Taxation Law Assignment: Compensation, CGT, and Main Residence

VerifiedAdded on 2022/11/19

|17

|4742

|160

Homework Assignment

AI Summary

This taxation law assignment examines the tax implications of various compensation receipts and capital gains tax (CGT) related to a beauty clinic owner and clients. The first part of the assignment explores the tax consequences of lump-sum damages for loss of reputation, compensation for loss of income, and reimbursement of legal fees for the beauty clinic owner, Sophie. The analysis references relevant taxation rulings and case law to determine whether these receipts are taxable income or capital in nature. The second part of the assignment delves into the CGT consequences for Joe and Amy, focusing on the disposal of a main residence, considering the deceased's pre- and post-CGT asset status, and the application of relevant CGT events. The assignment provides detailed explanations and legal references to support the conclusions regarding the tax treatment of different financial transactions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Introduction:...........................................................................................................................2

Various Compensation Receipts:...........................................................................................2

Sophie Client:.........................................................................................................................2

2.1: Lump sum damages for potential loss of reputation.......................................................2

2.2: Compensation for the loss of income whilst the machine was being replaced:..............3

2.3: Reimbursement of Legal Fees:.......................................................................................5

3: Kate Client:............................................................................................................................5

3.1 A Lump sum payment for pain and suffering:.................................................................5

3.2 Payment of ongoing medical and cosmetic surgery costs................................................6

3.3 Interest on the lump sum payment...................................................................................7

Conclusion:............................................................................................................................8

Answer to question 2:.................................................................................................................8

Introduction:...........................................................................................................................8

Issues:.....................................................................................................................................8

Laws:......................................................................................................................................8

Application:..........................................................................................................................12

References:...............................................................................................................................15

Table of Contents

Answer to question 1:.................................................................................................................2

Introduction:...........................................................................................................................2

Various Compensation Receipts:...........................................................................................2

Sophie Client:.........................................................................................................................2

2.1: Lump sum damages for potential loss of reputation.......................................................2

2.2: Compensation for the loss of income whilst the machine was being replaced:..............3

2.3: Reimbursement of Legal Fees:.......................................................................................5

3: Kate Client:............................................................................................................................5

3.1 A Lump sum payment for pain and suffering:.................................................................5

3.2 Payment of ongoing medical and cosmetic surgery costs................................................6

3.3 Interest on the lump sum payment...................................................................................7

Conclusion:............................................................................................................................8

Answer to question 2:.................................................................................................................8

Introduction:...........................................................................................................................8

Issues:.....................................................................................................................................8

Laws:......................................................................................................................................8

Application:..........................................................................................................................12

References:...............................................................................................................................15

2TAXATION LAW

Answer to question 1:

Introduction:

Issues:

1.1. The problems concerned in this question is linked with the tax implications of lump

sum amount of damages that is received by the taxpayer as the compensation for the

income loss and reimbursement that relates to the legal fees by Sophie and Kate. Whether

or not such receipts will be considered taxable as income under the ordinary sense of “sec

6-5, ITAA 1997”.

1.2. Another issue that is concerned in this question is regarding the consequences of

capital gains tax that transpires from the payment relating to the damages that is received,

whether or not such kinds of payment will be treated for assessment under “sec 118-37,

ITAA 1997”.

Various Compensation Receipts:

Sophie Client:

2.1: Lump sum damages for potential loss of reputation

Laws:

The description that is made in the “Taxation Ruling of TR 95/35” involves the

application of taxes on the earnings made by a taxpayer from receiving any compensation.

This ruling is imposed on taxpayers that reports the receipts from compensation (Bankman et

al., 2018). The “Taxation Ruling of TR 95/35” is regarded as supportive in establishing the

consequences of the CGT that is linked with the receipt of compensation and ascertaining

whether the money that is received will be considered taxable earnings for the recipient in

“Part IIIA of the ITAA 1936”.

Answer to question 1:

Introduction:

Issues:

1.1. The problems concerned in this question is linked with the tax implications of lump

sum amount of damages that is received by the taxpayer as the compensation for the

income loss and reimbursement that relates to the legal fees by Sophie and Kate. Whether

or not such receipts will be considered taxable as income under the ordinary sense of “sec

6-5, ITAA 1997”.

1.2. Another issue that is concerned in this question is regarding the consequences of

capital gains tax that transpires from the payment relating to the damages that is received,

whether or not such kinds of payment will be treated for assessment under “sec 118-37,

ITAA 1997”.

Various Compensation Receipts:

Sophie Client:

2.1: Lump sum damages for potential loss of reputation

Laws:

The description that is made in the “Taxation Ruling of TR 95/35” involves the

application of taxes on the earnings made by a taxpayer from receiving any compensation.

