Holms Institute HA3042 Taxation Law Assignment: CGT, Depreciation

VerifiedAdded on 2022/11/17

|11

|2720

|138

Homework Assignment

AI Summary

This taxation law assignment provides a comprehensive analysis of several key areas within the Australian tax system. The first part addresses capital gains tax (CGT) implications for various scenarios, including the sale of land (main residence and pre-CGT assets), cars (personal use assets), business assets (small business concessions), and personal assets such as furniture and paintings (collectables). The analysis considers relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and case law. The second part focuses on depreciation, specifically examining the deductibility of depreciation expenses for a CNC machine used in a business context. It explores the definition of depreciating assets, the determination of the cost base, and the timing of deductions under Division 40 of the ITAA 1997, referencing relevant case law like Wangaratta Woollen Mills Ltd v FCT (1969) and Broken Hill Pty Co Ltd v. FCT (1970). The assignment aims to demonstrate an understanding of tax law principles and their application to practical scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

Sale of Land:

As clarified in “sec 100-25 (1), ITAA 1997” the CGT system restricts the asset on

which Pt 3 is applicable to those that are purchased on or following 20 September 1985. The

provision of the capital gains tax is applicable on the actual or the realised gains (McCluskey

and Franzsen 2017). The capital gains tax are generally held for tax under the statutory

income under “sec 6-10” and the same is comprised in the taxable earning with respect to

“sec 102-5 (1), ITAA 1997”. The vital operative provision of the CGT regime is given in

“sec 102-5 (1)” which takes into the account the net capital gains in the assessable income.

Disposal of the CGT asset under CGT Event A1 is given in “sec 104-10, ITA Act 1997”. The

“CGT event A1” happens when the asset purchased on or after 20/9/1985 (McCluskey 2018).

The CGT must be disposed to another entity by the taxpayer. The “CGT event A1” is only

applied on assets purchased on that date only however assets purchased before the

aforementioned date is exempted from CGT.

As per the “Div 118-B” the general principles associated to the main residence is that

capital gain or loss from sale of house of the taxpayer is exempted or disregarded under “sec

118-110” (Mankiw, Weinzierl and Yagan 2019). The house should completely be used by

taxpayer for residence purpose only and should not be used for earning income.

A home was purchased in 1981 by paying $40,000 by Jasmine. As she is retiring from

her business and moving back to UK, Jasmine sold the house for $650,000. A “CGT event

A1” occurred in “sec 104-10 (1), ITAA 1997” when the house was sold (Cnossen 2015). The

house is a main residence of Jasmine which should be treated as a pre-CGT asset because it

was purchased in 1982 which is before the CGT system was introduced in 19/9/1985. No

CGT liability arises for Jasmine as it is a pre-CGT asset.

Answer to question 1:

Sale of Land:

As clarified in “sec 100-25 (1), ITAA 1997” the CGT system restricts the asset on

which Pt 3 is applicable to those that are purchased on or following 20 September 1985. The

provision of the capital gains tax is applicable on the actual or the realised gains (McCluskey

and Franzsen 2017). The capital gains tax are generally held for tax under the statutory

income under “sec 6-10” and the same is comprised in the taxable earning with respect to

“sec 102-5 (1), ITAA 1997”. The vital operative provision of the CGT regime is given in

“sec 102-5 (1)” which takes into the account the net capital gains in the assessable income.

Disposal of the CGT asset under CGT Event A1 is given in “sec 104-10, ITA Act 1997”. The

“CGT event A1” happens when the asset purchased on or after 20/9/1985 (McCluskey 2018).

The CGT must be disposed to another entity by the taxpayer. The “CGT event A1” is only

applied on assets purchased on that date only however assets purchased before the

aforementioned date is exempted from CGT.

As per the “Div 118-B” the general principles associated to the main residence is that

capital gain or loss from sale of house of the taxpayer is exempted or disregarded under “sec

118-110” (Mankiw, Weinzierl and Yagan 2019). The house should completely be used by

taxpayer for residence purpose only and should not be used for earning income.

