HA3042 Taxation Law Assignment: FBT and Capital Gains Analysis

VerifiedAdded on 2023/03/21

|10

|1773

|53

Homework Assignment

AI Summary

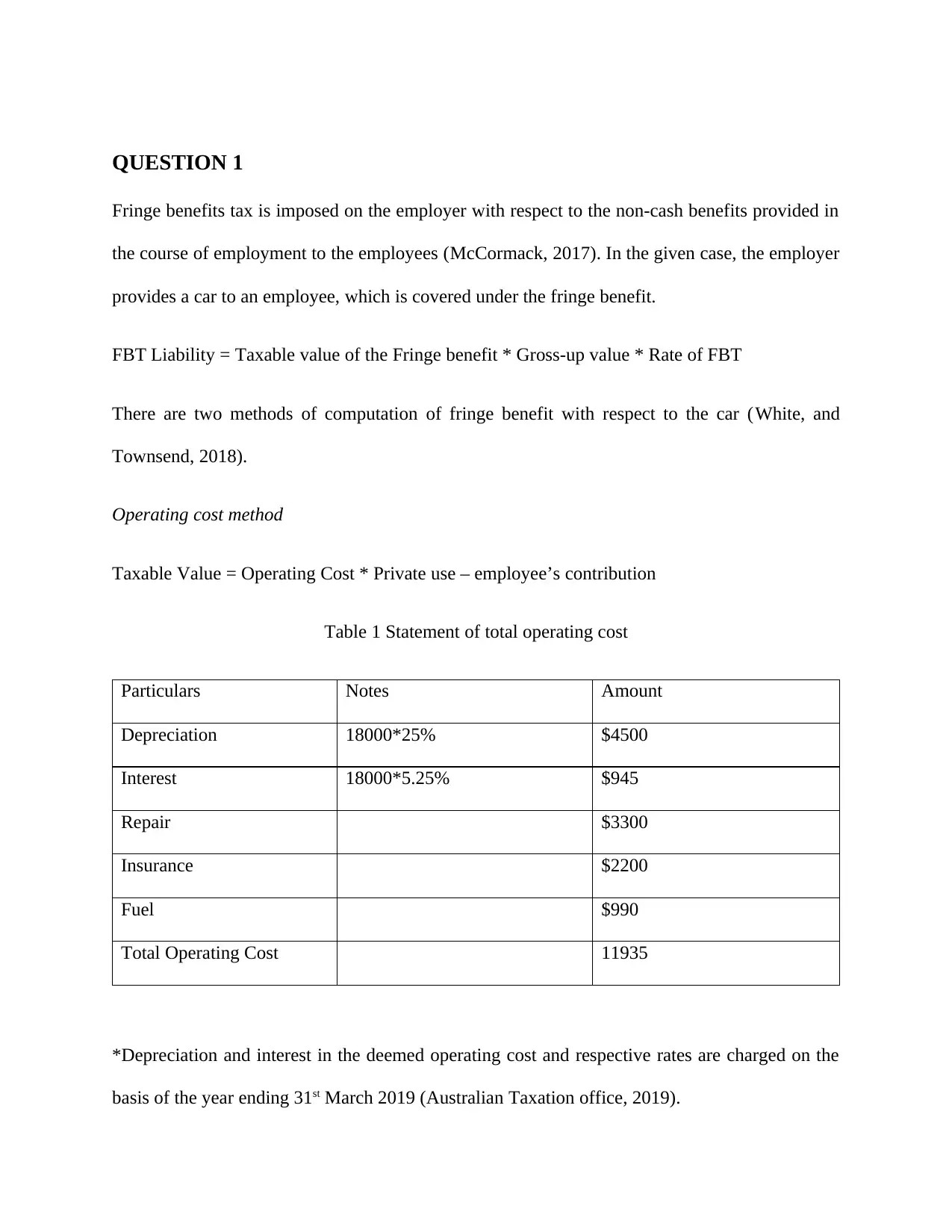

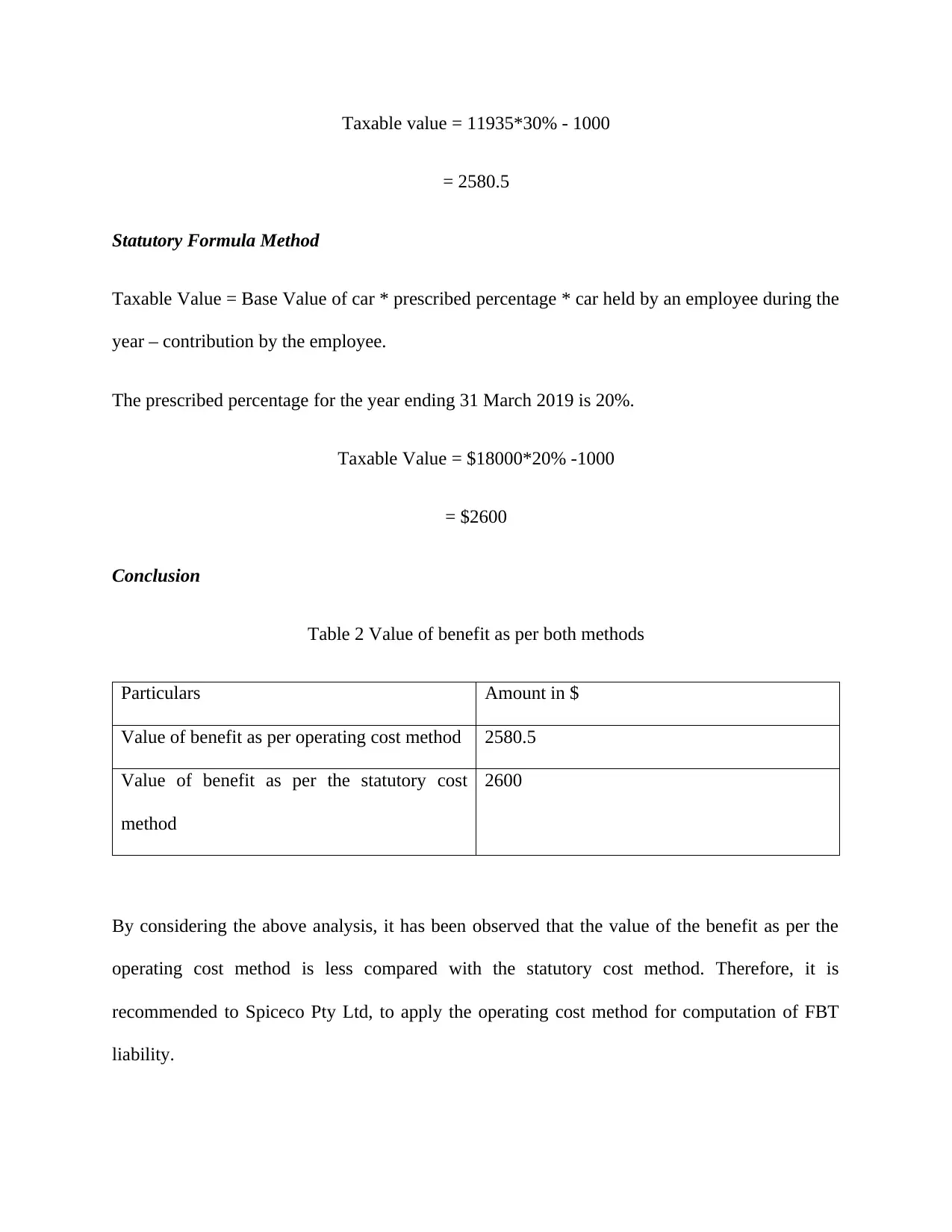

This assignment delves into key aspects of taxation law, specifically focusing on fringe benefits tax (FBT) and capital gains. The solution begins by addressing FBT, outlining the computation methods (operating cost and statutory formula) and recommending the optimal approach for Spiceco Pty Ltd. The assignment then moves on to capital gains, detailing the calculation of net capital gain or loss for the year ending June 30, 2019, for Daniel, including the treatment of various assets like property, paintings, a yacht, and shares. It analyzes the tax implications of different scenarios, such as a house sale contract that wasn't completed and the sale of shares. The solution concludes by suggesting strategies for Daniel to manage a likely net capital gain and loss, including investment in a superannuation fund. The assignment draws on relevant legal and financial principles, supported by citations of academic sources and online resources.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.