Holmes Institute HI6028 Taxation Law Assignment Solution

VerifiedAdded on 2022/10/19

|8

|2920

|269

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, addressing key concepts within the Australian taxation system. The assignment delves into Capital Gains Tax (CGT), examining the tax implications of various asset sales, including an antique painting, a historical sculpture, antique jewelry, and a picture, considering pre-CGT assets, collectables, and personal use assets. It further analyzes the concept of ordinary income, specifically focusing on whether receipts from personal exertion, such as writing a book and selling its copyright, are taxable. The solution references relevant case law to support its arguments. Finally, the assignment explores the taxability of interest earned from a loan, determining whether it constitutes ordinary income. The analysis considers the application of relevant legislation and legal precedents to provide a well-reasoned and detailed response to the assignment questions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................3

Answer to question 3:...................................................................................................5

References:..................................................................................................................7

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................3

Answer to question 3:...................................................................................................5

References:..................................................................................................................7

2TAXATION LAW

Answer to question 1:

Capital Gain Tax regarding antique impressionism painting

As noted in “sec 100-25 (1), ITAA 1997” capital gains tax is limited on the

assets to which it is applied and to those that are acquired on or following the 20 th

September 1985. Up to 21 September 1999 only the real gains that are made is

applied for tax under the capital gains tax regimes (Minas, Lim and Evans 2018). As

a result of this the cost base of the capital gains tax asset was indexed for the

purpose of inflation if the CGT asset sold that was held for greater than 12 months.

Assets which is purchased before the 20th September 1985 and gains derived

thereon, is not liable for CGT because they exempted assets.

The antique painting here is purchased by Helen before the 20th September

1985. In other words, the painting is purchased on February 1985 which is before the

introduction of the CGT regimes. however, the painting was sold in 2018 December.

The purchase price was $4,000 while the sales value stood $12,000. So the sale of

painting has led to capital gain. As the asset is bought before the CGT introduction

date so it is pre-CGT asset and the capital gains here is exempted for Helen.

Capital Gain Tax regarding historical sculpture:

The provision of CGT is applied on the actual or the realised gains. Under

“sec 102-5 (1)” The capital gains are taxable for the taxpayer as the statutory

income and also included in the assessable earnings. “Sec 104-10, ITAA 1997”

deals with the disposal of CGT asset (He et al. 2016). When the CGT asset is sold

then the CGT event A1 happens. A collectable implies items such as antiques,

sculptures, rare books, jewellery listed in “sec 108-10 (2), ITAA 1997” that is used

for personal enjoyment purpose.

An art work in the form of sculpture was purchased in 1993 for $5,500. Helen

sold it for $6,000 in 2018. The sculpture is regarded as an item of collectable under

“sec 108-10 (2), ITAA 1997”. The sale of sculpture has given rise to CGT event A1

under “sec 104-10, ITAA 1997”. The capital gains made is considered taxable as

statutory income under “sec 6-10” and will be included in Helen assessable income

based on “sec 102-5 (1)”.

Capital Gain Tax regarding antique jewellery piece:

Notably, “sec 108-10 (1), ITAA 1997” explains that capital loss from

collectables are quarantined and is only allowed to be offset against the capital gains

from other collectables (Harding and Marten 2018). This implies that amount that is

leftover from capital loss is carried forward to future years under “sec 108-10 (4)”.

The taxpayer here Helen has bought the jewellery for $14,000. The jewellery is sold

on 20 march 2018 for a loss of $1,000 from the actual purchase price. Abiding by the

quarantined rule given under “sec 108-10 (1), ITAA 1997” the capital loss must be

quarantined and can be offset against capital gain from sculpture. On the basis of

“sec 108-10 (4), ITAA 1997” while the remaining amount of $500 as the unused

capital loss should be carried forward to future year.

