Individual Assignment: Taxation Law, HA3042, T1 2019, Holmes Institute

VerifiedAdded on 2022/10/01

|13

|2883

|356

Homework Assignment

AI Summary

This assignment solution addresses two key questions in taxation law. The first question examines capital gains tax (CGT) implications for various scenarios, including the family home, a car, business sale, furniture, and paintings. It analyzes whether CGT applies, considering factors like pre-CGT assets, private use assets, small business concessions, and collectibles. The second question explores tax deductions related to depreciating assets, focusing on a CNC machine. It discusses relevant provisions of the ITAA 1997, including the 'decline in value' concept, the start time of depreciation, and the cost base of the asset, incorporating incidental costs like installation and guiding rods. The solution provides detailed analysis, computations, and references to relevant legislation and rulings.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

A: The capital gain in relation to the family home:...............................................................2

B: Capital gain or loss made from the car:.............................................................................2

C: The capital gain in relation to the sale of business:...........................................................3

D: The capital gain in relation to selling the furniture:..........................................................4

E: The capital gain in relation to selling the paintings:..........................................................5

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Law:........................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................9

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

A: The capital gain in relation to the family home:...............................................................2

B: Capital gain or loss made from the car:.............................................................................2

C: The capital gain in relation to the sale of business:...........................................................3

D: The capital gain in relation to selling the furniture:..........................................................4

E: The capital gain in relation to selling the paintings:..........................................................5

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Law:........................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................9

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

A: The capital gain in relation to the family home:

Capital gains tax is usually applied on those assets that is bought or further happening

on or following the 20th September 1985 (Barkoczy 2016). Consequently, the expression Pre-

CGT and post-CGT is commonly employed to denote those assets that are bought or events

happening preceding to or following that date.

For a taxpayer, basic exemption is allowed for capital gains or loss that originates

from the CGT event where the CGT asset is regarded as the house and under “section 118-

110 (1), ITAA 1997” the home formed the main dwelling of the taxpayer all through the

whole ownership period.

As evident in the case of Jasmine she bought a house in 1981 for $40,000 and

eventually sold in the current tax year for $650,000. Jasmine home can be classified as the

Pre-CGT asset since it was purchased prior to the application of the CGT regime.

Furthermore, she lived in that home ever since she purchased it and her dwelling qualifies for

main house under “section 118-110 (1)”. Therefore, the capital gains made from selling her

house will be excluded from CGT.

B: Capital gain or loss made from the car:

Under “section 104-10 (1)” a CGT event A1 happens when the CGT asset is sold by

the taxpayer (Evans, Minas and Lim 2015). Under the “section 108-20 (2))” private use asset

can be referred as those assets apart from collectables which is mainly used by the taxpayer

for their own usage and enjoyment purpose except land and buildings. The instances of

private use asset usually includes;

a. TV at home

b. Mobile phone for private usage

Answer to question 1:

A: The capital gain in relation to the family home:

Capital gains tax is usually applied on those assets that is bought or further happening

on or following the 20th September 1985 (Barkoczy 2016). Consequently, the expression Pre-

CGT and post-CGT is commonly employed to denote those assets that are bought or events

happening preceding to or following that date.

For a taxpayer, basic exemption is allowed for capital gains or loss that originates

from the CGT event where the CGT asset is regarded as the house and under “section 118-

110 (1), ITAA 1997” the home formed the main dwelling of the taxpayer all through the

whole ownership period.

As evident in the case of Jasmine she bought a house in 1981 for $40,000 and

eventually sold in the current tax year for $650,000. Jasmine home can be classified as the

Pre-CGT asset since it was purchased prior to the application of the CGT regime.

Furthermore, she lived in that home ever since she purchased it and her dwelling qualifies for

main house under “section 118-110 (1)”. Therefore, the capital gains made from selling her

house will be excluded from CGT.

B: Capital gain or loss made from the car:

Under “section 104-10 (1)” a CGT event A1 happens when the CGT asset is sold by

the taxpayer (Evans, Minas and Lim 2015). Under the “section 108-20 (2))” private use asset

can be referred as those assets apart from collectables which is mainly used by the taxpayer

for their own usage and enjoyment purpose except land and buildings. The instances of

private use asset usually includes;

a. TV at home

b. Mobile phone for private usage

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

c. A car or bicycle

d. A yacht for personal usage.

There are special rules that are applicable on private use assets. Under “section 118-

10 (3)”, the taxpayer should disregard the capital gains from the private use asset when it is

purchased for $10,000 or less. While under “section 108-20 (1)” capital loss from the sale of

private use asset is generally omitted.

As evident Jasmine bought a car in 2011 for $31,000 which was eventually sold for

$10,000. As a result, Jasmine incurs a capital loss from the disposal of car. However, as the

car is treated as personal use asset hence under “section 108-20 (1)” capital loss from the

disposal of private car should be disregarded by Jasmine.

