LAW300 Taxation Law Assignment - Trimester 1, 2019: Parts A and B

VerifiedAdded on 2022/11/13

|12

|2858

|118

Homework Assignment

AI Summary

This assignment solution addresses key aspects of taxation law, analyzing the tax implications of various income sources and deductions. Part A focuses on a case study involving an individual's income from employment, business activities, and related deductions, including travel expenses and gifts, applying relevant sections of the ITAA 1997. The solution calculates the individual's total taxable income and tax liability. Part B examines a court case related to deductible expenses, specifically concerning a company's voluntary payment to a competitor and its tax implications, referencing the Sun Newspapers Ltd v FCT (1938) case. The solution explores the principles of income characterization, the deductibility of expenses, and the application of tax law to real-world scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part A:........................................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................7

Part B:.........................................................................................................................................7

Facts:......................................................................................................................................7

Judgement:.............................................................................................................................8

Reason for Judgement:...........................................................................................................8

Significance of Principles in Case:........................................................................................8

References:...............................................................................................................................10

Table of Contents

Part A:........................................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................7

Part B:.........................................................................................................................................7

Facts:......................................................................................................................................7

Judgement:.............................................................................................................................8

Reason for Judgement:...........................................................................................................8

Significance of Principles in Case:........................................................................................8

References:...............................................................................................................................10

2TAXATION LAW

Part A:

Issues:

a. Is the taxpayer here held taxable for the income derived from the employment as

income from the personal exertion within the ordinary meaning of “sec 6-5, ITAA

1997”?

b. Will the taxpayer be held liable for assessment for gains derived from the home based

business as income from the business activities?

c. Is the taxpayer entitled to deduction from his assessable income for the outgoings

under the positive limbs of “section 8-1, ITAA 1997”?

Rule:

As per “section 6, ITAA 1997” income from the personal exertion is associated to the

performance of contract or the provision of service. It is important to characterise the receipts

that is received in the hand of recipients (Woellner et al. 2016). Earnings from personal

exertion is characterised as income if it represents adequate relation with the amount that is

received and the income producing activity. In “Hayes v FCT (1956)” the amount that is

received from private efforts is characterised as the incident of occupation or the reward for

rendering services.

There are certain situations where the employees are paid for the expenses they

incurred. The reimbursement will be non-assessable income for the employee while the

employer will be liable for the fringe benefit tax under the “section 23L of the ITAA 1936”.

There is situation where receipts may hold adequate relation with income generating

act of taxpayers. In “Kelly v FCT (1985)” the award that was received by the football player

was viewed as ordinary income under “sec 6-5, ITAA 1997” because it was having

satisfactory relation with skill and occupation of taxpayer (Braithwaite and Reinhart 2019).

Part A:

Issues:

a. Is the taxpayer here held taxable for the income derived from the employment as

income from the personal exertion within the ordinary meaning of “sec 6-5, ITAA

1997”?

b. Will the taxpayer be held liable for assessment for gains derived from the home based

business as income from the business activities?

c. Is the taxpayer entitled to deduction from his assessable income for the outgoings

under the positive limbs of “section 8-1, ITAA 1997”?

Rule:

As per “section 6, ITAA 1997” income from the personal exertion is associated to the

performance of contract or the provision of service. It is important to characterise the receipts

that is received in the hand of recipients (Woellner et al. 2016). Earnings from personal

exertion is characterised as income if it represents adequate relation with the amount that is

received and the income producing activity. In “Hayes v FCT (1956)” the amount that is

received from private efforts is characterised as the incident of occupation or the reward for

rendering services.

There are certain situations where the employees are paid for the expenses they

incurred. The reimbursement will be non-assessable income for the employee while the

employer will be liable for the fringe benefit tax under the “section 23L of the ITAA 1936”.

There is situation where receipts may hold adequate relation with income generating

act of taxpayers. In “Kelly v FCT (1985)” the award that was received by the football player

was viewed as ordinary income under “sec 6-5, ITAA 1997” because it was having

satisfactory relation with skill and occupation of taxpayer (Braithwaite and Reinhart 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

While “section 21A” explains that non-cash benefit might have connection with the personal

services but if it is not convertible cash it is not treated as ordinary earnings. As held in

“Cooke & Sherden v FCT (1980)” a non-cash business benefit does not have the character of

income if it cannot be converted in cash.

