Taxation Law: Input Tax Credit and Capital Gains Tax

VerifiedAdded on 2022/10/16

|12

|2702

|364

AI Summary

This article discusses the entitlements associated with input tax credit and capital gains tax in the context of City Sky Co. It also explains the cost base and capital gains for the sale of a block of land, shares in Rio Tinto, stamps, and a piano.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Issues:

The entitlements associated to the claim of input tax credit entitlement will be

considered in the present study of City Sky Co.

Laws:

The tax treatment associated to the vacant land and the proceeds from selling is

usually reliant on whether the land is regarded as the capital asset or it is subject of business

or commercial transactions. In most of the occasion the vacant land is regarded as the capital

asset that is subjected to the capital gains tax (Graetz and Warren 2016). Nevertheless, on

noticing that the transactions relating to land is undertaken as the business part or activities of

enterprise any kind of sales proceeds will be considered subjected to ordinary income and

may attract GST liability. GST is usually payable on the commercial property and the

company that is buying a real property might account for the GST and recover the GST paid

through their business as the input tax credit. Vacant land is usually considered exempted

from GST when it is sold.

Essentially GST should be regarded as the consumption tax and the taxes are imposed

on the supply of goods and services in Australia and goods that are imported in Australia.

The application of the GST is usually made on the valued added taxable supply. Normally the

end users shoulder the accumulated cost of paying the GST (James 2017). GST should be

interpreted as transaction based tax. There are certain elements that are associated to the

transactions which are as follows;

a. Suppliers: The suppliers are the one that provides the business material of the supply.

Answer to question 1:

Issues:

The entitlements associated to the claim of input tax credit entitlement will be

considered in the present study of City Sky Co.

Laws:

The tax treatment associated to the vacant land and the proceeds from selling is

usually reliant on whether the land is regarded as the capital asset or it is subject of business

or commercial transactions. In most of the occasion the vacant land is regarded as the capital

asset that is subjected to the capital gains tax (Graetz and Warren 2016). Nevertheless, on

noticing that the transactions relating to land is undertaken as the business part or activities of

enterprise any kind of sales proceeds will be considered subjected to ordinary income and

may attract GST liability. GST is usually payable on the commercial property and the

company that is buying a real property might account for the GST and recover the GST paid

through their business as the input tax credit. Vacant land is usually considered exempted

from GST when it is sold.

Essentially GST should be regarded as the consumption tax and the taxes are imposed

on the supply of goods and services in Australia and goods that are imported in Australia.

The application of the GST is usually made on the valued added taxable supply. Normally the

end users shoulder the accumulated cost of paying the GST (James 2017). GST should be

interpreted as transaction based tax. There are certain elements that are associated to the

transactions which are as follows;

a. Suppliers: The suppliers are the one that provides the business material of the supply.

3TAXATION LAW

b. Recipient: This involves the receiver of the supply and are under obligation of paying

consideration for the supply.

A liability of paying the GST initiates under the legislation of “sec 9-40” and “sec 13-

15” when the chargeable supply and imports is made. The term taxable supply is given in the

“sec 9-5” which implies that the taxpayer makes the supply if there is any consideration in

exchange of price (Snape and De Souza 2016). The taxable is commonly made in the

business course of the enterprise and the supplies is usually connected with Australia. Most

importantly the taxable supply should be made to an entity is registered for GST. While “sec

9-15” emphasizes on the consideration and the liability of paying GST. Consideration usually

amounts to the payment or forbearance in relation with, or in response for incentive of supply

of anything. Commonly, consideration involves the price that is paid for the supply.

Typically, there should be a payment that should be made in relation to or as the inducement

of supply (Ong 2018). The decision that was given in “Waverley Council v CT (2009)”

clarified that the consideration is ought to have the connection with the supply but the supply

must be also made for the consideration.

The Australian taxation office provides the explanation regarding the conditions when

the reverse charge mechanism is applied. It says that there are some situations where the

liability of paying the GST simply falls on the purchaser. The rules of the reverse charge say

that the liability for GST happens when the Australian business purchase them (Brown 2017).

This commonly happens when the business activities are out from out of Australia or the

things that are made is with the help of business that is performed by the seller out of

Australia. As a result of this, the liability of paying the GST simply falls on the purchaser and

the seller is simply not required to pay the GST on sale.

b. Recipient: This involves the receiver of the supply and are under obligation of paying

consideration for the supply.

A liability of paying the GST initiates under the legislation of “sec 9-40” and “sec 13-

15” when the chargeable supply and imports is made. The term taxable supply is given in the

“sec 9-5” which implies that the taxpayer makes the supply if there is any consideration in

exchange of price (Snape and De Souza 2016). The taxable is commonly made in the

business course of the enterprise and the supplies is usually connected with Australia. Most

importantly the taxable supply should be made to an entity is registered for GST. While “sec

9-15” emphasizes on the consideration and the liability of paying GST. Consideration usually

amounts to the payment or forbearance in relation with, or in response for incentive of supply

of anything. Commonly, consideration involves the price that is paid for the supply.

