Taxation Law: GST and Input Tax Credit, CGT and Capital Proceeds

VerifiedAdded on 2022/10/15

|12

|2624

|140

AI Summary

This article discusses GST and input tax credit, CGT and capital proceeds in taxation law. It also covers the sale of block of land, shares, stamps, and grand piano. The article provides a comprehensive analysis of the laws and issues involved in these topics.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

The issue that is taken in this case involves the discussion about the GST and the

input tax credit that can be availed by the taxpayer in regard to transactions occurred during

the business course.

Laws:

If the taxpayer has obtained the vacant land either for using it in private purpose or

using the land for investment purpose, land is on a general note considered as the capital asset

that is subject to CGT when it is sold by a taxpayer. But if the taxpayer purchase the land for

using it in the business purpose or for profit yielding activity, then any type of sales proceeds

are held as ordinary earnings and the taxpayer would be required to register for GST (Long,

Campbell and Kelshaw 2016). The tax treatment of the land and the revenue that is earned

from selling the land is commonly reliant on the fact that whether it can be treated as the

capital asset or the subject of business or the commercial deal.

The goods and service tax is also mentioned as the consumption duty. The GST is

applied on the supply of goods as well as services that are made in Australia and the goods

that are imported in Australia. Commonly GST should only be paid on the value added

assessable supply (Marateo 2017). Commonly GST is payable by every company that are

providing a supply at every step along with the supply chain. GST is regarded as the

transaction based tax and the elements of the transactions are;

a. Supplier: The suppliers delivers the business matter of supply.

b. Receiver: This involves the person that receives the supply and pay the price for

consideration.

Answer to question 1:

Issues:

The issue that is taken in this case involves the discussion about the GST and the

input tax credit that can be availed by the taxpayer in regard to transactions occurred during

the business course.

Laws:

If the taxpayer has obtained the vacant land either for using it in private purpose or

using the land for investment purpose, land is on a general note considered as the capital asset

that is subject to CGT when it is sold by a taxpayer. But if the taxpayer purchase the land for

using it in the business purpose or for profit yielding activity, then any type of sales proceeds

are held as ordinary earnings and the taxpayer would be required to register for GST (Long,

Campbell and Kelshaw 2016). The tax treatment of the land and the revenue that is earned

from selling the land is commonly reliant on the fact that whether it can be treated as the

capital asset or the subject of business or the commercial deal.

The goods and service tax is also mentioned as the consumption duty. The GST is

applied on the supply of goods as well as services that are made in Australia and the goods

that are imported in Australia. Commonly GST should only be paid on the value added

assessable supply (Marateo 2017). Commonly GST is payable by every company that are

providing a supply at every step along with the supply chain. GST is regarded as the

transaction based tax and the elements of the transactions are;

a. Supplier: The suppliers delivers the business matter of supply.

b. Receiver: This involves the person that receives the supply and pay the price for

consideration.

3TAXATION LAW

Under “sec 9-40 of the GST Act”, the liability paying GST happens when the taxable

supply or import is made. As noted in “sec 9.5 GST Act, GST” is commonly charged on the

assessable supply (Tully 2016). A taxpayer makes taxable supply if a supply is made for price

in carrying the business activity that is related with Australia by a company that is registered

under GST. While creditable acquisition given in “sec 11.5 GST Act” denotes that the

acquisition of items are made with the creditable purpose. This represents a situation when a

company purchases a thing at the time of carrying on the entity’s activities but does not

involve the extent that the acquisition is used for making an input tax supplies or the

acquisition is private or domestic in nature.

Commonly when a registered company purchases something, then they are considered

entitled to credit for GST that is paid on the purchase until and unless the acquisition made is

for creditable purpose and the taxpayer holds a valid tax invoice. The decision given in “AP

Group Ltd v CT (2013)” denoted that there should be a consideration that must have

connection with supply and the supply should also have the consideration (Lam and Whitney

2016).

On the other hand there is also a reverse charge mechanisms that requires the recipient

to pay the tax liability on GST as an alternative to supplier for the receipt of goods or

services. The rules that is laid down in ATO states that things beside the goods and actual

property might attract GST when the Australian business purchases them. The activities may

be done out of Australia or may be made with the help of business that are carried on by the

seller out of Australia (Lavermicocca 2017). The applicability of reverse charge mainly

involves the conditions where the things purchased is for the business use either completely

or partially that is performed in Australia and the sale made to the taxpayer is for payment.