C: The capital gain in relation to the sale of business:

Under “division 152” concessions are available to help the small businesses (Chardon,

Freudenberg and Brimble 2016). The basic conditions includes the following;

a. The entity should be a small business entity with aggregate turnover in the present

year or previous year is less than $2 million or the net worth of the assets is not more

than $6 million.

b. CGT asset is ought to be an active asset.

There are mainly four types of small business concessions. These are

1. 15-year exemption: The CGT assets are held for a minimum of 15 years by the

taxpayer.

2. 50% reduction: Taxpayer that qualifies under this scheme can reduce the capital gain

by 50%.

c. A car or bicycle

d. A yacht for personal usage.

There are special rules that are applicable on private use assets. Under “section 118-

10 (3)”, the taxpayer should disregard the capital gains from the private use asset when it is

purchased for $10,000 or less. While under “section 108-20 (1)” capital loss from the sale of

private use asset is generally omitted.

As evident Jasmine bought a car in 2011 for $31,000 which was eventually sold for

$10,000. As a result, Jasmine incurs a capital loss from the disposal of car. However, as the

car is treated as personal use asset hence under “section 108-20 (1)” capital loss from the

disposal of private car should be disregarded by Jasmine.

C: The capital gain in relation to the sale of business:

Under “division 152” concessions are available to help the small businesses (Chardon,

Freudenberg and Brimble 2016). The basic conditions includes the following;

a. The entity should be a small business entity with aggregate turnover in the present

year or previous year is less than $2 million or the net worth of the assets is not more

than $6 million.

b. CGT asset is ought to be an active asset.

There are mainly four types of small business concessions. These are

1. 15-year exemption: The CGT assets are held for a minimum of 15 years by the

taxpayer.

2. 50% reduction: Taxpayer that qualifies under this scheme can reduce the capital gain

by 50%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

3. Retirement concession: Ignore capital gain on the disposal of CGT asset associated

with the small business given the sales revenue are used for the purpose of retirement

(Davidson and Evans 2015).

4. Roll-over relief: The capital gains are deferred when the taxpayer purchases the

replacement asset.

As obvious from the circumstances of Jasmine she is retiring from her business of

cleaner and she is returning back to UK. She found a buyer for her business that would be

taking up the cleaning business for $125,000. The business assets were sold for $65,000 and

her goodwill is sold for $60,000. Under “division 152” concessions are available to Jasmine

since the net worth of the assets is not more than $6 million and the assets that are sold by

Jasmine has been used for carrying the business. Jasmine for her business equipment can

obtain a 15-year exemption for the CGT assets that is held for at least of 15 years.

In relation to her goodwill, a CGT event C1 took place since her business ceased

permanently. Rendering to “Taxation ruling of TR 1999/16” when a business is ceased

permanently from operations whether out of voluntary or involuntary act there is a loss or

destruction of the business goodwill (Sadiq 2019). Likewise, in case of Jasmine, while selling

her business goodwill, the operation of business was ceased on permanent basis. Hence,

Jasmine can obtain a 50% reduction under the “subdivision 152-C”.

D: The capital gain from selling the furniture:

Later instances from the case suggest that Jasmine also sold her furniture for $5,000

while the purchase price for the furniture stood $2,000. According to the “section 118-10

(3)” capital gains must be overlooked where the private use asset was purchased for lower

than $10,000 or less (Butler 2019). Similarly, in case of Jasmine the purchase price of

3. Retirement concession: Ignore capital gain on the disposal of CGT asset associated

with the small business given the sales revenue are used for the purpose of retirement

(Davidson and Evans 2015).

4. Roll-over relief: The capital gains are deferred when the taxpayer purchases the

replacement asset.

As obvious from the circumstances of Jasmine she is retiring from her business of

cleaner and she is returning back to UK. She found a buyer for her business that would be

taking up the cleaning business for $125,000. The business assets were sold for $65,000 and

her goodwill is sold for $60,000. Under “division 152” concessions are available to Jasmine

since the net worth of the assets is not more than $6 million and the assets that are sold by

Jasmine has been used for carrying the business. Jasmine for her business equipment can

obtain a 15-year exemption for the CGT assets that is held for at least of 15 years.

In relation to her goodwill, a CGT event C1 took place since her business ceased

permanently. Rendering to “Taxation ruling of TR 1999/16” when a business is ceased

permanently from operations whether out of voluntary or involuntary act there is a loss or

destruction of the business goodwill (Sadiq 2019). Likewise, in case of Jasmine, while selling

her business goodwill, the operation of business was ceased on permanent basis. Hence,

Jasmine can obtain a 50% reduction under the “subdivision 152-C”.

D: The capital gain from selling the furniture:

Later instances from the case suggest that Jasmine also sold her furniture for $5,000

while the purchase price for the furniture stood $2,000. According to the “section 118-10

(3)” capital gains must be overlooked where the private use asset was purchased for lower

than $10,000 or less (Butler 2019). Similarly, in case of Jasmine the purchase price of

5TAXATION LAW

furniture stood less than $2,000 and the capital gains that is made from the sale of furniture

by Jasmine will be disregarded under “section 118-10 (3)”.