Typically, there should be a payment that should be made in relation to or as the inducement

of supply (Ong 2018). The decision that was given in “Waverley Council v CT (2009)”

clarified that the consideration is ought to have the connection with the supply but the supply

must be also made for the consideration.

The Australian taxation office provides the explanation regarding the conditions when

the reverse charge mechanism is applied. It says that there are some situations where the

liability of paying the GST simply falls on the purchaser. The rules of the reverse charge say

that the liability for GST happens when the Australian business purchase them (Brown 2017).

This commonly happens when the business activities are out from out of Australia or the

things that are made is with the help of business that is performed by the seller out of

Australia. As a result of this, the liability of paying the GST simply falls on the purchaser and

the seller is simply not required to pay the GST on sale.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

The reverse charge rule is applicable if the business purchases the things absolutely

for the business purpose that is being carried on by them in Australia (Ingles 2016).

Moreover, the sale of the thing to the business is in exchange of payment and the business is

registered GST purpose. While there are also some important circumstances related to

purchase such as the sale that is made to the business is having the relations with Australia

and the purchase made to execute the business activities in Australia.

Application:

The information that is obtained from the above illuminated laws is applied in the

situation of City Sky Co. As understood the company has purchased the vacant land on which

it plans to build residential apartments for the purpose of sale. The vacant piece of land which

is bought by the City Sky Co must be viewed as the capital asset because the vacant land does

not attract GST. Even though it is noticed that City Sky Co is registered company for GST

purpose but the vacant is usually exempted from the GST. The vacant piece of land is not a

movable asset, it also does not amount to any goods and services. Henceforward, the vacant

piece of land cannot be considered taxable within the GST ambit. As the company is looking

forward to make residential apartments to ultimately sell it in the market, this falls within the

ambit of black credit. This implies that the vacant piece of land received by City Sky Co for

the construction of immovable property as the continuance of business is not falling within

the entitlements of input tax credit.

The case study of City Sky Co later details that it has taken the legal service from

Maurice Blackburn which is a legal adviser company registered for GST. The company

provided City Sky Co with the legal advice on land developmental service and billed

$33,000. The legal service is falling within the ambit of reverse charge mechanism where the

GST is paid on purchase made by City Sky Co. The supply of legal service to City Sky Co by

The reverse charge rule is applicable if the business purchases the things absolutely

for the business purpose that is being carried on by them in Australia (Ingles 2016).

Moreover, the sale of the thing to the business is in exchange of payment and the business is

registered GST purpose. While there are also some important circumstances related to

purchase such as the sale that is made to the business is having the relations with Australia

and the purchase made to execute the business activities in Australia.

Application:

The information that is obtained from the above illuminated laws is applied in the

situation of City Sky Co. As understood the company has purchased the vacant land on which

it plans to build residential apartments for the purpose of sale. The vacant piece of land which

is bought by the City Sky Co must be viewed as the capital asset because the vacant land does

not attract GST. Even though it is noticed that City Sky Co is registered company for GST

purpose but the vacant is usually exempted from the GST. The vacant piece of land is not a

movable asset, it also does not amount to any goods and services. Henceforward, the vacant

piece of land cannot be considered taxable within the GST ambit. As the company is looking

forward to make residential apartments to ultimately sell it in the market, this falls within the

ambit of black credit. This implies that the vacant piece of land received by City Sky Co for

the construction of immovable property as the continuance of business is not falling within

the entitlements of input tax credit.

The case study of City Sky Co later details that it has taken the legal service from

Maurice Blackburn which is a legal adviser company registered for GST. The company

provided City Sky Co with the legal advice on land developmental service and billed

$33,000. The legal service is falling within the ambit of reverse charge mechanism where the

GST is paid on purchase made by City Sky Co. The supply of legal service to City Sky Co by

5TAXATION LAW

Maurice Blackburn is a taxable supply that is made for consideration under “sec 9-15”.

Therefore, denoting the facts that was given in “Waverley Council v CT (2009)” the

consideration paid will be eligible for input tax credit (Dal Pont 2015). This is because the

legal services that was received by City Sky Co is mostly for the business activities that it is

conducting in Australia. The business is also registered for GST and supply of services is

connected with Australia. So an input tax credit is allowed for claim in this regard to City Sky

Co.

Conclusion:

The study comes to the conclusion that land is a fixed property and there cannot be

any GST implemented on it. Subsequently, City Sky Co is not permitted for claiming input

tax credit. The service relating to development of apartment that was sought from Maurice

Blackburn is an allowed for input tax claim.