A home was purchased in 1981 by paying $40,000 by Jasmine. As she is retiring from

her business and moving back to UK, Jasmine sold the house for $650,000. A “CGT event

A1” occurred in “sec 104-10 (1), ITAA 1997” when the house was sold (Cnossen 2015). The

house is a main residence of Jasmine which should be treated as a pre-CGT asset because it

was purchased in 1982 which is before the CGT system was introduced in 19/9/1985. No

CGT liability arises for Jasmine as it is a pre-CGT asset.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Capital gain or loss from car:

This is defined under “sec 108-20 (2)” which is used by taxpayer for personal purpose

and enjoyment. Common examples are television, car, bicycle, yacht and mobile phone that

are kept for private use (Nightingale 2014). Taxpayer must denote that under “sec 108-20

(1)”, when a capital loss happens from selling personal use asset then it is always ignored.

The situation here states that Jasmine sold a car for $10,000 that originally had the

worth of $31,000 in 2011. Car here is regarded as personal use asset under “s 108-20 (2)”.

Disposal of car has led to “CGT event A1”. The capital loss that is suffered from selling the

car should be ignored by Jasmine under “s 108-20 (1), ITA Act 1997”.

Capital gain in relation to sale of business:

There are four CGT concessions that can be accessible by taxpayer for the small

business when they sale their business assets. These are;

a. 15 year exemption: This is mainly for assets held for a minimum of 15 years.

b. The 50% reduction: Eligible taxpayers get 50% CGT discount

c. Retirement concession: Capital gains of $500,000 is ignored if the sales proceeds are

utilized in relation to taxpayer’s retirement (Burman et al., 2016).

d. Rollover relief: Capital gains from small business active asset is deferred when it is

replaced by another purchase of assets.

When a business goodwill is disposed a “CGT event C1” ensues. There must be a

perpetual end of business for happening of “CGT event C1”.

Jasmine here sold is moving to UK and sells all her business for $125,000. On selling

the assets Jasmine got $65,000 while selling her business goodwill it fetched her $60,000.

Capital gain or loss from car:

This is defined under “sec 108-20 (2)” which is used by taxpayer for personal purpose

and enjoyment. Common examples are television, car, bicycle, yacht and mobile phone that

are kept for private use (Nightingale 2014). Taxpayer must denote that under “sec 108-20

(1)”, when a capital loss happens from selling personal use asset then it is always ignored.

The situation here states that Jasmine sold a car for $10,000 that originally had the

worth of $31,000 in 2011. Car here is regarded as personal use asset under “s 108-20 (2)”.

Disposal of car has led to “CGT event A1”. The capital loss that is suffered from selling the

car should be ignored by Jasmine under “s 108-20 (1), ITA Act 1997”.

Capital gain in relation to sale of business:

There are four CGT concessions that can be accessible by taxpayer for the small

business when they sale their business assets. These are;

a. 15 year exemption: This is mainly for assets held for a minimum of 15 years.

b. The 50% reduction: Eligible taxpayers get 50% CGT discount

c. Retirement concession: Capital gains of $500,000 is ignored if the sales proceeds are

utilized in relation to taxpayer’s retirement (Burman et al., 2016).

d. Rollover relief: Capital gains from small business active asset is deferred when it is

replaced by another purchase of assets.

When a business goodwill is disposed a “CGT event C1” ensues. There must be a

perpetual end of business for happening of “CGT event C1”.

Jasmine here sold is moving to UK and sells all her business for $125,000. On selling

the assets Jasmine got $65,000 while selling her business goodwill it fetched her $60,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Jasmine here can obtain a small business concession on CGT assets from her capital gains.

As Jasmine is retiring from her business she can obtain a retirement concession for her CGT

assets and business goodwill because her capital gains is below $500,000.