E: The capital gain from selling the paintings:

According to “section 108-10, ITAA 1997” collectibles is defined as asset that is used

by taxpayer for their person pleasure purpose (Murray et al., 2018). “Section 108-10 (2)”

provides the list of collectibles which includes the following;

a. Antiques and jewellery

b. Art works such as (paintings and sculptures)

c. Rare stamps, coins

There are exceptional rules that are applicable for the collectibles. Accordingly under

“section 108-10 (1), ITAA 1997” the capital loss from the collectibles are set apart and is

only allowed for offset against the capital gains or other collectables (Morgan, Mortimer and

Pinto 2018). Under “section 118-10 (1)” the capital gains are disregarded if the collectible

was purchased for lower than $500.

In case of Jasmine she bought several paintings with each costing not more than $500.

All the paintings were sold by Jasmine for $35,000. With reference to the special rules given

under “section 108-10 (1)”, the capital gains derived from disposal of all her paintings will

be disregarded since the cost base of each painting is not more than $500. However, one of

her paintings costs $1,000 which was eventually sold for $5,000. Therefore, Jasmine has

made a capital gain of $4,000 from the paintings and it will be accountable for capital gains

tax.

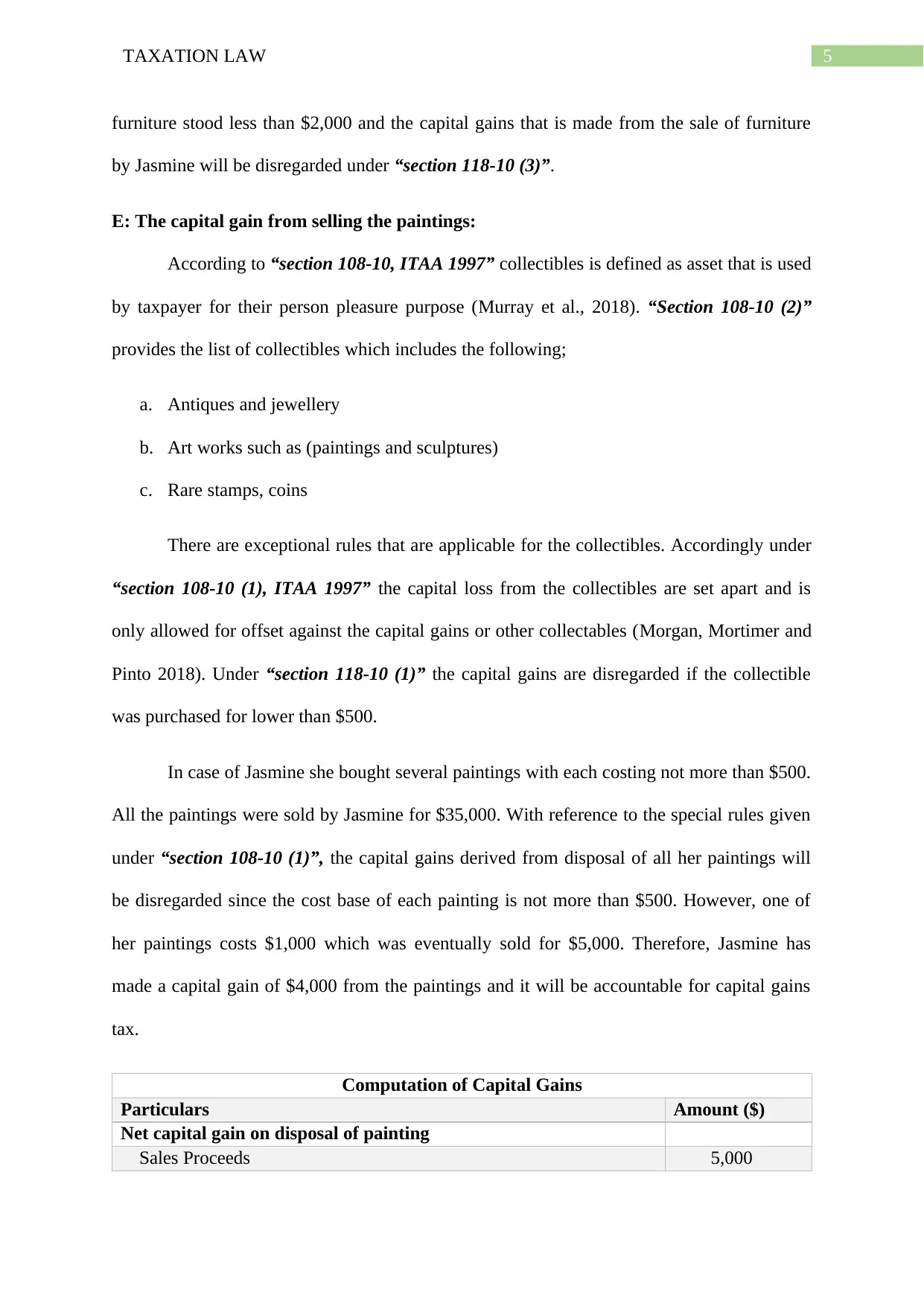

Computation of Capital Gains

Particulars Amount ($)

Net capital gain on disposal of painting

Sales Proceeds 5,000

furniture stood less than $2,000 and the capital gains that is made from the sale of furniture

by Jasmine will be disregarded under “section 118-10 (3)”.