Capital Gain Tax regarding picture:

“Sec 108-20 to 108-30” list down the personal use asset. These assets must

not be mistaken as collectables (Hellwig and McAllister 2018). Rather in includes

Answer to question 1:

Capital Gain Tax regarding antique impressionism painting

As noted in “sec 100-25 (1), ITAA 1997” capital gains tax is limited on the

assets to which it is applied and to those that are acquired on or following the 20 th

September 1985. Up to 21 September 1999 only the real gains that are made is

applied for tax under the capital gains tax regimes (Minas, Lim and Evans 2018). As

a result of this the cost base of the capital gains tax asset was indexed for the

purpose of inflation if the CGT asset sold that was held for greater than 12 months.

Assets which is purchased before the 20th September 1985 and gains derived

thereon, is not liable for CGT because they exempted assets.

The antique painting here is purchased by Helen before the 20th September

1985. In other words, the painting is purchased on February 1985 which is before the

introduction of the CGT regimes. however, the painting was sold in 2018 December.

The purchase price was $4,000 while the sales value stood $12,000. So the sale of

painting has led to capital gain. As the asset is bought before the CGT introduction

date so it is pre-CGT asset and the capital gains here is exempted for Helen.

Capital Gain Tax regarding historical sculpture:

The provision of CGT is applied on the actual or the realised gains. Under

“sec 102-5 (1)” The capital gains are taxable for the taxpayer as the statutory

income and also included in the assessable earnings. “Sec 104-10, ITAA 1997”

deals with the disposal of CGT asset (He et al. 2016). When the CGT asset is sold

then the CGT event A1 happens. A collectable implies items such as antiques,

sculptures, rare books, jewellery listed in “sec 108-10 (2), ITAA 1997” that is used

for personal enjoyment purpose.

An art work in the form of sculpture was purchased in 1993 for $5,500. Helen

sold it for $6,000 in 2018. The sculpture is regarded as an item of collectable under

“sec 108-10 (2), ITAA 1997”. The sale of sculpture has given rise to CGT event A1

under “sec 104-10, ITAA 1997”. The capital gains made is considered taxable as

statutory income under “sec 6-10” and will be included in Helen assessable income

based on “sec 102-5 (1)”.

Capital Gain Tax regarding antique jewellery piece:

Notably, “sec 108-10 (1), ITAA 1997” explains that capital loss from

collectables are quarantined and is only allowed to be offset against the capital gains

from other collectables (Harding and Marten 2018). This implies that amount that is

leftover from capital loss is carried forward to future years under “sec 108-10 (4)”.

The taxpayer here Helen has bought the jewellery for $14,000. The jewellery is sold

on 20 march 2018 for a loss of $1,000 from the actual purchase price. Abiding by the

quarantined rule given under “sec 108-10 (1), ITAA 1997” the capital loss must be

quarantined and can be offset against capital gain from sculpture. On the basis of

“sec 108-10 (4), ITAA 1997” while the remaining amount of $500 as the unused

capital loss should be carried forward to future year.

Capital Gain Tax regarding picture:

“Sec 108-20 to 108-30” list down the personal use asset. These assets must

not be mistaken as collectables (Hellwig and McAllister 2018). Rather in includes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

boats, racehorses, equipment, electronic items and household items which is for

personal use of taxpayer. In the meantime, “sec 118-10 (3)” ignores the personal

use assets for capital gains purpose if the value is less than $10,000.

Helen sold the picture on July 2018. The sales value of the picture was

$5,000. The picture was purchased in 1987 with the purchase value being $470. As

noted the picture should be categorized as the personal use asset under “sec 108-

20, ITAA 1997”. Abiding with the rules given under “sec 118-10 (3)”, the capital

gain from picture does not attracts any capital gain tax because the asset does not

qualify the eligibility criteria given in “sec 118-10 (3), ITAA 1997” as its cost price is

less than $10,000.

