Holmes Institute HA3042 Taxation Law Assignment: CGT, Depreciation

VerifiedAdded on 2022/10/14

|12

|2903

|485

Homework Assignment

AI Summary

This taxation law assignment explores the application of Capital Gains Tax (CGT) and depreciation in various scenarios. The assignment analyzes a case study involving Jasmine, an Australian resident, and her sale of multiple assets, including her main residence (pre-CGT asset), a car (personal use asset), a cleaning business, and furniture and paintings (collectables). The analysis covers the applicability of CGT, small business concessions, and exemptions based on asset types and purchase dates. The second part of the assignment addresses the deductibility of depreciation for depreciating assets used in generating taxable income, focusing on the case of John, a vehicle parts manufacturer who imports a CNC machine. The analysis considers relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997), including Division 40, and relevant case law to determine the appropriate tax treatment, cost base, and depreciation deductions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Requirement A: Sale of Main House

The basic feature of the CGT is that it is applied on the assets which is purchased on

or afterward 20th Sept 1985. Any assets or events that are taking after this date are taken into

the tax regime of capital gains (Evans 2019). While assets that are before this date are termed

as the pre-CGT asset and they are usually exempted from the capital gains tax regime

irrespective of gains or losses made. Assets bought on or after this date is considered as the

post-CGT asset.

The circumstance of Jasmine opens with the situation that she is an Australian dweller

and she is now selling all her assets that she had owned as she is permanently moving to UK.

Jasmine in her process of selling all the assets is found to be selling her home that she has

used as her main location of dwelling. The main dwelling was purchased in 1982 by Jasmine

and she paid a sum of $40,000 to acquire it. As in the current tax year she sells it for

$650,000. As understood from the transaction that Jasmine has yielded capital gains from

selling her main residence. But it must be noted that her main dwelling was purchased in

1982 and the asset will be termed as pre-CGT asset because the asset was bought by her

earlier to the application of CGT regime (Plummer 2016). The capital gains made thereon is

simply excluded or exempted from tax.

Requirement B: Sale of Car:

A capital gain happens when the proceeds on sale exceeds the cost of acquisition.

While a capital loss happens if the cost of purchase goes beyond the sale price. A CGT event

under “sec 104-10 (1), ITA Act 97” is only considered in the course of sale of CGT asset.

“Sec 108-5 (1)”, CGT asset usually involves any form of property excluding the land and

building (Coates 2015). Explained under “sec 108.20 (2)” a personal use asset (PUA’s)

Answer to question 1:

Requirement A: Sale of Main House

The basic feature of the CGT is that it is applied on the assets which is purchased on

or afterward 20th Sept 1985. Any assets or events that are taking after this date are taken into

the tax regime of capital gains (Evans 2019). While assets that are before this date are termed

as the pre-CGT asset and they are usually exempted from the capital gains tax regime

irrespective of gains or losses made. Assets bought on or after this date is considered as the

post-CGT asset.

The circumstance of Jasmine opens with the situation that she is an Australian dweller

and she is now selling all her assets that she had owned as she is permanently moving to UK.

Jasmine in her process of selling all the assets is found to be selling her home that she has

used as her main location of dwelling. The main dwelling was purchased in 1982 by Jasmine

and she paid a sum of $40,000 to acquire it. As in the current tax year she sells it for

$650,000. As understood from the transaction that Jasmine has yielded capital gains from

selling her main residence. But it must be noted that her main dwelling was purchased in

1982 and the asset will be termed as pre-CGT asset because the asset was bought by her

earlier to the application of CGT regime (Plummer 2016). The capital gains made thereon is

simply excluded or exempted from tax.

Requirement B: Sale of Car:

A capital gain happens when the proceeds on sale exceeds the cost of acquisition.

While a capital loss happens if the cost of purchase goes beyond the sale price. A CGT event

under “sec 104-10 (1), ITA Act 97” is only considered in the course of sale of CGT asset.

“Sec 108-5 (1)”, CGT asset usually involves any form of property excluding the land and

building (Coates 2015). Explained under “sec 108.20 (2)” a personal use asset (PUA’s)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

denotes assets such as television, furniture, motor vehicle etc. kept or used by taxpayer for

private purpose and enjoyment. When a capital loss happens from PUA’s it should be

disregarded under “sec.108-20(1)” by taxpayers.