The reverse charge is applied when the sale has relation with Australia and the things

purchased by the taxpayer is the Australian based business recipient.

Under “sec 9-40 of the GST Act”, the liability paying GST happens when the taxable

supply or import is made. As noted in “sec 9.5 GST Act, GST” is commonly charged on the

assessable supply (Tully 2016). A taxpayer makes taxable supply if a supply is made for price

in carrying the business activity that is related with Australia by a company that is registered

under GST. While creditable acquisition given in “sec 11.5 GST Act” denotes that the

acquisition of items are made with the creditable purpose. This represents a situation when a

company purchases a thing at the time of carrying on the entity’s activities but does not

involve the extent that the acquisition is used for making an input tax supplies or the

acquisition is private or domestic in nature.

Commonly when a registered company purchases something, then they are considered

entitled to credit for GST that is paid on the purchase until and unless the acquisition made is

for creditable purpose and the taxpayer holds a valid tax invoice. The decision given in “AP

Group Ltd v CT (2013)” denoted that there should be a consideration that must have

connection with supply and the supply should also have the consideration (Lam and Whitney

2016).

On the other hand there is also a reverse charge mechanisms that requires the recipient

to pay the tax liability on GST as an alternative to supplier for the receipt of goods or

services. The rules that is laid down in ATO states that things beside the goods and actual

property might attract GST when the Australian business purchases them. The activities may

be done out of Australia or may be made with the help of business that are carried on by the

seller out of Australia (Lavermicocca 2017). The applicability of reverse charge mainly

involves the conditions where the things purchased is for the business use either completely

or partially that is performed in Australia and the sale made to the taxpayer is for payment.

The reverse charge is applied when the sale has relation with Australia and the things

purchased by the taxpayer is the Australian based business recipient.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

Application:

The case City Sky Co reveals that the company has been registered for GST and it is

conducting the business of property development. In the recent transaction reported by City

Sky Co it has acquired a vacant land in Brisbane on which it intends to construct apartment

for trading it in the marketplace. As obvious the land that is bought by City Sky Co is termed

as the CGT asset. The land is not a movable property in case of City Sky Co and it also does

not constitute any type of services. The liability of GST does not originates in this situation.

As a result, there cannot be any claim for input tax credit.

While in the later part, City Sky Co paid Maurice Blackburn for availing its legal

service. The legal services that were provided by Maurice Blackburn to City Sky Co was for

developmental purpose and incurred $33,000 for the same. The services taken from the

advocate by City Sky Co qualifies under the mechanism of reverse charge. This is because

the services were completely for the business purpose and services was in exchange of

payment. The legal services was also connected to Australia and were mainly occurred in

continuance of the City Sky Co enterprise activity. Denoting “sec 11.5 GST Act” the legal

services sought by City Sky Co is a creditable acquisition (Eccleston and Smith 2015).

Noting the judgement of “AP Group Ltd v CT (2013)” City Sky Co is entitled to input tax

credit for the GST paid under the reverse charge mechanism.

Conclusion:

The purchase of vacant land cannot be considered as the GST transaction and as a

result no input tax credit is allowable however the legal services that is taken by City Sky Co

from Maurice Blackburn being GST registered will be able to claim the input tax credit for

the services taken.

Application:

The case City Sky Co reveals that the company has been registered for GST and it is

conducting the business of property development. In the recent transaction reported by City

Sky Co it has acquired a vacant land in Brisbane on which it intends to construct apartment

for trading it in the marketplace. As obvious the land that is bought by City Sky Co is termed

as the CGT asset. The land is not a movable property in case of City Sky Co and it also does

not constitute any type of services. The liability of GST does not originates in this situation.

As a result, there cannot be any claim for input tax credit.

While in the later part, City Sky Co paid Maurice Blackburn for availing its legal

service. The legal services that were provided by Maurice Blackburn to City Sky Co was for

developmental purpose and incurred $33,000 for the same. The services taken from the

advocate by City Sky Co qualifies under the mechanism of reverse charge. This is because

the services were completely for the business purpose and services was in exchange of

payment. The legal services was also connected to Australia and were mainly occurred in

continuance of the City Sky Co enterprise activity. Denoting “sec 11.5 GST Act” the legal

services sought by City Sky Co is a creditable acquisition (Eccleston and Smith 2015).