This ruling is imposed on taxpayers that reports the receipts from compensation (Bankman et

al., 2018). The “Taxation Ruling of TR 95/35” is regarded as supportive in establishing the

consequences of the CGT that is linked with the receipt of compensation and ascertaining

whether the money that is received will be considered taxable earnings for the recipient in

“Part IIIA of the ITAA 1936”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

On finding that the taxpayer has got compensation which is primarily as the outcome

of disposal of any form of underlying asset or any part of the underlying asset of taxpayer,

then in such situation the compensation received will be treated as consideration obtained

from disposing the underlying asset (Oishi et al., 2018). The decision which is passed by the

law court in “Speedly Securities Ltd v FC of T (1988)” on receiving any form of

compensation for the damage of goodwill of business the amount that is given to the taxpayer

is treated capital in nature.

Application:

As understood from the situation of Sophie, it is noticed that she has bought forward a

law suit against Fracpro for providing her with the laser machine that had faulty calibration.

In return Sophie was compensated by Fracpro because she suffered loss of business goodwill

and reputation. The amount of $100,000 given to Sophie by Fracpro amounted to damages

that is received on account of loss of business reputation. By referring the decision that was

made in “Speedly Securities Ltd v FC of T (1988)” the sum of $10,000 that is given to

Sophie is a compensation for the loss business reputation (Schenk, 2017). The money

received does not hold any character of ordinary taxable income under “sec 6-5, ITAA 1997”

and the amount must be considered as the capital in nature.

2.2: Compensation for the loss of income whilst the machine was being replaced:

Laws:

The elucidation that has been given in “taxation determination ruling of TD 93/58”

there are some instances when a taxpayer receives any compensation as the lump sum amount

or in regard to the settlement payment, then the amount that will be received will be held as

taxable income (Miller, 2018). When noticing that the taxpayer has received compensation

On finding that the taxpayer has got compensation which is primarily as the outcome

of disposal of any form of underlying asset or any part of the underlying asset of taxpayer,

then in such situation the compensation received will be treated as consideration obtained

from disposing the underlying asset (Oishi et al., 2018). The decision which is passed by the

law court in “Speedly Securities Ltd v FC of T (1988)” on receiving any form of

compensation for the damage of goodwill of business the amount that is given to the taxpayer

is treated capital in nature.

Application:

As understood from the situation of Sophie, it is noticed that she has bought forward a

law suit against Fracpro for providing her with the laser machine that had faulty calibration.

In return Sophie was compensated by Fracpro because she suffered loss of business goodwill

and reputation. The amount of $100,000 given to Sophie by Fracpro amounted to damages

that is received on account of loss of business reputation. By referring the decision that was

made in “Speedly Securities Ltd v FC of T (1988)” the sum of $10,000 that is given to

Sophie is a compensation for the loss business reputation (Schenk, 2017). The money

received does not hold any character of ordinary taxable income under “sec 6-5, ITAA 1997”

and the amount must be considered as the capital in nature.

2.2: Compensation for the loss of income whilst the machine was being replaced:

Laws:

The elucidation that has been given in “taxation determination ruling of TD 93/58”

there are some instances when a taxpayer receives any compensation as the lump sum amount

or in regard to the settlement payment, then the amount that will be received will be held as

taxable income (Miller, 2018). When noticing that the taxpayer has received compensation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

for the loss of income then those receipts attracts tax liability under the legislative provision

of “subsection 25 (1) of the ITAA 1936”, provided that;

a. The amount received by taxpayer constitute the payment made as compensation for

the loss of income; or

b. The payment to a certain extent can be identified and categorized as income (Feld,

2016). This becomes possible only when there is an existence of impliedly or

expressly agreement between either of the parties that some portion of the

compensation that is received is related to the loss of income.

The judgement that was handed down by the federal court in “Allsop v FC of T

(1965)” noted that the amount received by the recipient that was included into the lump sum

receipt also holds the nature of capital as well (Schmalbeck et al., 2015). But, the ingredients

of the payment can be identified as income and a portion of those payments which is related

to income is considered as taxable income.

Application:

The case study vibrantly provides that Sophie has received compensation from

Fracpro that is associated to the loss of income. The lump sum value of $20,000 that is

received as loss of income must be treated as carrying the elements of income and would be

treated taxable under the legislation of “subsection 25 (1) of the ITAA 1936”. By denoting

the judgement that was given in “Allsop v FC of T (1965)” the lump sum value of $20,000

received as loss of income by Sophie is regarded as income (Abrams & Leatherman, 2019).

This is because the amount received by Sophie is quantifiable and indefinable as receipts of

income nature. Hence, under the legislative provision of “subsection 25 (1) of the ITAA

1936” the lump sum value of $20,000 is a taxable income for Sophie.

for the loss of income then those receipts attracts tax liability under the legislative provision

of “subsection 25 (1) of the ITAA 1936”, provided that;

a. The amount received by taxpayer constitute the payment made as compensation for

the loss of income; or

b. The payment to a certain extent can be identified and categorized as income (Feld,

2016). This becomes possible only when there is an existence of impliedly or

expressly agreement between either of the parties that some portion of the

compensation that is received is related to the loss of income.