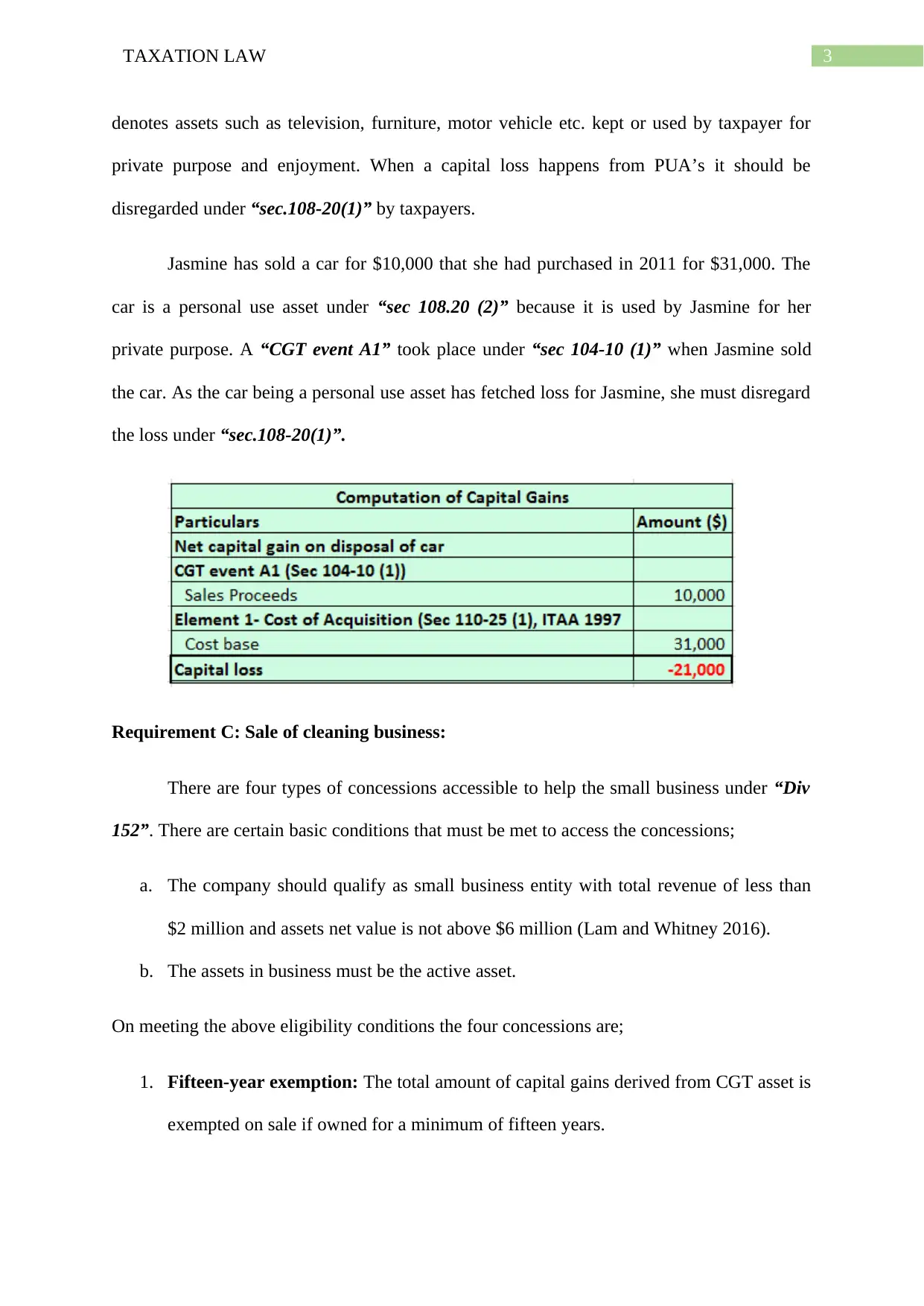

Jasmine has sold a car for $10,000 that she had purchased in 2011 for $31,000. The

car is a personal use asset under “sec 108.20 (2)” because it is used by Jasmine for her

private purpose. A “CGT event A1” took place under “sec 104-10 (1)” when Jasmine sold

the car. As the car being a personal use asset has fetched loss for Jasmine, she must disregard

the loss under “sec.108-20(1)”.

Requirement C: Sale of cleaning business:

There are four types of concessions accessible to help the small business under “Div

152”. There are certain basic conditions that must be met to access the concessions;

a. The company should qualify as small business entity with total revenue of less than

$2 million and assets net value is not above $6 million (Lam and Whitney 2016).

b. The assets in business must be the active asset.

On meeting the above eligibility conditions the four concessions are;

1. Fifteen-year exemption: The total amount of capital gains derived from CGT asset is

exempted on sale if owned for a minimum of fifteen years.

denotes assets such as television, furniture, motor vehicle etc. kept or used by taxpayer for

private purpose and enjoyment. When a capital loss happens from PUA’s it should be

disregarded under “sec.108-20(1)” by taxpayers.

Jasmine has sold a car for $10,000 that she had purchased in 2011 for $31,000. The

car is a personal use asset under “sec 108.20 (2)” because it is used by Jasmine for her

private purpose. A “CGT event A1” took place under “sec 104-10 (1)” when Jasmine sold

the car. As the car being a personal use asset has fetched loss for Jasmine, she must disregard

the loss under “sec.108-20(1)”.

Requirement C: Sale of cleaning business:

There are four types of concessions accessible to help the small business under “Div

152”. There are certain basic conditions that must be met to access the concessions;

a. The company should qualify as small business entity with total revenue of less than

$2 million and assets net value is not above $6 million (Lam and Whitney 2016).

b. The assets in business must be the active asset.

On meeting the above eligibility conditions the four concessions are;

1. Fifteen-year exemption: The total amount of capital gains derived from CGT asset is

exempted on sale if owned for a minimum of fifteen years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

2. 50% reduction concession: A reduction of 50% is available from CGT even after

applying the general 50% discount.