Noting the judgement of “AP Group Ltd v CT (2013)” City Sky Co is entitled to input tax

credit for the GST paid under the reverse charge mechanism.

Conclusion:

The purchase of vacant land cannot be considered as the GST transaction and as a

result no input tax credit is allowable however the legal services that is taken by City Sky Co

from Maurice Blackburn being GST registered will be able to claim the input tax credit for

the services taken.

5TAXATION LAW

Answer to question 2:

Sale of block of land:

Most importantly the general rule that is clarified in “sec 116-20” provides that

capital proceeds involves consideration received in either cash or in kind in terms of market

value that is received by taxpayer in respect of CGT event (Blakelock & King 2017). The

computation of CGT normally involves adding up the elements of cost base or the reduced

cost base. There are notably five elements that are added all together.

I. Element 1 involves the purchase price, market value of the property and

construction cost under “sec 110-25 (2), ITA Act 97”.

II. Element 2 denotes the incidental expenses that have happened in regard to the

acquisition or disposing of the asset under “sec 110-25 (3), ITA Act 97”.

III. Element 3 is the non-capital ownership cost. Under “sec 110-25 (4), ITA Act

97” this characterizes the cost which not allowed to taxpayer as claim for tax

deduction (Khoury 2014). Examples are loan interest, rates, repairs etc.

IV. Element 4 of the cost base is the capital expenses when occurred by the

taxpayer in improving the value of asset. Under “sec 110-25 (5), ITA Act 97”

the examples of the cost are improvement, moving or installing expenditure

occurred on the asset.

V. Element 5 cost base involves the expenses that is occurred by the taxpayers in

increasing the value of the asset under “sec 110-25 (6), ITA Act 97”.

