Taxation Laws : Sample Assignment PDF

VerifiedAdded on 2021/06/14

|16

|3617

|25

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to C:..........................................................................................................................4

Answer to D:..........................................................................................................................5

Answer to E:...........................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................6

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................6

Answer to E:...........................................................................................................................6

Answer to question 3:.................................................................................................................7

Answer to B:..........................................................................................................................7

Answer to C:..........................................................................................................................8

Answer to D:..........................................................................................................................8

Answer to E:...........................................................................................................................9

Part B:.......................................................................................................................................10

Small Business Concessions:...................................................................................................10

Introduction:.........................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to C:..........................................................................................................................4

Answer to D:..........................................................................................................................5

Answer to E:...........................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................6

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................6

Answer to E:...........................................................................................................................6

Answer to question 3:.................................................................................................................7

Answer to B:..........................................................................................................................7

Answer to C:..........................................................................................................................8

Answer to D:..........................................................................................................................8

Answer to E:...........................................................................................................................9

Part B:.......................................................................................................................................10

Small Business Concessions:...................................................................................................10

Introduction:.........................................................................................................................10

2TAXATION LAW

Types of Concessions:..........................................................................................................10

Criteria of eligibility:............................................................................................................10

Objectives of Small business Concessions:.........................................................................11

History of tax measures for small business:.........................................................................11

Recent amendments made to the small business concessions:............................................11

Effectiveness of the methods:..............................................................................................13

Recommendations:...............................................................................................................13

Conclusion:..........................................................................................................................13

References................................................................................................................................14

Types of Concessions:..........................................................................................................10

Criteria of eligibility:............................................................................................................10

Objectives of Small business Concessions:.........................................................................11

History of tax measures for small business:.........................................................................11

Recent amendments made to the small business concessions:............................................11

Effectiveness of the methods:..............................................................................................13

Recommendations:...............................................................................................................13

Conclusion:..........................................................................................................................13

References................................................................................................................................14

3TAXATION LAW

Answer to question 1:

Answer to A:

According to the “section 25-10 of the ITAA 1997” an individual is allowed to claim

deductions relating to the expenditure that is incurred for repair on the premises or the

depreciating assets that is entirely held for generating income (Barkoczy, 2014). However, an

individual is not allowed to claim deductions relating to expenses that are capital in nature.

As evident in the situation of Bhavraj who bought a property on 30 June and undertook the

decision of repainting the entire building so that an Indian theme is reflected.

Any kind of repair that is carried out following the acquisition of property is referred

as initial repair. This reflects that the property is not in better order when it was purchased

and not suitable for producing income as the way planned. In the leading case of “W Thomas

and Co Pty Ltd v FCT (1965)” the cost incurred by the taxpayer on repairing the roof and

painting the building during the year in which it was acquired is regarded as capital

expenditure and not deductible (Brokelind, 2014). Similarly for Bhavraj the cost of repainting

the building is an initial repair of capital in nature and no deductions is allowable.

Answer to B:

According to the “division 40-25(1)” an entity can claim deductions for an amount

that is equivalent to the decline in value for the income year of the depreciating asset that is

held throughout the year (Coleman & Sadiq, 2013). As evident in the situation of Bhavraj a

new oven was installed with a cost price of $10,000 and incurs $1000 for transportation with

another $1000 for installation purpose. According to the simpler depreciation for small entity

an individual is allowed to immediately write off the or deduct the full cost of the asset in the

year when it is purchased given the cost of depreciating assets is less than $20,000.

Additionally the cost of assets also includes the cost that is incurred in transporting and

Answer to question 1:

Answer to A:

According to the “section 25-10 of the ITAA 1997” an individual is allowed to claim

deductions relating to the expenditure that is incurred for repair on the premises or the

depreciating assets that is entirely held for generating income (Barkoczy, 2014). However, an

individual is not allowed to claim deductions relating to expenses that are capital in nature.

As evident in the situation of Bhavraj who bought a property on 30 June and undertook the

decision of repainting the entire building so that an Indian theme is reflected.

Any kind of repair that is carried out following the acquisition of property is referred

as initial repair. This reflects that the property is not in better order when it was purchased

and not suitable for producing income as the way planned. In the leading case of “W Thomas

and Co Pty Ltd v FCT (1965)” the cost incurred by the taxpayer on repairing the roof and

painting the building during the year in which it was acquired is regarded as capital

expenditure and not deductible (Brokelind, 2014). Similarly for Bhavraj the cost of repainting

the building is an initial repair of capital in nature and no deductions is allowable.

Answer to B:

According to the “division 40-25(1)” an entity can claim deductions for an amount

that is equivalent to the decline in value for the income year of the depreciating asset that is

held throughout the year (Coleman & Sadiq, 2013). As evident in the situation of Bhavraj a

new oven was installed with a cost price of $10,000 and incurs $1000 for transportation with

another $1000 for installation purpose. According to the simpler depreciation for small entity

an individual is allowed to immediately write off the or deduct the full cost of the asset in the

year when it is purchased given the cost of depreciating assets is less than $20,000.