3. Retirement concession: Ignore the capital gains earned from the CGT asset related

with small business up to $500,000 as long as the proceeds are used in retirement

purpose.

4. Roll-over relief: Defer the capital gains when the taxpayer purchase another

replacement asset.

The case of Jasmine further contributes to the knowledge that she is retiring from her

small cleaning business. She sells her business for $125,000 with all her equipment sold for

$65,000 while her assets sold for $60,000. Jasmine can claim the available concession under

“Div 152” as her small cleaning business net value of assets does not surpasses $6 million

and all the CGT asset is an active asset (Villios, 2013). Assuming that Jasmine has held all

her assets for fifteen years so she can avail the fifteen year exemption following the sale of

CGT asset. Additionally, Jasmine is also more than 55 years old, so a concession from CGT

should be availed.

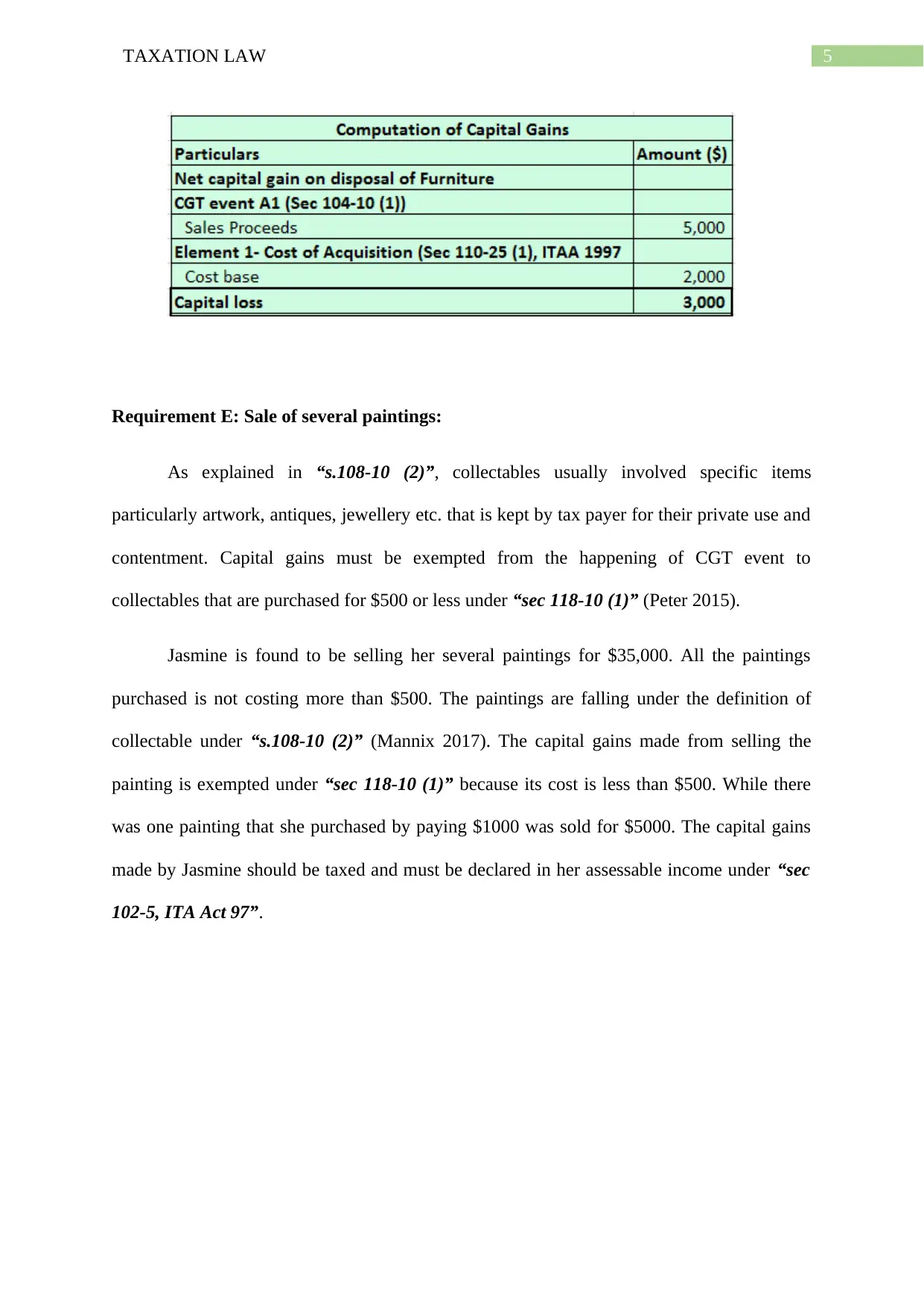

Requirement D: Sale of Furniture:

Jasmine is also found to be selling her furniture for $5,000 while its purchase price

stands $2,000. The CGT event occurred under “s.104-10(1)” when Jasmine sold the furniture

(Minas et al. 2018). While Jasmine must denote that the cost of her furniture is below

$10,000 and for this purpose the capital gains made from selling it is exempted under “sec

118.10 (3), ITA Act 97”.

2. 50% reduction concession: A reduction of 50% is available from CGT even after

applying the general 50% discount.