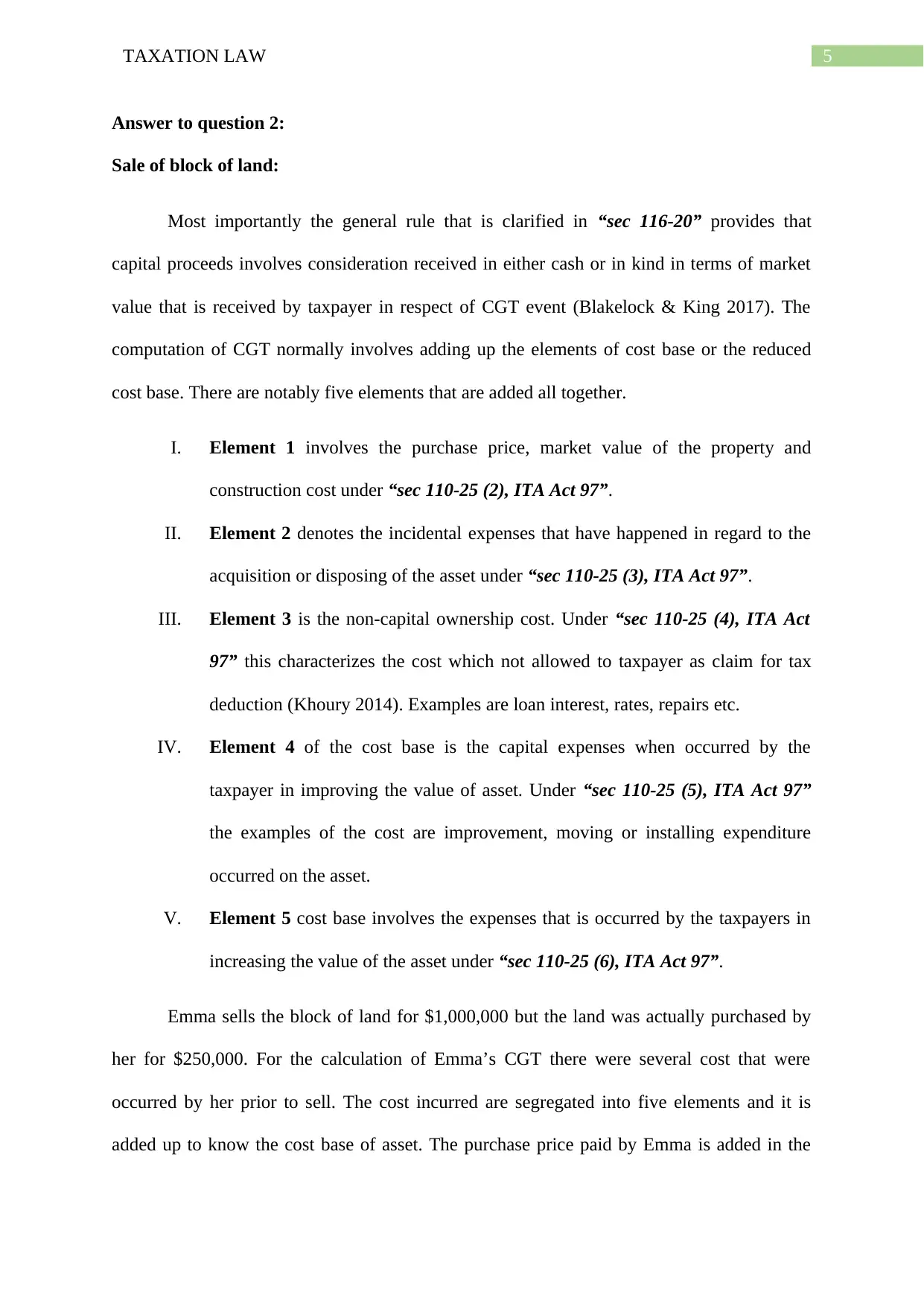

Emma sells the block of land for $1,000,000 but the land was actually purchased by

her for $250,000. For the calculation of Emma’s CGT there were several cost that were

occurred by her prior to sell. The cost incurred are segregated into five elements and it is

added up to know the cost base of asset. The purchase price paid by Emma is added in the

Answer to question 2:

Sale of block of land:

Most importantly the general rule that is clarified in “sec 116-20” provides that

capital proceeds involves consideration received in either cash or in kind in terms of market

value that is received by taxpayer in respect of CGT event (Blakelock & King 2017). The

computation of CGT normally involves adding up the elements of cost base or the reduced

cost base. There are notably five elements that are added all together.

I. Element 1 involves the purchase price, market value of the property and

construction cost under “sec 110-25 (2), ITA Act 97”.

II. Element 2 denotes the incidental expenses that have happened in regard to the

acquisition or disposing of the asset under “sec 110-25 (3), ITA Act 97”.

III. Element 3 is the non-capital ownership cost. Under “sec 110-25 (4), ITA Act

97” this characterizes the cost which not allowed to taxpayer as claim for tax

deduction (Khoury 2014). Examples are loan interest, rates, repairs etc.

IV. Element 4 of the cost base is the capital expenses when occurred by the

taxpayer in improving the value of asset. Under “sec 110-25 (5), ITA Act 97”

the examples of the cost are improvement, moving or installing expenditure

occurred on the asset.

V. Element 5 cost base involves the expenses that is occurred by the taxpayers in

increasing the value of the asset under “sec 110-25 (6), ITA Act 97”.

Emma sells the block of land for $1,000,000 but the land was actually purchased by

her for $250,000. For the calculation of Emma’s CGT there were several cost that were

occurred by her prior to sell. The cost incurred are segregated into five elements and it is

added up to know the cost base of asset. The purchase price paid by Emma is added in the

6TAXATION LAW

Element 1 cost base of asset under “sec 110-25 (2)” as the market value paid to acquire the

asset (Guez 2018). While the stamp duty and legal fees were added up to cost base element 2

as incidental cost of purchase under “sec 110-25 (3)”.

She also took up loan to fund for the land’s purchase. The loan interest amounting to

$32,000 is a non-capital ownership cost under “sec 110-25(4)”. Till the time Emma held the

property she paid council rates, water rates and insurance (Pagura 2017). These cost are

added in the Element 3 cost base of property under “sec 110-25(4)”.

When the property was under her ownership there was also a legal expenses reported

by Emma for occurring dispute with the neighbours. The legal expenses is a capital expense

that is was incurred for preserving her rights on the asset. Under “sec 110-25 (6), ITA Act

97” it is added up as in Element 5 cost base of block of land. Emma lastly incurred outgoings

on cutting down the pine trees that were on the land (Sadiq 2017). The cutting down of pine

trees is a capital improvement cost occurred for improving the land. So under “sec 110-25

(6), ITA Act 97” it is added up in Element 4 cost base of land.