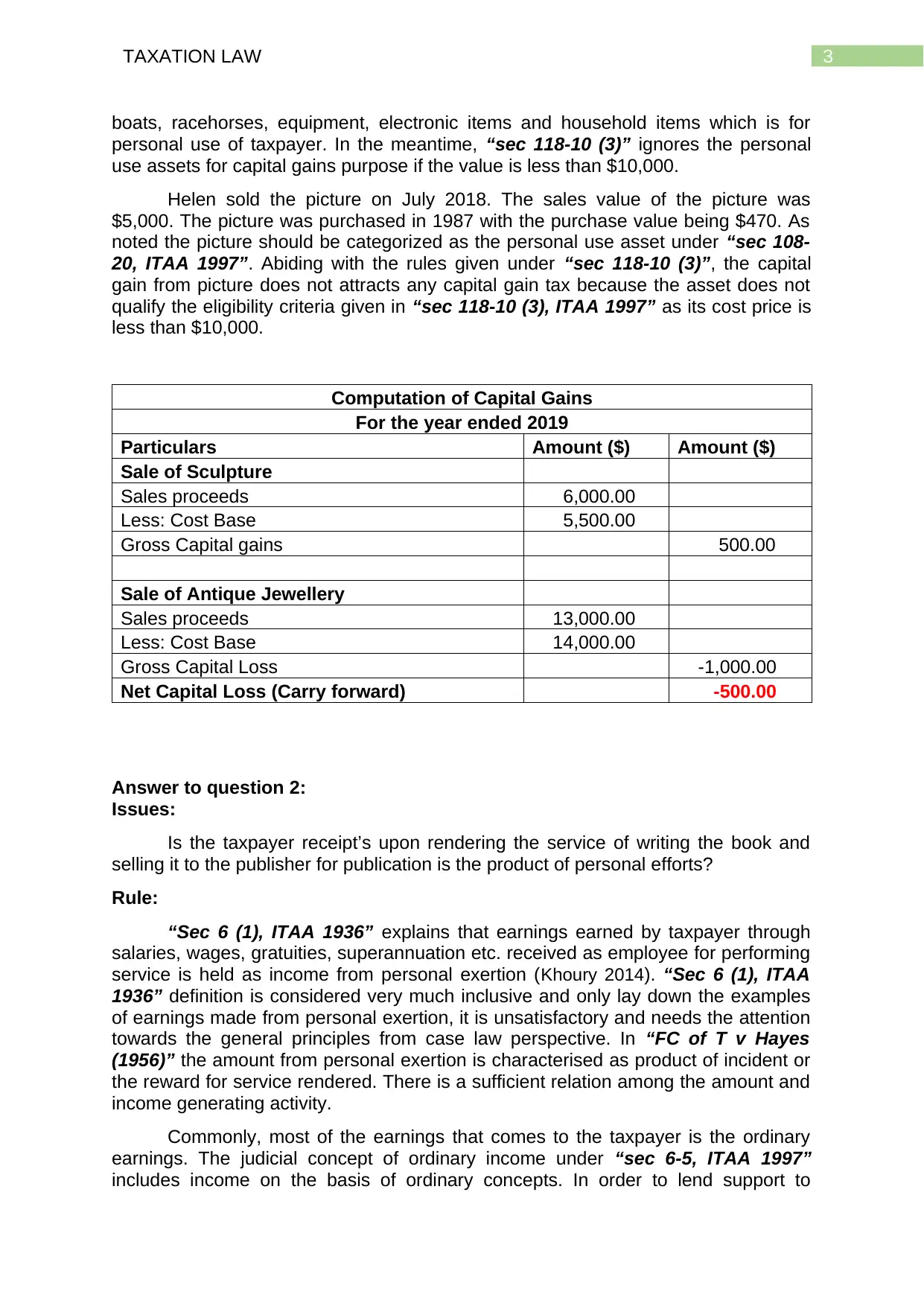

Computation of Capital Gains

For the year ended 2019

Particulars Amount ($) Amount ($)

Sale of Sculpture

Sales proceeds 6,000.00

Less: Cost Base 5,500.00

Gross Capital gains 500.00

Sale of Antique Jewellery

Sales proceeds 13,000.00

Less: Cost Base 14,000.00

Gross Capital Loss -1,000.00

Net Capital Loss (Carry forward) -500.00

Answer to question 2:

Issues:

Is the taxpayer receipt’s upon rendering the service of writing the book and

selling it to the publisher for publication is the product of personal efforts?