3. Retirement concession: Ignore the capital gains earned from the CGT asset related

with small business up to $500,000 as long as the proceeds are used in retirement

purpose.

4. Roll-over relief: Defer the capital gains when the taxpayer purchase another

replacement asset.

The case of Jasmine further contributes to the knowledge that she is retiring from her

small cleaning business. She sells her business for $125,000 with all her equipment sold for

$65,000 while her assets sold for $60,000. Jasmine can claim the available concession under

“Div 152” as her small cleaning business net value of assets does not surpasses $6 million

and all the CGT asset is an active asset (Villios, 2013). Assuming that Jasmine has held all

her assets for fifteen years so she can avail the fifteen year exemption following the sale of

CGT asset. Additionally, Jasmine is also more than 55 years old, so a concession from CGT

should be availed.

Requirement D: Sale of Furniture:

Jasmine is also found to be selling her furniture for $5,000 while its purchase price

stands $2,000. The CGT event occurred under “s.104-10(1)” when Jasmine sold the furniture

(Minas et al. 2018). While Jasmine must denote that the cost of her furniture is below

$10,000 and for this purpose the capital gains made from selling it is exempted under “sec

118.10 (3), ITA Act 97”.

5TAXATION LAW

Requirement E: Sale of several paintings:

As explained in “s.108-10 (2)”, collectables usually involved specific items

particularly artwork, antiques, jewellery etc. that is kept by tax payer for their private use and

contentment. Capital gains must be exempted from the happening of CGT event to

collectables that are purchased for $500 or less under “sec 118-10 (1)” (Peter 2015).

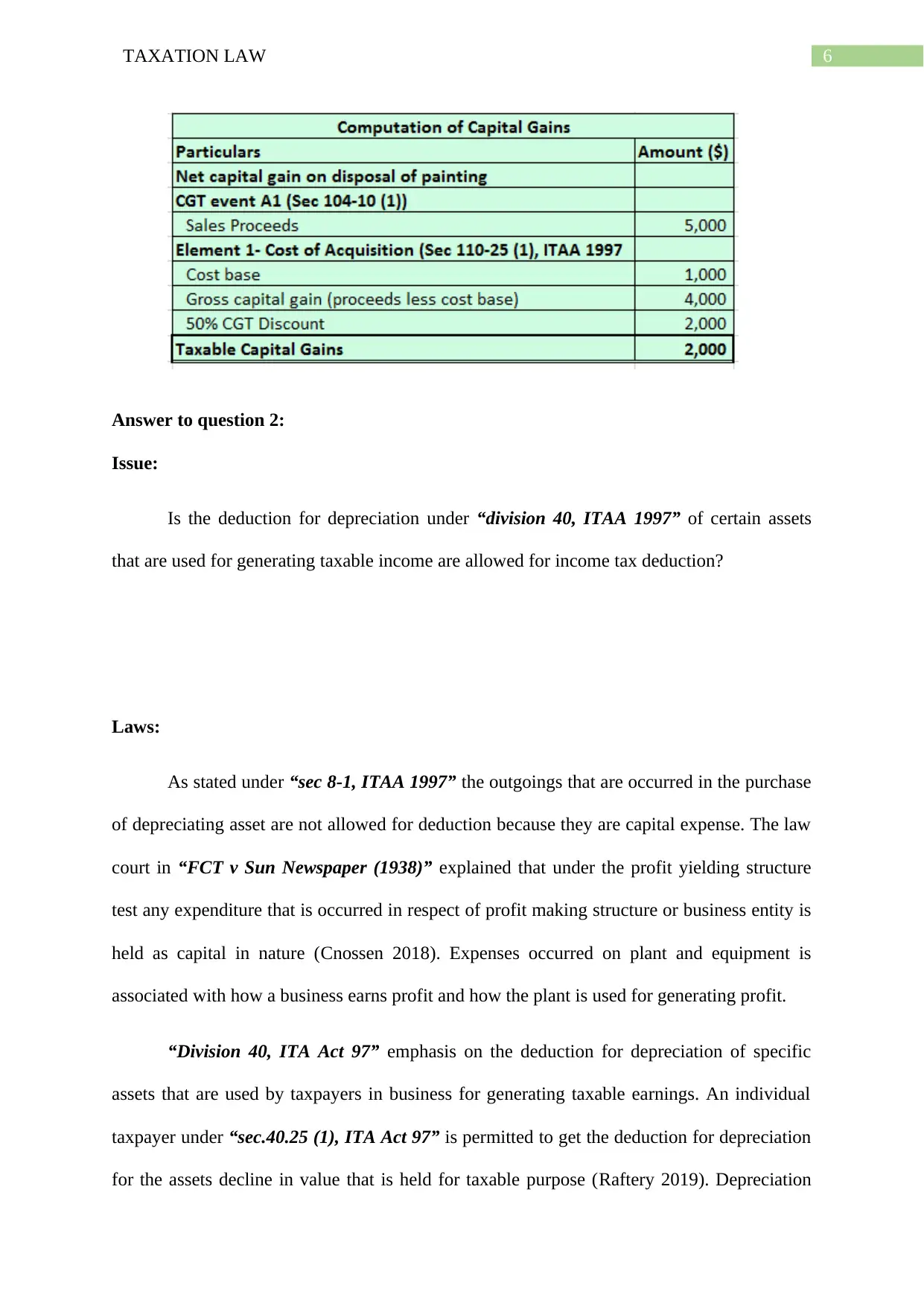

Jasmine is found to be selling her several paintings for $35,000. All the paintings

purchased is not costing more than $500. The paintings are falling under the definition of

collectable under “s.108-10 (2)” (Mannix 2017). The capital gains made from selling the

painting is exempted under “sec 118-10 (1)” because its cost is less than $500. While there

was one painting that she purchased by paying $1000 was sold for $5000. The capital gains

made by Jasmine should be taxed and must be declared in her assessable income under “sec

102-5, ITA Act 97”.