E: The capital gain from selling the paintings:

According to “section 108-10, ITAA 1997” collectibles is defined as asset that is used

by taxpayer for their person pleasure purpose (Murray et al., 2018). “Section 108-10 (2)”

provides the list of collectibles which includes the following;

a. Antiques and jewellery

b. Art works such as (paintings and sculptures)

c. Rare stamps, coins

There are exceptional rules that are applicable for the collectibles. Accordingly under

“section 108-10 (1), ITAA 1997” the capital loss from the collectibles are set apart and is

only allowed for offset against the capital gains or other collectables (Morgan, Mortimer and

Pinto 2018). Under “section 118-10 (1)” the capital gains are disregarded if the collectible

was purchased for lower than $500.

In case of Jasmine she bought several paintings with each costing not more than $500.

All the paintings were sold by Jasmine for $35,000. With reference to the special rules given

under “section 108-10 (1)”, the capital gains derived from disposal of all her paintings will

be disregarded since the cost base of each painting is not more than $500. However, one of

her paintings costs $1,000 which was eventually sold for $5,000. Therefore, Jasmine has

made a capital gain of $4,000 from the paintings and it will be accountable for capital gains

tax.

Computation of Capital Gains

Particulars Amount ($)

Net capital gain on disposal of painting

Sales Proceeds 5,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

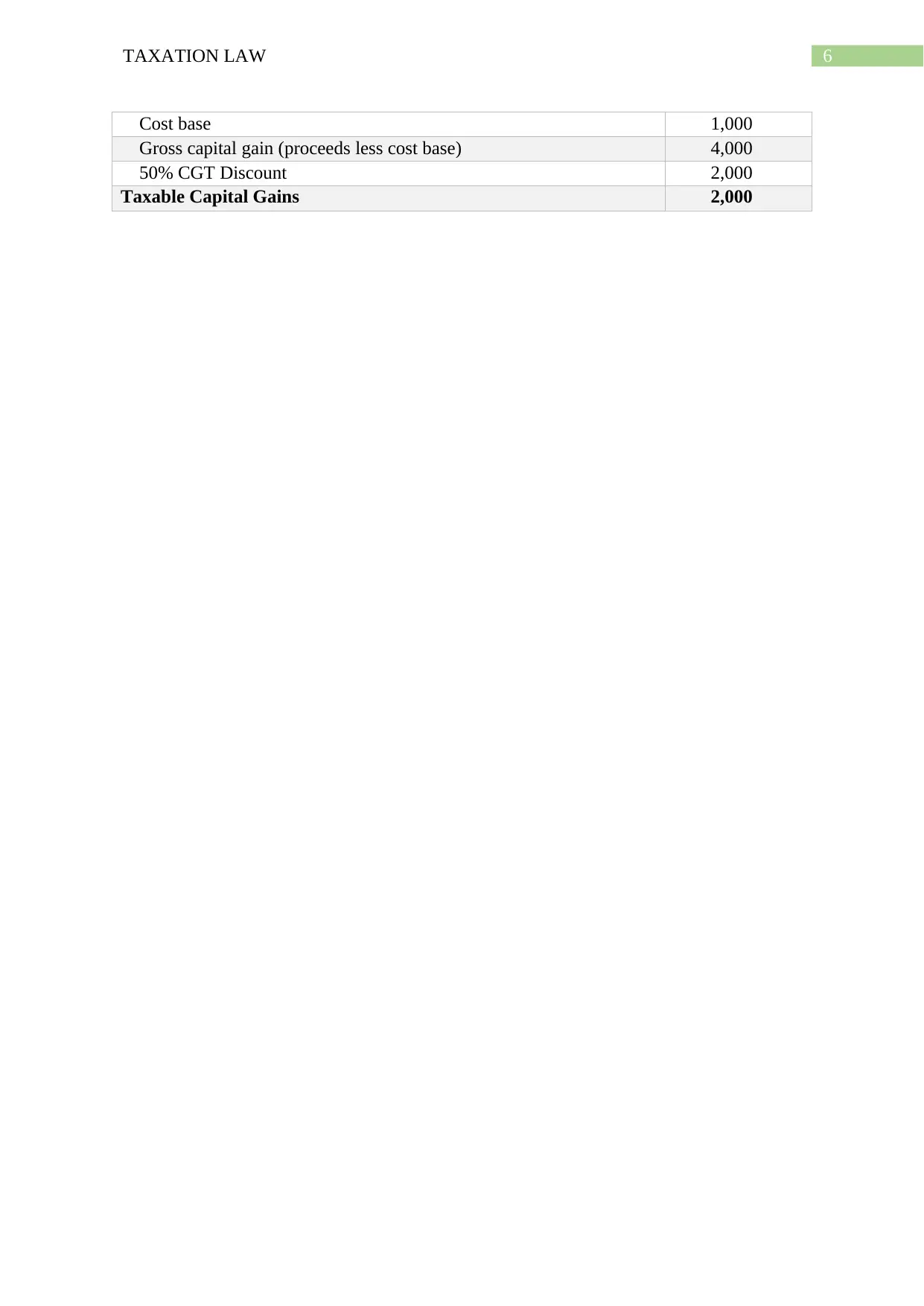

Cost base 1,000

Gross capital gain (proceeds less cost base) 4,000

50% CGT Discount 2,000

Taxable Capital Gains 2,000

Cost base 1,000

Gross capital gain (proceeds less cost base) 4,000

50% CGT Discount 2,000

Taxable Capital Gains 2,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Issues:

Will the taxpayer be permitted to claim tax deduction under the operative provision of

“section 40-25 (1), ITAA 1997” equivalent to the decline in value of the depreciating asset

that is held by the taxpayer and was installed ready for taxable purpose?

Law:

According to the “division 40 of ITAA 1997”, a taxpayer is permitted to obtain

deduction for the amount that is equal to the “decline in value” of the depreciating asset

based on the effective which is held by the taxpayer (Morgan and Castelyn 2018). According

to the chief operative provision of “section 40-25 (1)”, deductions are allowed to taxpayers

equivalent to the decline in value of the depreciating asset that is held by the taxpayer for any

time throughout the year and that was used for generating chargeable earnings or installed

ready for use.

Taxpayers holding the depreciating assets begins to fall in terms of worth when its

start time happens under “section 40-60 (1)”. The start time of the depreciating asset

represents when the taxpayer at first uses the asset or it has been installed for ready use (Liu

2018). This implies that the decline in value of the assets commences when the asset is first