A gain that has the character of simple gift should be viewed as income. In “FCT v

Scott (1966)” gift received out of personal relationship should not be viewed as having the

character of income (Barkoczy 2016). The ATO explains that a person is allowed to claim

deduction which they incur for business purpose travel. The examples include airfares,

accommodations, taxi fares etc. Voluntary payment that are received by the taxpayer that has

adequate relation with the taxpayer revenue creating acts will be held as taxable ordinary

income. In “Calvert v Wainwright (1947)” tips that are received by the taxi driver was

regarded as chargeable earnings.

The taxpayers are not entitled to any claim for deduction associated to the cost of

acquiring or selling the rental property. The example of such outgoings include the purchase

price of property, fees on bank guarantee, stamp duty etc. Rather these costs are included into

the purchase price of the property for capital gains tax purpose (Keyzer, Goff and Fisher

2017). However, upon renting the property the taxpayer is entitled to deduction for cost that

are occurred when the property is let-out for tax purpose.

A taxpayer is entitled to deduction for outgoings that are occurred at the time of

generating assessable earnings. A deduction is permitted under “section 8-1, ITAA 1997”

when the outgoings occurred is necessarily for business purpose or for generating taxable

business earnings (Burton and Karlinsky 2016). It should be noted that outgoings that

occurred before the beginning of income generating acts are not held as income because they

are not occurred while generating assessable income. In “Goodman Fielder Wattie v FCT

While “section 21A” explains that non-cash benefit might have connection with the personal

services but if it is not convertible cash it is not treated as ordinary earnings. As held in

“Cooke & Sherden v FCT (1980)” a non-cash business benefit does not have the character of

income if it cannot be converted in cash.

A gain that has the character of simple gift should be viewed as income. In “FCT v

Scott (1966)” gift received out of personal relationship should not be viewed as having the

character of income (Barkoczy 2016). The ATO explains that a person is allowed to claim

deduction which they incur for business purpose travel. The examples include airfares,

accommodations, taxi fares etc. Voluntary payment that are received by the taxpayer that has

adequate relation with the taxpayer revenue creating acts will be held as taxable ordinary

income. In “Calvert v Wainwright (1947)” tips that are received by the taxi driver was

regarded as chargeable earnings.

The taxpayers are not entitled to any claim for deduction associated to the cost of

acquiring or selling the rental property. The example of such outgoings include the purchase

price of property, fees on bank guarantee, stamp duty etc. Rather these costs are included into

the purchase price of the property for capital gains tax purpose (Keyzer, Goff and Fisher

2017). However, upon renting the property the taxpayer is entitled to deduction for cost that

are occurred when the property is let-out for tax purpose.

A taxpayer is entitled to deduction for outgoings that are occurred at the time of

generating assessable earnings. A deduction is permitted under “section 8-1, ITAA 1997”

when the outgoings occurred is necessarily for business purpose or for generating taxable

business earnings (Burton and Karlinsky 2016). It should be noted that outgoings that

occurred before the beginning of income generating acts are not held as income because they

are not occurred while generating assessable income. In “Goodman Fielder Wattie v FCT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

(1991)” the taxpayer was denied deduction for initial R&D outgoings on project because the

expenses were provisional in nature and not associated to derivation of income generating

activities. Hence, it is non-deductible under “sec 8-1, ITAA 1997”. There must be an

adequate and necessary relation with the loss or outgoings (Langham and Paulsen 2017). The

court in “Amalgamated Zinc v FCT (1935)” held that gaining or producing the chargeable

earnings should be interpreted as in the course of deriving income.

Gains that originates from conducting the business activities is viewed as ordinary

earnings under “sec 6-5, ITAA 1997”. Characterising the receipts as the ordinary earnings

from business involves ascertaining whether the taxpayer is performing the business activities

and considering whether the receipts are treated as normal business of that business activity

(Freudenberg et al. 2017).

As stated by the Australian taxation office deduction is allowed to taxpayers for gifts

or donations that are made to the deductible gift recipients. A taxpayer is permitted to

deduction for gifts or donations that are made to the approved organizations.

