Taxation Law Assignment: Question Answers - Taxation Law 2 Course

VerifiedAdded on 2021/06/17

|11

|1786

|23

Homework Assignment

AI Summary

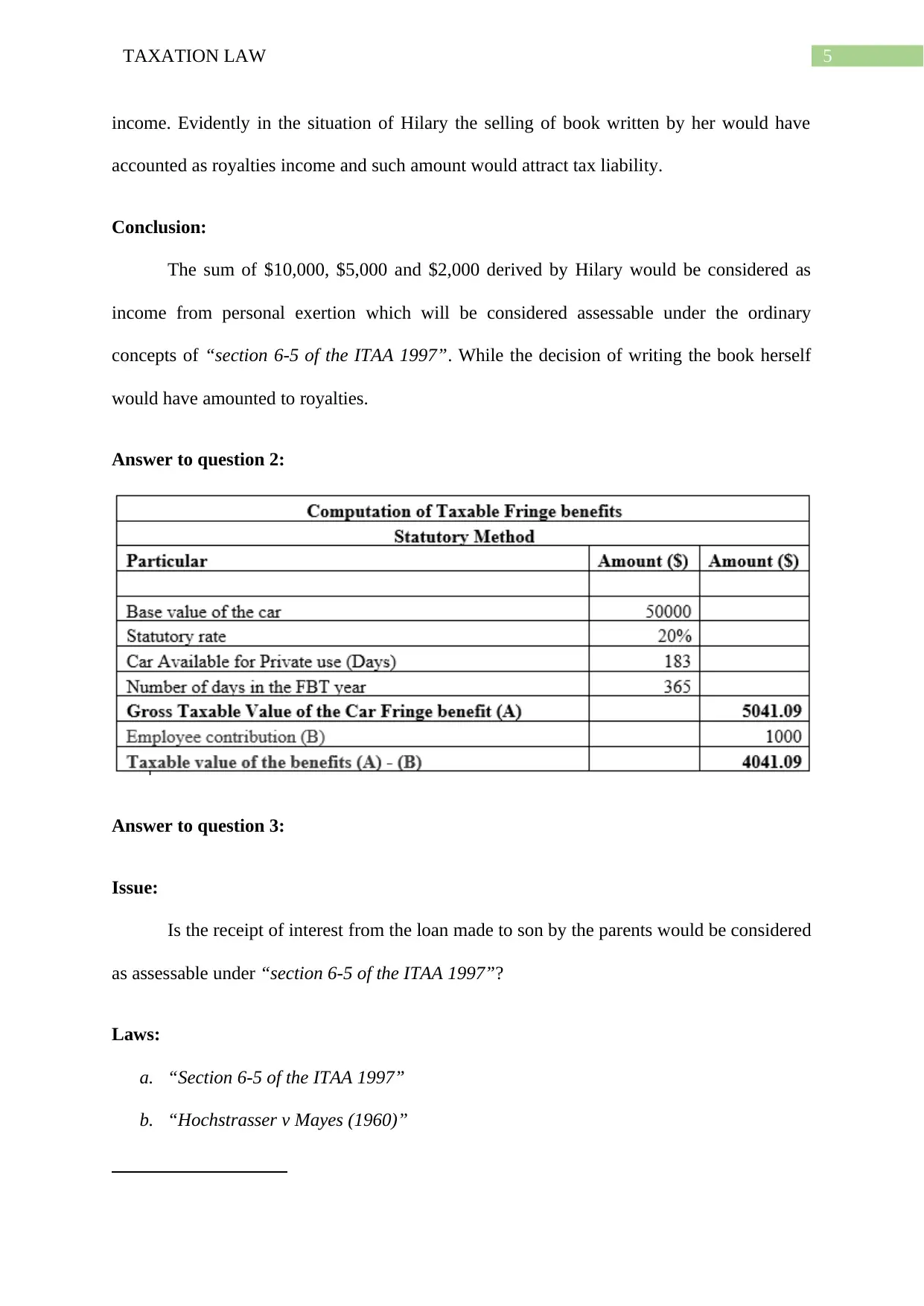

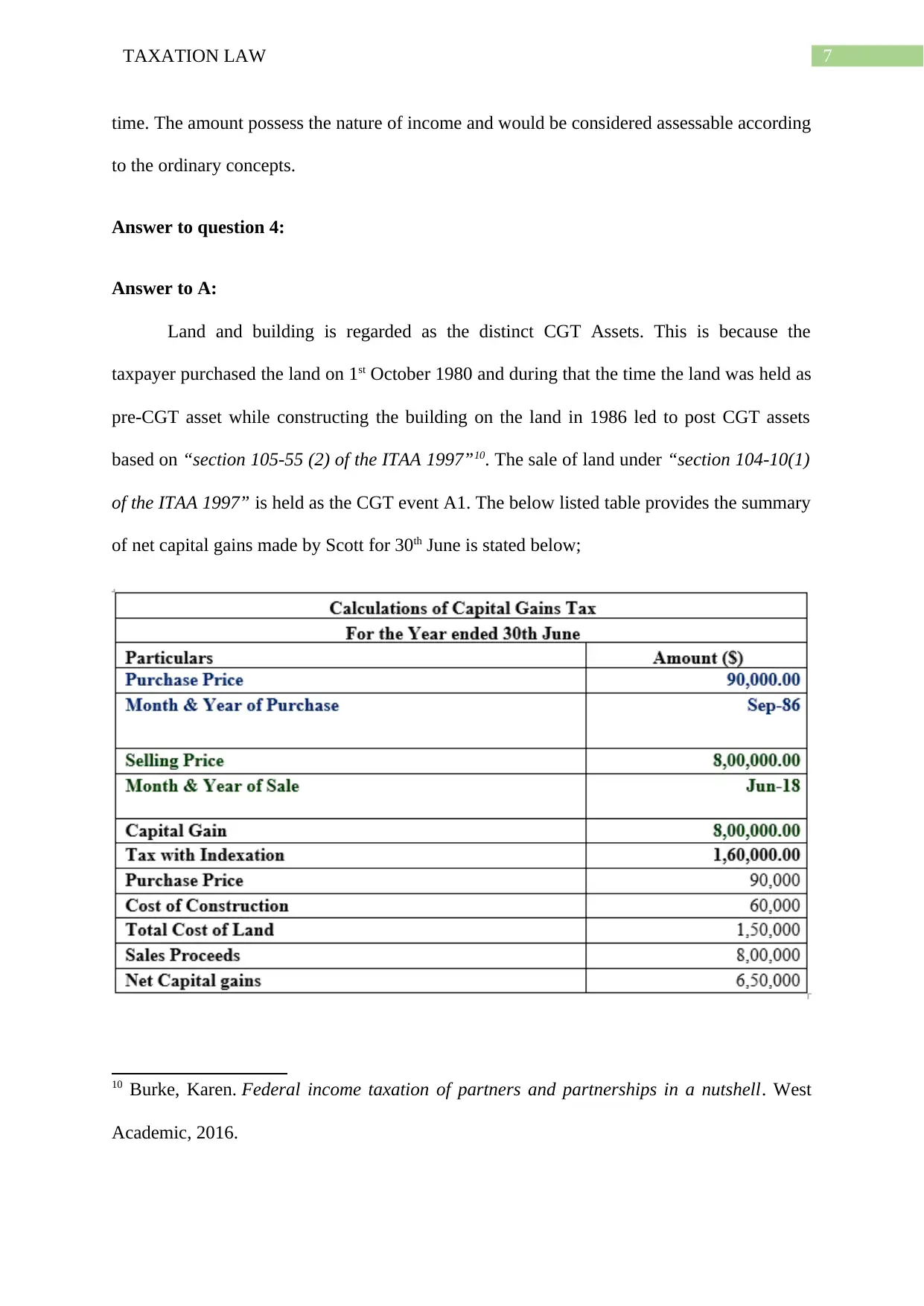

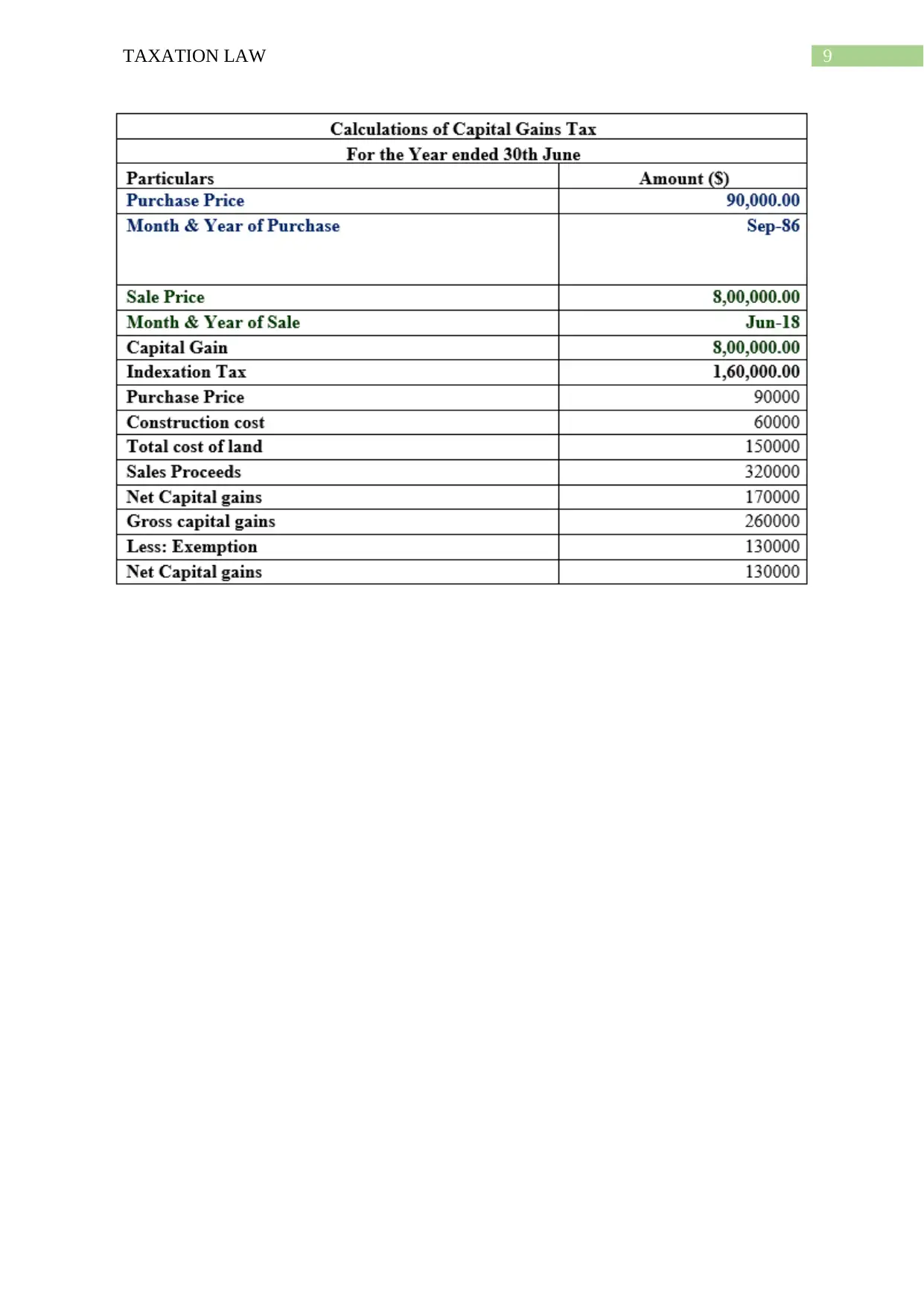

This Taxation Law assignment solution addresses several key areas of taxation, including assessable income, capital gains tax (CGT), and relevant case law. The first question examines whether income from selling book interests and photographs is taxable under section 6-5 of the ITAA 1997, referencing cases like Brent v Federal Commissioner of Taxation. The second question, though not fully present, implies discussion on related topics. The third question analyzes the tax implications of interest received from a loan between parents and their son, also referencing the ITAA 1997. Finally, question four explores CGT events related to land and building sales, providing calculations and scenarios related to asset disposal, including the impact of selling property to a daughter and the implications if the property owner was a company. The assignment demonstrates an understanding of the ITAA 1997 and its application to various financial situations.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.