The judgement that was handed down by the federal court in “Allsop v FC of T

(1965)” noted that the amount received by the recipient that was included into the lump sum

receipt also holds the nature of capital as well (Schmalbeck et al., 2015). But, the ingredients

of the payment can be identified as income and a portion of those payments which is related

to income is considered as taxable income.

Application:

The case study vibrantly provides that Sophie has received compensation from

Fracpro that is associated to the loss of income. The lump sum value of $20,000 that is

received as loss of income must be treated as carrying the elements of income and would be

treated taxable under the legislation of “subsection 25 (1) of the ITAA 1936”. By denoting

the judgement that was given in “Allsop v FC of T (1965)” the lump sum value of $20,000

received as loss of income by Sophie is regarded as income (Abrams & Leatherman, 2019).

This is because the amount received by Sophie is quantifiable and indefinable as receipts of

income nature. Hence, under the legislative provision of “subsection 25 (1) of the ITAA

1936” the lump sum value of $20,000 is a taxable income for Sophie.

5TAXATION LAW

2.3: Reimbursement of Legal Fees:

Laws:

As elaborated under the “section 118-37 (2)”, the taxpayers are required to simply

overlook the capital gains and loss when they receive any form of reimbursement for the

outgoings that is occurred by them (Sadiq et al., 2016). This usually includes the

reimbursement associated to the legal expenditure. The legal expense reimbursement cannot

be regarded as the capital gains because they are treated as the capital asset for those that

receives it.

Application:

The case study of Sophie provides an instance where it is noticed that she received a

reimbursement of legal expenditure that she has occurred when bringing a law suit against the

Fracpro. The reimbursement of the legal expenditure must be regarded as the element of the

cost base of business. As a result, no CGT consequences arises in this context regarding the

receipt of legal expenditure.