Additionally the cost of assets also includes the cost that is incurred in transporting and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

installing the assets. Similarly for Bhavraj the cost of new oven can be immediately written

off since it is less than $20,000 and the additional cost on transportation and installation can

be allowed as deductions.

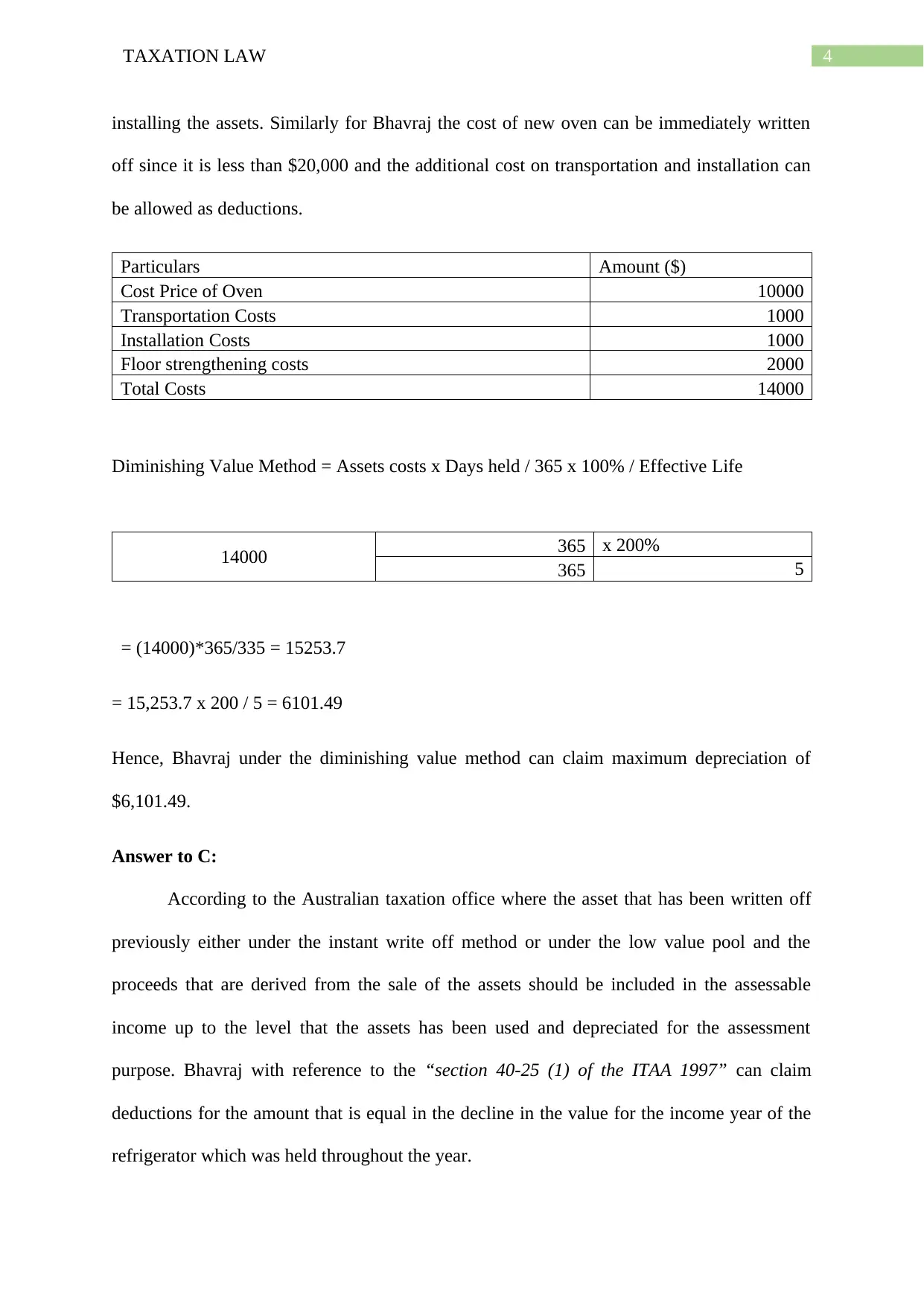

Particulars Amount ($)

Cost Price of Oven 10000

Transportation Costs 1000

Installation Costs 1000

Floor strengthening costs 2000

Total Costs 14000

Diminishing Value Method = Assets costs x Days held / 365 x 100% / Effective Life

14000 365 x 200%

365 5

= (14000)*365/335 = 15253.7

= 15,253.7 x 200 / 5 = 6101.49

Hence, Bhavraj under the diminishing value method can claim maximum depreciation of

$6,101.49.