The overall capital proceeds obtained under “sec 116-20” after adding all the five

elements for CGT purpose is computed below;

Element 1 cost base of asset under “sec 110-25 (2)” as the market value paid to acquire the

asset (Guez 2018). While the stamp duty and legal fees were added up to cost base element 2

as incidental cost of purchase under “sec 110-25 (3)”.

She also took up loan to fund for the land’s purchase. The loan interest amounting to

$32,000 is a non-capital ownership cost under “sec 110-25(4)”. Till the time Emma held the

property she paid council rates, water rates and insurance (Pagura 2017). These cost are

added in the Element 3 cost base of property under “sec 110-25(4)”.

When the property was under her ownership there was also a legal expenses reported

by Emma for occurring dispute with the neighbours. The legal expenses is a capital expense

that is was incurred for preserving her rights on the asset. Under “sec 110-25 (6), ITA Act

97” it is added up as in Element 5 cost base of block of land. Emma lastly incurred outgoings

on cutting down the pine trees that were on the land (Sadiq 2017). The cutting down of pine

trees is a capital improvement cost occurred for improving the land. So under “sec 110-25

(6), ITA Act 97” it is added up in Element 4 cost base of land.

The overall capital proceeds obtained under “sec 116-20” after adding all the five

elements for CGT purpose is computed below;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