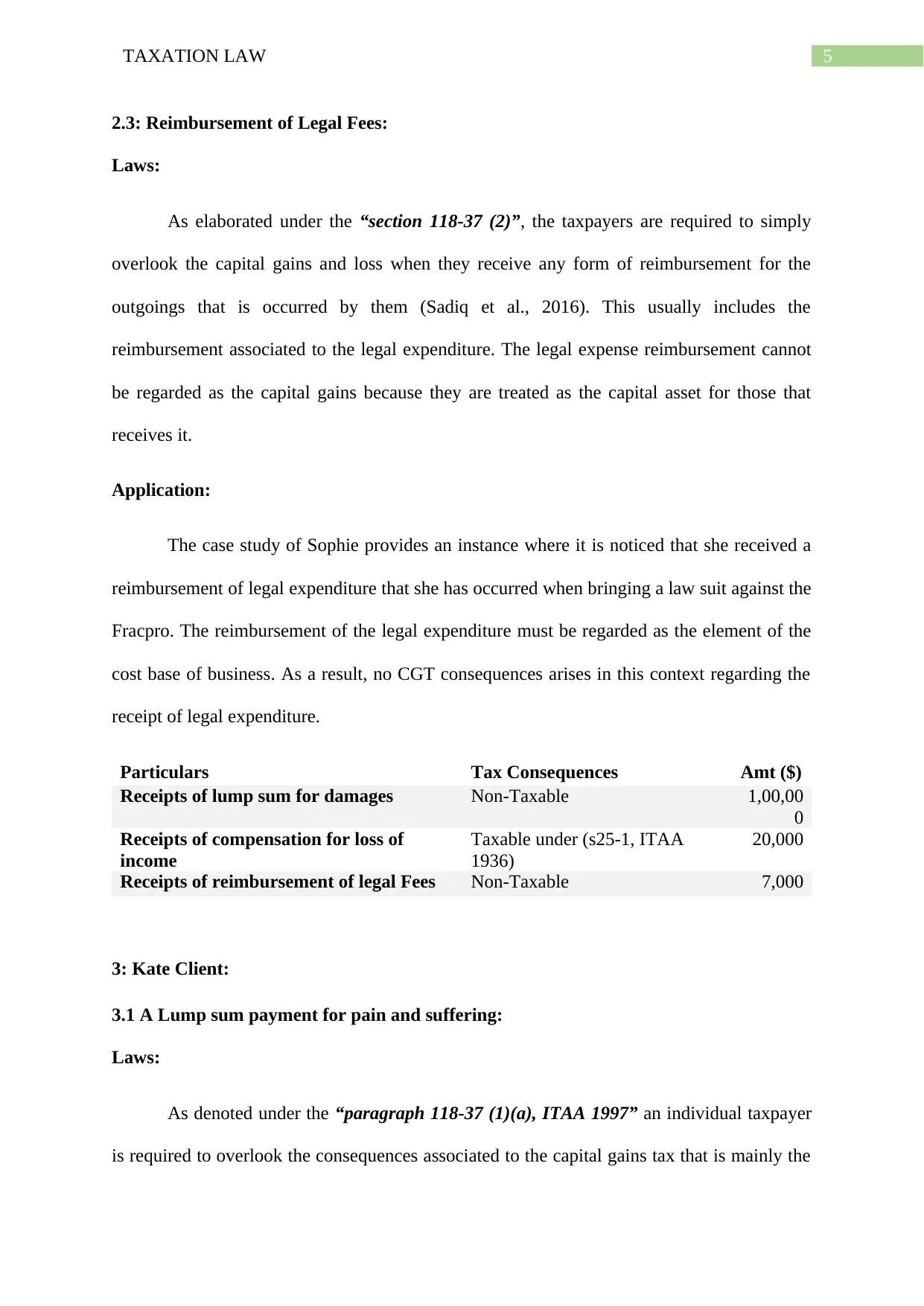

Particulars Tax Consequences Amt ($)

Receipts of lump sum for damages Non-Taxable 1,00,00

0

Receipts of compensation for loss of

income

Taxable under (s25-1, ITAA

1936)

20,000

Receipts of reimbursement of legal Fees Non-Taxable 7,000

3: Kate Client:

3.1 A Lump sum payment for pain and suffering:

Laws:

As denoted under the “paragraph 118-37 (1)(a), ITAA 1997” an individual taxpayer

is required to overlook the consequences associated to the capital gains tax that is mainly the

2.3: Reimbursement of Legal Fees:

Laws:

As elaborated under the “section 118-37 (2)”, the taxpayers are required to simply

overlook the capital gains and loss when they receive any form of reimbursement for the

outgoings that is occurred by them (Sadiq et al., 2016). This usually includes the

reimbursement associated to the legal expenditure. The legal expense reimbursement cannot

be regarded as the capital gains because they are treated as the capital asset for those that

receives it.

Application:

The case study of Sophie provides an instance where it is noticed that she received a

reimbursement of legal expenditure that she has occurred when bringing a law suit against the

Fracpro. The reimbursement of the legal expenditure must be regarded as the element of the

cost base of business. As a result, no CGT consequences arises in this context regarding the

receipt of legal expenditure.

Particulars Tax Consequences Amt ($)

Receipts of lump sum for damages Non-Taxable 1,00,00

0

Receipts of compensation for loss of

income

Taxable under (s25-1, ITAA

1936)

20,000

Receipts of reimbursement of legal Fees Non-Taxable 7,000

3: Kate Client:

3.1 A Lump sum payment for pain and suffering:

Laws:

As denoted under the “paragraph 118-37 (1)(a), ITAA 1997” an individual taxpayer

is required to overlook the consequences associated to the capital gains tax that is mainly the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

outcome of the compensation receipt derived from the injuries or any form of wrong doings

suffered by a person (Kenny et al., 2016). An important explanation has been made in the

“paragraph 118-37 (1)(a), ITAA 1997” where it states that the capital gains which is

obtained from the “right to seek” compensation is generally ignored. This is because the

receipts that are received by the taxpayer are treated as capital in type.

Application:

The case of Kate brings forward that the lump sum amount of money is given to Kate

by Fracpro because she has suffered personal injuries and pain from the faulty calibration of

the laser machine. The compensation were mainly for the medical treatment. The lump sum

amount given to Kate for medical treatment will be considered as the payment for personal

injuries. With respect to the “paragraph 118-37 (1)(a), ITAA 1997” Kate should simply

ignore any kind of capital gains or capital loss that is made from the compensation that is

received for the wrong and injuries suffered by her personally (Stumbles et al., 2016). This

implies that the compensation that is received by Kate for the personal injury is not included

into her assessable income by virtue of the CGT provisions. Neither the compensation

amounts to ordinary income nor it is a statutory income. Therefore it is not taxable under

“subsection 6-15, ITAA 1997” as assessable income.

3.2 Payment of ongoing medical and cosmetic surgery costs

Laws:

As explained in the “paragraph 118-37(1)(a), ITAA 1997” capital gains should be

disregarded if the compensation or damages that is given to the taxpayer as the outcome of

illness or injury suffered on a personal account (Sadiq et al., 2016). The Taxation Ruling of

TR 95/35, compensation receipts comprises of the sum received by the taxpayer in respect of

the right of seeking compensation or any kind of proceedings instituted by the taxpayer due

outcome of the compensation receipt derived from the injuries or any form of wrong doings

suffered by a person (Kenny et al., 2016). An important explanation has been made in the

“paragraph 118-37 (1)(a), ITAA 1997” where it states that the capital gains which is

obtained from the “right to seek” compensation is generally ignored. This is because the

receipts that are received by the taxpayer are treated as capital in type.