Answer to C:

According to the Australian taxation office where the asset that has been written off

previously either under the instant write off method or under the low value pool and the

proceeds that are derived from the sale of the assets should be included in the assessable

income up to the level that the assets has been used and depreciated for the assessment

purpose. Bhavraj with reference to the “section 40-25 (1) of the ITAA 1997” can claim

deductions for the amount that is equal in the decline in the value for the income year of the

refrigerator which was held throughout the year.

installing the assets. Similarly for Bhavraj the cost of new oven can be immediately written

off since it is less than $20,000 and the additional cost on transportation and installation can

be allowed as deductions.

Particulars Amount ($)

Cost Price of Oven 10000

Transportation Costs 1000

Installation Costs 1000

Floor strengthening costs 2000

Total Costs 14000

Diminishing Value Method = Assets costs x Days held / 365 x 100% / Effective Life

14000 365 x 200%

365 5

= (14000)*365/335 = 15253.7

= 15,253.7 x 200 / 5 = 6101.49

Hence, Bhavraj under the diminishing value method can claim maximum depreciation of

$6,101.49.

Answer to C:

According to the Australian taxation office where the asset that has been written off

previously either under the instant write off method or under the low value pool and the

proceeds that are derived from the sale of the assets should be included in the assessable

income up to the level that the assets has been used and depreciated for the assessment

purpose. Bhavraj with reference to the “section 40-25 (1) of the ITAA 1997” can claim

deductions for the amount that is equal in the decline in the value for the income year of the

refrigerator which was held throughout the year.

5TAXATION LAW

Answer to D:

According to “section 8-1 of the ITAA 1997” an individual is allowed to claim

deductions relating to the cost that is incurred in producing the taxable income (Grange et al.,

2014). An individual taxpayer is allowed to claim deductions when the expenses are

necessarily incurred in producing or gaining the taxable income. Similarly in the case of

Bhavraj the cost that is incurred in resealing of customer car park cannot be allowed as

deductions since the cost of $5000 is not associated to the income deriving activities of the

taxpayer. The cost of resealing the car park is neither relevant nor incidental in derivation of

the taxable income.

Answer to E:

According to Australian taxation office a car is defined as motor vehicle that is

designed to carry load for less than one tonne (James, 2015). An individual at the time of

working out their deductions can use the cents per kilometre or the log book methods to claim

deductions. Evidently in case of Bhavraj the purchase of car was entirely for the business

purpose and he can claim deductions relating to the running expenditure of the car that are

incurred in process of business.

Answer to question 2:

Answer to A:

According to ATO ID 2004/489 an employer is entitled to claim deductions under

“section 8-1 of the ITAA 1997” relating to the long service leave contributions to the worker

entitlement fund (Kenny, 2013). Similarly in the case of Raj the payment of $10,000 for the

long service leave for his employees will be allowed as deductions under “section 8-1 of the

ITAA 1997”. The expenses are incurred in producing the assessable income of the taxpayer.

Answer to D:

According to “section 8-1 of the ITAA 1997” an individual is allowed to claim

deductions relating to the cost that is incurred in producing the taxable income (Grange et al.,

2014). An individual taxpayer is allowed to claim deductions when the expenses are

necessarily incurred in producing or gaining the taxable income. Similarly in the case of

Bhavraj the cost that is incurred in resealing of customer car park cannot be allowed as

deductions since the cost of $5000 is not associated to the income deriving activities of the

taxpayer. The cost of resealing the car park is neither relevant nor incidental in derivation of

the taxable income.

Answer to E:

According to Australian taxation office a car is defined as motor vehicle that is

designed to carry load for less than one tonne (James, 2015). An individual at the time of

working out their deductions can use the cents per kilometre or the log book methods to claim

deductions. Evidently in case of Bhavraj the purchase of car was entirely for the business

purpose and he can claim deductions relating to the running expenditure of the car that are

incurred in process of business.

Answer to question 2:

Answer to A:

According to ATO ID 2004/489 an employer is entitled to claim deductions under

“section 8-1 of the ITAA 1997” relating to the long service leave contributions to the worker

entitlement fund (Kenny, 2013). Similarly in the case of Raj the payment of $10,000 for the

long service leave for his employees will be allowed as deductions under “section 8-1 of the

ITAA 1997”. The expenses are incurred in producing the assessable income of the taxpayer.

6TAXATION LAW

Answer to B:

According to Section 26-5 of the ITAA 1997” an individual taxpayers is not allowed

to claim deductions relating to the penalties or fines that is imposed as the breach of the

Australian law (Krever, 2013). This includes parking fines that is incurred in the work related

travel. The parking fines of $5000 which is incurred by staff at the time of delivery of food

constitutes business fines. Under Section 26-5 of the ITAA 1997”, the parking fines will not

be allowed as deductions.

Answer to C:

For an expenditure to be considered as the allowable deductions for an outgoing it

must be incurred in gaining or producing the taxable income and should be incidental and

relevant to the end. As held in “W Neville & Co v FCT” the taxpayer was allowed to claim

deductions for the sum paid to the managing director for agreeing to resign since the payment

was to increase the efficiency of the company (Morgan et al., 2013). Referring to above

instance the payment of $10,000 made by Raj to obtain the resignation of restaurant manager

would be an allowable deductions under “section 8-1 of the ITAA 1997”.

