Commonwealth Act. By considering this, deductions are

considered such as:

PARTICULARS

Amount

Deductions

Amount

(in $) (in $)

salary from America 250000 75000 250000

Revenue through rent (Canada) 30000 3000 30000

allowable deduction of income -10000

3 Income tax assessment Act, 1997

4 Income tax assessment Act, 1993

By considering this, it can be presented that as per Sec 6 and 180 days – resident test referring

ITAA (1936) Jack was not recognized as an Australian resident for the purpose of taxation.

Calculating taxable income of Jack for the year ended on 30 June 2016

Issue: In accordance with the given case situation Jack Jones is considered as an

Australian resident for tax purpose. Thus, in this, main issue is to assess the taxable income of

him related to income tax year ended on 30th June 2016.

Laws: In order to assess taxable income of Jack Jones several sections and case laws have

been considered. Hence, section 6 (5 & 10), section 8 (1-10) has been assessed3. In addition to

this, section 25 (A) and case of Australia v Commonwealth Act has been considered4. Along

with this, TR 98/1 has also been followed to assess the taxable income of Jack Jones.

Application: As per ITAA (1936) an Australian resident must declare their foreign

income which is earned by him / her from anywhere in the world. Hence, in comparison with

foreign resident’s tax paid by Australian residents are lower (Pattenden & Twite, 2008). By

considering this, income earned by Jack Jones has been considered while determining tax

liability or obligation. Further, case situation presents that Jack Jones was not paid any tax on the

on the income earned in Canada. On the basis of such aspect Jack is obliged to pay tax on the

income earned in Canada during the year of 2015-16. Along with this, section 6 has also been

considered for assessing that salary from Canada is taxable (South Australia v Commonwealth,

2017). Further, through assessment, it has been identified case of Jack Jones is highly similar to

the case situation of South Australia V Commonwealth Act. By considering this, deductions are

considered such as:

PARTICULARS

Amount

Deductions

Amount

(in $) (in $)