Rule:

“Sec 6 (1), ITAA 1936” explains that earnings earned by taxpayer through

salaries, wages, gratuities, superannuation etc. received as employee for performing

service is held as income from personal exertion (Khoury 2014). “Sec 6 (1), ITAA

1936” definition is considered very much inclusive and only lay down the examples

of earnings made from personal exertion, it is unsatisfactory and needs the attention

towards the general principles from case law perspective. In “FC of T v Hayes

(1956)” the amount from personal exertion is characterised as product of incident or

the reward for service rendered. There is a sufficient relation among the amount and

income generating activity.

Commonly, most of the earnings that comes to the taxpayer is the ordinary

earnings. The judicial concept of ordinary income under “sec 6-5, ITAA 1997”

includes income on the basis of ordinary concepts. In order to lend support to

boats, racehorses, equipment, electronic items and household items which is for

personal use of taxpayer. In the meantime, “sec 118-10 (3)” ignores the personal

use assets for capital gains purpose if the value is less than $10,000.

Helen sold the picture on July 2018. The sales value of the picture was

$5,000. The picture was purchased in 1987 with the purchase value being $470. As

noted the picture should be categorized as the personal use asset under “sec 108-

20, ITAA 1997”. Abiding with the rules given under “sec 118-10 (3)”, the capital

gain from picture does not attracts any capital gain tax because the asset does not

qualify the eligibility criteria given in “sec 118-10 (3), ITAA 1997” as its cost price is

less than $10,000.

Computation of Capital Gains

For the year ended 2019

Particulars Amount ($) Amount ($)

Sale of Sculpture

Sales proceeds 6,000.00

Less: Cost Base 5,500.00

Gross Capital gains 500.00

Sale of Antique Jewellery

Sales proceeds 13,000.00

Less: Cost Base 14,000.00

Gross Capital Loss -1,000.00

Net Capital Loss (Carry forward) -500.00

Answer to question 2:

Issues:

Is the taxpayer receipt’s upon rendering the service of writing the book and

selling it to the publisher for publication is the product of personal efforts?

Rule:

“Sec 6 (1), ITAA 1936” explains that earnings earned by taxpayer through

salaries, wages, gratuities, superannuation etc. received as employee for performing

service is held as income from personal exertion (Khoury 2014). “Sec 6 (1), ITAA

1936” definition is considered very much inclusive and only lay down the examples

of earnings made from personal exertion, it is unsatisfactory and needs the attention

towards the general principles from case law perspective. In “FC of T v Hayes

(1956)” the amount from personal exertion is characterised as product of incident or

the reward for service rendered. There is a sufficient relation among the amount and

income generating activity.

Commonly, most of the earnings that comes to the taxpayer is the ordinary

earnings. The judicial concept of ordinary income under “sec 6-5, ITAA 1997”

includes income on the basis of ordinary concepts. In order to lend support to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

consider the personal exertion income as income case laws such as “Brent v FCT

(1971)” is approached (Morrison 2015). The was held for deriving taxable earnings

when she was given money for telling the story of her life to the newspaper in order

to make exclusive publication.

In view of that, another example can be considered of “Hobbs v Hussey

(1942)” where the notorious criminal received £1,500 for selling the autobiography to

the publisher for making an exclusive publication of the story in the newspaper article

(Pert et al. 2016). The quantum of the payment that is made to the taxpayer is not to

simply cover the cost or the inconvenience.

