Taxation law Sample Assignment (pdf)

VerifiedAdded on 2021/02/20

|10

|2742

|18

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Taxation law

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

Question 1: The goods and service tax (GST)............................................................................1

Question 2: Capital gain tax (CGT)............................................................................................3

CONCLUSION................................................................................................................................6

REFERENCES ...............................................................................................................................6

INTRODUCTION...........................................................................................................................1

Question 1: The goods and service tax (GST)............................................................................1

Question 2: Capital gain tax (CGT)............................................................................................3

CONCLUSION................................................................................................................................6

REFERENCES ...............................................................................................................................6

INTRODUCTION

Taxation law is the rules book to provide several rules and provisions which are several

things which render guide towards several business individuals and organisations. This law was

to maintain and create a betterment of environment of working conditions of business. These

laws and provisions help in creating several it points towards total wealth and revenue generated

in assessment year. These guidelines in Australia are created by federal government with help

from Australian taxation office. The following report refers toward two cases with different

circumstances in which what rules and codes are to be followed are mentioned under this report

(Bant, 2015).

Question 1: The goods and service tax (GST).

Facts of case: city sky co is a firm which deals in property development and investment,

after a recent purchase they contacted a lawyer Maurice Blackburn for legal help regarding

development for $ 33,000. This person being single owner of his firm has a revenue generation

of $ 300,000 per annum. Here they availed service of an local lawyer to accumulate services

regarding purchase of an vacant land.

The legal issue or suggestion here is very clear that GST stands for goods and services

tax, property bought by city sky co is an land which comes into immovable property. Its not a

good nor its a service. First of all company is a registered firm in GST so they can avail input tax

credits. Their is no GST on land so company shall not pay anything. No GST shall be implied

over this concept to understand things with more perspective one should understand following

concepts:

GST credit claims: this means that any person who pays tax is using some property for

his personal or business purpose then no input tax credit will be implied over it.

Reverse charge techniques: this term means to attain legal help from some lawyer or

any one, this theses services come under business purposes so they can be claimed under the

input tax credit (Bartleet And et. al., 2014).

GST over immovable property: the basic definition of GST is goods and service tax

which states that any good or service taken by any person or given by any person is made

available only for these things. The immovable properties which neither is a good nor a service.

The GST application of input tax credit will not be applicable in such cases.

1

Taxation law is the rules book to provide several rules and provisions which are several

things which render guide towards several business individuals and organisations. This law was

to maintain and create a betterment of environment of working conditions of business. These

laws and provisions help in creating several it points towards total wealth and revenue generated

in assessment year. These guidelines in Australia are created by federal government with help

from Australian taxation office. The following report refers toward two cases with different

circumstances in which what rules and codes are to be followed are mentioned under this report

(Bant, 2015).

Question 1: The goods and service tax (GST).

Facts of case: city sky co is a firm which deals in property development and investment,

after a recent purchase they contacted a lawyer Maurice Blackburn for legal help regarding

development for $ 33,000. This person being single owner of his firm has a revenue generation

of $ 300,000 per annum. Here they availed service of an local lawyer to accumulate services

regarding purchase of an vacant land.

The legal issue or suggestion here is very clear that GST stands for goods and services

tax, property bought by city sky co is an land which comes into immovable property. Its not a

good nor its a service. First of all company is a registered firm in GST so they can avail input tax

credits. Their is no GST on land so company shall not pay anything. No GST shall be implied

over this concept to understand things with more perspective one should understand following

concepts:

GST credit claims: this means that any person who pays tax is using some property for

his personal or business purpose then no input tax credit will be implied over it.

Reverse charge techniques: this term means to attain legal help from some lawyer or

any one, this theses services come under business purposes so they can be claimed under the

input tax credit (Bartleet And et. al., 2014).

GST over immovable property: the basic definition of GST is goods and service tax

which states that any good or service taken by any person or given by any person is made

available only for these things. The immovable properties which neither is a good nor a service.