Answer to D:

According to the Australian taxation office an individual is allowed to claim tax

deductions for the super payment that is made for the employees during the financial

(Murphy & Higgins, 2016). Evidently in the situation of Raj the superannuation contribution

that is made to the complying superannuation fund will be allowed as deductions. Therefore,

the sum of $45,000 can be claimed by Raj as an allowable deductions.

Answer to E:

Any form of losses or outgoing that are preliminary in the commencement of the

income generating business activities are usually not incurred in the course of business and

Answer to B:

According to Section 26-5 of the ITAA 1997” an individual taxpayers is not allowed

to claim deductions relating to the penalties or fines that is imposed as the breach of the

Australian law (Krever, 2013). This includes parking fines that is incurred in the work related

travel. The parking fines of $5000 which is incurred by staff at the time of delivery of food

constitutes business fines. Under Section 26-5 of the ITAA 1997”, the parking fines will not

be allowed as deductions.

Answer to C:

For an expenditure to be considered as the allowable deductions for an outgoing it

must be incurred in gaining or producing the taxable income and should be incidental and

relevant to the end. As held in “W Neville & Co v FCT” the taxpayer was allowed to claim

deductions for the sum paid to the managing director for agreeing to resign since the payment

was to increase the efficiency of the company (Morgan et al., 2013). Referring to above

instance the payment of $10,000 made by Raj to obtain the resignation of restaurant manager

would be an allowable deductions under “section 8-1 of the ITAA 1997”.

Answer to D:

According to the Australian taxation office an individual is allowed to claim tax

deductions for the super payment that is made for the employees during the financial

(Murphy & Higgins, 2016). Evidently in the situation of Raj the superannuation contribution

that is made to the complying superannuation fund will be allowed as deductions. Therefore,

the sum of $45,000 can be claimed by Raj as an allowable deductions.

Answer to E:

Any form of losses or outgoing that are preliminary in the commencement of the

income generating business activities are usually not incurred in the course of business and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

not allowed for deductions under the general provision of “section 8-1 of the ITAA 1997”. As

held in “Softwood Pulp & Paper v Federal Commissioner of Taxation (1976)” the company

occurred a feasibility study and other costs in order to ascertain whether to establish a new

production mill for paper (Pope et al., 2017). The taxation commissioner held that the cost

would not be allowed as deductions as it was preliminary to the commencement of the

income generating activities. Similarly, in case of Raj, the cost of $6,000 on feasibility study

for opening a new restaurant is a pre-commencement cost and no deductions is allowable as it

is preliminary to the commencement of the income generating activities.

Answer to question 3:

According to “section 108-10 (2) of the ITAA 1997” collectible refers to any artwork,

antique or a jewellery that is used or kept for the personal use or enjoyment (Woellner, 2013).

According to “section 118-10(1)” any form of capital gains and capital loss is disregarded

under the first element of the collectible’s cost base if it is less acquired for less than $500.

As evident an antique desk was acquired for a cost of $4000 but was sold for a loss at $3500.

According to subsection 108-10 (1) of the ITAA 1997 provides that at the time of

working out the net capital gains for the income year capital losses from the collectables can

be only used to reduce the capital gains from the collectables (Woellner et al., 2014). An

individual is required to disregard the capital losses made from the collectables. The loss

from the sale of Antique desk cannot be used to offset any capital gains since no gains was

reported from the sale of collectible. With reference to “subsection 108-10 of the ITAA

1997” Raj should disregard the loss from the sale of antique desk.

Answer to B:

A person used use asset under “subdivision 108-C” refers to the non-collectable

assets that are largely kept for personal use and enjoyment. This includes Yacht, furniture,

not allowed for deductions under the general provision of “section 8-1 of the ITAA 1997”. As

held in “Softwood Pulp & Paper v Federal Commissioner of Taxation (1976)” the company

occurred a feasibility study and other costs in order to ascertain whether to establish a new

production mill for paper (Pope et al., 2017). The taxation commissioner held that the cost

would not be allowed as deductions as it was preliminary to the commencement of the

income generating activities. Similarly, in case of Raj, the cost of $6,000 on feasibility study

for opening a new restaurant is a pre-commencement cost and no deductions is allowable as it

is preliminary to the commencement of the income generating activities.

Answer to question 3:

According to “section 108-10 (2) of the ITAA 1997” collectible refers to any artwork,

antique or a jewellery that is used or kept for the personal use or enjoyment (Woellner, 2013).

According to “section 118-10(1)” any form of capital gains and capital loss is disregarded

under the first element of the collectible’s cost base if it is less acquired for less than $500.

As evident an antique desk was acquired for a cost of $4000 but was sold for a loss at $3500.