In another example of “Housden v Marshall (1958)” the taxpayer was the

taxable when he sold the experience of Jockey which also included the photographs

and the cuttings of newspaper (Graetz 2015). The amount received was ordinary

income and taxable under the ordinary meaning of “sec 6-5, ITAA 1997”.

Application:

Barbara is the economist and also a research commentator. A publisher

named Eco Books Ltd provided Barbara with the $13,000 to write book on

economics. She accepted the offer and wrote the book named as Principle of

Economics. The sum of $13,000 relates to Barbara’s provision of services.

Additionally, discussing the example of “Brent v FCT (1971)” the payment is having

nexus among the services that is rendered and the earning activity (Kenny 2015).

The character of payment that is received in the hand of Barbara is personal exertion

income under “sec 6 (1), ITAA 1997”. The amount will be taxable as ordinary

earnings within the judicial meaning of “sec 6-5, ITAA 1997”.

She later assigned the copyright of Principle of Economics to the Eco Books

Ltd. The amount paid to sell the copyright of book was $13,400. Discussing the

similar case example of “Hobbs v Hussey (1942)” selling the copyright to publisher

by assigning the copyright of the books by Barbara is a taxable ordinary income

under the judicial meaning of “sec 6-5, ITAA 1997”. The amount was received by

Barbara because she was required to provide the personal service to get the

payment (Williams 2015). In other words, she was required to write the book before

being paid by the Eco Books Ltd. The significance of payment that was given to

Barbara was not simply to cover the outgoings incurred by taxpayer rather the

taxpayer here Barbara was motivated to render the service and the payment was the

product of income.

Finally, the manuscript of the books was sold by Barbara to the library and

she also sold the interview manuscripts to the library. The sale of manuscripts

yielded her money. Referring to “Housden v Marshall (1958)” selling of interview

manuscripts and books manuscripts along with the receipt of income thereon is a

taxable ordinary income under the judicial concept of “sec 6-5, ITAA 1997” (Smyth

et al. 2015).

If she simply writes the book in her leisure time and then sells the books to the

publisher for its publication. Any amount derived thereon by Barbara will be treated

as income from the personal service exertion and taxable under the ordinary

meaning of “sec 6-5, ITAA 1997”.

consider the personal exertion income as income case laws such as “Brent v FCT

(1971)” is approached (Morrison 2015). The was held for deriving taxable earnings

when she was given money for telling the story of her life to the newspaper in order

to make exclusive publication.

In view of that, another example can be considered of “Hobbs v Hussey

(1942)” where the notorious criminal received £1,500 for selling the autobiography to

the publisher for making an exclusive publication of the story in the newspaper article

(Pert et al. 2016). The quantum of the payment that is made to the taxpayer is not to

simply cover the cost or the inconvenience.

In another example of “Housden v Marshall (1958)” the taxpayer was the

taxable when he sold the experience of Jockey which also included the photographs

and the cuttings of newspaper (Graetz 2015). The amount received was ordinary

income and taxable under the ordinary meaning of “sec 6-5, ITAA 1997”.

Application:

Barbara is the economist and also a research commentator. A publisher

named Eco Books Ltd provided Barbara with the $13,000 to write book on

economics. She accepted the offer and wrote the book named as Principle of

Economics. The sum of $13,000 relates to Barbara’s provision of services.

Additionally, discussing the example of “Brent v FCT (1971)” the payment is having

nexus among the services that is rendered and the earning activity (Kenny 2015).

The character of payment that is received in the hand of Barbara is personal exertion

income under “sec 6 (1), ITAA 1997”. The amount will be taxable as ordinary

earnings within the judicial meaning of “sec 6-5, ITAA 1997”.