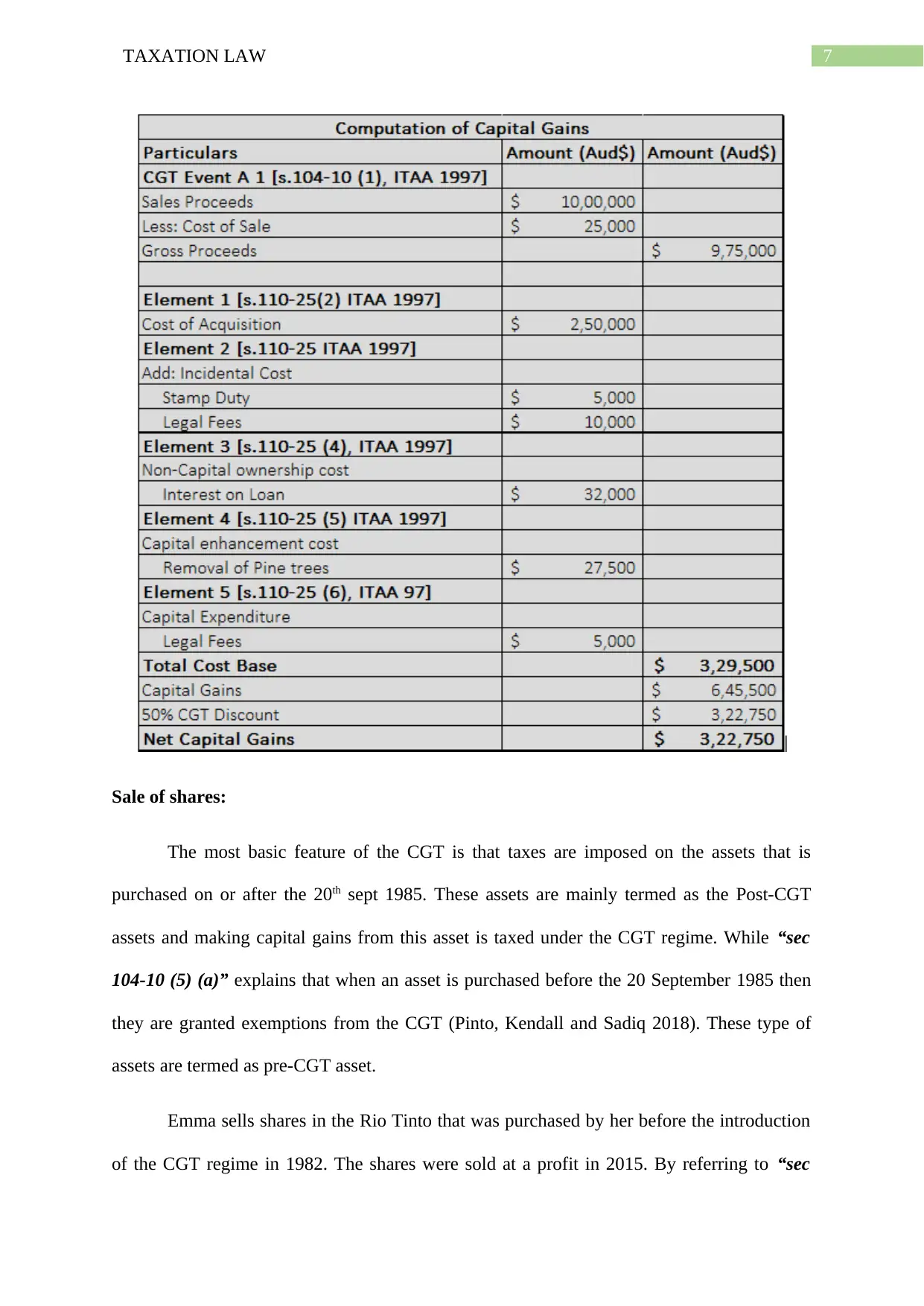

Sale of shares:

The most basic feature of the CGT is that taxes are imposed on the assets that is

purchased on or after the 20th sept 1985. These assets are mainly termed as the Post-CGT

assets and making capital gains from this asset is taxed under the CGT regime. While “sec

104-10 (5) (a)” explains that when an asset is purchased before the 20 September 1985 then

they are granted exemptions from the CGT (Pinto, Kendall and Sadiq 2018). These type of

assets are termed as pre-CGT asset.

Emma sells shares in the Rio Tinto that was purchased by her before the introduction

of the CGT regime in 1982. The shares were sold at a profit in 2015. By referring to “sec

Sale of shares:

The most basic feature of the CGT is that taxes are imposed on the assets that is

purchased on or after the 20th sept 1985. These assets are mainly termed as the Post-CGT

assets and making capital gains from this asset is taxed under the CGT regime. While “sec

104-10 (5) (a)” explains that when an asset is purchased before the 20 September 1985 then

they are granted exemptions from the CGT (Pinto, Kendall and Sadiq 2018). These type of

assets are termed as pre-CGT asset.

Emma sells shares in the Rio Tinto that was purchased by her before the introduction

of the CGT regime in 1982. The shares were sold at a profit in 2015. By referring to “sec

8TAXATION LAW

104-10 (5) (a)” the shares are acquired before 20 sept. 1985 (Pert, Chen and Carvosso 2017).

Therefore, the shares are pre-CGT asset and the capital gains is exempted for Emma.

Sale of stamps:

A collectables involves any one of the items that is listed under “sec 108-10 (2)”.

These are

Art works (sculptures, paintings)

Rare manuscripts or books

Rare stamps, medals or coins

Jewellery

This type of items are used by the taxpayers for their private purpose and enjoyment.

While “sec.108-10 (4)”, directs the taxpayers to quarantine the capital loss from collectables

(Killaly 2017). Emma derived a capital proceeds of $50,000 from sale of stamps. The stamps

are treated as an item of collectable listed under “sec 108-10 (2)”. The proceeds yielded

capital loss as the stamps were purchased for $60,000. The capital loss must be carried

forward to subsequent year because no other gains from collectables were reported in present

year.

104-10 (5) (a)” the shares are acquired before 20 sept. 1985 (Pert, Chen and Carvosso 2017).

Therefore, the shares are pre-CGT asset and the capital gains is exempted for Emma.