Application:

The taxpayer here Arun Sharma is originally graduated from Australia and works with

Bell Computers Pty Ltd as the financial controller. He reported the receipt of salary that

amounted to $85,000. The salary that is received from employment by Arun should be

considered as income from personal exertion because it holds adequate relation with the

income generating activity of taxpayer. Citing “Hayes v FCT (1956)” the employment

income of Arun is assessable under ordinary meaning of “section 6-5, ITA Act 1997” (Main

2019).

The taxpayer here also reported the receipt of $2,910 for using his car for work-

related purpose. The amount should be considered as employer provided benefit which will

(1991)” the taxpayer was denied deduction for initial R&D outgoings on project because the

expenses were provisional in nature and not associated to derivation of income generating

activities. Hence, it is non-deductible under “sec 8-1, ITAA 1997”. There must be an

adequate and necessary relation with the loss or outgoings (Langham and Paulsen 2017). The

court in “Amalgamated Zinc v FCT (1935)” held that gaining or producing the chargeable

earnings should be interpreted as in the course of deriving income.

Gains that originates from conducting the business activities is viewed as ordinary

earnings under “sec 6-5, ITAA 1997”. Characterising the receipts as the ordinary earnings

from business involves ascertaining whether the taxpayer is performing the business activities

and considering whether the receipts are treated as normal business of that business activity

(Freudenberg et al. 2017).

As stated by the Australian taxation office deduction is allowed to taxpayers for gifts

or donations that are made to the deductible gift recipients. A taxpayer is permitted to

deduction for gifts or donations that are made to the approved organizations.

Application:

The taxpayer here Arun Sharma is originally graduated from Australia and works with

Bell Computers Pty Ltd as the financial controller. He reported the receipt of salary that

amounted to $85,000. The salary that is received from employment by Arun should be

considered as income from personal exertion because it holds adequate relation with the

income generating activity of taxpayer. Citing “Hayes v FCT (1956)” the employment

income of Arun is assessable under ordinary meaning of “section 6-5, ITA Act 1997” (Main

2019).

The taxpayer here also reported the receipt of $2,910 for using his car for work-

related purpose. The amount should be considered as employer provided benefit which will

5TAXATION LAW

be considered as non-assessable income for the Arun under the “section 23L of the ITAA

1936” (Murray et al. 2018). The employer of Arun however will be considered liable for the

expense payment fringe benefit relating to the value of car expnses reimbursed.

Arun was later gifted Sony TV for best employee of the year. With references to the

section 21A non-cash benefits are not treated as income because it is non-convertible to cash.

Referring to judgement of court in “Cooke & Sherden v FCT (1980)” a non-cash benefit of

Sony TV does not have the character of income since it cannot be converted in cash (Pert,

Chen and Carvosso 2018).

Arun also reported the receipt of $2,000 in cash as the token of honorarium. Citing

“Calvert v Wainwright (1947)” voluntary payment that are received by Arun has adequate

relation with the taxpayer revenue creating acts and will be held as taxable ordinary income

under “sec 6-5, ITAA 1997” (Morgan, Mortimer and Pinto 2018).

As the chairman of business council Arun is required to travel in the offices of

Australian capital cities. He occurred an expense of $12,750 on airfares, accommodations and

taxis. With reference to the guidelines of ATO it can be stated that expenses incurred by Arun

is tax deductible because it is incurred for business travel purpose.

Arun also reported that he received a gift $2,000 in cash on the event of marriage

anniversary. The amount of $2,000 should be viewed as mere gift that does not has the

character of income. Citing “FCT v Scott (1966)” gift received by Arun is out of personal

relationship and should not be viewed as having the character of income (Morgan and

Castelyn 2018). Therefore, it is non-taxable.

In the later stages it is noticed that Mr and Mrs Sharman bought a property together in

Sydney. They further incurred a cost on stamp duty, loan application fees, solicitor fees while

purchasing the property. The taxpayer here is not allowed to claim the deduction related to

be considered as non-assessable income for the Arun under the “section 23L of the ITAA

1936” (Murray et al. 2018). The employer of Arun however will be considered liable for the

expense payment fringe benefit relating to the value of car expnses reimbursed.

Arun was later gifted Sony TV for best employee of the year. With references to the

section 21A non-cash benefits are not treated as income because it is non-convertible to cash.