Application:

The case of Kate brings forward that the lump sum amount of money is given to Kate

by Fracpro because she has suffered personal injuries and pain from the faulty calibration of

the laser machine. The compensation were mainly for the medical treatment. The lump sum

amount given to Kate for medical treatment will be considered as the payment for personal

injuries. With respect to the “paragraph 118-37 (1)(a), ITAA 1997” Kate should simply

ignore any kind of capital gains or capital loss that is made from the compensation that is

received for the wrong and injuries suffered by her personally (Stumbles et al., 2016). This

implies that the compensation that is received by Kate for the personal injury is not included

into her assessable income by virtue of the CGT provisions. Neither the compensation

amounts to ordinary income nor it is a statutory income. Therefore it is not taxable under

“subsection 6-15, ITAA 1997” as assessable income.

3.2 Payment of ongoing medical and cosmetic surgery costs

Laws:

As explained in the “paragraph 118-37(1)(a), ITAA 1997” capital gains should be

disregarded if the compensation or damages that is given to the taxpayer as the outcome of

illness or injury suffered on a personal account (Sadiq et al., 2016). The Taxation Ruling of

TR 95/35, compensation receipts comprises of the sum received by the taxpayer in respect of

the right of seeking compensation or any kind of proceedings instituted by the taxpayer due

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

to the cause of action. A claim made for the past and future medical expenditure cannot be

regarded as taxable income.

Application:

The evidences that is gained from the situation of Kate suggest she received cost for

medical and cosmetic surgery. Under the “paragraph 118-37(1)(a), ITAA 1997” the claims

for medical expenses should be ignored since the compensation or damages that is given to

Kate as the outcome of illness or injury suffered on a personal account (Kenny, 2015). The

compensation does not amounts to ordinary income nor is it a statutory income. Therefore it

is not taxable under “subsection 6-15, ITAA 1997” as assessable income.