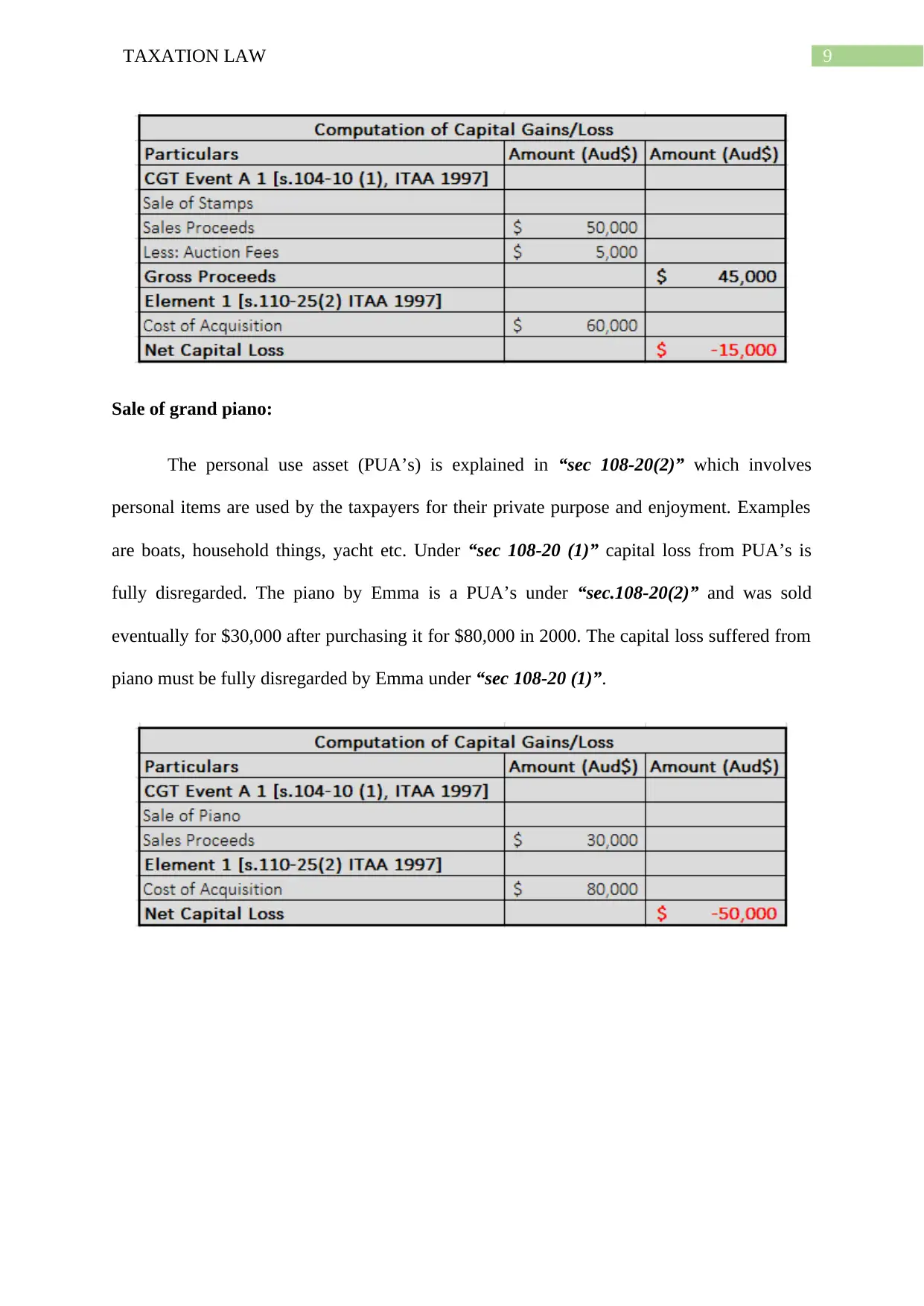

Sale of stamps:

A collectables involves any one of the items that is listed under “sec 108-10 (2)”.

These are

Art works (sculptures, paintings)

Rare manuscripts or books

Rare stamps, medals or coins

Jewellery

This type of items are used by the taxpayers for their private purpose and enjoyment.

While “sec.108-10 (4)”, directs the taxpayers to quarantine the capital loss from collectables

(Killaly 2017). Emma derived a capital proceeds of $50,000 from sale of stamps. The stamps

are treated as an item of collectable listed under “sec 108-10 (2)”. The proceeds yielded

capital loss as the stamps were purchased for $60,000. The capital loss must be carried

forward to subsequent year because no other gains from collectables were reported in present

year.

9TAXATION LAW

Sale of grand piano:

The personal use asset (PUA’s) is explained in “sec 108-20(2)” which involves

personal items are used by the taxpayers for their private purpose and enjoyment. Examples

are boats, household things, yacht etc. Under “sec 108-20 (1)” capital loss from PUA’s is

fully disregarded. The piano by Emma is a PUA’s under “sec.108-20(2)” and was sold

eventually for $30,000 after purchasing it for $80,000 in 2000. The capital loss suffered from

piano must be fully disregarded by Emma under “sec 108-20 (1)”.

Sale of grand piano:

The personal use asset (PUA’s) is explained in “sec 108-20(2)” which involves

personal items are used by the taxpayers for their private purpose and enjoyment. Examples

are boats, household things, yacht etc. Under “sec 108-20 (1)” capital loss from PUA’s is

fully disregarded. The piano by Emma is a PUA’s under “sec.108-20(2)” and was sold

eventually for $30,000 after purchasing it for $80,000 in 2000. The capital loss suffered from

piano must be fully disregarded by Emma under “sec 108-20 (1)”.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

References:

Blakelock, S & King, P, 2017. Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), pp.18–21.