The GST application of input tax credit will not be applicable in such cases.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Hence, in provided case scenario city sky co has acquired a vacant land and in present he

help of an lawyer is been taken for prominent purposes of making legal bindings and

requirements for a future project of developing 15 apartments. The goods and services tax will

not be applicable (Buchan, 2014).

The plans on constructing apartment on a vacant land under credit but black which

basically mean when a person who is taxable resident if buying such property shall not be liable

for any direct tax input. It is mentioned that city sky co is attaining help from a local lawyer

Maurice Blackburn for property development costing $33,000. Such services are made available

for purpose of attaining legal necessaries for particular project. The only regulations the business

firm will have should be this services attained by them, input direct tax will only be liable for

accumulating such services. In case of such property which is not even ready in present shall

require to provided to the receiver of property not person developing it.

The revenue generation for revenues given for the local lawyer Maurice Blackburn does not

make any sense and is not connected to case.

Recommendation: summarising the whole case the advice to firm city sky firm is that they are

never considered to be paying any taxes rather than input tax credit. Any other things mentioned

are not required to be paid by this firm, other things are liabilities of the person who will

eventually own such vacant lands after development (Dowling, 2014).

Having proper invoices of revenues is very important aspect according to Australian

system for taxation. It provides both GST collections and the credits which several business-men

are available to acquire and claim.

Any such business person should have all the invoices related to business demands and

requires all these to claim input tax credit from government. In several cases one can claim bona

fide tax invoice which should include names and identity of both buyer and seller.

Guidelines of GST are mentioned particularly in ATO on tax invoices and regulations. These

things qualify the fact that only goods or service which are provided are marked under GST not

any immovable property.

2

help of an lawyer is been taken for prominent purposes of making legal bindings and

requirements for a future project of developing 15 apartments. The goods and services tax will

not be applicable (Buchan, 2014).

The plans on constructing apartment on a vacant land under credit but black which

basically mean when a person who is taxable resident if buying such property shall not be liable

for any direct tax input. It is mentioned that city sky co is attaining help from a local lawyer

Maurice Blackburn for property development costing $33,000. Such services are made available

for purpose of attaining legal necessaries for particular project. The only regulations the business

firm will have should be this services attained by them, input direct tax will only be liable for

accumulating such services. In case of such property which is not even ready in present shall

require to provided to the receiver of property not person developing it.

The revenue generation for revenues given for the local lawyer Maurice Blackburn does not

make any sense and is not connected to case.

Recommendation: summarising the whole case the advice to firm city sky firm is that they are

never considered to be paying any taxes rather than input tax credit. Any other things mentioned

are not required to be paid by this firm, other things are liabilities of the person who will

eventually own such vacant lands after development (Dowling, 2014).

Having proper invoices of revenues is very important aspect according to Australian

system for taxation. It provides both GST collections and the credits which several business-men

are available to acquire and claim.

Any such business person should have all the invoices related to business demands and

requires all these to claim input tax credit from government. In several cases one can claim bona

fide tax invoice which should include names and identity of both buyer and seller.

Guidelines of GST are mentioned particularly in ATO on tax invoices and regulations. These

things qualify the fact that only goods or service which are provided are marked under GST not

any immovable property.