According to subsection 108-10 (1) of the ITAA 1997 provides that at the time of

working out the net capital gains for the income year capital losses from the collectables can

be only used to reduce the capital gains from the collectables (Woellner et al., 2014). An

individual is required to disregard the capital losses made from the collectables. The loss

from the sale of Antique desk cannot be used to offset any capital gains since no gains was

reported from the sale of collectible. With reference to “subsection 108-10 of the ITAA

1997” Raj should disregard the loss from the sale of antique desk.

Answer to B:

A person used use asset under “subdivision 108-C” refers to the non-collectable

assets that are largely kept for personal use and enjoyment. This includes Yacht, furniture,

8TAXATION LAW

electrical goods and household items (Barkoczy, 2014). Under “section 118-10 (3)” any form

of capital gains made is disregarded from the personal use asset when the asset is acquired for

$10,000 or less. Referring to “section 118-10 (3)” Raj reported capital gains of $11,000 from

sale of Yacht but the cost base was less than $10,000 (i.e. $6000). Therefore, Raj should

disregard the capital gains from sale of Yacht.

Answer to C:

“Section 108-5 of the ITAA 1997” is concerned with CGT assets which includes,

shares in company land and buildings, goodwill etc. The shares in the company or units are

treated in the similar manner as any other assets for the purpose of capital gains tax

(Brokelind, 2014). The sale of shares by Raj and profits derived from such sale of shares

would be subjected to capital gains tax.

The 12-month ownership rule: Yes

Sold price: $8,500

Purchase price: $5,000

Capital gain $3,500

CGT Discount @ 50%

Taxable capital gain $1,750

Answer to D:

According to “section 108-5 (1) of the ITAA 1997” CGT asset also includes personal

use assets that costs more than $10,000 (Coleman & Sadiq, 2013). The sale or Mercedes car

by Raj constitutes personal use assets as the value of the car was greater than the threshold

limit of $10,000. The capital gains made from the sale of Mercedes car would be liable for

capital gains tax.

The 12-month ownership rule: Yes

Sold price: $175,000

electrical goods and household items (Barkoczy, 2014). Under “section 118-10 (3)” any form

of capital gains made is disregarded from the personal use asset when the asset is acquired for

$10,000 or less. Referring to “section 118-10 (3)” Raj reported capital gains of $11,000 from

sale of Yacht but the cost base was less than $10,000 (i.e. $6000). Therefore, Raj should

disregard the capital gains from sale of Yacht.

Answer to C:

“Section 108-5 of the ITAA 1997” is concerned with CGT assets which includes,

shares in company land and buildings, goodwill etc. The shares in the company or units are

treated in the similar manner as any other assets for the purpose of capital gains tax

(Brokelind, 2014). The sale of shares by Raj and profits derived from such sale of shares

would be subjected to capital gains tax.

The 12-month ownership rule: Yes

Sold price: $8,500

Purchase price: $5,000

Capital gain $3,500

CGT Discount @ 50%

Taxable capital gain $1,750

Answer to D:

According to “section 108-5 (1) of the ITAA 1997” CGT asset also includes personal

use assets that costs more than $10,000 (Coleman & Sadiq, 2013). The sale or Mercedes car

by Raj constitutes personal use assets as the value of the car was greater than the threshold

limit of $10,000. The capital gains made from the sale of Mercedes car would be liable for

capital gains tax.