She later assigned the copyright of Principle of Economics to the Eco Books

Ltd. The amount paid to sell the copyright of book was $13,400. Discussing the

similar case example of “Hobbs v Hussey (1942)” selling the copyright to publisher

by assigning the copyright of the books by Barbara is a taxable ordinary income

under the judicial meaning of “sec 6-5, ITAA 1997”. The amount was received by

Barbara because she was required to provide the personal service to get the

payment (Williams 2015). In other words, she was required to write the book before

being paid by the Eco Books Ltd. The significance of payment that was given to

Barbara was not simply to cover the outgoings incurred by taxpayer rather the

taxpayer here Barbara was motivated to render the service and the payment was the

product of income.

Finally, the manuscript of the books was sold by Barbara to the library and

she also sold the interview manuscripts to the library. The sale of manuscripts

yielded her money. Referring to “Housden v Marshall (1958)” selling of interview

manuscripts and books manuscripts along with the receipt of income thereon is a

taxable ordinary income under the judicial concept of “sec 6-5, ITAA 1997” (Smyth

et al. 2015).

If she simply writes the book in her leisure time and then sells the books to the

publisher for its publication. Any amount derived thereon by Barbara will be treated

as income from the personal service exertion and taxable under the ordinary

meaning of “sec 6-5, ITAA 1997”.

5TAXATION LAW

Conclusion:

The monies received by Barbara is exclusively from the personal exertion.

The amount will be taxable under the judicial concept of “sec 6-5, ITAA 1997” as

the ordinary earnings.

Answer to question 3:

Issues:

Is the one-off receipt of interest earned by the taxpayer from providing loan is

a taxable as income under “sec 6-5, ITAA 1997”?

Rule:

The taxable income comprises of the ordinary income and the statutory

income. Ordinary income is usually considered as income the courts have

ascertained usually by implementing the definition of income based on the ordinary

concepts. “Sec 6-5 (1)” assesses the ordinary income for tax (Mortimore 2015). The

taxpayer’s taxable income comprises of the income based on the ordinary earnings

concept. To characterise the income it is necessary to take into the account its

necessary characteristics. This includes whether the receipt that is earned is easily

convertible to cash and is a money. Characterising the receipts as income usually

involve determining whether the receipts are holding periodicity, recurrence and

regularity. The receipts from the income generating activities are generally held as

ordinary earnings.

It is worth mentioning that ordinary earnings generally have two prerequisites.

This involves whether the receipts are a real gain for the receiver and whether the

receipts are convertible into cash. The court of law in the “Hochstrasser v Mayes

(1960)” explained that if the receipt cannot be considered as the genuine gain then it

is not held as the ordinary income (Lam and Whitney 2016). As long as the

prerequisites of the ordinary income is satisfied, the gains will be considered as the

ordinary income and may show the sufficient characteristics of income. Most notably,

the one-off receipts are not held as the ordinary income. Similarly, the lump sum

gains may be held as the ordinary income if the one-off receipt of the interest under

the agreement of loan is held as ordinary income.

Applications:

The rules that is explained above can be applied in the situation of Patrick and

his son David. A loan was given to David by Patrick with the loan period of five

years. Patrick was also required to pay the loan with the interest amount of $6,000

as the interest on loan. The son here paid the loan amount through cheque and in

addition to this also paid 5% on the borrowing sum as the interest for loan taken.

The interest that is received by Patrick should be viewed as the real gain to

the taxpayer and has the characteristics of income. The receipt of interest is fulfilling

both the prerequisite since it is easily convertible cash and also a real gain. Citing

the case of “Hochstrasser v Mayes (1960)” the one-off receipt of interest from the

loan agreement is the real gain and it is an ordinary income under “sec 6-5, ITAA

1997” (Waterhouse 2015).

Conclusion:

The monies received by Barbara is exclusively from the personal exertion.

The amount will be taxable under the judicial concept of “sec 6-5, ITAA 1997” as

the ordinary earnings.

Answer to question 3:

Issues:

Is the one-off receipt of interest earned by the taxpayer from providing loan is

a taxable as income under “sec 6-5, ITAA 1997”?