Answer to question 2:

Sale of block of land:

CGT is treated as the form of statutory earnings and falls within the chapter 3 of the

ITAA 97. The definition that is given of capital proceeds inside “s.116-20 (1)”, is a money

that is received when selling the property. The proceeds are also considered as the market

value of a property which the taxpayer will be receiving when making its sale. Noticing the

explanation of “sec.116.20 (1)” there is no deduction allowed from the sale proceeds, rather

it is added to the cost base (Gilders et al. 2016). Most commonly the cost base of the CGT

asset inside “s.110-25 (1)” amounts to five elements. The first element is explained in

“sec.110-25(2)” which accounts for the purchase price paid by taxpayer.

The second element is called as incidental cost that a taxpayer pays involved in

purchase and sale inside “sec 110-25 (3)”. The list of cost under this are stamp duty, legal

Maurice Blackburn is a taxable supply that is made for consideration under “sec 9-15”.

Therefore, denoting the facts that was given in “Waverley Council v CT (2009)” the

consideration paid will be eligible for input tax credit (Dal Pont 2015). This is because the

legal services that was received by City Sky Co is mostly for the business activities that it is

conducting in Australia. The business is also registered for GST and supply of services is

connected with Australia. So an input tax credit is allowed for claim in this regard to City Sky

Co.

Conclusion:

The study comes to the conclusion that land is a fixed property and there cannot be

any GST implemented on it. Subsequently, City Sky Co is not permitted for claiming input

tax credit. The service relating to development of apartment that was sought from Maurice

Blackburn is an allowed for input tax claim.

Answer to question 2:

Sale of block of land:

CGT is treated as the form of statutory earnings and falls within the chapter 3 of the

ITAA 97. The definition that is given of capital proceeds inside “s.116-20 (1)”, is a money

that is received when selling the property. The proceeds are also considered as the market

value of a property which the taxpayer will be receiving when making its sale. Noticing the

explanation of “sec.116.20 (1)” there is no deduction allowed from the sale proceeds, rather

it is added to the cost base (Gilders et al. 2016). Most commonly the cost base of the CGT

asset inside “s.110-25 (1)” amounts to five elements. The first element is explained in

“sec.110-25(2)” which accounts for the purchase price paid by taxpayer.

The second element is called as incidental cost that a taxpayer pays involved in

purchase and sale inside “sec 110-25 (3)”. The list of cost under this are stamp duty, legal

6TAXATION LAW

fees etc. related to property at the time of purchase. The third element is the non-capital costs

that a taxpayer pays during the ownership of asset under “sec 110.25 (4)”. The list of cost

involves the borrowings interest, rates, insurance etc. incurred by taxpayer (Armenter and

Hnatkovska 2017). The fourth element is the capital outgoings when a taxpayer pays under

“sec 110.25 (5)” mainly for improving the asset. The final and fifth element is the capital

outgoings occurred for preserving, defending the rights and preserving the assets under

“sec.116-25 (6)”.