The 12-month ownership rule: Yes

Sold price: $175,000

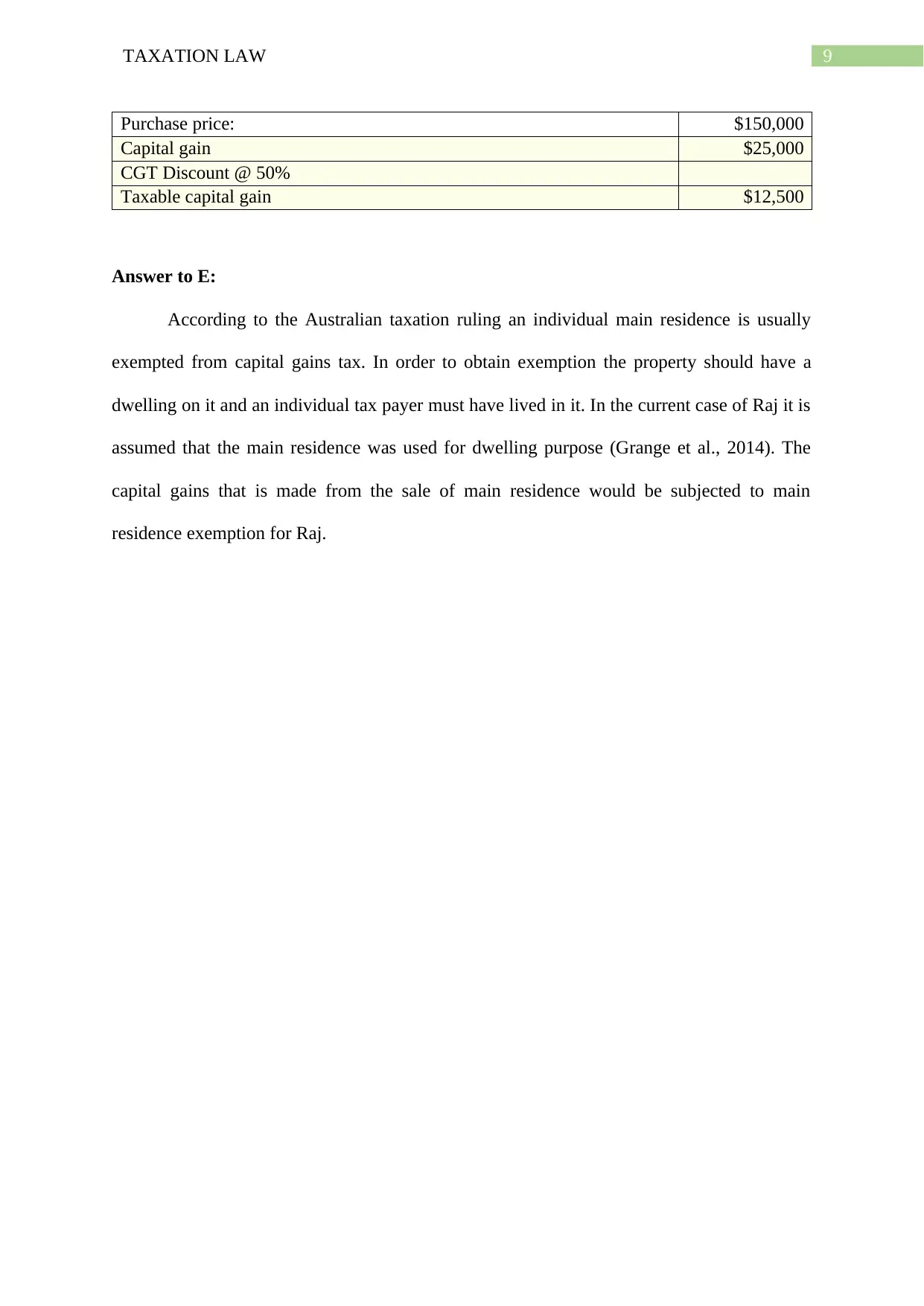

9TAXATION LAW

Purchase price: $150,000

Capital gain $25,000

CGT Discount @ 50%

Taxable capital gain $12,500

Answer to E:

According to the Australian taxation ruling an individual main residence is usually

exempted from capital gains tax. In order to obtain exemption the property should have a

dwelling on it and an individual tax payer must have lived in it. In the current case of Raj it is

assumed that the main residence was used for dwelling purpose (Grange et al., 2014). The

capital gains that is made from the sale of main residence would be subjected to main

residence exemption for Raj.

Purchase price: $150,000

Capital gain $25,000

CGT Discount @ 50%

Taxable capital gain $12,500

Answer to E:

According to the Australian taxation ruling an individual main residence is usually

exempted from capital gains tax. In order to obtain exemption the property should have a

dwelling on it and an individual tax payer must have lived in it. In the current case of Raj it is

assumed that the main residence was used for dwelling purpose (Grange et al., 2014). The

capital gains that is made from the sale of main residence would be subjected to main

residence exemption for Raj.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

Part B:

Small Business Concessions:

Introduction:

Small business accounts a sizeable portion of the Australian economy. The small

business contributes more than $1.5 trillion as revenue to the Australian economy. In spite of

their large contributions the small business are unable to attain a large scale benefits than the

larger counterparts (James, 2015). Because of the growing importance of the small business a

simplified tax system was introduced with the attempt of providing small business with the

options of tax measures in order to simply their tax measures and simultaneously reducing

their cost of tax compliance. For several small business owners the major source of

retirement funding constitute the sale of their business or the assets that are owned by them

(Kenny, 2013). The small business CGT concessions helps the taxpayers to reduce or

eliminate their capital gains based on sale of certain assets.

Types of Concessions:

There are usually four types of small business concessions that are available;

a. 15 year exemptions

b. 50% reduction in the active assets

c. Exemptions relating to retirement

d. Rollover exemptions

Criteria of eligibility:

To be eligible for small business concessions there are following eligibility criteria that is

required to be fulfilled;

a. Satisfying the net asset value test

Part B:

Small Business Concessions:

Introduction:

Small business accounts a sizeable portion of the Australian economy. The small

business contributes more than $1.5 trillion as revenue to the Australian economy. In spite of

their large contributions the small business are unable to attain a large scale benefits than the

larger counterparts (James, 2015). Because of the growing importance of the small business a

simplified tax system was introduced with the attempt of providing small business with the

options of tax measures in order to simply their tax measures and simultaneously reducing

their cost of tax compliance. For several small business owners the major source of

retirement funding constitute the sale of their business or the assets that are owned by them

(Kenny, 2013). The small business CGT concessions helps the taxpayers to reduce or

eliminate their capital gains based on sale of certain assets.