2

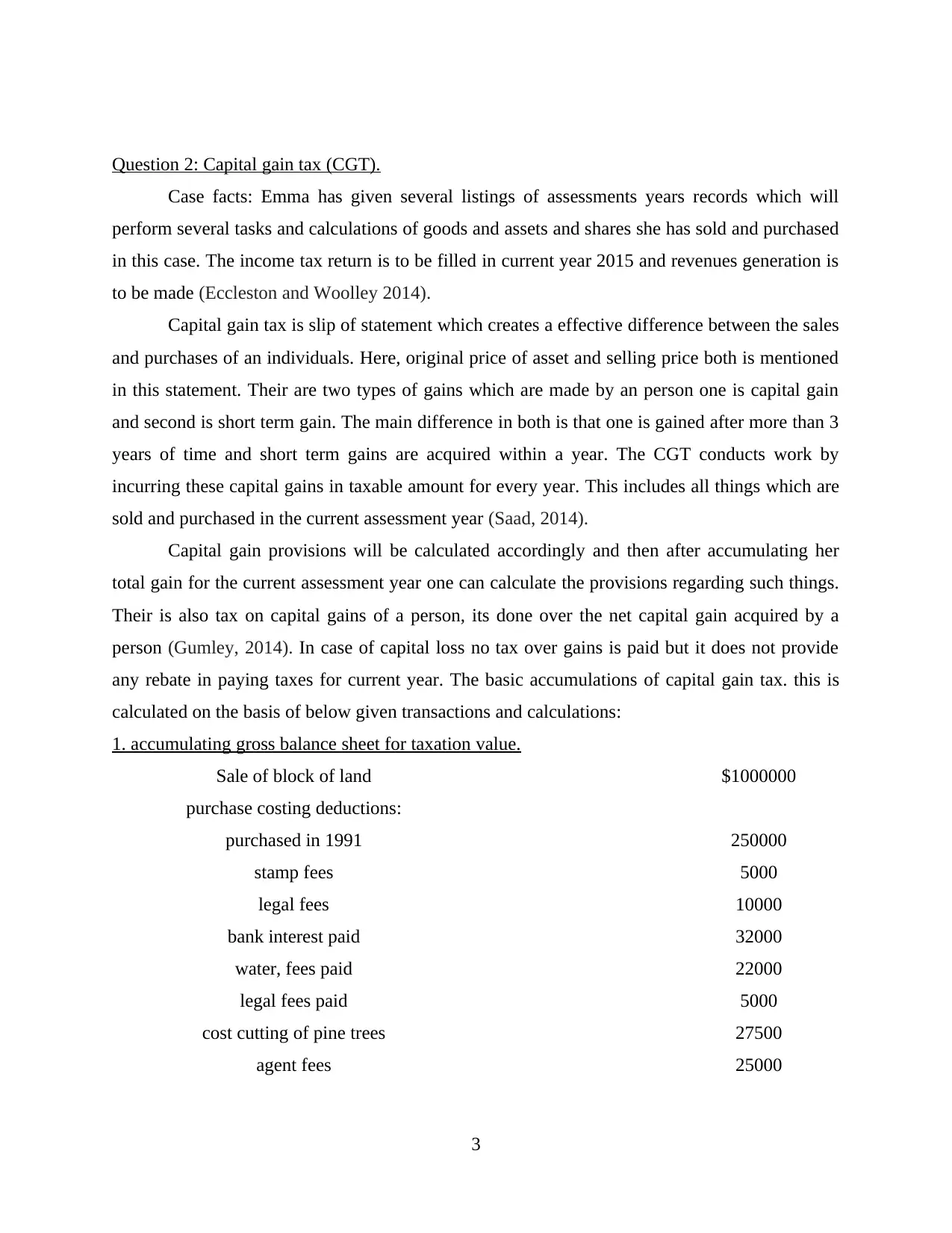

Question 2: Capital gain tax (CGT).

Case facts: Emma has given several listings of assessments years records which will

perform several tasks and calculations of goods and assets and shares she has sold and purchased

in this case. The income tax return is to be filled in current year 2015 and revenues generation is

to be made (Eccleston and Woolley 2014).

Capital gain tax is slip of statement which creates a effective difference between the sales

and purchases of an individuals. Here, original price of asset and selling price both is mentioned

in this statement. Their are two types of gains which are made by an person one is capital gain

and second is short term gain. The main difference in both is that one is gained after more than 3

years of time and short term gains are acquired within a year. The CGT conducts work by

incurring these capital gains in taxable amount for every year. This includes all things which are

sold and purchased in the current assessment year (Saad, 2014).

Capital gain provisions will be calculated accordingly and then after accumulating her

total gain for the current assessment year one can calculate the provisions regarding such things.