Rule:

The taxable income comprises of the ordinary income and the statutory

income. Ordinary income is usually considered as income the courts have

ascertained usually by implementing the definition of income based on the ordinary

concepts. “Sec 6-5 (1)” assesses the ordinary income for tax (Mortimore 2015). The

taxpayer’s taxable income comprises of the income based on the ordinary earnings

concept. To characterise the income it is necessary to take into the account its

necessary characteristics. This includes whether the receipt that is earned is easily

convertible to cash and is a money. Characterising the receipts as income usually

involve determining whether the receipts are holding periodicity, recurrence and

regularity. The receipts from the income generating activities are generally held as

ordinary earnings.

It is worth mentioning that ordinary earnings generally have two prerequisites.

This involves whether the receipts are a real gain for the receiver and whether the

receipts are convertible into cash. The court of law in the “Hochstrasser v Mayes

(1960)” explained that if the receipt cannot be considered as the genuine gain then it

is not held as the ordinary income (Lam and Whitney 2016). As long as the

prerequisites of the ordinary income is satisfied, the gains will be considered as the

ordinary income and may show the sufficient characteristics of income. Most notably,

the one-off receipts are not held as the ordinary income. Similarly, the lump sum

gains may be held as the ordinary income if the one-off receipt of the interest under

the agreement of loan is held as ordinary income.

Applications:

The rules that is explained above can be applied in the situation of Patrick and

his son David. A loan was given to David by Patrick with the loan period of five

years. Patrick was also required to pay the loan with the interest amount of $6,000

as the interest on loan. The son here paid the loan amount through cheque and in

addition to this also paid 5% on the borrowing sum as the interest for loan taken.

The interest that is received by Patrick should be viewed as the real gain to

the taxpayer and has the characteristics of income. The receipt of interest is fulfilling

both the prerequisite since it is easily convertible cash and also a real gain. Citing

the case of “Hochstrasser v Mayes (1960)” the one-off receipt of interest from the

loan agreement is the real gain and it is an ordinary income under “sec 6-5, ITAA

1997” (Waterhouse 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Finally, to determine the tax liability of the interest income the mode of

payment that is utilised by son does not affect the tax position (Samiec and Bale

2016). The taxpayer here Patrick will be only held assessable for the interest amount

that is received in respect of the loan given to son. While the overall loan amount will

not be held taxable because it is a capital amount and non-taxable.

Conclusion:

On arriving at the conclusive note, it can be stated that the interest on loan

that is received by the father here, Patrick will be considered as the taxable income

under “sec 6-5, ITAA 1997” since it is a real gain for the taxpayer.

Finally, to determine the tax liability of the interest income the mode of

payment that is utilised by son does not affect the tax position (Samiec and Bale

2016). The taxpayer here Patrick will be only held assessable for the interest amount

that is received in respect of the loan given to son. While the overall loan amount will

not be held taxable because it is a capital amount and non-taxable.

Conclusion:

On arriving at the conclusive note, it can be stated that the interest on loan

that is received by the father here, Patrick will be considered as the taxable income

under “sec 6-5, ITAA 1997” since it is a real gain for the taxpayer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

References:

Graetz, Michael J, 2015. Can a 20th century business income tax regime serve a 21st

century economy? Australian Tax Forum, 30(3), pp.551–567.

Harding, M. and Marten, M., 2018. Statutory tax rates on dividends, interest and

capital gains.

He, E., Jacob, M., Vashishtha, R. and Venkatachalam, M., 2019. The effect of capital

gains tax policy changes on long-term investments. Available at SSRN 3383649.

Hellwig, T. and McAllister, I., 2018. The impact of economic assets on party choice in

Australia. Journal of Elections, Public Opinion and Parties, 28(4), pp.516-534.

Kenny, P. et al., 2015. Australian tax 2015, Chatswood: LexisNexis Butterworths.