Capital gain for sale of furniture:

Taxpayers must denote that some special rules given in “sec 118-10 (3), ITA Act

1997” requires taxpayers to disregard capital gains made from the personal assets (Wanless

2018). This includes the situation when capital gains happens for a furniture which was

purchased for $10,000 or less. Here Jasmine made capital gains from selling her furniture

which was purchased for $2,000. The furniture were eventually sold for $5,000. As furniture

has been classified as personal use asset under “sec 104-10 (1)”, the capital gains that is

earned from selling the furniture should be ignored under “sec 118- 10 (3)”, because the first

element cost base of personal use asset is not met here. Hence the furniture cost below $10k

and capital gains must be disregarded by Jasmine in this circumstances.

Capital gains on sale of paintings:

Accordingly in “sec 108-10, ITA Act 1997” collectables implies those assets that are

a. Kept for own usage and enjoyment by taxpayer

b. Assets listed in “sec 108-10 (2), ITA Act 1997” such as paintings, jewellery, rare

stamps etc.

The noteworthy rule under “sec 118-10 (1)” for taxpayers regarding collectables is

that capital gains or loss is simply not taken into account when first element cost base of asset

is below $500.

As noticed several paintings were owned by Jasmine. The paintings here amounts to

collectibles under “sec 108-10 (2), ITA Act 1997” that she has kept for own enjoyment and

Jasmine here can obtain a small business concession on CGT assets from her capital gains.

As Jasmine is retiring from her business she can obtain a retirement concession for her CGT

assets and business goodwill because her capital gains is below $500,000.

Capital gain for sale of furniture:

Taxpayers must denote that some special rules given in “sec 118-10 (3), ITA Act

1997” requires taxpayers to disregard capital gains made from the personal assets (Wanless

2018). This includes the situation when capital gains happens for a furniture which was

purchased for $10,000 or less. Here Jasmine made capital gains from selling her furniture

which was purchased for $2,000. The furniture were eventually sold for $5,000. As furniture

has been classified as personal use asset under “sec 104-10 (1)”, the capital gains that is

earned from selling the furniture should be ignored under “sec 118- 10 (3)”, because the first

element cost base of personal use asset is not met here. Hence the furniture cost below $10k

and capital gains must be disregarded by Jasmine in this circumstances.

Capital gains on sale of paintings:

Accordingly in “sec 108-10, ITA Act 1997” collectables implies those assets that are

a. Kept for own usage and enjoyment by taxpayer

b. Assets listed in “sec 108-10 (2), ITA Act 1997” such as paintings, jewellery, rare

stamps etc.

The noteworthy rule under “sec 118-10 (1)” for taxpayers regarding collectables is

that capital gains or loss is simply not taken into account when first element cost base of asset

is below $500.

As noticed several paintings were owned by Jasmine. The paintings here amounts to

collectibles under “sec 108-10 (2), ITA Act 1997” that she has kept for own enjoyment and