Referring to judgement of court in “Cooke & Sherden v FCT (1980)” a non-cash benefit of

Sony TV does not have the character of income since it cannot be converted in cash (Pert,

Chen and Carvosso 2018).

Arun also reported the receipt of $2,000 in cash as the token of honorarium. Citing

“Calvert v Wainwright (1947)” voluntary payment that are received by Arun has adequate

relation with the taxpayer revenue creating acts and will be held as taxable ordinary income

under “sec 6-5, ITAA 1997” (Morgan, Mortimer and Pinto 2018).

As the chairman of business council Arun is required to travel in the offices of

Australian capital cities. He occurred an expense of $12,750 on airfares, accommodations and

taxis. With reference to the guidelines of ATO it can be stated that expenses incurred by Arun

is tax deductible because it is incurred for business travel purpose.

Arun also reported that he received a gift $2,000 in cash on the event of marriage

anniversary. The amount of $2,000 should be viewed as mere gift that does not has the

character of income. Citing “FCT v Scott (1966)” gift received by Arun is out of personal

relationship and should not be viewed as having the character of income (Morgan and

Castelyn 2018). Therefore, it is non-taxable.

In the later stages it is noticed that Mr and Mrs Sharman bought a property together in

Sydney. They further incurred a cost on stamp duty, loan application fees, solicitor fees while

purchasing the property. The taxpayer here is not allowed to claim the deduction related to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

the acquisition cost because it is capital expenditure and forms the part of cost base of the

property. While the taxpayer here Arun has also rented the property at a rate of $750 per

week. The other expenses that is incurred while the property was rented out includes property

agent fees, council rates, interest on borrowings, travel expenses etc. With respect to the

“section 8-1, ITAA 1997” Arun will be permitted to claim deduction for the aforementioned

cost because the expenses were incurred when the property was let-out for producing rental

income (Robin and Barkoczy 2019).

In the later instances, Arun also opened a home based business. He occurred expenses

on book-keeping services to local business operators to obtaining advice relating to formation

of business. Citing the event of “Goodman Fielder Wattie v FCT (1991)” it can be stated

that the expenses on book-keeping services is pre-commencement to the income producing

activities (Miller and Oats 2016). The expenses incurred by Arun is not in the course of the

business activity and it is not allowed for tax deduction in general provision of “sec 8-1,

ITAA 1997”.

Arun reported cash receipts from his home based business. He reported cash receipts

from the ABC Petrol Station Pty Ltd and Sweet Indian Restaurant. The receipts should be

categorized as the gains from business activity of Arun. It is included into the assessable

income for assessment purpose. However, the receipt of $15,000 was received by Arun on

10th July 2019. The receipt is received following the present income year and hence it is not

included for assessment purpose (Jones and Rhoades-Catanach 2015). This is because cash

basis of accounting has been followed by Arun.

Arun also donated a sum of $550 to the Brighton School. The sum of $500 is a

deductible gift for the Arun because Brighton school is the deductible gift recipient.

Calculation of Income Tax Liability

the acquisition cost because it is capital expenditure and forms the part of cost base of the

property. While the taxpayer here Arun has also rented the property at a rate of $750 per

week. The other expenses that is incurred while the property was rented out includes property

agent fees, council rates, interest on borrowings, travel expenses etc. With respect to the

“section 8-1, ITAA 1997” Arun will be permitted to claim deduction for the aforementioned

cost because the expenses were incurred when the property was let-out for producing rental

income (Robin and Barkoczy 2019).

In the later instances, Arun also opened a home based business. He occurred expenses

on book-keeping services to local business operators to obtaining advice relating to formation

of business. Citing the event of “Goodman Fielder Wattie v FCT (1991)” it can be stated

that the expenses on book-keeping services is pre-commencement to the income producing

activities (Miller and Oats 2016). The expenses incurred by Arun is not in the course of the

business activity and it is not allowed for tax deduction in general provision of “sec 8-1,

ITAA 1997”.