Requirement E: Sale of several paintings:

As explained in “s.108-10 (2)”, collectables usually involved specific items

particularly artwork, antiques, jewellery etc. that is kept by tax payer for their private use and

contentment. Capital gains must be exempted from the happening of CGT event to

collectables that are purchased for $500 or less under “sec 118-10 (1)” (Peter 2015).

Jasmine is found to be selling her several paintings for $35,000. All the paintings

purchased is not costing more than $500. The paintings are falling under the definition of

collectable under “s.108-10 (2)” (Mannix 2017). The capital gains made from selling the

painting is exempted under “sec 118-10 (1)” because its cost is less than $500. While there

was one painting that she purchased by paying $1000 was sold for $5000. The capital gains

made by Jasmine should be taxed and must be declared in her assessable income under “sec

102-5, ITA Act 97”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Issue:

Is the deduction for depreciation under “division 40, ITAA 1997” of certain assets

that are used for generating taxable income are allowed for income tax deduction?

Laws:

As stated under “sec 8-1, ITAA 1997” the outgoings that are occurred in the purchase

of depreciating asset are not allowed for deduction because they are capital expense. The law

court in “FCT v Sun Newspaper (1938)” explained that under the profit yielding structure

test any expenditure that is occurred in respect of profit making structure or business entity is

held as capital in nature (Cnossen 2018). Expenses occurred on plant and equipment is

associated with how a business earns profit and how the plant is used for generating profit.

“Division 40, ITA Act 97” emphasis on the deduction for depreciation of specific

assets that are used by taxpayers in business for generating taxable earnings. An individual

taxpayer under “sec.40.25 (1), ITA Act 97” is permitted to get the deduction for depreciation

for the assets decline in value that is held for taxable purpose (Raftery 2019). Depreciation

Answer to question 2:

Issue:

Is the deduction for depreciation under “division 40, ITAA 1997” of certain assets

that are used for generating taxable income are allowed for income tax deduction?

Laws:

As stated under “sec 8-1, ITAA 1997” the outgoings that are occurred in the purchase

of depreciating asset are not allowed for deduction because they are capital expense. The law

court in “FCT v Sun Newspaper (1938)” explained that under the profit yielding structure

test any expenditure that is occurred in respect of profit making structure or business entity is

held as capital in nature (Cnossen 2018). Expenses occurred on plant and equipment is

associated with how a business earns profit and how the plant is used for generating profit.

“Division 40, ITA Act 97” emphasis on the deduction for depreciation of specific

assets that are used by taxpayers in business for generating taxable earnings. An individual

taxpayer under “sec.40.25 (1), ITA Act 97” is permitted to get the deduction for depreciation

for the assets decline in value that is held for taxable purpose (Raftery 2019). Depreciation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

should not be viewed as the loss or outgoing and the acquisition of depreciating asset is held

as capital in nature, therefore the operation of “sec 8-1” is prohibited.

As explained in “sec 40.30(1)” depreciating asset is commonly treated as asset which

only has some degree of valuable lifespan. The depreciating asset are usually anticipated to

fall in their value on the basis of its usage. It do not take into account the trading stock.

Usually under “sec 40.30 (1), ITA Act 97”assets are not and it carries its original meaning.

Assets are usually considered under the definition of plant (Hegemann et al. 2017). The

judgement handed in “Wangaratta Woollen Mills Ltd v. FCT (1969)” stated that a structure

that was having the form of dye house was treated as plant as opposed to the normal

condition with constructions.

While “sec 40.40, ITA Act 97” is concerned with holding of an asset. Commonly, the

holder of the asset is regarded as its lawful owner. It may also include the partnership asset as

well. For a taxpayer to claim a deduction for the decline in value of the depreciating asset it is

necessary to have the taxable purpose. With regard to “sec.40.25 (2)” depreciation is

permitted for claim in respect to the depreciating assets which is used for assessable purpose

(Reynolds and Neubig 2016). In the meantime, under “sec 40-25 (7)”, a taxable purpose is

usually existent where the assets are used by the taxpayer for the production of assessable

earnings. The deduction is lowered based on the proportion of non-taxable purpose usage.

There are certain rules that is given in “Sub-Div.40-C” for ascertaining the cost of

depreciating asset for depreciation purpose. “Sub Div-40-C” lists down the two elements.