5TAXATION LAW

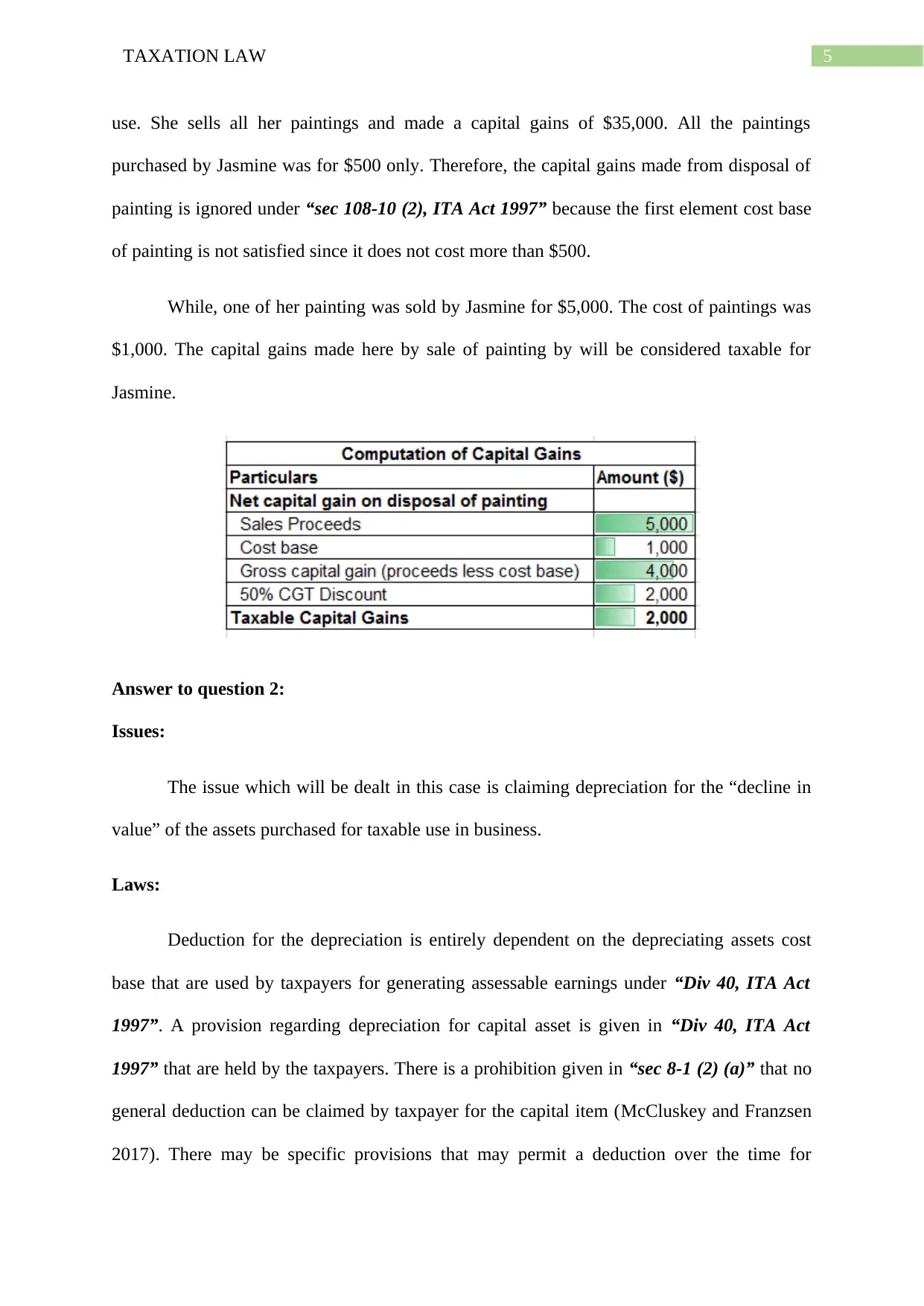

use. She sells all her paintings and made a capital gains of $35,000. All the paintings

purchased by Jasmine was for $500 only. Therefore, the capital gains made from disposal of

painting is ignored under “sec 108-10 (2), ITA Act 1997” because the first element cost base

of painting is not satisfied since it does not cost more than $500.

While, one of her painting was sold by Jasmine for $5,000. The cost of paintings was

$1,000. The capital gains made here by sale of painting by will be considered taxable for

Jasmine.

Answer to question 2:

Issues:

The issue which will be dealt in this case is claiming depreciation for the “decline in

value” of the assets purchased for taxable use in business.

Laws:

Deduction for the depreciation is entirely dependent on the depreciating assets cost

base that are used by taxpayers for generating assessable earnings under “Div 40, ITA Act

1997”. A provision regarding depreciation for capital asset is given in “Div 40, ITA Act

1997” that are held by the taxpayers. There is a prohibition given in “sec 8-1 (2) (a)” that no

general deduction can be claimed by taxpayer for the capital item (McCluskey and Franzsen

2017). There may be specific provisions that may permit a deduction over the time for

use. She sells all her paintings and made a capital gains of $35,000. All the paintings

purchased by Jasmine was for $500 only. Therefore, the capital gains made from disposal of

painting is ignored under “sec 108-10 (2), ITA Act 1997” because the first element cost base

of painting is not satisfied since it does not cost more than $500.