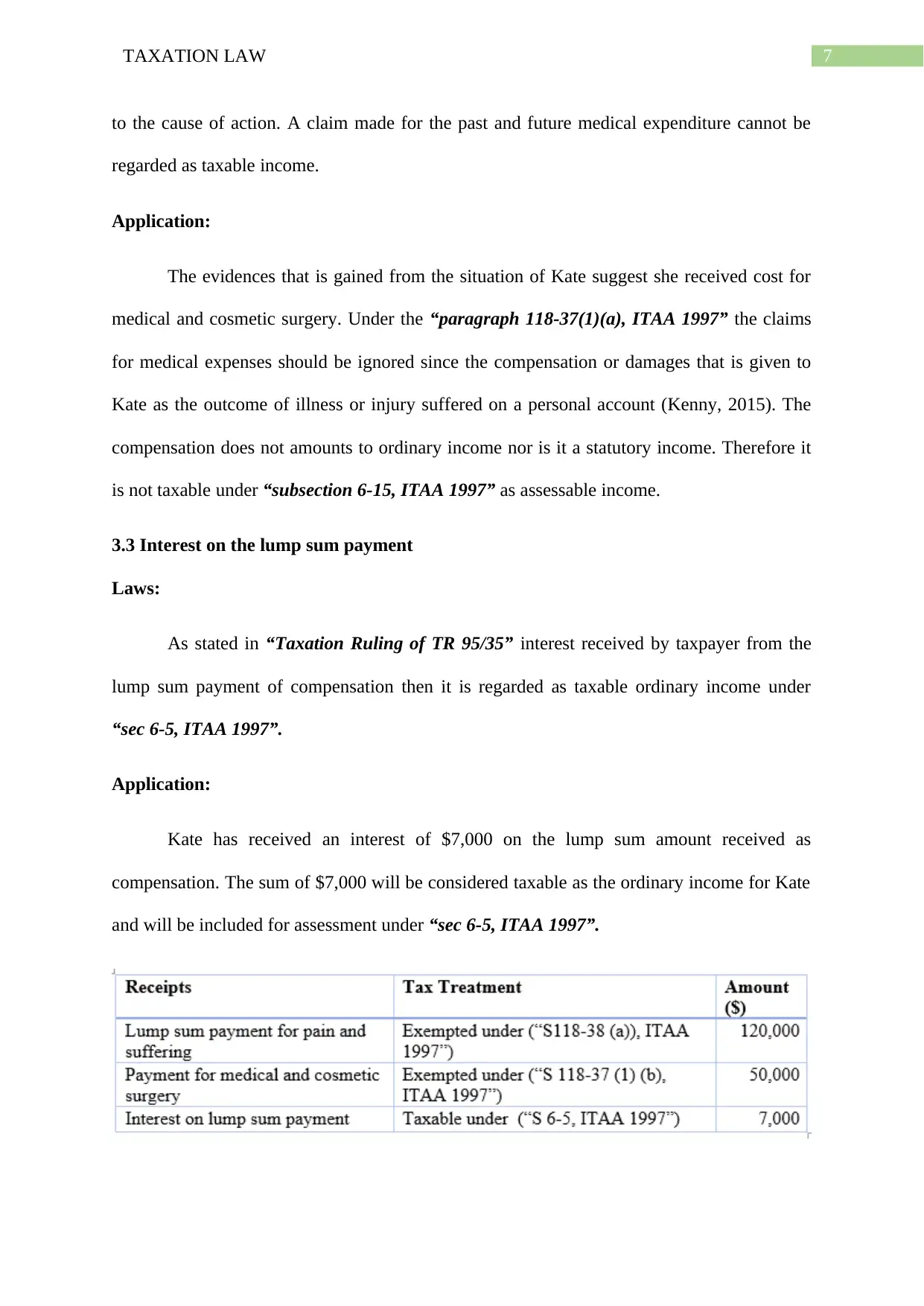

3.3 Interest on the lump sum payment

Laws:

As stated in “Taxation Ruling of TR 95/35” interest received by taxpayer from the

lump sum payment of compensation then it is regarded as taxable ordinary income under

“sec 6-5, ITAA 1997”.

Application:

Kate has received an interest of $7,000 on the lump sum amount received as

compensation. The sum of $7,000 will be considered taxable as the ordinary income for Kate

and will be included for assessment under “sec 6-5, ITAA 1997”.

to the cause of action. A claim made for the past and future medical expenditure cannot be

regarded as taxable income.

Application:

The evidences that is gained from the situation of Kate suggest she received cost for

medical and cosmetic surgery. Under the “paragraph 118-37(1)(a), ITAA 1997” the claims

for medical expenses should be ignored since the compensation or damages that is given to

Kate as the outcome of illness or injury suffered on a personal account (Kenny, 2015). The

compensation does not amounts to ordinary income nor is it a statutory income. Therefore it

is not taxable under “subsection 6-15, ITAA 1997” as assessable income.

3.3 Interest on the lump sum payment

Laws:

As stated in “Taxation Ruling of TR 95/35” interest received by taxpayer from the

lump sum payment of compensation then it is regarded as taxable ordinary income under

“sec 6-5, ITAA 1997”.

Application:

Kate has received an interest of $7,000 on the lump sum amount received as

compensation. The sum of $7,000 will be considered taxable as the ordinary income for Kate

and will be included for assessment under “sec 6-5, ITAA 1997”.

8TAXATION LAW

Conclusion:

The lump sum payment received by Sophie and Kate cannot be considered as

outcome of any personal services rather it amounts to compensation for the pain and injuries

suffered both professional and personally. The compensation amount will be considered

capital receipt under “sec 118-38 (a)” and “sec 118-37 (1) (b), ITAA 1997”.

Answer to question 2:

Introduction:

Issues:

The problem that is taken under discussion is regarding the outcome associated to the

capital gains tax consequences for Joe and Amy, the taxpayer in the present case, for the

disposal of main residence assuming that;

a. The main residence can be considered as the post-CGT asset of the deceased

b. The property was viewed as the main house of dwelling for the deceased before the

death

c. The main house of dwelling was obtained by the present taxpayer in the current based

on the will of deceased estate.

d. The present taxpayer lived in the as their main residence from the day when the

deceased passed away till the day when the main dwelling was disposed.

Laws:

The CGT is made applicable commonly on the assets that is purchased or events that

happens on or following the 20 September 1985. Accordingly, there are certain common

terms that are used to refer the assets acquired are the word pre-CGT and post-CGT (Miller,

2018). This is mainly because of the events that occurs prior to or after the aforementioned

date. Assets that are bought before the introduction of the CGT system or before 19th

Conclusion:

The lump sum payment received by Sophie and Kate cannot be considered as

outcome of any personal services rather it amounts to compensation for the pain and injuries

suffered both professional and personally. The compensation amount will be considered

capital receipt under “sec 118-38 (a)” and “sec 118-37 (1) (b), ITAA 1997”.

Answer to question 2:

Introduction:

Issues:

The problem that is taken under discussion is regarding the outcome associated to the

capital gains tax consequences for Joe and Amy, the taxpayer in the present case, for the

disposal of main residence assuming that;

a. The main residence can be considered as the post-CGT asset of the deceased

b. The property was viewed as the main house of dwelling for the deceased before the

death

c. The main house of dwelling was obtained by the present taxpayer in the current based

on the will of deceased estate.

d. The present taxpayer lived in the as their main residence from the day when the

deceased passed away till the day when the main dwelling was disposed.