used by the taxpayer even though it is used for private purpose. The taxpayer should denote

that under “section 40-25 (2), ITAA 1997” no deduction is allowed to taxpayers until the

time the asset is used for taxable purpose. If the taxpayer uses the asset completely for private

purpose then there will be 100% reduction in the deduction for that period but there would be

not deduction for the private purpose (Robin and Barkoczy 2019). Conferring to “section 40-

30 (1)” a depreciating asset are those assets that has the limited actual life and it is rationally

anticipated to the fall in the value till the phase it is used.

Answer to question 2:

Issues:

Will the taxpayer be permitted to claim tax deduction under the operative provision of

“section 40-25 (1), ITAA 1997” equivalent to the decline in value of the depreciating asset

that is held by the taxpayer and was installed ready for taxable purpose?

Law:

According to the “division 40 of ITAA 1997”, a taxpayer is permitted to obtain

deduction for the amount that is equal to the “decline in value” of the depreciating asset

based on the effective which is held by the taxpayer (Morgan and Castelyn 2018). According

to the chief operative provision of “section 40-25 (1)”, deductions are allowed to taxpayers

equivalent to the decline in value of the depreciating asset that is held by the taxpayer for any

time throughout the year and that was used for generating chargeable earnings or installed

ready for use.

Taxpayers holding the depreciating assets begins to fall in terms of worth when its

start time happens under “section 40-60 (1)”. The start time of the depreciating asset

represents when the taxpayer at first uses the asset or it has been installed for ready use (Liu

2018). This implies that the decline in value of the assets commences when the asset is first

used by the taxpayer even though it is used for private purpose. The taxpayer should denote

that under “section 40-25 (2), ITAA 1997” no deduction is allowed to taxpayers until the

time the asset is used for taxable purpose. If the taxpayer uses the asset completely for private

purpose then there will be 100% reduction in the deduction for that period but there would be

not deduction for the private purpose (Robin and Barkoczy 2019). Conferring to “section 40-

30 (1)” a depreciating asset are those assets that has the limited actual life and it is rationally

anticipated to the fall in the value till the phase it is used.

8TAXATION LAW

Under the “sub-division 40-C” depreciation is allowed on the price of asset. As a

general rule, the court of law in “Broken Hill Pty Co Ltd v. FCT” (1969-70) stated that the

cost would not include the purchase price but would also include the incidental cost relating

to delivery and installation (Braithwaite and Reinhart 2019). Additionally, minor expenditure

occurred in re-arranging or removing other plant for accommodating the new plant might be

included into the cost as well.