While, one of her painting was sold by Jasmine for $5,000. The cost of paintings was

$1,000. The capital gains made here by sale of painting by will be considered taxable for

Jasmine.

Answer to question 2:

Issues:

The issue which will be dealt in this case is claiming depreciation for the “decline in

value” of the assets purchased for taxable use in business.

Laws:

Deduction for the depreciation is entirely dependent on the depreciating assets cost

base that are used by taxpayers for generating assessable earnings under “Div 40, ITA Act

1997”. A provision regarding depreciation for capital asset is given in “Div 40, ITA Act

1997” that are held by the taxpayers. There is a prohibition given in “sec 8-1 (2) (a)” that no

general deduction can be claimed by taxpayer for the capital item (McCluskey and Franzsen

2017). There may be specific provisions that may permit a deduction over the time for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

outgoings that are anticipated to generate benefit. It is worth noting for taxpayers that they are

entitled to equivalent deduction for “depreciating assets” decline in value which they have

held under “sec 40-25, ITAA 1997”. Taxpayers should denote that deduction is claimed for

assets over their useful life.

There is an important definition given in “sec 40-30 (1), ITAA 1997” regarding the

depreciating asset. As per this provision an asset that only has the limited life and they are

anticipated to fall in their value over the time based on their usage (Miller and Oats 2016).

The taxpayers should denote that if they want to obtain a deduction for “depreciating asset”

under “sec 40-25, ITA Act 1997” then they should determine that they have held the

depreciating asset and the deduction is equal to “decline in value” by considering the taxable

purpose of asset.

Most notably, the taxpayers must take into account that “decline in value” is only

permitted for claim in regard to depreciating asset which is used for assessable business

purpose under “s 40-25 (2), ITA Act 1997” (Kothari 2017). An assessable business purpose

most commonly happens when the asset is employed in business for generating income under

“sec 40-25 (7)”. While a deduction may be reduced in terms of percentage for any non-

taxable purpose.

Where a taxpayer holds a “deprecating asset” begins to fall when the start time

happens in “sec 40-60, ITA Act 1997”. This generally involves the time when the taxpayer at

the initial stages uses the asset or they have installed it for ready usage for any purpose

(Brown 2017). The court in “Wangaratta Woollen Mills Ltd v FCT (1969)” defined

depreciating asset as something that are used by business man for conducing the business.

“Sub-Div 40-C” articulates that for depreciation purpose the cost base of depreciating

asset is regarded as the total cost of the asset. Usually, it will take into account only the

outgoings that are anticipated to generate benefit. It is worth noting for taxpayers that they are

entitled to equivalent deduction for “depreciating assets” decline in value which they have

held under “sec 40-25, ITAA 1997”. Taxpayers should denote that deduction is claimed for

assets over their useful life.

There is an important definition given in “sec 40-30 (1), ITAA 1997” regarding the

depreciating asset. As per this provision an asset that only has the limited life and they are

anticipated to fall in their value over the time based on their usage (Miller and Oats 2016).

The taxpayers should denote that if they want to obtain a deduction for “depreciating asset”

under “sec 40-25, ITA Act 1997” then they should determine that they have held the

depreciating asset and the deduction is equal to “decline in value” by considering the taxable

purpose of asset.

Most notably, the taxpayers must take into account that “decline in value” is only

permitted for claim in regard to depreciating asset which is used for assessable business

purpose under “s 40-25 (2), ITA Act 1997” (Kothari 2017). An assessable business purpose

most commonly happens when the asset is employed in business for generating income under

“sec 40-25 (7)”. While a deduction may be reduced in terms of percentage for any non-

taxable purpose.

Where a taxpayer holds a “deprecating asset” begins to fall when the start time

happens in “sec 40-60, ITA Act 1997”. This generally involves the time when the taxpayer at

the initial stages uses the asset or they have installed it for ready usage for any purpose

(Brown 2017). The court in “Wangaratta Woollen Mills Ltd v FCT (1969)” defined

depreciating asset as something that are used by business man for conducing the business.