According to the “sec 40-175, ITA Act 1997” the cost of depreciating assets is usually

divided in two elements (Long et al. 2016). The first element under “sec 40.180” is worked

out when a taxpayer starts holding the asset. Under “sec 40-180 (3)” the first element would

usually comprise of the purchase price that is paid by taxpayers in acquiring the asset.

should not be viewed as the loss or outgoing and the acquisition of depreciating asset is held

as capital in nature, therefore the operation of “sec 8-1” is prohibited.

As explained in “sec 40.30(1)” depreciating asset is commonly treated as asset which

only has some degree of valuable lifespan. The depreciating asset are usually anticipated to

fall in their value on the basis of its usage. It do not take into account the trading stock.

Usually under “sec 40.30 (1), ITA Act 97”assets are not and it carries its original meaning.

Assets are usually considered under the definition of plant (Hegemann et al. 2017). The

judgement handed in “Wangaratta Woollen Mills Ltd v. FCT (1969)” stated that a structure

that was having the form of dye house was treated as plant as opposed to the normal

condition with constructions.

While “sec 40.40, ITA Act 97” is concerned with holding of an asset. Commonly, the

holder of the asset is regarded as its lawful owner. It may also include the partnership asset as

well. For a taxpayer to claim a deduction for the decline in value of the depreciating asset it is

necessary to have the taxable purpose. With regard to “sec.40.25 (2)” depreciation is

permitted for claim in respect to the depreciating assets which is used for assessable purpose

(Reynolds and Neubig 2016). In the meantime, under “sec 40-25 (7)”, a taxable purpose is

usually existent where the assets are used by the taxpayer for the production of assessable

earnings. The deduction is lowered based on the proportion of non-taxable purpose usage.

There are certain rules that is given in “Sub-Div.40-C” for ascertaining the cost of

depreciating asset for depreciation purpose. “Sub Div-40-C” lists down the two elements.

According to the “sec 40-175, ITA Act 1997” the cost of depreciating assets is usually

divided in two elements (Long et al. 2016). The first element under “sec 40.180” is worked

out when a taxpayer starts holding the asset. Under “sec 40-180 (3)” the first element would

usually comprise of the purchase price that is paid by taxpayers in acquiring the asset.

8TAXATION LAW

While “sec 40-190, ITA Act 97” is primarily dealing with second element. Under the

second element it mainly includes the cost that is paid in bringing the asset to its current state

and location and cost that are attributable to the balancing adjustment (Sikka 2017). The

examples of second element cost include the cost involved in delivery, capital improvements

made to the asset, installation expenses, removal or rearrangement fees and capital repairs

also included under this element.

Despite the fact, it is also necessary to identify the start time for claiming the decline

in value of asset. Under “sec 40.60 (1), ITA Act 97” a depreciating which is held by the

taxpayer begins to fall in value when the start time of the asset happens (Kenny 2017). The

depreciating asset start time begins when the asset is first utilized or the taxpayer has installed

the asset as set for commercial use.

Application:

The case provides the instances that John is manufacturer and producer of vehicle

parts and accessories. His main production includes the manufacturing of BMW vehicle

parts. He visited Germany to purchase a CNC machine and successfully imported it to

Australia by paying an amount of $300,000. The purchase of depreciating asset under “sec 8-

1, ITA Act 97” forms capital which is not permitted for deduction to John. Citing “FCT v

Sun Newspaper (1938)” the expenses amounts to profit yielding and it is capital in nature.

Alternatively “Div 40” can be implemented by John to claim deduction for the

depreciation of its CNC machine. Under “sec 40-25 (1), ITA Act 1997” an allowable

deduction for decline in value of CNC machine is claimable under this provision by John.

The CNC machine is categorized as depreciating asset under “sec.40-30 (1)” (Kenny 2017).

By referring to “Wangaratta Woollen Mills Ltd v. FCT (1969)” the CNC machine satisifies

While “sec 40-190, ITA Act 97” is primarily dealing with second element. Under the

second element it mainly includes the cost that is paid in bringing the asset to its current state

and location and cost that are attributable to the balancing adjustment (Sikka 2017). The

examples of second element cost include the cost involved in delivery, capital improvements

made to the asset, installation expenses, removal or rearrangement fees and capital repairs

also included under this element.

Despite the fact, it is also necessary to identify the start time for claiming the decline

in value of asset. Under “sec 40.60 (1), ITA Act 97” a depreciating which is held by the

taxpayer begins to fall in value when the start time of the asset happens (Kenny 2017). The

depreciating asset start time begins when the asset is first utilized or the taxpayer has installed

the asset as set for commercial use.

Application:

The case provides the instances that John is manufacturer and producer of vehicle

parts and accessories. His main production includes the manufacturing of BMW vehicle

parts. He visited Germany to purchase a CNC machine and successfully imported it to

Australia by paying an amount of $300,000. The purchase of depreciating asset under “sec 8-

1, ITA Act 97” forms capital which is not permitted for deduction to John. Citing “FCT v

Sun Newspaper (1938)” the expenses amounts to profit yielding and it is capital in nature.

Alternatively “Div 40” can be implemented by John to claim deduction for the

depreciation of its CNC machine. Under “sec 40-25 (1), ITA Act 1997” an allowable

deduction for decline in value of CNC machine is claimable under this provision by John.