As per “section 110-25, ITAA 1997” the cost base of asset comprises of five elements

(Miller and Oats 2016). The first element comprises of money paid to purchase the asset and

the marketplace worth of asset. The cost base elements are as follows;

1. Amount paid or necessarily needed to be paid in relation to the purchase of asset

2. Related charges occurred in purchasing or selling the asset

3. For assets purchased following 20 August 1991, the cost of title is included.

4. Capital expenses to increase assets value or associated to installing or moving asset

5. Capital expenses occurred in preserving title rights of assets.

The second element associated to acquisition or sale only comprises of costs listed under

“section 110-35” such as cost of transfer, professional fees such as surveyor cost, stamp duty,

advertisement and cost of valuation or borrowing expenses (Thuronyi and Brooks 2016).

Application:

Evidently, the circumstances of John it is found that he imported a CNC machine

from Germany on 1st November 2014 for a cost of $300,000. With reference to “section 40-

30 (1)”, the CNC machine should be treated as a depreciating asset since it has the limited

operative lifespan and it is reasonably anticipated to the decline in the value till the time it is

used by John for taxable purpose.

Under the “sub-division 40-C” depreciation is allowed on the price of asset. As a

general rule, the court of law in “Broken Hill Pty Co Ltd v. FCT” (1969-70) stated that the

cost would not include the purchase price but would also include the incidental cost relating

to delivery and installation (Braithwaite and Reinhart 2019). Additionally, minor expenditure

occurred in re-arranging or removing other plant for accommodating the new plant might be

included into the cost as well.

As per “section 110-25, ITAA 1997” the cost base of asset comprises of five elements

(Miller and Oats 2016). The first element comprises of money paid to purchase the asset and

the marketplace worth of asset. The cost base elements are as follows;

1. Amount paid or necessarily needed to be paid in relation to the purchase of asset

2. Related charges occurred in purchasing or selling the asset

3. For assets purchased following 20 August 1991, the cost of title is included.

4. Capital expenses to increase assets value or associated to installing or moving asset

5. Capital expenses occurred in preserving title rights of assets.

The second element associated to acquisition or sale only comprises of costs listed under

“section 110-35” such as cost of transfer, professional fees such as surveyor cost, stamp duty,

advertisement and cost of valuation or borrowing expenses (Thuronyi and Brooks 2016).

Application:

Evidently, the circumstances of John it is found that he imported a CNC machine

from Germany on 1st November 2014 for a cost of $300,000. With reference to “section 40-

30 (1)”, the CNC machine should be treated as a depreciating asset since it has the limited

operative lifespan and it is reasonably anticipated to the decline in the value till the time it is

used by John for taxable purpose.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