“Sub-Div 40-C” articulates that for depreciation purpose the cost base of depreciating

asset is regarded as the total cost of the asset. Usually, it will take into account only the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

purchase price that is paid to acquire the asset but may also include the incidental costs of the

delivery and installation (Turley 2017). The verdict handed in “Broken Hill Pty Co Ltd v.

FCT (1970)” minor rearrangement expenses that happens to the plant is also contained

within in the cost base.

The legislation of “sec 40-175, ITA Act 1997” provides the classification of the cost

base of depreciation asset in two elements (Dennis-Escoffier and Fortin 2016). The specific

rules that are contained in “sec 40-180, ITA Act 1997” says that the first element is computed

when a taxpayer holds the depreciating asset such as the amount paid to purchase the asset

under “sec 40-185”. Whereas, “sec 40-190” mainly provides explanation regarding second

element. This widely includes the cost that is paid for delivery, installation and capital

improvements that a taxpayer makes to the depreciating asset when they have held asset in

their business course of producing income.

Application:

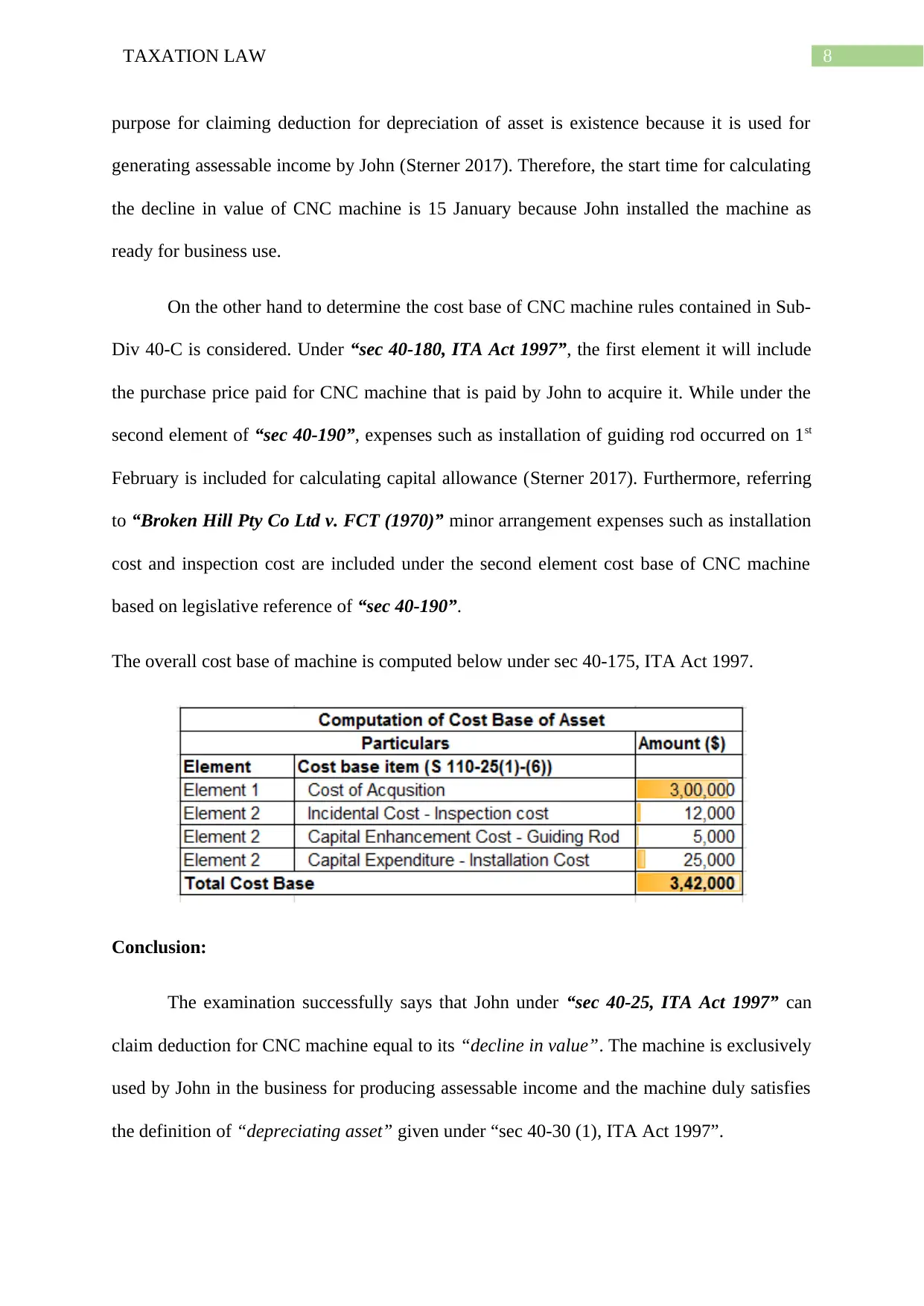

As understood here, John carries a certified business of BMW parts. He went to

Germany to inspect the CNC machine and on 1st November 2014 he eventually imported the

machine. John paid $300,000 for that CNC machine which he intends to use it for business

purpose. The CNC machine is referred as the depreciating asset under “sec 40-30 (1), ITA

Act 1997”. Citing the reference of “Wangaratta Woollen Mills Ltd v FCT (1969)” the CNC

machine has only limited effective usage and the machine is anticipated to fall in terms of

value till the time John uses it.

John here is allowed to get the deduction that is equivalent to “decline in value” of

CNC machine which he has held under sec 40-25. It can also be stated under “sec 40-25, ITA

Act 1997” John has held the CNC machine as the depreciating asset and he can get the

deduction for depreciation for taxable purpose. With regard to “sec 40-25 (7)”, the taxable

purchase price that is paid to acquire the asset but may also include the incidental costs of the

delivery and installation (Turley 2017). The verdict handed in “Broken Hill Pty Co Ltd v.

FCT (1970)” minor rearrangement expenses that happens to the plant is also contained

within in the cost base.

The legislation of “sec 40-175, ITA Act 1997” provides the classification of the cost