The CNC machine is categorized as depreciating asset under “sec.40-30 (1)” (Kenny 2017).

By referring to “Wangaratta Woollen Mills Ltd v. FCT (1969)” the CNC machine satisifies

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

the ordinary meaning plant since it is limited effective life and it is projected to fall in value

on the basis of its usage over the time period. As the asset is bought by John under “sec

40.40”, he is considered as the legal owner or the holder of the asset.

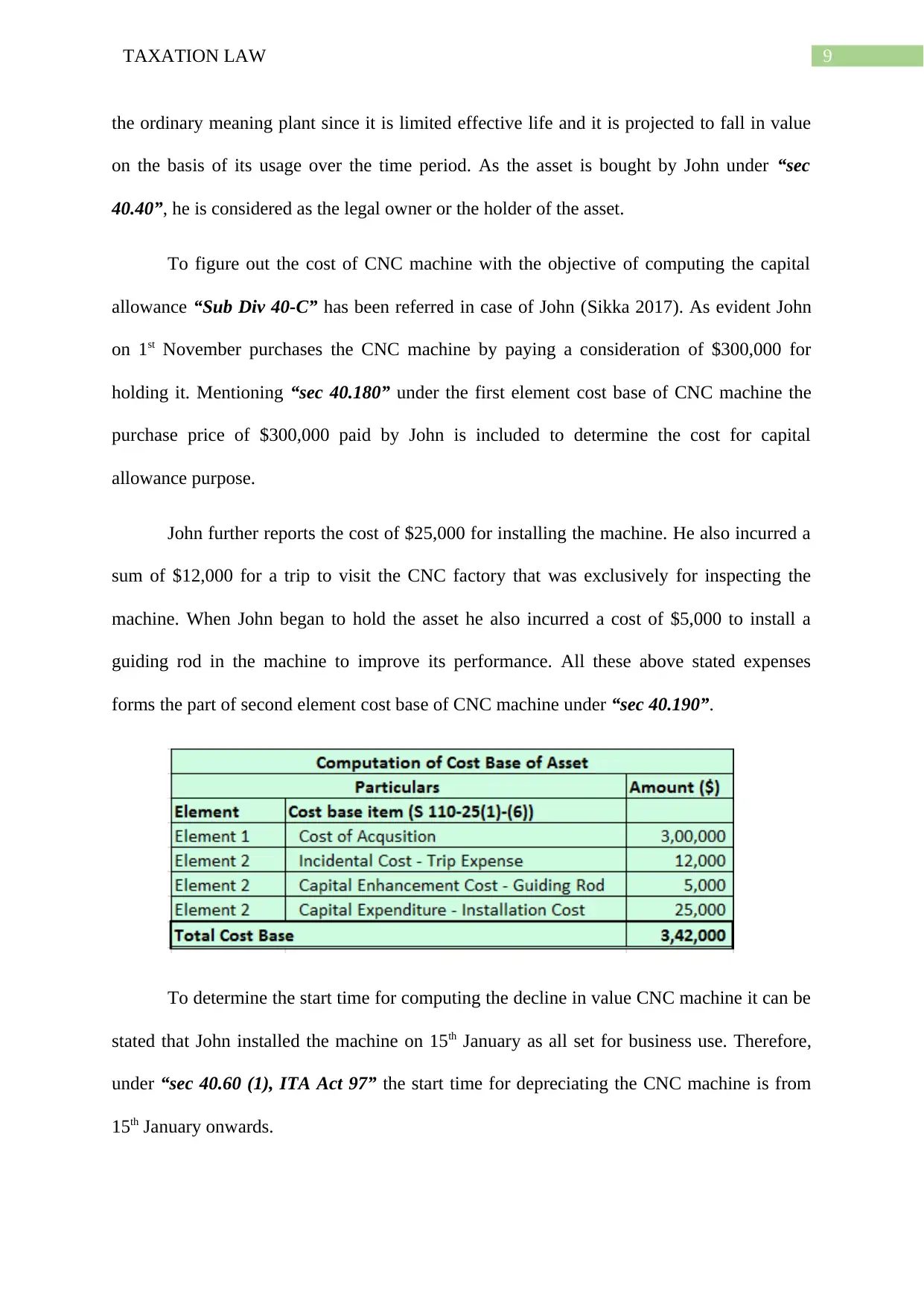

To figure out the cost of CNC machine with the objective of computing the capital

allowance “Sub Div 40-C” has been referred in case of John (Sikka 2017). As evident John

on 1st November purchases the CNC machine by paying a consideration of $300,000 for

holding it. Mentioning “sec 40.180” under the first element cost base of CNC machine the

purchase price of $300,000 paid by John is included to determine the cost for capital

allowance purpose.

John further reports the cost of $25,000 for installing the machine. He also incurred a

sum of $12,000 for a trip to visit the CNC factory that was exclusively for inspecting the

machine. When John began to hold the asset he also incurred a cost of $5,000 to install a

guiding rod in the machine to improve its performance. All these above stated expenses

forms the part of second element cost base of CNC machine under “sec 40.190”.