Their is also tax on capital gains of a person, its done over the net capital gain acquired by a

person (Gumley, 2014). In case of capital loss no tax over gains is paid but it does not provide

any rebate in paying taxes for current year. The basic accumulations of capital gain tax. this is

calculated on the basis of below given transactions and calculations:

1. accumulating gross balance sheet for taxation value.

Sale of block of land $1000000

purchase costing deductions:

purchased in 1991 250000

stamp fees 5000

legal fees 10000

bank interest paid 32000

water, fees paid 22000

legal fees paid 5000

cost cutting of pine trees 27500

agent fees 25000

3

Case facts: Emma has given several listings of assessments years records which will

perform several tasks and calculations of goods and assets and shares she has sold and purchased

in this case. The income tax return is to be filled in current year 2015 and revenues generation is

to be made (Eccleston and Woolley 2014).

Capital gain tax is slip of statement which creates a effective difference between the sales

and purchases of an individuals. Here, original price of asset and selling price both is mentioned

in this statement. Their are two types of gains which are made by an person one is capital gain

and second is short term gain. The main difference in both is that one is gained after more than 3

years of time and short term gains are acquired within a year. The CGT conducts work by

incurring these capital gains in taxable amount for every year. This includes all things which are

sold and purchased in the current assessment year (Saad, 2014).

Capital gain provisions will be calculated accordingly and then after accumulating her

total gain for the current assessment year one can calculate the provisions regarding such things.

Their is also tax on capital gains of a person, its done over the net capital gain acquired by a

person (Gumley, 2014). In case of capital loss no tax over gains is paid but it does not provide

any rebate in paying taxes for current year. The basic accumulations of capital gain tax. this is

calculated on the basis of below given transactions and calculations:

1. accumulating gross balance sheet for taxation value.

Sale of block of land $1000000

purchase costing deductions:

purchased in 1991 250000

stamp fees 5000

legal fees 10000

bank interest paid 32000

water, fees paid 22000

legal fees paid 5000

cost cutting of pine trees 27500

agent fees 25000

3

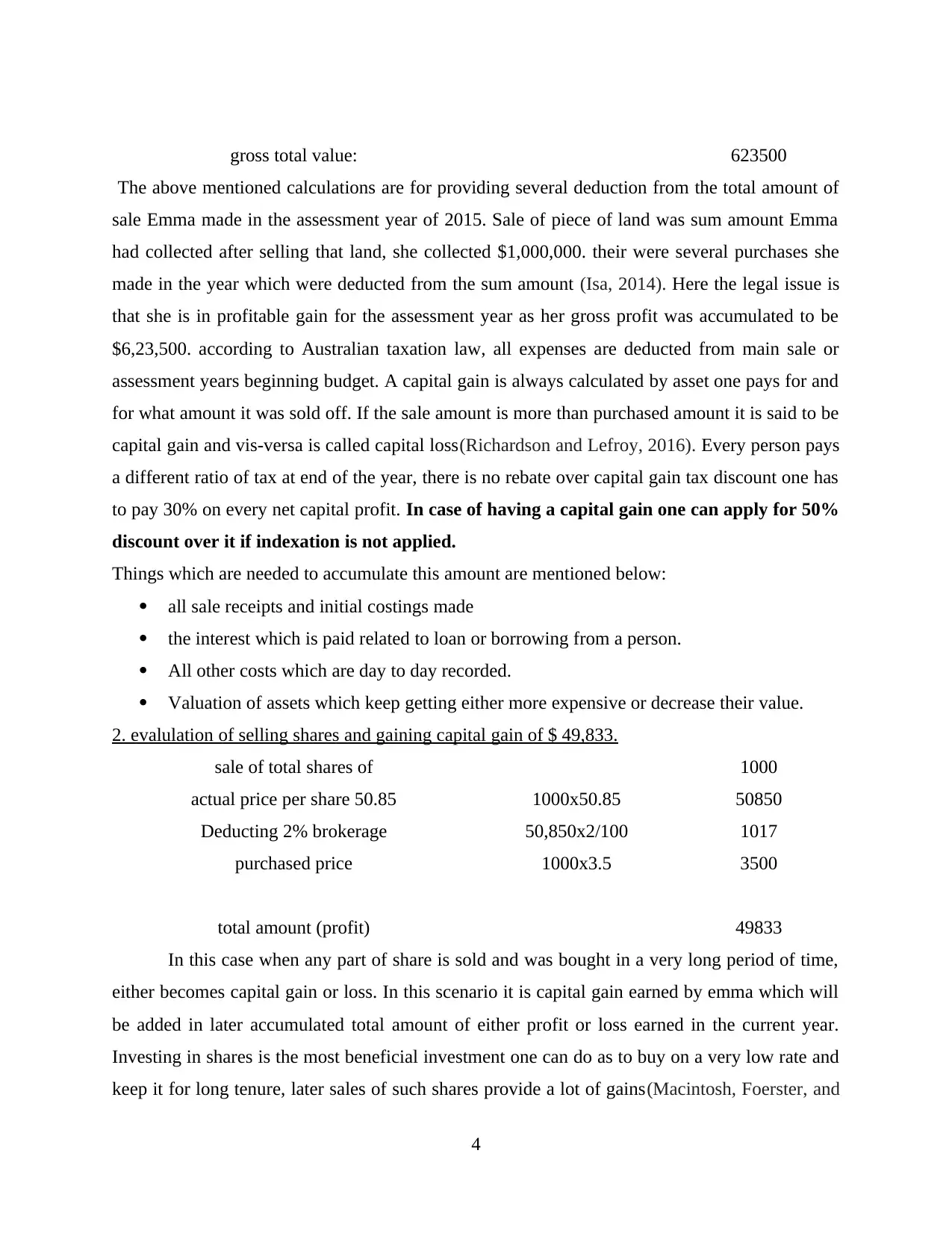

gross total value: 623500

The above mentioned calculations are for providing several deduction from the total amount of

sale Emma made in the assessment year of 2015. Sale of piece of land was sum amount Emma

had collected after selling that land, she collected $1,000,000. their were several purchases she

made in the year which were deducted from the sum amount (Isa, 2014). Here the legal issue is

that she is in profitable gain for the assessment year as her gross profit was accumulated to be

$6,23,500. according to Australian taxation law, all expenses are deducted from main sale or

assessment years beginning budget. A capital gain is always calculated by asset one pays for and

for what amount it was sold off. If the sale amount is more than purchased amount it is said to be

capital gain and vis-versa is called capital loss(Richardson and Lefroy, 2016). Every person pays

a different ratio of tax at end of the year, there is no rebate over capital gain tax discount one has

to pay 30% on every net capital profit. In case of having a capital gain one can apply for 50%

discount over it if indexation is not applied.

Things which are needed to accumulate this amount are mentioned below:

all sale receipts and initial costings made

the interest which is paid related to loan or borrowing from a person.

All other costs which are day to day recorded.

Valuation of assets which keep getting either more expensive or decrease their value.

2. evalulation of selling shares and gaining capital gain of $ 49,833.

sale of total shares of 1000

actual price per share 50.85 1000x50.85 50850

Deducting 2% brokerage 50,850x2/100 1017

purchased price 1000x3.5 3500

total amount (profit) 49833

In this case when any part of share is sold and was bought in a very long period of time,

either becomes capital gain or loss. In this scenario it is capital gain earned by emma which will

be added in later accumulated total amount of either profit or loss earned in the current year.