Khoury, Daniel, 2014. Widening the availability of deductions under Australian taxation

law. Tax Specialist, 14(4), pp.207–211.

Lam, Dung and Whitney, Alex, 2016. Taxation and property: Practical aspects of the

new foreign resident CGT witholding tax. LSJ: Law Society of NSW Journal, (21), pp.84–

85.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on

capital gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33,

No. 4).

Morrison, D., 2015. Never mind the law, just hurry up and collect more tax! The ATO

persists with unnecessary litigation. Insolvency Law Journal, 23(4), pp.196–208.

Mortimore, Anna, 2015. Will cars go green in the ACT?: A case study of the

reformed vehicle stamp duty. Australian Tax Forum, 30(1), pp.205-[254].

Pert, Alison, Abi-Hanna, Stephanie and Smith, Cassandra, 2016. Macoun v

Commissioner of Taxation [2015] HCA 44. Australian Year Book of International Law,

34, pp.207–210.

Samiec, J. and Bale, S., 2016. Australian practice in international law 2015. Australian

Yearbook of International Law, 34, pp.297–475.

Smyth, Christine, 2015. What's new in succession law: Death and taxes: Executor's

commission ATO ID 2014/44. Proctor, The, 35(3), p.42.

Waterhouse, Tania, 2015. Taxation: Fear not the ATO: Handy tips for lawyers. LSJ: Law

Society of NSW Journal, 2(5), pp.92–93.

Williams, G., 2015. BRYAN PAPE AND HIS LEGACY TO THE LAW. University of

Queensland Law Journal, 34(1), pp.29–46.

References:

Graetz, Michael J, 2015. Can a 20th century business income tax regime serve a 21st

century economy? Australian Tax Forum, 30(3), pp.551–567.

Harding, M. and Marten, M., 2018. Statutory tax rates on dividends, interest and

capital gains.

He, E., Jacob, M., Vashishtha, R. and Venkatachalam, M., 2019. The effect of capital

gains tax policy changes on long-term investments. Available at SSRN 3383649.

Hellwig, T. and McAllister, I., 2018. The impact of economic assets on party choice in

Australia. Journal of Elections, Public Opinion and Parties, 28(4), pp.516-534.

Kenny, P. et al., 2015. Australian tax 2015, Chatswood: LexisNexis Butterworths.

Khoury, Daniel, 2014. Widening the availability of deductions under Australian taxation

law. Tax Specialist, 14(4), pp.207–211.

Lam, Dung and Whitney, Alex, 2016. Taxation and property: Practical aspects of the

new foreign resident CGT witholding tax. LSJ: Law Society of NSW Journal, (21), pp.84–

85.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on

capital gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33,

No. 4).

Morrison, D., 2015. Never mind the law, just hurry up and collect more tax! The ATO

persists with unnecessary litigation. Insolvency Law Journal, 23(4), pp.196–208.

Mortimore, Anna, 2015. Will cars go green in the ACT?: A case study of the

reformed vehicle stamp duty. Australian Tax Forum, 30(1), pp.205-[254].

Pert, Alison, Abi-Hanna, Stephanie and Smith, Cassandra, 2016. Macoun v

Commissioner of Taxation [2015] HCA 44. Australian Year Book of International Law,

34, pp.207–210.

Samiec, J. and Bale, S., 2016. Australian practice in international law 2015. Australian

Yearbook of International Law, 34, pp.297–475.

Smyth, Christine, 2015. What's new in succession law: Death and taxes: Executor's

commission ATO ID 2014/44. Proctor, The, 35(3), p.42.

Waterhouse, Tania, 2015. Taxation: Fear not the ATO: Handy tips for lawyers. LSJ: Law

Society of NSW Journal, 2(5), pp.92–93.

Williams, G., 2015. BRYAN PAPE AND HIS LEGACY TO THE LAW. University of

Queensland Law Journal, 34(1), pp.29–46.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.