To determine the start time for computing the decline in value CNC machine it can be

stated that John installed the machine on 15th January as all set for business use. Therefore,

under “sec 40.60 (1), ITA Act 97” the start time for depreciating the CNC machine is from

15th January onwards.

the ordinary meaning plant since it is limited effective life and it is projected to fall in value

on the basis of its usage over the time period. As the asset is bought by John under “sec

40.40”, he is considered as the legal owner or the holder of the asset.

To figure out the cost of CNC machine with the objective of computing the capital

allowance “Sub Div 40-C” has been referred in case of John (Sikka 2017). As evident John

on 1st November purchases the CNC machine by paying a consideration of $300,000 for

holding it. Mentioning “sec 40.180” under the first element cost base of CNC machine the

purchase price of $300,000 paid by John is included to determine the cost for capital

allowance purpose.

John further reports the cost of $25,000 for installing the machine. He also incurred a

sum of $12,000 for a trip to visit the CNC factory that was exclusively for inspecting the

machine. When John began to hold the asset he also incurred a cost of $5,000 to install a

guiding rod in the machine to improve its performance. All these above stated expenses

forms the part of second element cost base of CNC machine under “sec 40.190”.

To determine the start time for computing the decline in value CNC machine it can be

stated that John installed the machine on 15th January as all set for business use. Therefore,

under “sec 40.60 (1), ITA Act 97” the start time for depreciating the CNC machine is from

15th January onwards.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Cnossen, S., 2018. Corporation taxes in the European Union: Slowly moving toward

comprehensive business income taxation?. International Tax and Public Finance, 25(3),

pp.808-840.

Coates, M., 2015. Tax on property in deceased Estates - Part I: CGT. Mondaq Business

Briefing, pp.Mondaq Business Briefing, May 6, 2015.

Evans, A.C., 2019. Why we use private trusts in Australia: The income tax dimension

explained. Sydney L. Rev., 41, p.217.

Hegemann, A., Kunoth, A., Rupp, K. and Sureth-Sloane, C., 2017. Hold or sell? How capital

gains taxation affects holding decisions. Review of Managerial Science, 11(3), pp.571-603.

Kenny, P., 2017. Tax opportunities for state governments.

Lam, D. and Whitney, A., 2016. Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

Mannix, J.E., 2017. An introduction to capital gains tax, Sydney: Butterworths.

Minas, John, Lim, Youngdeok and Evans, Chris, 2018. The impact of tax rate changes on

capital gains realisations: Evidence from Australia. Australian Tax Forum, 33(4), pp.635–

666.

Peter, M, 2015. Change to negative gearing and capital gains tax could save $9b. The Sydney

Morning Herald (Sydney, Australia), p.5.

References:

Cnossen, S., 2018. Corporation taxes in the European Union: Slowly moving toward

comprehensive business income taxation?. International Tax and Public Finance, 25(3),

pp.808-840.

Coates, M., 2015. Tax on property in deceased Estates - Part I: CGT. Mondaq Business

Briefing, pp.Mondaq Business Briefing, May 6, 2015.

Evans, A.C., 2019. Why we use private trusts in Australia: The income tax dimension

explained. Sydney L. Rev., 41, p.217.

Hegemann, A., Kunoth, A., Rupp, K. and Sureth-Sloane, C., 2017. Hold or sell? How capital

gains taxation affects holding decisions. Review of Managerial Science, 11(3), pp.571-603.

Kenny, P., 2017. Tax opportunities for state governments.

Lam, D. and Whitney, A., 2016. Practical aspects of the new foreign resident CGT

withholding tax. LSJ: Law Society of NSW Journal, (21), p.84.

Long, B., Campbell, J. and Kelshaw, C., 2016. The justice lens on taxation policy in

Australia. St Mark's Review, (235), p.94.

Mannix, J.E., 2017. An introduction to capital gains tax, Sydney: Butterworths.

Minas, John, Lim, Youngdeok and Evans, Chris, 2018. The impact of tax rate changes on

capital gains realisations: Evidence from Australia. Australian Tax Forum, 33(4), pp.635–

666.

Peter, M, 2015. Change to negative gearing and capital gains tax could save $9b. The Sydney

Morning Herald (Sydney, Australia), p.5.

11TAXATION LAW

Plummer, W., 2016. Tax consolidation update: Still grappling with these rules?. Tax

Specialist, 19(5), p.209.

Raftery, A., 2019. 101 Ways to Save Money on Your Tax-Legally! 2019-2020. Wiley.

Reynolds, H. and Neubig, T., 2016. Distinguishing between “normal” and “excess” returns

for tax policy.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Taylor & Francis.

Villios, S., et al., 2013. The capital gains tax implications of buy-sell agreements.(Australia).

Australian Tax Review, 41(2), pp.100–112.

Plummer, W., 2016. Tax consolidation update: Still grappling with these rules?. Tax

Specialist, 19(5), p.209.

Raftery, A., 2019. 101 Ways to Save Money on Your Tax-Legally! 2019-2020. Wiley.

Reynolds, H. and Neubig, T., 2016. Distinguishing between “normal” and “excess” returns

for tax policy.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Taylor & Francis.

Villios, S., et al., 2013. The capital gains tax implications of buy-sell agreements.(Australia).

Australian Tax Review, 41(2), pp.100–112.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.