Investing in shares is the most beneficial investment one can do as to buy on a very low rate and

keep it for long tenure, later sales of such shares provide a lot of gains(Macintosh, Foerster, and

4

The above mentioned calculations are for providing several deduction from the total amount of

sale Emma made in the assessment year of 2015. Sale of piece of land was sum amount Emma

had collected after selling that land, she collected $1,000,000. their were several purchases she

made in the year which were deducted from the sum amount (Isa, 2014). Here the legal issue is

that she is in profitable gain for the assessment year as her gross profit was accumulated to be

$6,23,500. according to Australian taxation law, all expenses are deducted from main sale or

assessment years beginning budget. A capital gain is always calculated by asset one pays for and

for what amount it was sold off. If the sale amount is more than purchased amount it is said to be

capital gain and vis-versa is called capital loss(Richardson and Lefroy, 2016). Every person pays

a different ratio of tax at end of the year, there is no rebate over capital gain tax discount one has

to pay 30% on every net capital profit. In case of having a capital gain one can apply for 50%

discount over it if indexation is not applied.

Things which are needed to accumulate this amount are mentioned below:

all sale receipts and initial costings made

the interest which is paid related to loan or borrowing from a person.

All other costs which are day to day recorded.

Valuation of assets which keep getting either more expensive or decrease their value.

2. evalulation of selling shares and gaining capital gain of $ 49,833.

sale of total shares of 1000

actual price per share 50.85 1000x50.85 50850

Deducting 2% brokerage 50,850x2/100 1017

purchased price 1000x3.5 3500

total amount (profit) 49833

In this case when any part of share is sold and was bought in a very long period of time,

either becomes capital gain or loss. In this scenario it is capital gain earned by emma which will

be added in later accumulated total amount of either profit or loss earned in the current year.

Investing in shares is the most beneficial investment one can do as to buy on a very low rate and

keep it for long tenure, later sales of such shares provide a lot of gains(Macintosh, Foerster, and