Types of Concessions:

There are usually four types of small business concessions that are available;

a. 15 year exemptions

b. 50% reduction in the active assets

c. Exemptions relating to retirement

d. Rollover exemptions

Criteria of eligibility:

To be eligible for small business concessions there are following eligibility criteria that is

required to be fulfilled;

a. Satisfying the net asset value test

11TAXATION LAW

b. Meeting the test of active assets

c. Where the assets are in the form of shares in the company or unit in the trust

Objectives of Small business Concessions:

The objective of the small business concessions was to provide eligible small business

with the new platform of dealing with their tax. The objective of implementing the simplified

tax measures was to reduce the compliance of income tax by 95% of the business. The initial

small business concession packaged enabled the small business with the options of

collectively adopting the four tax treatment packages (Krever, 2013). This included the

simplified rules for depreciation, cash accounting for income tax purpose, simplified trading

stock accounting rules and the capability of claiming an immediate tax deductions relating to

the prepaid expenditure. The four concessions that are provided in the small business

concessions is to increase the simplicity to qualify as the small business.

History of tax measures for small business:

The history of tax measures shows that the additional concessions were made

available to the business that included the CGT relief and the GST relief for accounting on

the cash basis (Morgan et al., 2013). The provision of the small business was applied on the

business that had turnover of less than $1 million each year, although the test of eligibility

differed in relation to other associated provisions. The old system required ignoring the

debtors and creditors with work-in-progress only taxed when it is realised.

Recent amendments made to the small business concessions:

The current regime is introduced through new business tax system relief that are

designed to attain the simplifications and greater degree of equity for the business. This

includes introducing the choice of accounting for GST based on the cash basis. Other notable

changes that were introduced are stated below;

b. Meeting the test of active assets

c. Where the assets are in the form of shares in the company or unit in the trust

Objectives of Small business Concessions:

The objective of the small business concessions was to provide eligible small business

with the new platform of dealing with their tax. The objective of implementing the simplified

tax measures was to reduce the compliance of income tax by 95% of the business. The initial

small business concession packaged enabled the small business with the options of

collectively adopting the four tax treatment packages (Krever, 2013). This included the

simplified rules for depreciation, cash accounting for income tax purpose, simplified trading

stock accounting rules and the capability of claiming an immediate tax deductions relating to

the prepaid expenditure. The four concessions that are provided in the small business

concessions is to increase the simplicity to qualify as the small business.

History of tax measures for small business:

The history of tax measures shows that the additional concessions were made

available to the business that included the CGT relief and the GST relief for accounting on

the cash basis (Morgan et al., 2013). The provision of the small business was applied on the

business that had turnover of less than $1 million each year, although the test of eligibility

differed in relation to other associated provisions. The old system required ignoring the

debtors and creditors with work-in-progress only taxed when it is realised.

Recent amendments made to the small business concessions:

The current regime is introduced through new business tax system relief that are

designed to attain the simplifications and greater degree of equity for the business. This

includes introducing the choice of accounting for GST based on the cash basis. Other notable

changes that were introduced are stated below;

12TAXATION LAW

a. Simplified depreciation method: The new amendments made enables the small

business to take the advantage of the simplified rules of depreciation under “section

328-170 to 325-257 of the ITAA 1997” (Murphy & Higgins, 2016). Another

significant change made is the using the simplified depreciation rules when the asset

is purchased during the year of income it can only be depreciated at half of the pool

rate for that year. The use of pro-rating depreciation is eliminated with the new rules.

b. Simplified rules for trading stock: A small business entity is not required to value

every item of their trading stock in hand at the end of the year of income. The value of

the trading stock can be carried forward indefinitely unless the value of the trading

stock goes surpasses the value of the opening stock by more than $5,000.

c. Claiming immediate deductions for prepayments: The small business will be

entitled to claim deductions relating to the prepaid tax expenses given the qualified

period of service is less than 12 months (Woellner et al., 2014). The new rules enables

the small business to claim tax deductions given the eligible service period ends prior

to the end of the income year after the year of expenditure.

d. Income tax on cash basis of accounting: Under the old method the small business

were required to account for the income tax based on the cash basis. However, with

the introduction of the new rules the small business entity can continue to make use of

the accounting for cash basis for the purpose of income tax given they are using cash

method of accounting before 30 June 2005. The system allows the business with

larger debtors balance to defer the payment of tax till the next income year in which

money was collected.

e. Accounting for GST for cash basis: An entity that meets the criteria of “section

328-110 of the ITAA 1997” would be able to account for GST based on cash basis

a. Simplified depreciation method: The new amendments made enables the small

business to take the advantage of the simplified rules of depreciation under “section

328-170 to 325-257 of the ITAA 1997” (Murphy & Higgins, 2016). Another

significant change made is the using the simplified depreciation rules when the asset

is purchased during the year of income it can only be depreciated at half of the pool

rate for that year. The use of pro-rating depreciation is eliminated with the new rules.