Arun reported cash receipts from his home based business. He reported cash receipts

from the ABC Petrol Station Pty Ltd and Sweet Indian Restaurant. The receipts should be

categorized as the gains from business activity of Arun. It is included into the assessable

income for assessment purpose. However, the receipt of $15,000 was received by Arun on

10th July 2019. The receipt is received following the present income year and hence it is not

included for assessment purpose (Jones and Rhoades-Catanach 2015). This is because cash

basis of accounting has been followed by Arun.

Arun also donated a sum of $550 to the Brighton School. The sum of $500 is a

deductible gift for the Arun because Brighton school is the deductible gift recipient.

Calculation of Income Tax Liability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

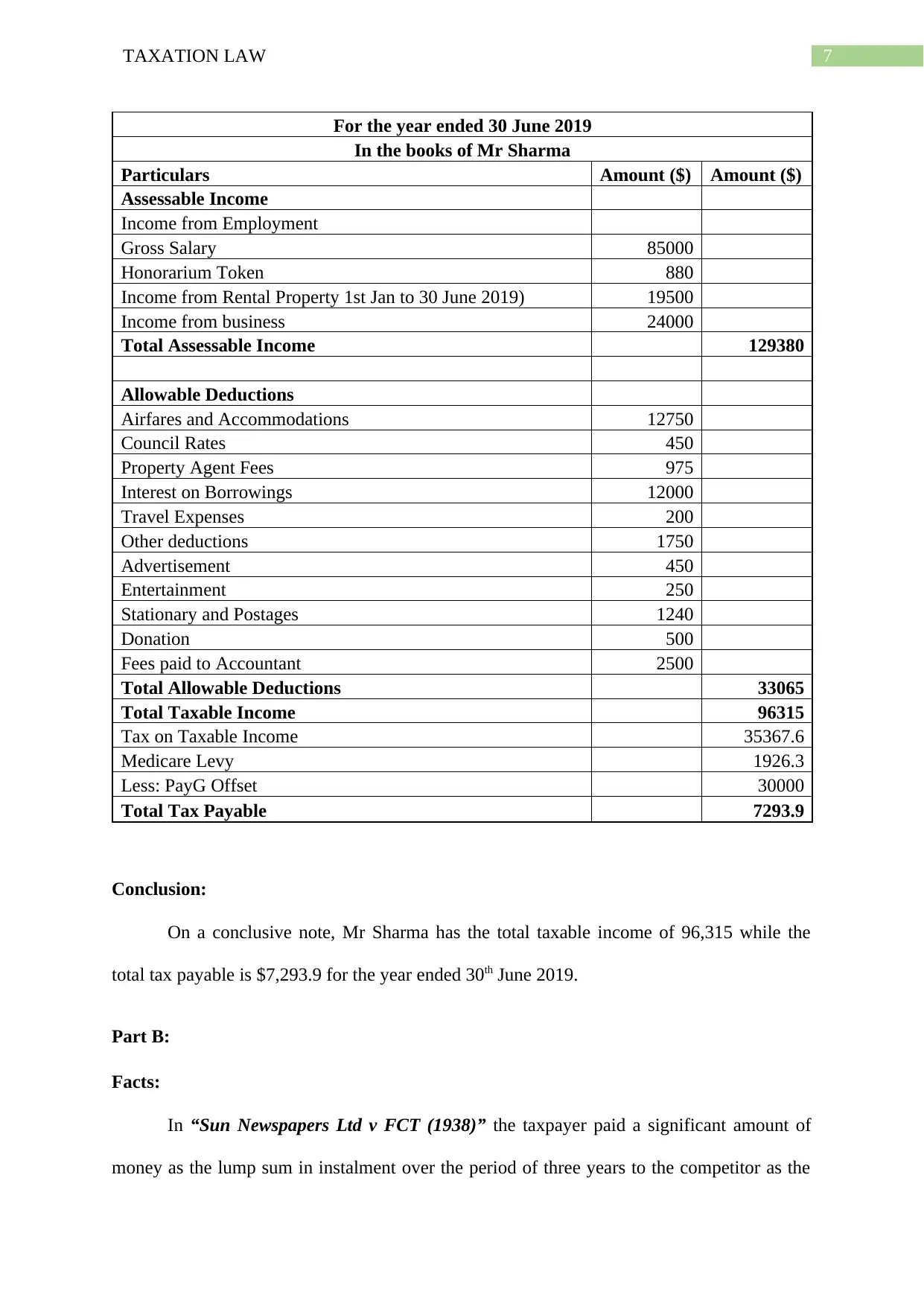

For the year ended 30 June 2019

In the books of Mr Sharma

Particulars Amount ($) Amount ($)