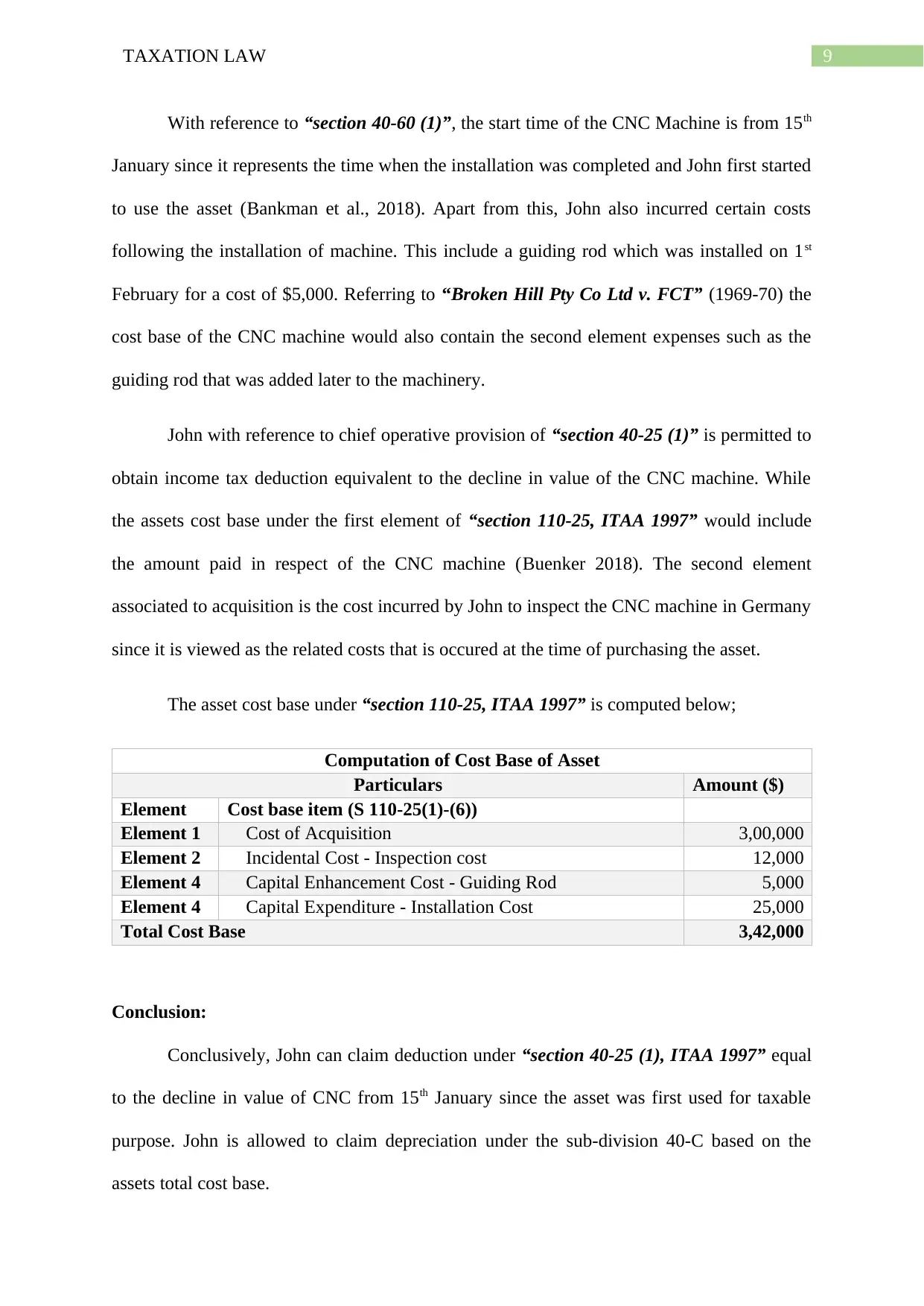

With reference to “section 40-60 (1)”, the start time of the CNC Machine is from 15th

January since it represents the time when the installation was completed and John first started

to use the asset (Bankman et al., 2018). Apart from this, John also incurred certain costs

following the installation of machine. This include a guiding rod which was installed on 1st

February for a cost of $5,000. Referring to “Broken Hill Pty Co Ltd v. FCT” (1969-70) the

cost base of the CNC machine would also contain the second element expenses such as the

guiding rod that was added later to the machinery.

John with reference to chief operative provision of “section 40-25 (1)” is permitted to

obtain income tax deduction equivalent to the decline in value of the CNC machine. While

the assets cost base under the first element of “section 110-25, ITAA 1997” would include

the amount paid in respect of the CNC machine (Buenker 2018). The second element

associated to acquisition is the cost incurred by John to inspect the CNC machine in Germany

since it is viewed as the related costs that is occured at the time of purchasing the asset.