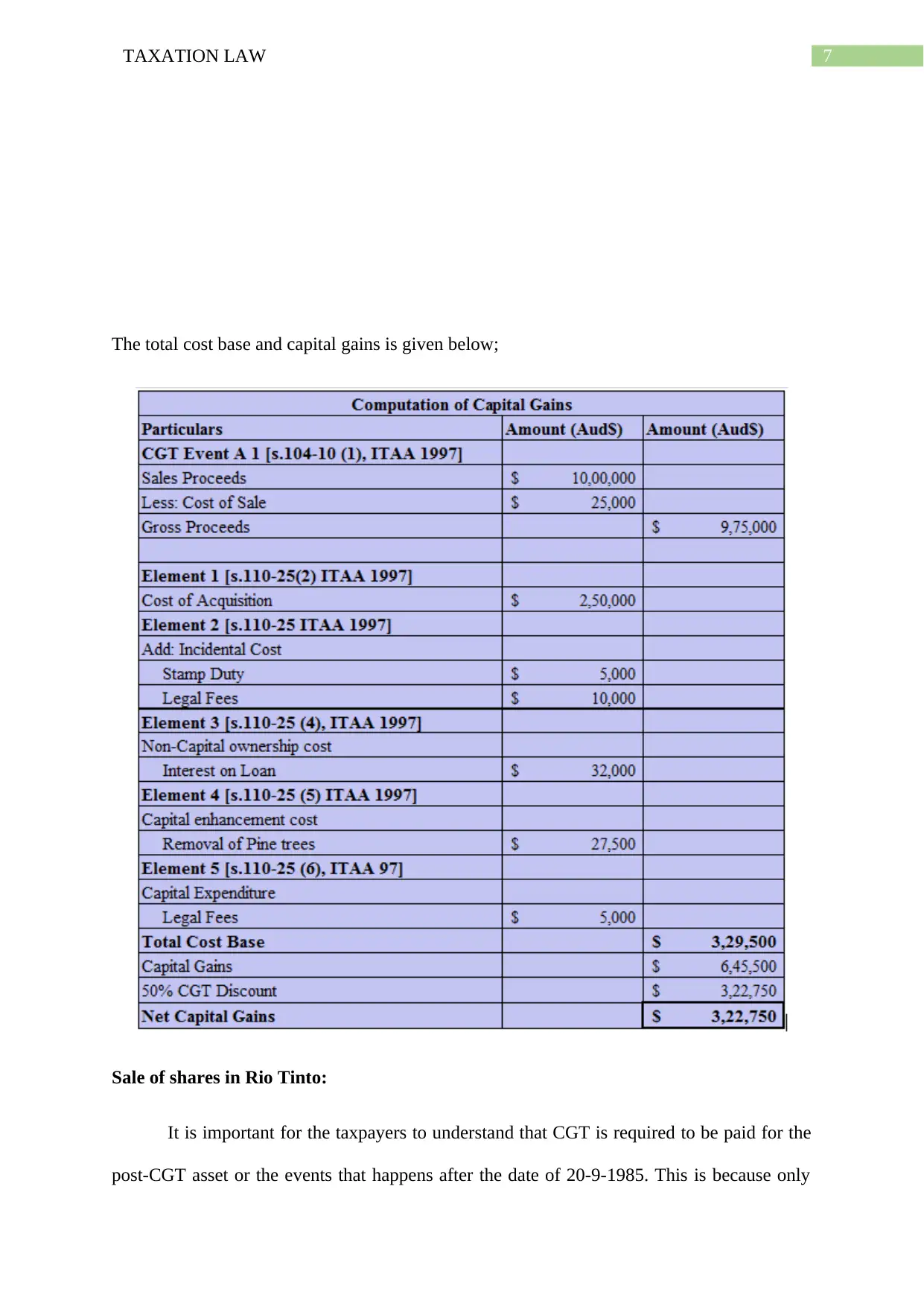

There is an evidence in the case study of Emma as she purchased a block of land for

$250,000 and sold it for $1,000,000. After the purchase of land, it was reported by Emma that

she incurred several cost. Under “sec 116-20 (1)” Emma must not that she cannot deduct the

cost from the sales proceeds as they are the part of her asset’s cost base (Becker, Reimer and

Rust 2015). The purchase price that Emma has paid for purchasing the land is the part of first

element cost of land within “sec.110-25 (2)”. The stamp duty and legal fees paid by Emma is

under “sec.110-25 (3)” an incidental cost of property. So it is added up in second element

cost base. The interest on loan that Emma has paid for the property is added in the cost base

because the asset was not used by Emma for generating income to claim deduction for the

cost. There were also outgoings incurred for water rates and insurance. These costs is also a

non-capital ownership charge and it is added in the property cost base.

Emma also paid legal fees to resolve the disagreement that occurred with neighbours

over the usage of land. The legal fees are added in the fifth element under “sec.110-25 (6)” as

it is a capital outgoing for her rights on the land. At last Emma further incurs cost on clearing

the pine trees located in the land (Kane 2015). The sum of $27,500 is added in fourth element

cost base under “sec.110-25 (5)” as capital outgoing for improving the assets value.

fees etc. related to property at the time of purchase. The third element is the non-capital costs

that a taxpayer pays during the ownership of asset under “sec 110.25 (4)”. The list of cost

involves the borrowings interest, rates, insurance etc. incurred by taxpayer (Armenter and

Hnatkovska 2017). The fourth element is the capital outgoings when a taxpayer pays under

“sec 110.25 (5)” mainly for improving the asset. The final and fifth element is the capital

outgoings occurred for preserving, defending the rights and preserving the assets under

“sec.116-25 (6)”.

There is an evidence in the case study of Emma as she purchased a block of land for

$250,000 and sold it for $1,000,000. After the purchase of land, it was reported by Emma that

she incurred several cost. Under “sec 116-20 (1)” Emma must not that she cannot deduct the

cost from the sales proceeds as they are the part of her asset’s cost base (Becker, Reimer and

Rust 2015). The purchase price that Emma has paid for purchasing the land is the part of first

element cost of land within “sec.110-25 (2)”. The stamp duty and legal fees paid by Emma is

under “sec.110-25 (3)” an incidental cost of property. So it is added up in second element

cost base. The interest on loan that Emma has paid for the property is added in the cost base

because the asset was not used by Emma for generating income to claim deduction for the

cost. There were also outgoings incurred for water rates and insurance. These costs is also a

non-capital ownership charge and it is added in the property cost base.