b. Simplified rules for trading stock: A small business entity is not required to value

every item of their trading stock in hand at the end of the year of income. The value of

the trading stock can be carried forward indefinitely unless the value of the trading

stock goes surpasses the value of the opening stock by more than $5,000.

c. Claiming immediate deductions for prepayments: The small business will be

entitled to claim deductions relating to the prepaid tax expenses given the qualified

period of service is less than 12 months (Woellner et al., 2014). The new rules enables

the small business to claim tax deductions given the eligible service period ends prior

to the end of the income year after the year of expenditure.

d. Income tax on cash basis of accounting: Under the old method the small business

were required to account for the income tax based on the cash basis. However, with

the introduction of the new rules the small business entity can continue to make use of

the accounting for cash basis for the purpose of income tax given they are using cash

method of accounting before 30 June 2005. The system allows the business with

larger debtors balance to defer the payment of tax till the next income year in which

money was collected.

e. Accounting for GST for cash basis: An entity that meets the criteria of “section

328-110 of the ITAA 1997” would be able to account for GST based on cash basis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13TAXATION LAW

(Pope et al., 2017). All the entities under the new rules are required to account for

GST based on the non-cash or accrual basis.

Effectiveness of the methods:

The findings from the study suggest that introducing the new policies for the small

business concessions has helped in reducing the compliance cost of tax that was faced by the

business (Woellner, 2013). This has enabled the small business with the choice in adopting

simplified tax rules and has ultimate resulted in reduced burden of compliance costs.

Recommendations:

It is disputed that the ability of the taxpayers to satisfy the $6 million maximum test

may be difficult to meet. It is recommended that the $6 million maximum net asset value test

should be replaced with some alternative eligibility test. This can be done through revised

aggregated turnover that would lead the concession being reduced gradually above the

threshold limit.

Conclusion:

The results obtained suggest that small business entity concession is being widely

adopted. The most popular small business concession were the CGT reliefs for small business

with the adoption of cash basis accounting for GST purpose. The simplified depreciations

rules and the immediate deductions for prepaid expenses could be viewed as an attempt in

reducing the cost compliance for the business.

(Pope et al., 2017). All the entities under the new rules are required to account for

GST based on the non-cash or accrual basis.

Effectiveness of the methods:

The findings from the study suggest that introducing the new policies for the small

business concessions has helped in reducing the compliance cost of tax that was faced by the

business (Woellner, 2013). This has enabled the small business with the choice in adopting

simplified tax rules and has ultimate resulted in reduced burden of compliance costs.

Recommendations:

It is disputed that the ability of the taxpayers to satisfy the $6 million maximum test

may be difficult to meet. It is recommended that the $6 million maximum net asset value test

should be replaced with some alternative eligibility test. This can be done through revised

aggregated turnover that would lead the concession being reduced gradually above the

threshold limit.

Conclusion:

The results obtained suggest that small business entity concession is being widely

adopted. The most popular small business concession were the CGT reliefs for small business

with the adoption of cash basis accounting for GST purpose. The simplified depreciations

rules and the immediate deductions for prepaid expenses could be viewed as an attempt in

reducing the cost compliance for the business.

14TAXATION LAW

References

Barkoczy, S. (2014) Foundations of taxation law.

Brokelind, C. (2014). Principles of law: function, status and impact in EU tax law.

Amsterdam: IBFD.

Coleman, C., & Sadiq, K. (2013) Principles of taxation law.

Grange, J., Jover-Ledesma, G., & Maydew, G. (2014) principles of business taxation.

James, M. (2015) Taxation of small businesses.

Kenny, P. (2013). Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. (2013). Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Murphy, K. E., & Higgins, M. (2016). Concepts in Federal Taxation 2017. Cengage

Learning.

Pope, T. R., Rupert, T. J., & Anderson, K. E. (2017). Pearson's Federal Taxation 2018

Corporations, Partnerships, Estates & Trusts. Pearson.

Woellner, R. (2013). Australian taxation law select 2013. North Ryde, N.S.W.: CCH

Australia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2014) Australian taxation

law.

References

Barkoczy, S. (2014) Foundations of taxation law.

Brokelind, C. (2014). Principles of law: function, status and impact in EU tax law.

Amsterdam: IBFD.

Coleman, C., & Sadiq, K. (2013) Principles of taxation law.

Grange, J., Jover-Ledesma, G., & Maydew, G. (2014) principles of business taxation.

James, M. (2015) Taxation of small businesses.

Kenny, P. (2013). Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. (2013). Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Murphy, K. E., & Higgins, M. (2016). Concepts in Federal Taxation 2017. Cengage

Learning.

Pope, T. R., Rupert, T. J., & Anderson, K. E. (2017). Pearson's Federal Taxation 2018

Corporations, Partnerships, Estates & Trusts. Pearson.

Woellner, R. (2013). Australian taxation law select 2013. North Ryde, N.S.W.: CCH

Australia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2014) Australian taxation

law.

15TAXATION LAW

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.