Laws:

The CGT is made applicable commonly on the assets that is purchased or events that

happens on or following the 20 September 1985. Accordingly, there are certain common

terms that are used to refer the assets acquired are the word pre-CGT and post-CGT (Miller,

2018). This is mainly because of the events that occurs prior to or after the aforementioned

date. Assets that are bought before the introduction of the CGT system or before 19th

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

September 1985 then it is termed as the pre-CGT asset. On the other hand, the assets that are

acquired after this date are termed as post-CGT asset. Capital gains are ignored from the

events occurring for the pre-CGT asset while the post-CGT events are only included into the

assessable income and tax regimes. The sale of CGT asset usually results in CGT event A1

under “sec 104-10, ITAA 1997”. When making the disposal of the assets when the proceeds

exceeds the cost base then the capital gains would originate.

Where the net capital gains has been accrued to the taxpayer during the relevant

income year, that gain is included in the assessable income of the taxpayer for that year

(Siebert, 2019). The capital is not considered for deduction but it is rather allowed for offset

against the capital gains made during the same year or in the future years to ascertain the net

capital gains. The wider concept of the CGT usually involves the comparison among the

capital proceeds and the cost base of the assets. A capital gains or loss is usually ascertained

by subtracting the relevant cost base associated to the asset or events that takes from the

capital proceeds following the sale of the asset or other forms of events.

For a taxpayer to obtain the exemption on the main house of dwelling under “sec

118-110, ITAA 1997”, the house must qualify as the main dwelling for the taxpayer

(Lieuallen & Shurtz, 2018). When it is noticed that the taxpayer has more than one dwelling,

then it becomes necessary to ascertain which dwelling is used by the taxpayer as his or her

main residence and hence eligible for exemption. When it is noticed that the taxpayer has

owned only a single house of dwelling, then it self cannot be viewed as sufficient enough that

house is being used by the taxpayer as their main dwelling. Whether the dwelling is regarded

as the main house of residence is completely dependent on the fact. There are some of the

important factors that should be considered;

a. The amount of time the taxpayer has spent on the house.

September 1985 then it is termed as the pre-CGT asset. On the other hand, the assets that are

acquired after this date are termed as post-CGT asset. Capital gains are ignored from the

events occurring for the pre-CGT asset while the post-CGT events are only included into the

assessable income and tax regimes. The sale of CGT asset usually results in CGT event A1

under “sec 104-10, ITAA 1997”. When making the disposal of the assets when the proceeds

exceeds the cost base then the capital gains would originate.

Where the net capital gains has been accrued to the taxpayer during the relevant

income year, that gain is included in the assessable income of the taxpayer for that year

(Siebert, 2019). The capital is not considered for deduction but it is rather allowed for offset

against the capital gains made during the same year or in the future years to ascertain the net

capital gains. The wider concept of the CGT usually involves the comparison among the

capital proceeds and the cost base of the assets. A capital gains or loss is usually ascertained

by subtracting the relevant cost base associated to the asset or events that takes from the

capital proceeds following the sale of the asset or other forms of events.

For a taxpayer to obtain the exemption on the main house of dwelling under “sec

118-110, ITAA 1997”, the house must qualify as the main dwelling for the taxpayer

(Lieuallen & Shurtz, 2018). When it is noticed that the taxpayer has more than one dwelling,

then it becomes necessary to ascertain which dwelling is used by the taxpayer as his or her

main residence and hence eligible for exemption. When it is noticed that the taxpayer has

owned only a single house of dwelling, then it self cannot be viewed as sufficient enough that

house is being used by the taxpayer as their main dwelling. Whether the dwelling is regarded

as the main house of residence is completely dependent on the fact. There are some of the

important factors that should be considered;

a. The amount of time the taxpayer has spent on the house.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

b. The place where the family of the taxpayer resides

c. Whether or not the taxpayer has moved his personal belongings in the dwelling

d. The fixed address of the taxpayer where the main is delivered

e. The intention of taxpayer in occupying the new dwelling

f. Connection of the services such as telephone, gas etc. for the taxpayer.

As evident from the above stated factors, there should be some certain degree of

occupancy that is required to set up the entitlements for main residence exemption.

There are some important rules that are associated to the CGT event and demise of an

individual taxpayer. As per the broad rule, when the taxpayer dies, under the “sec 128-10,

ITAA 1997” the CGT event linked to the CGT asset is ignored. In the event of the death of

the taxpayer their lawful heirs is assumed to hold the possession of the asset on the very same

day when the taxpayer passes away (Miller & Oats, 2016). Where the asset becomes the pre-

CGT asset of the deceased taxpayer, the new heir or the beneficiary is supposed to hold the

possession of the asset with the respect to the current market value on the day of demise. Sec

“128-15, ITAA 1997” delivers elucidation regarding the inherited post-CGT assets (Arnold,

2019). Where the asset turn out to be the post-CGT asset of the deceased taxpayer, the new

heir or the recipient is believed to hold the ownership of the asset with the respect to the

existing market price on the day of demise.