Emma also paid legal fees to resolve the disagreement that occurred with neighbours

over the usage of land. The legal fees are added in the fifth element under “sec.110-25 (6)” as

it is a capital outgoing for her rights on the land. At last Emma further incurs cost on clearing

the pine trees located in the land (Kane 2015). The sum of $27,500 is added in fourth element

cost base under “sec.110-25 (5)” as capital outgoing for improving the assets value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

The total cost base and capital gains is given below;

Sale of shares in Rio Tinto:

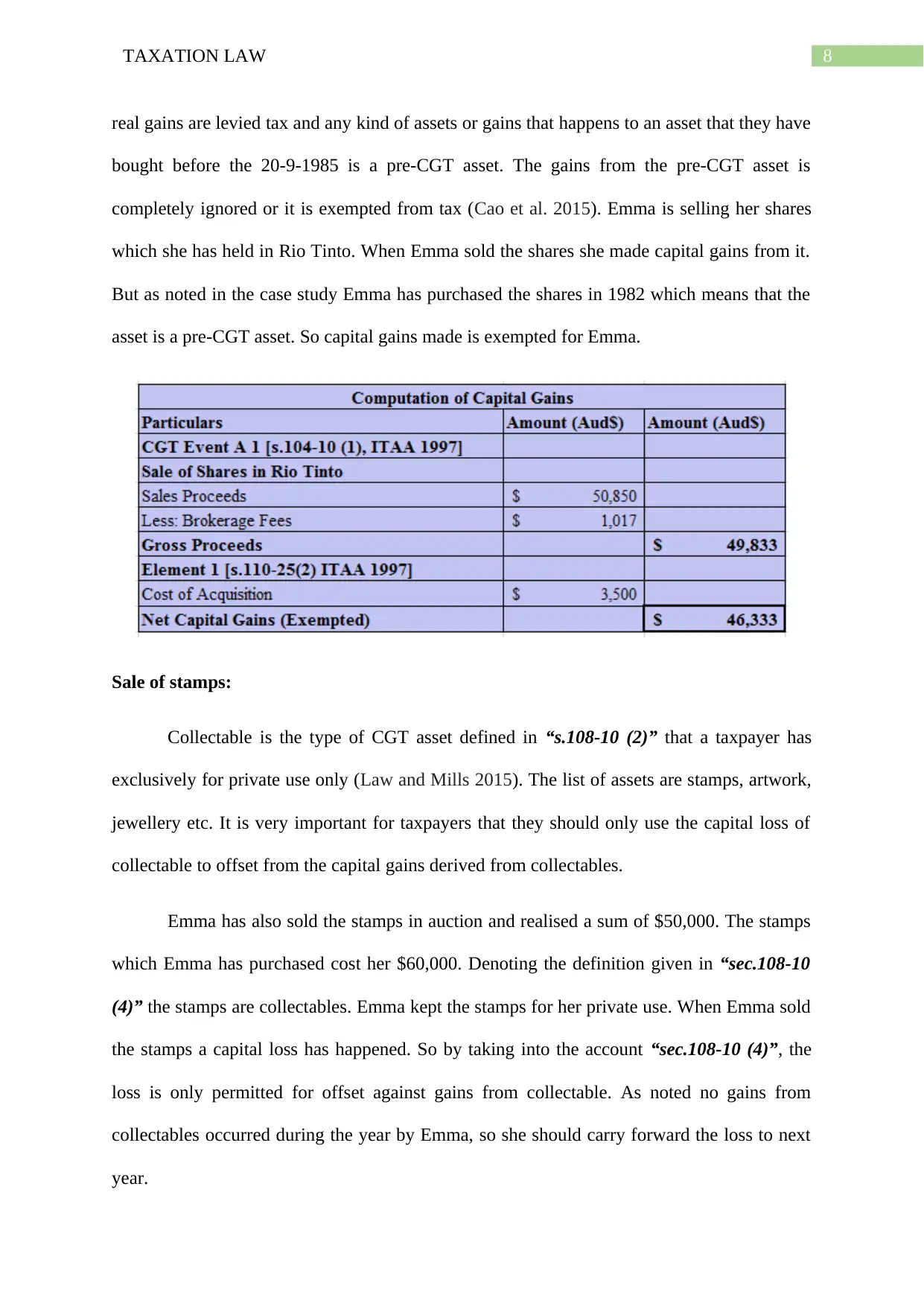

It is important for the taxpayers to understand that CGT is required to be paid for the

post-CGT asset or the events that happens after the date of 20-9-1985. This is because only

The total cost base and capital gains is given below;

Sale of shares in Rio Tinto:

It is important for the taxpayers to understand that CGT is required to be paid for the

post-CGT asset or the events that happens after the date of 20-9-1985. This is because only

8TAXATION LAW

real gains are levied tax and any kind of assets or gains that happens to an asset that they have

bought before the 20-9-1985 is a pre-CGT asset. The gains from the pre-CGT asset is

completely ignored or it is exempted from tax (Cao et al. 2015). Emma is selling her shares

which she has held in Rio Tinto. When Emma sold the shares she made capital gains from it.