Eccleston, R. and Smith, H., 2015. Fixing Funding in the Australian Federation: Issues and

Options for State Tax Reform. , 74(4), p.435.

Guez, S. et al., 2018. FINANCE & TAXATION. Stetson Law Review, 47(3), pp.561–582.

Khoury, D, 2014. Widening the availability of deductions under Australian taxation law. Tax

Specialist, 14(4), pp.207–211.

Killaly, J, 2017. Law design and compliance management for a viable company tax base :

Chapter 3. JOURNAL OF AUSTRALIAN TAXATION, 19(3), pp.45–50.

Lam, D. and Whitney, A., 2016. Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Lavermicocca, C, 2017. Tax risk management and the application of ethics by large

Australian companies. AUSTRALIAN TAX FORUM, 32(4), pp.741–756.

Long, B, Campbell, J and Kelshaw, C, 2016. The justice lens on taxation policy in Australia.

St Mark's Review, (235), pp.[94]-106.

Marateo, D., 2017. An Effective Priority for the Commissioner of Taxation in Liquidation:

Bell Group NV (in Liq.) v. Western Australia. Adelaide Law Review, 38(1), pp.223–231.

Pagura, I, 2017. Law report: Tax update. Journal of the Australian Traditional-Medicine

Society, 23(3), pp.160–161.

References:

Blakelock, S & King, P, 2017. Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), pp.18–21.

Eccleston, R. and Smith, H., 2015. Fixing Funding in the Australian Federation: Issues and

Options for State Tax Reform. , 74(4), p.435.

Guez, S. et al., 2018. FINANCE & TAXATION. Stetson Law Review, 47(3), pp.561–582.

Khoury, D, 2014. Widening the availability of deductions under Australian taxation law. Tax

Specialist, 14(4), pp.207–211.

Killaly, J, 2017. Law design and compliance management for a viable company tax base :

Chapter 3. JOURNAL OF AUSTRALIAN TAXATION, 19(3), pp.45–50.

Lam, D. and Whitney, A., 2016. Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Lavermicocca, C, 2017. Tax risk management and the application of ethics by large

Australian companies. AUSTRALIAN TAX FORUM, 32(4), pp.741–756.

Long, B, Campbell, J and Kelshaw, C, 2016. The justice lens on taxation policy in Australia.

St Mark's Review, (235), pp.[94]-106.

Marateo, D., 2017. An Effective Priority for the Commissioner of Taxation in Liquidation:

Bell Group NV (in Liq.) v. Western Australia. Adelaide Law Review, 38(1), pp.223–231.

Pagura, I, 2017. Law report: Tax update. Journal of the Australian Traditional-Medicine

Society, 23(3), pp.160–161.

11TAXATION LAW

Pert, A, Chen, H and Carvosso, R, 2017. 'Bywater Investments Limited v Commissioner of

Taxation'; 'Hua Wang Bank Berhad v Commissioner of Taxation' (2016) 91 ALJR 59.

Australian Year Book of International Law, 35, pp.250–252.

Pinto, D., Kendall, K. and Sadiq, K., 2018. Fundamental tax legislation 2018 Twenty-sixth.,

Sadiq, K. and C.C.& H.R.E.A.L. et al., 2017. Principles of taxation law 2017 10th ed., Place

of publication not identified]: THOMSON LAWBOOK CO.

Tully, S, 2016. Taxation: Interpreting bilateral tax treaties. LSJ: Law Society of NSW

Journal, (28), pp.76–77.

Pert, A, Chen, H and Carvosso, R, 2017. 'Bywater Investments Limited v Commissioner of

Taxation'; 'Hua Wang Bank Berhad v Commissioner of Taxation' (2016) 91 ALJR 59.

Australian Year Book of International Law, 35, pp.250–252.

Pinto, D., Kendall, K. and Sadiq, K., 2018. Fundamental tax legislation 2018 Twenty-sixth.,

Sadiq, K. and C.C.& H.R.E.A.L. et al., 2017. Principles of taxation law 2017 10th ed., Place

of publication not identified]: THOMSON LAWBOOK CO.

Tully, S, 2016. Taxation: Interpreting bilateral tax treaties. LSJ: Law Society of NSW

Journal, (28), pp.76–77.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.