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

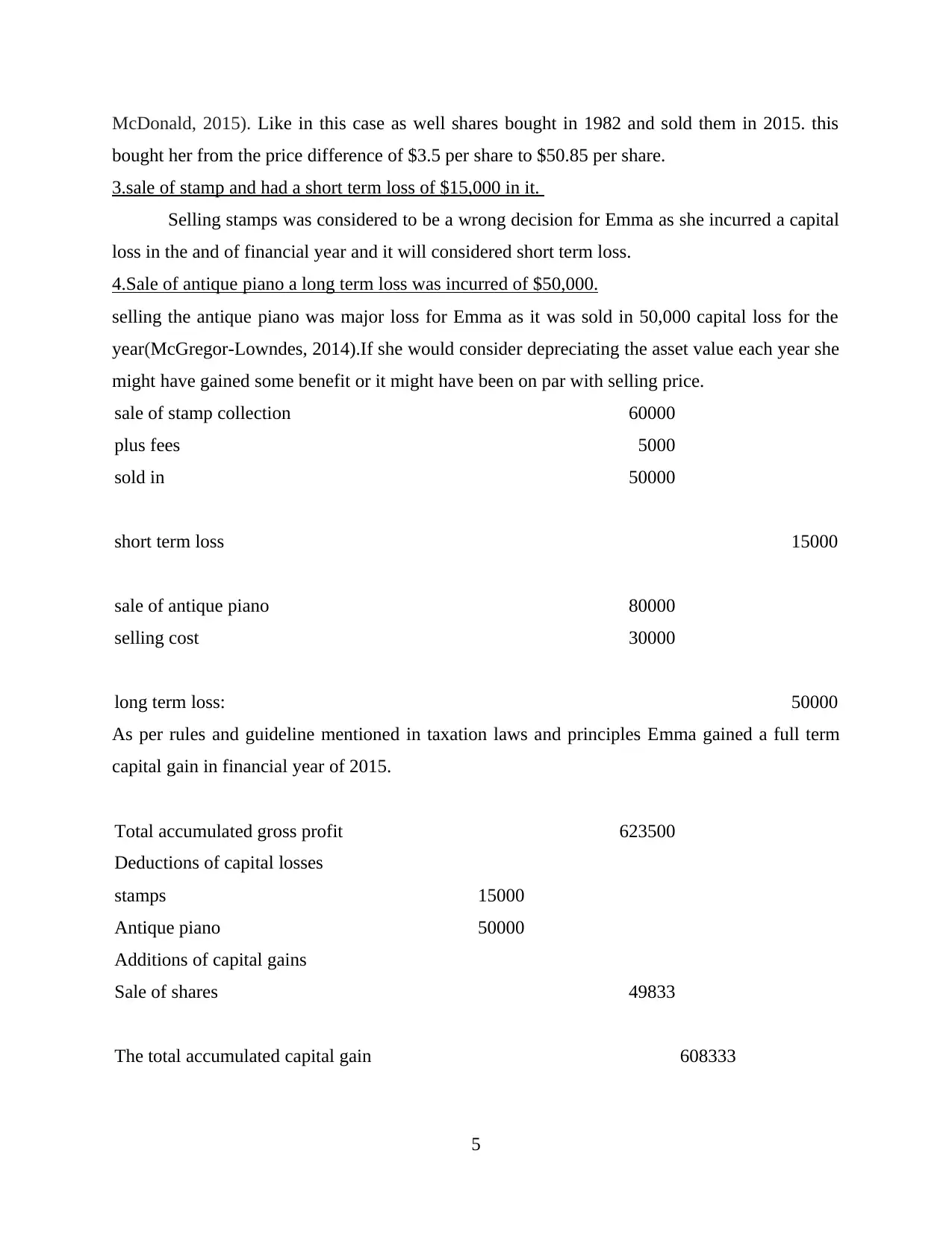

McDonald, 2015). Like in this case as well shares bought in 1982 and sold them in 2015. this

bought her from the price difference of $3.5 per share to $50.85 per share.

3.sale of stamp and had a short term loss of $15,000 in it.

Selling stamps was considered to be a wrong decision for Emma as she incurred a capital

loss in the and of financial year and it will considered short term loss.

4.Sale of antique piano a long term loss was incurred of $50,000.

selling the antique piano was major loss for Emma as it was sold in 50,000 capital loss for the

year(McGregor-Lowndes, 2014).If she would consider depreciating the asset value each year she

might have gained some benefit or it might have been on par with selling price.

sale of stamp collection 60000

plus fees 5000

sold in 50000

short term loss 15000

sale of antique piano 80000

selling cost 30000

long term loss: 50000

As per rules and guideline mentioned in taxation laws and principles Emma gained a full term

capital gain in financial year of 2015.

Total accumulated gross profit 623500

Deductions of capital losses

stamps 15000

Antique piano 50000

Additions of capital gains

Sale of shares 49833

The total accumulated capital gain 608333

5

bought her from the price difference of $3.5 per share to $50.85 per share.

3.sale of stamp and had a short term loss of $15,000 in it.

Selling stamps was considered to be a wrong decision for Emma as she incurred a capital

loss in the and of financial year and it will considered short term loss.

4.Sale of antique piano a long term loss was incurred of $50,000.

selling the antique piano was major loss for Emma as it was sold in 50,000 capital loss for the

year(McGregor-Lowndes, 2014).If she would consider depreciating the asset value each year she

might have gained some benefit or it might have been on par with selling price.

sale of stamp collection 60000

plus fees 5000

sold in 50000

short term loss 15000

sale of antique piano 80000

selling cost 30000

long term loss: 50000

As per rules and guideline mentioned in taxation laws and principles Emma gained a full term

capital gain in financial year of 2015.

Total accumulated gross profit 623500

Deductions of capital losses

stamps 15000

Antique piano 50000

Additions of capital gains

Sale of shares 49833

The total accumulated capital gain 608333

5

In the following case scenario, one can accumulate the legal issue to be that Emma

should have had applied for the policy of gaining 50% benefit over profit in assessment year.

The guidelines which were followed in the course year were from rule book of taxation in

Australian laws (Moretto and et. al., 2014).

According to superannuation funds should register and fill form of capital gain tax(NAT

3423).

One shall consider several tax and regulation rule books which will provide several benefits and

rules to solve all issues and accumulate the net gain and loss of the year(Picciotto, 2015). Such

guide books are:

company tax return act

trust tax return

fund income tax return

Self-managed superannuation fund annual return.