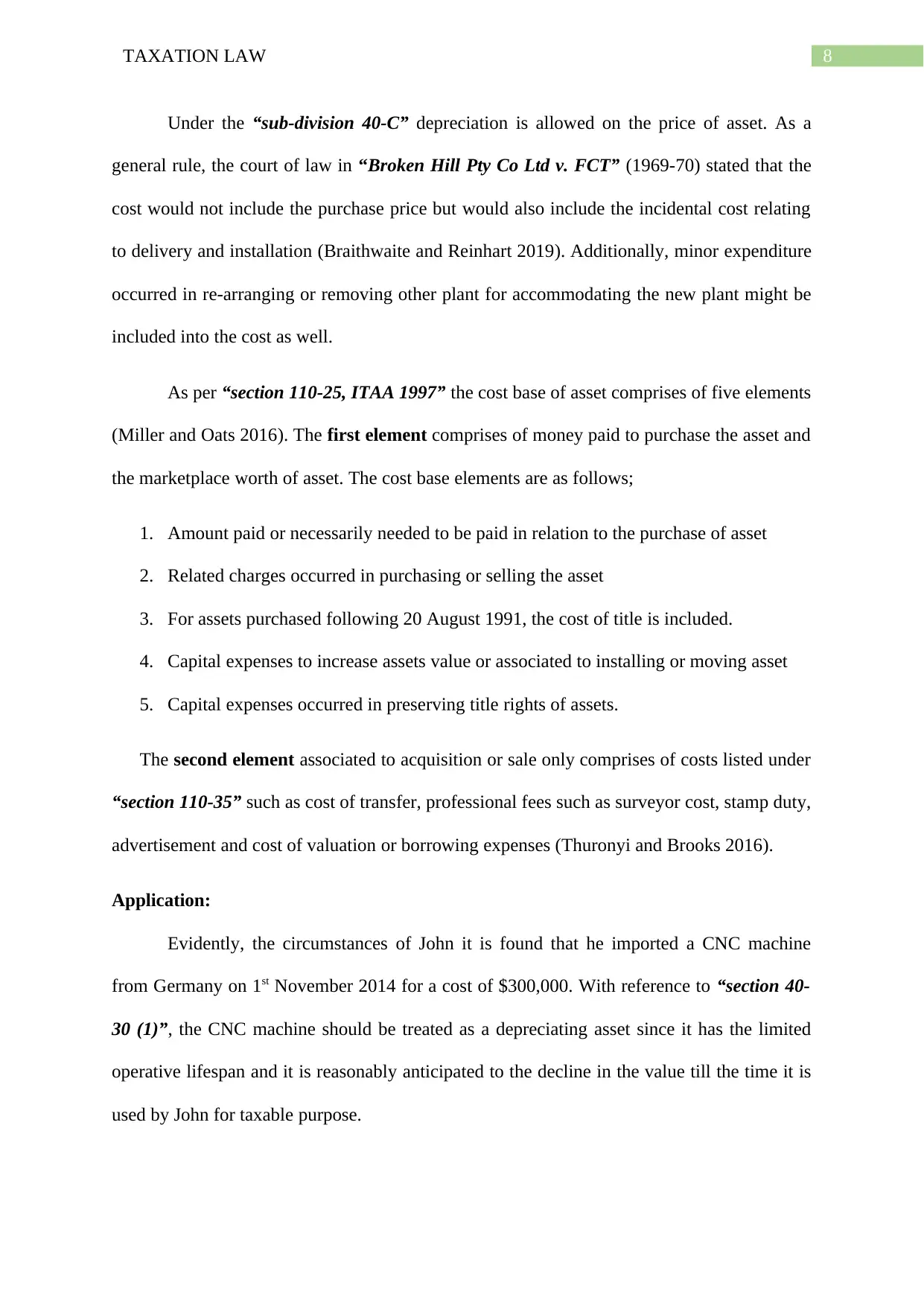

The asset cost base under “section 110-25, ITAA 1997” is computed below;

Computation of Cost Base of Asset

Particulars Amount ($)

Element Cost base item (S 110-25(1)-(6))

Element 1 Cost of Acquisition 3,00,000

Element 2 Incidental Cost - Inspection cost 12,000

Element 4 Capital Enhancement Cost - Guiding Rod 5,000

Element 4 Capital Expenditure - Installation Cost 25,000

Total Cost Base 3,42,000

Conclusion:

Conclusively, John can claim deduction under “section 40-25 (1), ITAA 1997” equal

to the decline in value of CNC from 15th January since the asset was first used for taxable

purpose. John is allowed to claim depreciation under the sub-division 40-C based on the

assets total cost base.

With reference to “section 40-60 (1)”, the start time of the CNC Machine is from 15th

January since it represents the time when the installation was completed and John first started

to use the asset (Bankman et al., 2018). Apart from this, John also incurred certain costs

following the installation of machine. This include a guiding rod which was installed on 1st

February for a cost of $5,000. Referring to “Broken Hill Pty Co Ltd v. FCT” (1969-70) the

cost base of the CNC machine would also contain the second element expenses such as the

guiding rod that was added later to the machinery.

John with reference to chief operative provision of “section 40-25 (1)” is permitted to

obtain income tax deduction equivalent to the decline in value of the CNC machine. While

the assets cost base under the first element of “section 110-25, ITAA 1997” would include

the amount paid in respect of the CNC machine (Buenker 2018). The second element

associated to acquisition is the cost incurred by John to inspect the CNC machine in Germany

since it is viewed as the related costs that is occured at the time of purchasing the asset.

The asset cost base under “section 110-25, ITAA 1997” is computed below;

Computation of Cost Base of Asset

Particulars Amount ($)

Element Cost base item (S 110-25(1)-(6))

Element 1 Cost of Acquisition 3,00,000

Element 2 Incidental Cost - Inspection cost 12,000

Element 4 Capital Enhancement Cost - Guiding Rod 5,000

Element 4 Capital Expenditure - Installation Cost 25,000

Total Cost Base 3,42,000

Conclusion:

Conclusively, John can claim deduction under “section 40-25 (1), ITAA 1997” equal

to the decline in value of CNC from 15th January since the asset was first used for taxable

purpose. John is allowed to claim depreciation under the sub-division 40-C based on the

assets total cost base.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

11TAXATION LAW

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School

of Social Sciences, The Australian National University.

Buenker, J.D., 2018. The Income Tax and the Progressive Era. Routledge.

Butler, D., 2019. Who can provide taxation advice?. Taxation in Australia, 53(7), p.381.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Davidson, P. and Evans, R., 2015. Fuel on the fire: Negative gearing, capital gains tax &

housing affordability. ACOSS Papers, p.29.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Liu, J., 2018. Understanding Australian commercial law. Taxation in Australia, 53(6), p.300.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Morgan, A. and Castelyn, D., 2018. Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

References:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School

of Social Sciences, The Australian National University.

Buenker, J.D., 2018. The Income Tax and the Progressive Era. Routledge.

Butler, D., 2019. Who can provide taxation advice?. Taxation in Australia, 53(7), p.381.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Davidson, P. and Evans, R., 2015. Fuel on the fire: Negative gearing, capital gains tax &

housing affordability. ACOSS Papers, p.29.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Liu, J., 2018. Understanding Australian commercial law. Taxation in Australia, 53(6), p.300.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Morgan, A. and Castelyn, D., 2018. Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.