salary from America 250000 75000 250000

Revenue through rent (Canada) 30000 3000 30000

allowable deduction of income -10000

3 Income tax assessment Act, 1997

4 Income tax assessment Act, 1993

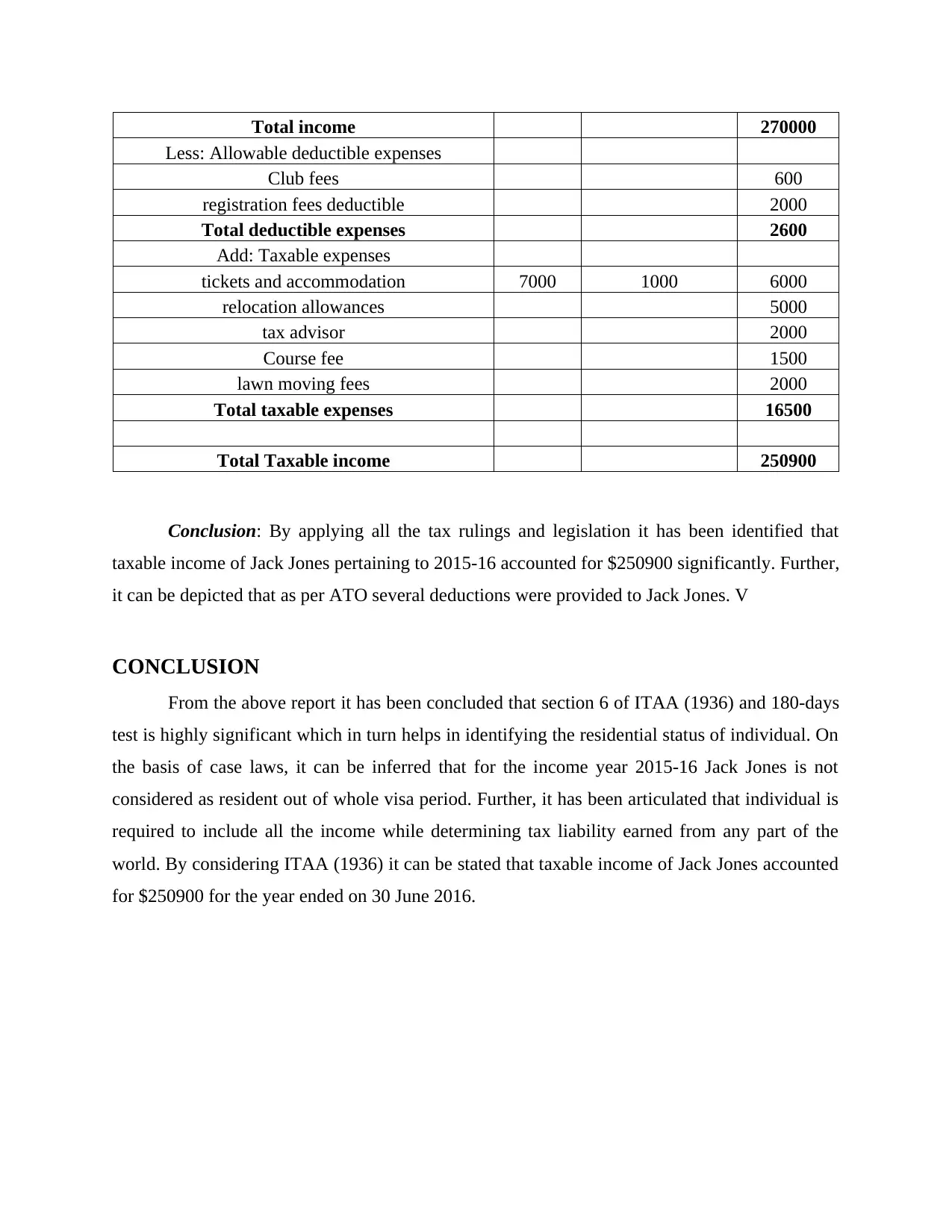

Total income 270000

Less: Allowable deductible expenses

Club fees 600

registration fees deductible 2000

Total deductible expenses 2600

Add: Taxable expenses

tickets and accommodation 7000 1000 6000

relocation allowances 5000

tax advisor 2000

Course fee 1500

lawn moving fees 2000

Total taxable expenses 16500

Total Taxable income 250900

Conclusion: By applying all the tax rulings and legislation it has been identified that

taxable income of Jack Jones pertaining to 2015-16 accounted for $250900 significantly. Further,

it can be depicted that as per ATO several deductions were provided to Jack Jones. V

CONCLUSION

From the above report it has been concluded that section 6 of ITAA (1936) and 180-days

test is highly significant which in turn helps in identifying the residential status of individual. On

the basis of case laws, it can be inferred that for the income year 2015-16 Jack Jones is not

considered as resident out of whole visa period. Further, it has been articulated that individual is

required to include all the income while determining tax liability earned from any part of the

world. By considering ITAA (1936) it can be stated that taxable income of Jack Jones accounted

for $250900 for the year ended on 30 June 2016.

Less: Allowable deductible expenses

Club fees 600

registration fees deductible 2000

Total deductible expenses 2600

Add: Taxable expenses

tickets and accommodation 7000 1000 6000

relocation allowances 5000

tax advisor 2000

Course fee 1500

lawn moving fees 2000

Total taxable expenses 16500

Total Taxable income 250900

Conclusion: By applying all the tax rulings and legislation it has been identified that

taxable income of Jack Jones pertaining to 2015-16 accounted for $250900 significantly. Further,

it can be depicted that as per ATO several deductions were provided to Jack Jones. V

CONCLUSION

From the above report it has been concluded that section 6 of ITAA (1936) and 180-days

test is highly significant which in turn helps in identifying the residential status of individual. On

the basis of case laws, it can be inferred that for the income year 2015-16 Jack Jones is not

considered as resident out of whole visa period. Further, it has been articulated that individual is

required to include all the income while determining tax liability earned from any part of the

world. By considering ITAA (1936) it can be stated that taxable income of Jack Jones accounted

for $250900 for the year ended on 30 June 2016.

REFERENCES

Books and Journals

King, A., 2016. Mid market focus: The new attribution tax regime for MITs: Part 1. Taxation in

Australia. 50(10). p.590.

Pattenden, K. & Twite, G., 2008. Taxes and dividend policy under alternative tax regimes.

Journal of Corporate Finance. 14(1). pp.1-16.

Reinhardt, S. & Steel, L., 2016. A brief history of Australia's tax system. Economic Round-up.

(Winter 2006). p.1.

Online

Residency – the resides test. 2017. Online. Available through: <

https://www.ato.gov.au/Individuals/International-tax-for-individuals/In-detail/Residency/

Residency---the-resides-test/>. [Accessed on 3rd October 2017].

South Australia v Commonwealth. 2017. Online. Available through: < https://jade.io/j/?

a=outline&id=64227>. [Accessed on 3rd October 2017].

Books and Journals

King, A., 2016. Mid market focus: The new attribution tax regime for MITs: Part 1. Taxation in

Australia. 50(10). p.590.

Pattenden, K. & Twite, G., 2008. Taxes and dividend policy under alternative tax regimes.

Journal of Corporate Finance. 14(1). pp.1-16.

Reinhardt, S. & Steel, L., 2016. A brief history of Australia's tax system. Economic Round-up.

(Winter 2006). p.1.

Online

Residency – the resides test. 2017. Online. Available through: <

https://www.ato.gov.au/Individuals/International-tax-for-individuals/In-detail/Residency/

Residency---the-resides-test/>. [Accessed on 3rd October 2017].

South Australia v Commonwealth. 2017. Online. Available through: < https://jade.io/j/?

a=outline&id=64227>. [Accessed on 3rd October 2017].

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.