But as noted in the case study Emma has purchased the shares in 1982 which means that the

asset is a pre-CGT asset. So capital gains made is exempted for Emma.

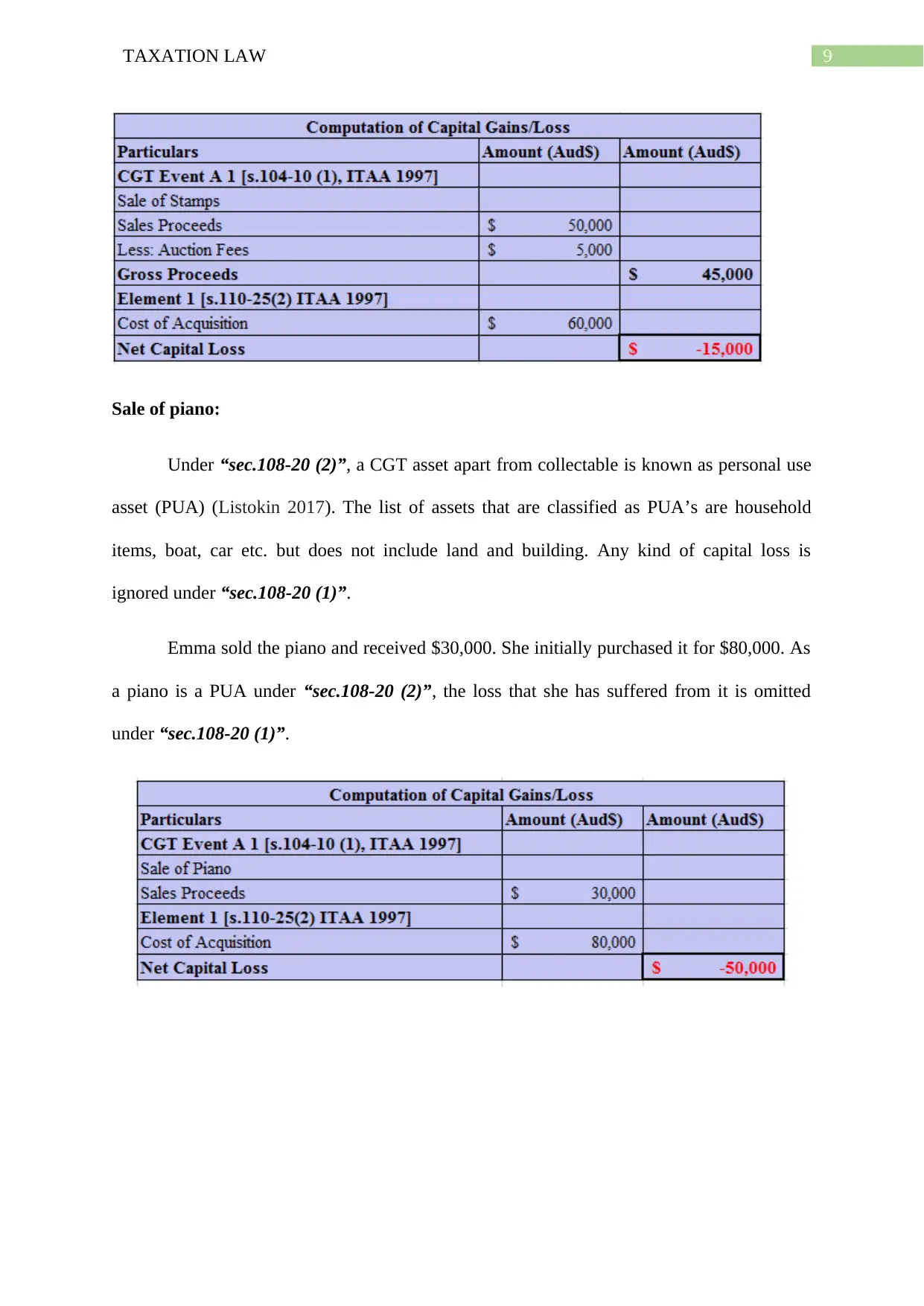

Sale of stamps:

Collectable is the type of CGT asset defined in “s.108-10 (2)” that a taxpayer has

exclusively for private use only (Law and Mills 2015). The list of assets are stamps, artwork,

jewellery etc. It is very important for taxpayers that they should only use the capital loss of

collectable to offset from the capital gains derived from collectables.