base of depreciation asset in two elements (Dennis-Escoffier and Fortin 2016). The specific

rules that are contained in “sec 40-180, ITA Act 1997” says that the first element is computed

when a taxpayer holds the depreciating asset such as the amount paid to purchase the asset

under “sec 40-185”. Whereas, “sec 40-190” mainly provides explanation regarding second

element. This widely includes the cost that is paid for delivery, installation and capital

improvements that a taxpayer makes to the depreciating asset when they have held asset in

their business course of producing income.

Application:

As understood here, John carries a certified business of BMW parts. He went to

Germany to inspect the CNC machine and on 1st November 2014 he eventually imported the

machine. John paid $300,000 for that CNC machine which he intends to use it for business

purpose. The CNC machine is referred as the depreciating asset under “sec 40-30 (1), ITA

Act 1997”. Citing the reference of “Wangaratta Woollen Mills Ltd v FCT (1969)” the CNC

machine has only limited effective usage and the machine is anticipated to fall in terms of

value till the time John uses it.

John here is allowed to get the deduction that is equivalent to “decline in value” of

CNC machine which he has held under sec 40-25. It can also be stated under “sec 40-25, ITA

Act 1997” John has held the CNC machine as the depreciating asset and he can get the

deduction for depreciation for taxable purpose. With regard to “sec 40-25 (7)”, the taxable

8TAXATION LAW

purpose for claiming deduction for depreciation of asset is existence because it is used for

generating assessable income by John (Sterner 2017). Therefore, the start time for calculating

the decline in value of CNC machine is 15 January because John installed the machine as

ready for business use.

On the other hand to determine the cost base of CNC machine rules contained in Sub-

Div 40-C is considered. Under “sec 40-180, ITA Act 1997”, the first element it will include

the purchase price paid for CNC machine that is paid by John to acquire it. While under the

second element of “sec 40-190”, expenses such as installation of guiding rod occurred on 1st

February is included for calculating capital allowance (Sterner 2017). Furthermore, referring

to “Broken Hill Pty Co Ltd v. FCT (1970)” minor arrangement expenses such as installation

cost and inspection cost are included under the second element cost base of CNC machine

based on legislative reference of “sec 40-190”.