Assessable Income

Income from Employment

Gross Salary 85000

Honorarium Token 880

Income from Rental Property 1st Jan to 30 June 2019) 19500

Income from business 24000

Total Assessable Income 129380

Allowable Deductions

Airfares and Accommodations 12750

Council Rates 450

Property Agent Fees 975

Interest on Borrowings 12000

Travel Expenses 200

Other deductions 1750

Advertisement 450

Entertainment 250

Stationary and Postages 1240

Donation 500

Fees paid to Accountant 2500

Total Allowable Deductions 33065

Total Taxable Income 96315

Tax on Taxable Income 35367.6

Medicare Levy 1926.3

Less: PayG Offset 30000

Total Tax Payable 7293.9

Conclusion:

On a conclusive note, Mr Sharma has the total taxable income of 96,315 while the

total tax payable is $7,293.9 for the year ended 30th June 2019.

Part B:

Facts:

In “Sun Newspapers Ltd v FCT (1938)” the taxpayer paid a significant amount of

money as the lump sum in instalment over the period of three years to the competitor as the

For the year ended 30 June 2019

In the books of Mr Sharma

Particulars Amount ($) Amount ($)

Assessable Income

Income from Employment

Gross Salary 85000

Honorarium Token 880

Income from Rental Property 1st Jan to 30 June 2019) 19500

Income from business 24000

Total Assessable Income 129380

Allowable Deductions

Airfares and Accommodations 12750

Council Rates 450

Property Agent Fees 975

Interest on Borrowings 12000

Travel Expenses 200

Other deductions 1750

Advertisement 450

Entertainment 250

Stationary and Postages 1240

Donation 500

Fees paid to Accountant 2500

Total Allowable Deductions 33065

Total Taxable Income 96315

Tax on Taxable Income 35367.6

Medicare Levy 1926.3

Less: PayG Offset 30000

Total Tax Payable 7293.9

Conclusion:

On a conclusive note, Mr Sharma has the total taxable income of 96,315 while the

total tax payable is $7,293.9 for the year ended 30th June 2019.

Part B:

Facts:

In “Sun Newspapers Ltd v FCT (1938)” the taxpayer paid a significant amount of

money as the lump sum in instalment over the period of three years to the competitor as the

8TAXATION LAW

consideration for the competitor for not being related with the production of daily paper

inside the 300 miles of Sydney. The taxpayer in this case was the director as well as

shareholder of the company and the company while carrying the business occurred a business

related liability which was not paid. The company stopped its trading and was subsequently

liquidated.

Judgement:

The taxpayer here satisfied that the liability that was occurred by the company was

voluntarily by paying the sum of liability which was occurred by the creditor of company.

The taxpayer did not provide any kind of personal guarantee in this aspect of the liability that

was occurred by the company (Bankman et al. 2018). There was no such kind of ancillary

agreement among the company and the taxpayer for the organization to reimburse the

taxpayer for the sum paid. The sum was not paid to the company by taxpayer in the form of

loan.

Reason for Judgement:

Consequently, the decision of the court in “Sun Newspapers Ltd v FCT (1938)” held

that the voluntary payment did not occurred in respect of their revenue outgoings as there was

no such ancillary agreement and the taxpayer paid the expenditure voluntarily (Morgan and

Castelyn 2018). The high court held that the lump sum amount was not allowed as deduction

because it was capital in nature. The reason for the judgement was that the character of the

advantage that is sought and in this its lasting qualities may play an active part. The way in

which it is to be used was reliant on or enjoyed and under the former head recurrence might

play its share as well.

consideration for the competitor for not being related with the production of daily paper

inside the 300 miles of Sydney. The taxpayer in this case was the director as well as

shareholder of the company and the company while carrying the business occurred a business

related liability which was not paid. The company stopped its trading and was subsequently

liquidated.

Judgement:

The taxpayer here satisfied that the liability that was occurred by the company was

voluntarily by paying the sum of liability which was occurred by the creditor of company.