Emma has also sold the stamps in auction and realised a sum of $50,000. The stamps

which Emma has purchased cost her $60,000. Denoting the definition given in “sec.108-10

(4)” the stamps are collectables. Emma kept the stamps for her private use. When Emma sold

the stamps a capital loss has happened. So by taking into the account “sec.108-10 (4)”, the

loss is only permitted for offset against gains from collectable. As noted no gains from

collectables occurred during the year by Emma, so she should carry forward the loss to next

year.

real gains are levied tax and any kind of assets or gains that happens to an asset that they have

bought before the 20-9-1985 is a pre-CGT asset. The gains from the pre-CGT asset is

completely ignored or it is exempted from tax (Cao et al. 2015). Emma is selling her shares

which she has held in Rio Tinto. When Emma sold the shares she made capital gains from it.

But as noted in the case study Emma has purchased the shares in 1982 which means that the

asset is a pre-CGT asset. So capital gains made is exempted for Emma.

Sale of stamps:

Collectable is the type of CGT asset defined in “s.108-10 (2)” that a taxpayer has

exclusively for private use only (Law and Mills 2015). The list of assets are stamps, artwork,

jewellery etc. It is very important for taxpayers that they should only use the capital loss of

collectable to offset from the capital gains derived from collectables.

Emma has also sold the stamps in auction and realised a sum of $50,000. The stamps

which Emma has purchased cost her $60,000. Denoting the definition given in “sec.108-10

(4)” the stamps are collectables. Emma kept the stamps for her private use. When Emma sold

the stamps a capital loss has happened. So by taking into the account “sec.108-10 (4)”, the

loss is only permitted for offset against gains from collectable. As noted no gains from

collectables occurred during the year by Emma, so she should carry forward the loss to next

year.

9TAXATION LAW

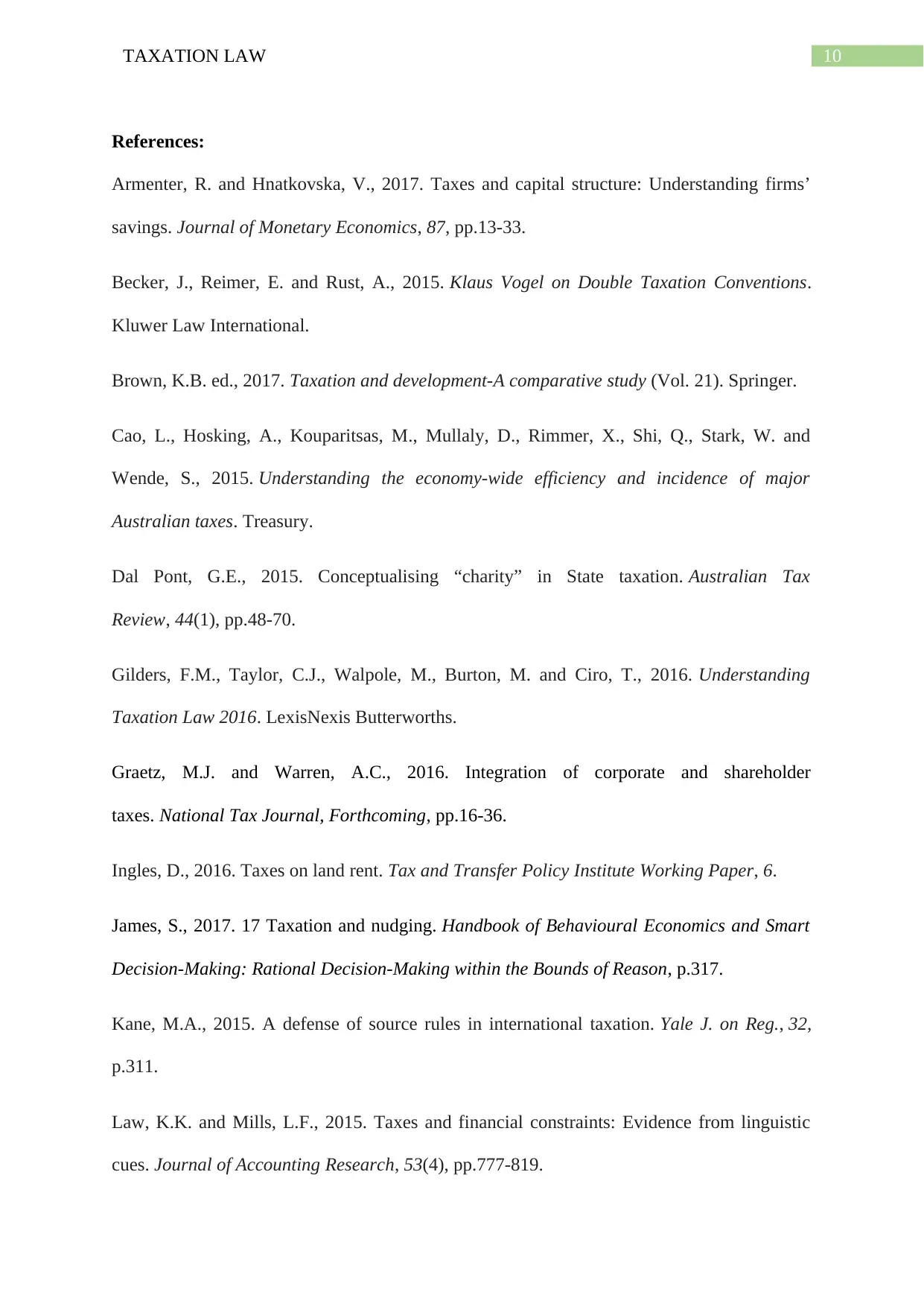

Sale of piano:

Under “sec.108-20 (2)”, a CGT asset apart from collectable is known as personal use

asset (PUA) (Listokin 2017). The list of assets that are classified as PUA’s are household

items, boat, car etc. but does not include land and building. Any kind of capital loss is

ignored under “sec.108-20 (1)”.

Emma sold the piano and received $30,000. She initially purchased it for $80,000. As

a piano is a PUA under “sec.108-20 (2)”, the loss that she has suffered from it is omitted

under “sec.108-20 (1)”.

Sale of piano:

Under “sec.108-20 (2)”, a CGT asset apart from collectable is known as personal use

asset (PUA) (Listokin 2017). The list of assets that are classified as PUA’s are household

items, boat, car etc. but does not include land and building. Any kind of capital loss is

ignored under “sec.108-20 (1)”.

Emma sold the piano and received $30,000. She initially purchased it for $80,000. As

a piano is a PUA under “sec.108-20 (2)”, the loss that she has suffered from it is omitted

under “sec.108-20 (1)”.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

References:

Armenter, R. and Hnatkovska, V., 2017. Taxes and capital structure: Understanding firms’

savings. Journal of Monetary Economics, 87, pp.13-33.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Brown, K.B. ed., 2017. Taxation and development-A comparative study (Vol. 21). Springer.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury.

Dal Pont, G.E., 2015. Conceptualising “charity” in State taxation. Australian Tax

Review, 44(1), pp.48-70.

Gilders, F.M., Taylor, C.J., Walpole, M., Burton, M. and Ciro, T., 2016. Understanding

Taxation Law 2016. LexisNexis Butterworths.

Graetz, M.J. and Warren, A.C., 2016. Integration of corporate and shareholder

taxes. National Tax Journal, Forthcoming, pp.16-36.

Ingles, D., 2016. Taxes on land rent. Tax and Transfer Policy Institute Working Paper, 6.

James, S., 2017. 17 Taxation and nudging. Handbook of Behavioural Economics and Smart

Decision-Making: Rational Decision-Making within the Bounds of Reason, p.317.

Kane, M.A., 2015. A defense of source rules in international taxation. Yale J. on Reg., 32,

p.311.

Law, K.K. and Mills, L.F., 2015. Taxes and financial constraints: Evidence from linguistic

cues. Journal of Accounting Research, 53(4), pp.777-819.

References:

Armenter, R. and Hnatkovska, V., 2017. Taxes and capital structure: Understanding firms’

savings. Journal of Monetary Economics, 87, pp.13-33.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Brown, K.B. ed., 2017. Taxation and development-A comparative study (Vol. 21). Springer.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury.

Dal Pont, G.E., 2015. Conceptualising “charity” in State taxation. Australian Tax

Review, 44(1), pp.48-70.

Gilders, F.M., Taylor, C.J., Walpole, M., Burton, M. and Ciro, T., 2016. Understanding

Taxation Law 2016. LexisNexis Butterworths.

Graetz, M.J. and Warren, A.C., 2016. Integration of corporate and shareholder

taxes. National Tax Journal, Forthcoming, pp.16-36.

Ingles, D., 2016. Taxes on land rent. Tax and Transfer Policy Institute Working Paper, 6.

James, S., 2017. 17 Taxation and nudging. Handbook of Behavioural Economics and Smart

Decision-Making: Rational Decision-Making within the Bounds of Reason, p.317.

Kane, M.A., 2015. A defense of source rules in international taxation. Yale J. on Reg., 32,

p.311.

Law, K.K. and Mills, L.F., 2015. Taxes and financial constraints: Evidence from linguistic

cues. Journal of Accounting Research, 53(4), pp.777-819.

11TAXATION LAW

Listokin, D., 2017. Landmarks Preservation and the Property Tax: Assessing Landmark

Buildings for Real Taxation Purposes. Routledge.

Ong, D., 2018. Trust law in Australia. Federation Press.

Snape, J. and De Souza, J., 2016. Environmental taxation law: policy, contexts and practice.

Routledge.

Listokin, D., 2017. Landmarks Preservation and the Property Tax: Assessing Landmark

Buildings for Real Taxation Purposes. Routledge.

Ong, D., 2018. Trust law in Australia. Federation Press.

Snape, J. and De Souza, J., 2016. Environmental taxation law: policy, contexts and practice.

Routledge.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.