Discussion concerning the inherited main residence is given in “sec 188-195, ITAA

1997”. On noticing that the asset constitutes the main residence of the deceased taxpayer and

the property is not put into use for the purpose of making taxable earnings, the cost base of

the property to the heir in this situation denotes the market price on the day of demise (Evans

et al., 2015). When noticing that the asset formed the main dwelling of the deceased, the

b. The place where the family of the taxpayer resides

c. Whether or not the taxpayer has moved his personal belongings in the dwelling

d. The fixed address of the taxpayer where the main is delivered

e. The intention of taxpayer in occupying the new dwelling

f. Connection of the services such as telephone, gas etc. for the taxpayer.

As evident from the above stated factors, there should be some certain degree of

occupancy that is required to set up the entitlements for main residence exemption.

There are some important rules that are associated to the CGT event and demise of an

individual taxpayer. As per the broad rule, when the taxpayer dies, under the “sec 128-10,

ITAA 1997” the CGT event linked to the CGT asset is ignored. In the event of the death of

the taxpayer their lawful heirs is assumed to hold the possession of the asset on the very same

day when the taxpayer passes away (Miller & Oats, 2016). Where the asset becomes the pre-

CGT asset of the deceased taxpayer, the new heir or the beneficiary is supposed to hold the

possession of the asset with the respect to the current market value on the day of demise. Sec

“128-15, ITAA 1997” delivers elucidation regarding the inherited post-CGT assets (Arnold,

2019). Where the asset turn out to be the post-CGT asset of the deceased taxpayer, the new

heir or the recipient is believed to hold the ownership of the asset with the respect to the

existing market price on the day of demise.

Discussion concerning the inherited main residence is given in “sec 188-195, ITAA

1997”. On noticing that the asset constitutes the main residence of the deceased taxpayer and

the property is not put into use for the purpose of making taxable earnings, the cost base of

the property to the heir in this situation denotes the market price on the day of demise (Evans

et al., 2015). When noticing that the asset formed the main dwelling of the deceased, the

11TAXATION LAW

beneficiary in this situation can inherit the exemption on the main dwelling upon satisfying

the required conditions.

Under the “division 110”, the cost base of the asset is generally ascertained (Yates,

2016). Under “sec 128-15, ITAA 1997” nevertheless, when the ownership of the asset is

passed on to the taxpayer on the basis of the deceased’s legal heir, the house was put into use

for main dwelling of the taxpayer instantly prior to demise and was never utilized for making

income, the cost base is represented on the basis of the market value of CGT asset.

Under the “sec 118-195”, capital gains or loss that are originating from the CGT event in

respect to the main dwelling is ignored in some of the situation. This includes when the

taxpayer is regarded as the individual and interest of title is given to the taxpayer in the form

of heir, or the taxpayer has owned as the trustee of deceased estate (Feld et al., 2016). While

“sec 118-195, ITAA 1997”, also explains that when the asset is viewed as the pre-CGT asset

to the receiver of the deceased and it is sold inside two years of deceased death or any long

time period given the commissioner has applied any discretion, a full exemption under this is

situation is available to the taxpayer from CGT.

In the alternative situation given in the “sec 118-195”,, on discovering that the asset is

the pre-CGT asset and sold inside the prescribed time period, then full exemption may still be

available to the taxpayer on meeting certain criteria given under this act (Chardon et al.,

2016). This includes, if from the day of demise until the day when the title of interest comes

to an end, it formed the main residence of either;

a. The deceased spouse or

b. An individual that is treated as having the right of occupying the asset under the will

of deceased; or

beneficiary in this situation can inherit the exemption on the main dwelling upon satisfying

the required conditions.

Under the “division 110”, the cost base of the asset is generally ascertained (Yates,

2016). Under “sec 128-15, ITAA 1997” nevertheless, when the ownership of the asset is

passed on to the taxpayer on the basis of the deceased’s legal heir, the house was put into use

for main dwelling of the taxpayer instantly prior to demise and was never utilized for making

income, the cost base is represented on the basis of the market value of CGT asset.

Under the “sec 118-195”, capital gains or loss that are originating from the CGT event in

respect to the main dwelling is ignored in some of the situation. This includes when the

taxpayer is regarded as the individual and interest of title is given to the taxpayer in the form

of heir, or the taxpayer has owned as the trustee of deceased estate (Feld et al., 2016). While

“sec 118-195, ITAA 1997”, also explains that when the asset is viewed as the pre-CGT asset

to the receiver of the deceased and it is sold inside two years of deceased death or any long

time period given the commissioner has applied any discretion, a full exemption under this is

situation is available to the taxpayer from CGT.

In the alternative situation given in the “sec 118-195”,, on discovering that the asset is

the pre-CGT asset and sold inside the prescribed time period, then full exemption may still be

available to the taxpayer on meeting certain criteria given under this act (Chardon et al.,

2016). This includes, if from the day of demise until the day when the title of interest comes

to an end, it formed the main residence of either;

a. The deceased spouse or

b. An individual that is treated as having the right of occupying the asset under the will

of deceased; or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.