The taxpayer did not provide any kind of personal guarantee in this aspect of the liability that

was occurred by the company (Bankman et al. 2018). There was no such kind of ancillary

agreement among the company and the taxpayer for the organization to reimburse the

taxpayer for the sum paid. The sum was not paid to the company by taxpayer in the form of

loan.

Reason for Judgement:

Consequently, the decision of the court in “Sun Newspapers Ltd v FCT (1938)” held

that the voluntary payment did not occurred in respect of their revenue outgoings as there was

no such ancillary agreement and the taxpayer paid the expenditure voluntarily (Morgan and

Castelyn 2018). The high court held that the lump sum amount was not allowed as deduction

because it was capital in nature. The reason for the judgement was that the character of the

advantage that is sought and in this its lasting qualities may play an active part. The way in

which it is to be used was reliant on or enjoyed and under the former head recurrence might

play its share as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Significance of Principles in Case:

The principles established in this case stated that the legal expenses is only deductible

if it is revenue in nature and therefore it will be considered deductible if they originate out of

the daily business activities or income generating activities. Where an outgoing is directed

towards the structural instead of operational purpose, the outgoings are held as capital in

nature and non-deductible.

Significance of Principles in Case:

The principles established in this case stated that the legal expenses is only deductible

if it is revenue in nature and therefore it will be considered deductible if they originate out of

the daily business activities or income generating activities. Where an outgoing is directed

towards the structural instead of operational purpose, the outgoings are held as capital in

nature and non-deductible.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School

of Social Sciences, The Australian National University.

Burton, H.A. and Karlinsky, S., 2016. Tax professionals' perception of large and mid-size

business US tax law complexity. eJTR, 14, p.61.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, p.21.

Jones, S. and Rhoades-Catanach, S., 2015. Principles of Taxation for Business and

Investment Planning 2016 Edition. McGraw-Hill Education.

Keyzer, P., Goff, C. and Fisher, A., 2017. Principles of Australian constitutional law.

LexisNexis Butterworths.

Langham, J.A. and Paulsen, N., 2017. Invisible Taxation: Fantasy or Just Good Service

Design. Austl. Tax F., 32, p.129.

Main, J., 2019. Taxation: Buying or selling: beware the sting of GST. LSJ: Law Society of

NSW Journal, (55), p.73.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Morgan, A. and Castelyn, D., 2018. Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School

of Social Sciences, The Australian National University.

Burton, H.A. and Karlinsky, S., 2016. Tax professionals' perception of large and mid-size

business US tax law complexity. eJTR, 14, p.61.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, p.21.

Jones, S. and Rhoades-Catanach, S., 2015. Principles of Taxation for Business and

Investment Planning 2016 Edition. McGraw-Hill Education.

Keyzer, P., Goff, C. and Fisher, A., 2017. Principles of Australian constitutional law.

LexisNexis Butterworths.

Langham, J.A. and Paulsen, N., 2017. Invisible Taxation: Fantasy or Just Good Service

Design. Austl. Tax F., 32, p.129.

Main, J., 2019. Taxation: Buying or selling: beware the sting of GST. LSJ: Law Society of

NSW Journal, (55), p.73.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Morgan, A. and Castelyn, D., 2018. Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

11TAXATION LAW

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

Murray, I., Taylor, J., Walpole, M., Burton, M. and Ciro, T., 2018. Understanding Taxation

Law 2019.

Pert, A., Chen, H. and Carvosso, R., 2018. 'Bywater Investments Limited v Commissioner of

Taxation';'Hua Wang Bank Berhad v Commissioner of Taxation'(2016) 91 ALJR

59. Australian Year Book of International Law, 35, p.250.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.), 2019. Australian Taxation

Law Select 2019: Legislation And Commentary. Oxford University Press.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

Murray, I., Taylor, J., Walpole, M., Burton, M. and Ciro, T., 2018. Understanding Taxation

Law 2019.

Pert, A., Chen, H. and Carvosso, R., 2018. 'Bywater Investments Limited v Commissioner of

Taxation';'Hua Wang Bank Berhad v Commissioner of Taxation'(2016) 91 ALJR

59. Australian Year Book of International Law, 35, p.250.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.), 2019. Australian Taxation

Law Select 2019: Legislation And Commentary. Oxford University Press.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.