The overall cost base of machine is computed below under sec 40-175, ITA Act 1997.

Conclusion:

The examination successfully says that John under “sec 40-25, ITA Act 1997” can

claim deduction for CNC machine equal to its “decline in value”. The machine is exclusively

used by John in the business for producing assessable income and the machine duly satisfies

the definition of “depreciating asset” given under “sec 40-30 (1), ITA Act 1997”.

purpose for claiming deduction for depreciation of asset is existence because it is used for

generating assessable income by John (Sterner 2017). Therefore, the start time for calculating

the decline in value of CNC machine is 15 January because John installed the machine as

ready for business use.

On the other hand to determine the cost base of CNC machine rules contained in Sub-

Div 40-C is considered. Under “sec 40-180, ITA Act 1997”, the first element it will include

the purchase price paid for CNC machine that is paid by John to acquire it. While under the

second element of “sec 40-190”, expenses such as installation of guiding rod occurred on 1st

February is included for calculating capital allowance (Sterner 2017). Furthermore, referring

to “Broken Hill Pty Co Ltd v. FCT (1970)” minor arrangement expenses such as installation

cost and inspection cost are included under the second element cost base of CNC machine

based on legislative reference of “sec 40-190”.

The overall cost base of machine is computed below under sec 40-175, ITA Act 1997.

Conclusion:

The examination successfully says that John under “sec 40-25, ITA Act 1997” can

claim deduction for CNC machine equal to its “decline in value”. The machine is exclusively

used by John in the business for producing assessable income and the machine duly satisfies

the definition of “depreciating asset” given under “sec 40-30 (1), ITA Act 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Brown, K.B., 2017. Taxation and Development: Overview. In Taxation and Development-A

Comparative Study (pp. 3-14). Springer, Cham.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016. Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), pp.171-216.

Cnossen, S. ed., 2015. Theory and practice of excise taxation: smoking, drinking, gambling,

polluting, and driving. Oxford University Press.

Dennis-Escoffier, S. and Fortin, K.A., 2016. Taxation for decision makers. John Wiley &

Sons.

Kothari, V., 2017. Applicability of Foreign Decisions and Interpretation of Tax Treaties in

International Taxation.

Mankiw, N.G., Weinzierl, M. and Yagan, D., 2019. Optimal taxation in theory and

practice. Journal of Economic Perspectives, 23(4), pp.147-74.

McCluskey, W., 2018. Property tax: An international comparative review. Routledge.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Nightingale, K., 2014. Taxation: theory and practice. Pearson Education.

Sterner, T., 2017. Environmental taxation in practice. Routledge.

References:

Brown, K.B., 2017. Taxation and Development: Overview. In Taxation and Development-A

Comparative Study (pp. 3-14). Springer, Cham.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016. Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), pp.171-216.

Cnossen, S. ed., 2015. Theory and practice of excise taxation: smoking, drinking, gambling,

polluting, and driving. Oxford University Press.

Dennis-Escoffier, S. and Fortin, K.A., 2016. Taxation for decision makers. John Wiley &

Sons.

Kothari, V., 2017. Applicability of Foreign Decisions and Interpretation of Tax Treaties in

International Taxation.

Mankiw, N.G., Weinzierl, M. and Yagan, D., 2019. Optimal taxation in theory and

practice. Journal of Economic Perspectives, 23(4), pp.147-74.

McCluskey, W., 2018. Property tax: An international comparative review. Routledge.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Nightingale, K., 2014. Taxation: theory and practice. Pearson Education.

Sterner, T., 2017. Environmental taxation in practice. Routledge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Turley, G., 2017. Transition, taxation and the State. Routledge.

Wanless, P.T., 2018. Taxation in centrally planned economies. Routledge.

Turley, G., 2017. Transition, taxation and the State. Routledge.

Wanless, P.T., 2018. Taxation in centrally planned economies. Routledge.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.