Recommendation: In this case scenario Emma will gain capital gain tax and can file for claiming

all her expenses incurred in whole assessment year. According to policies in taxation laws one

can claim back their all expenses in end of year though gaining capital gain in the end (Murray,

2015).

CONCLUSION

In report mentioned above two scenarios provided guide through several guidelines

provided for the correct analysis of tax savings and accumulating gains and losses (Welsh, 2014).

Taxation law of Australia is strict policy act but it does provide several remedies. In certain case

laws one can gain many benefits out of filling in provisions form to gain extra benefit & claim

several expenses back at time of tax paying.

6

should have had applied for the policy of gaining 50% benefit over profit in assessment year.

The guidelines which were followed in the course year were from rule book of taxation in

Australian laws (Moretto and et. al., 2014).

According to superannuation funds should register and fill form of capital gain tax(NAT

3423).

One shall consider several tax and regulation rule books which will provide several benefits and

rules to solve all issues and accumulate the net gain and loss of the year(Picciotto, 2015). Such

guide books are:

company tax return act

trust tax return

fund income tax return

Self-managed superannuation fund annual return.

Recommendation: In this case scenario Emma will gain capital gain tax and can file for claiming

all her expenses incurred in whole assessment year. According to policies in taxation laws one

can claim back their all expenses in end of year though gaining capital gain in the end (Murray,

2015).

CONCLUSION

In report mentioned above two scenarios provided guide through several guidelines

provided for the correct analysis of tax savings and accumulating gains and losses (Welsh, 2014).

Taxation law of Australia is strict policy act but it does provide several remedies. In certain case

laws one can gain many benefits out of filling in provisions form to gain extra benefit & claim

several expenses back at time of tax paying.

6

REFERENCES

Books and journals

Bant, E., 2015. Statute and common law: Interaction and influence in light of the principle of

coherence. UNSWLJ. 38. p.367.

Bartleet, B.L. And et. al., 2014. Reconciliation and transformation through mutual learning:

Outlining a framework for arts-based service learning with Indigenous communities in

Australia. International Journal of Education & the Arts. 15(8).

Buchan, J., 2014. Deconstructing the franchise as a legal entity: practice and research in

international franchise law. Journal of Marketing Channels. 21(3). pp.143-158.

Dowling, G. R., 2014. The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics. 124(1). pp.173-184.

Eccleston, R. and Woolley, T., 2014. From Calgary to Canberra: resource taxation and fiscal

federalism in Canada and Australia. Publius: The Journal of Federalism. 45(2). pp.216-

243.

Gumley, W., 2014. An analysis of regulatory strategies for recycling and re-use of metals in

Australia. Resources. 3(2). pp.395-415.

Isa, K., 2014. Tax complexities in the Malaysian corporate tax system: minimise to

maximise. International Journal of Law and Management. 56(1). pp.50-65.

7

Books and journals

Bant, E., 2015. Statute and common law: Interaction and influence in light of the principle of

coherence. UNSWLJ. 38. p.367.

Bartleet, B.L. And et. al., 2014. Reconciliation and transformation through mutual learning:

Outlining a framework for arts-based service learning with Indigenous communities in

Australia. International Journal of Education & the Arts. 15(8).

Buchan, J., 2014. Deconstructing the franchise as a legal entity: practice and research in

international franchise law. Journal of Marketing Channels. 21(3). pp.143-158.

Dowling, G. R., 2014. The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics. 124(1). pp.173-184.

Eccleston, R. and Woolley, T., 2014. From Calgary to Canberra: resource taxation and fiscal

federalism in Canada and Australia. Publius: The Journal of Federalism. 45(2). pp.216-

243.

Gumley, W., 2014. An analysis of regulatory strategies for recycling and re-use of metals in

Australia. Resources. 3(2). pp.395-415.

Isa, K., 2014. Tax complexities in the Malaysian corporate tax system: minimise to

maximise. International Journal of Law and Management. 56(1). pp.50-65.

7

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.