Taxation Law: Residency, Rental Income, and Sale of Land

VerifiedAdded on 2022/10/19

|14

|3590

|192

AI Summary

This document discusses the taxation law related to residency, rental income, and sale of land. It covers the rules and tests for determining residency status, tax obligations for rental income earned through digital platforms, and assessability of profits earned from selling sub-divided land. The document provides a comprehensive analysis of the relevant provisions and case laws.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Issues:.....................................................................................................................................5

Rule:.......................................................................................................................................5

Application:............................................................................................................................6

Conclusion:............................................................................................................................7

Answer to question 3:.................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................9

Answer to question 4:.................................................................................................................9

References:...............................................................................................................................12

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Issues:.....................................................................................................................................5

Rule:.......................................................................................................................................5

Application:............................................................................................................................6

Conclusion:............................................................................................................................7

Answer to question 3:.................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................9

Answer to question 4:.................................................................................................................9

References:...............................................................................................................................12

2TAXATION LAW

Answer to question 1:

Issues:

Will the taxpayer be treated as the resident of Australia under the definition of

“section 6 (1), ITAA 1936” for the purpose of tax?

Rule:

As given under “s995-1, ITAA 1997” Australian occupant denotes those people that

are living in Australia and includes those individuals who has their permanent residence or

house in Australia, barring when the tax officer is satisfied that the taxpayer has the fixed

home in overseas nation (Braithwaite & Reinhart, 2019). A person would be held as

Australian resident either on the continuous basis or sporadically if they have been present

physical in Australia for a minimum of six months barring when the commissioner is content

that an individual has fixed residence out of Australia and has no purpose of living in

Australia.

There are four test given under “s995-1, ITAA 1997” for ascertaining his or her status

of residence in Australia. they are as follows;

a. Resides Test

b. Permanent place of Abode Test

c. 183-Days Test

d. Superannuation Test

Resides Test:

The term resides implies to live for a considerable time period in Australia. It mainly

involves the extent of fact and degree (Barkoczy, 2016). This mainly involves the behaviour

while physically present in Australia. This mainly involves;

Answer to question 1:

Issues:

Will the taxpayer be treated as the resident of Australia under the definition of

“section 6 (1), ITAA 1936” for the purpose of tax?

Rule:

As given under “s995-1, ITAA 1997” Australian occupant denotes those people that

are living in Australia and includes those individuals who has their permanent residence or

house in Australia, barring when the tax officer is satisfied that the taxpayer has the fixed

home in overseas nation (Braithwaite & Reinhart, 2019). A person would be held as

Australian resident either on the continuous basis or sporadically if they have been present

physical in Australia for a minimum of six months barring when the commissioner is content

that an individual has fixed residence out of Australia and has no purpose of living in

Australia.

There are four test given under “s995-1, ITAA 1997” for ascertaining his or her status

of residence in Australia. they are as follows;

a. Resides Test

b. Permanent place of Abode Test

c. 183-Days Test

d. Superannuation Test

Resides Test:

The term resides implies to live for a considerable time period in Australia. It mainly

involves the extent of fact and degree (Barkoczy, 2016). This mainly involves the behaviour

while physically present in Australia. This mainly involves;

3TAXATION LAW

a. The intention of physically present in Australia

b. Family, business or work ties

c. Maintenance and location of Assets

d. Social arrangements for living

Weightage must be provided to each above outlined factor as it will vary with case

and no single factor will be treated exclusive. The court in “FCT v Joachim (2002)” held

that physically present and intentions may overlap for most of the time nevertheless, there are

some persons that may be considered as residing in Australia (Burton & Karlinsky, 2016).

The primary test is, whether the taxpayer has any kind of continuousness with the place

together with the purpose of coming back to that same place and the assertiveness that the

places is their home.

Domicile Test:

Under this test an individual if domiciled in Australia then they will continue to

remain Australian resident despite they live in foreign nation, unless the ATO is content that

an individual has made their permanent home in another nation. The “taxation ruling of IT

2650” deals with the permanent place of abode out of Australia. Relevant consideration such

as the intended length of individuals that stay in their overseas along with the duration and

continuity of a person’s stay in foreign country (Saad, 2014). The abandonment of any place

of residence in Australia and permanency of association which an individual has with the

specific place in Australia. As held in “Applegate v FCT (1979)” the law court held that the

word permanent implies everlasting and its objectivity is determined each year. The taxpayer

was considered to have permanent place of abode out of Australia.

183-Days Test:

a. The intention of physically present in Australia

b. Family, business or work ties

c. Maintenance and location of Assets

d. Social arrangements for living

Weightage must be provided to each above outlined factor as it will vary with case

and no single factor will be treated exclusive. The court in “FCT v Joachim (2002)” held

that physically present and intentions may overlap for most of the time nevertheless, there are

some persons that may be considered as residing in Australia (Burton & Karlinsky, 2016).

The primary test is, whether the taxpayer has any kind of continuousness with the place

together with the purpose of coming back to that same place and the assertiveness that the

places is their home.

Domicile Test:

Under this test an individual if domiciled in Australia then they will continue to

remain Australian resident despite they live in foreign nation, unless the ATO is content that

an individual has made their permanent home in another nation. The “taxation ruling of IT

2650” deals with the permanent place of abode out of Australia. Relevant consideration such

as the intended length of individuals that stay in their overseas along with the duration and

continuity of a person’s stay in foreign country (Saad, 2014). The abandonment of any place

of residence in Australia and permanency of association which an individual has with the

specific place in Australia. As held in “Applegate v FCT (1979)” the law court held that the

word permanent implies everlasting and its objectivity is determined each year. The taxpayer

was considered to have permanent place of abode out of Australia.

183-Days Test:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

A person is held to Australian resident on constant or intermittent basis for a

minimum of 183 days or more in the relevant income year.

Superannuation Test:

This test is applied on individuals that are the member of commonwealth superannuation

fund.

Application:

The case study provides that Adam worked in Dubai from 1st November 2017 till 1st

April 2018 and resided in the leased apartment given by the company. Nevertheless, in May

2018 Adam relocated to Dubai for an indefinite time period. Below outlined test is

implemented to determine Adam residency position;

Resides Test: In spite of the fact that Adam has the residence in Australia where his family

resided, this factor cannot be considered significant enough to determine his residency

position. Adam for the first half of 2017/18 was not present in Australia and resided in a

temporary leased apartment in Dubai given by his company. While for 2018/19 he signed the

contract of relocating to Dubai for the indefinite time period. As held in “Joachim v FCT

(2002)” he would not be considered as Australian occupant since Adam was not existent

physically in Australia and only came back for a short visit to spend time with his family.

Domicile Test: Starting from 1st November to 1st April 2017/18, Adam during his

employment visit in Dubai lived in temporary leased apartment that was given by his

employer. This means that his stay was temporary in nature and Adam did not set up any

permanent residence out of Australia. Within the meaning of “section 6 (1), ITAA 1936”,

Adam for 2017/18 will be treated as Australian resident (Thuronyi & Brooks, 2016). Whereas

in 2018/19 after relocating to Dubai for indefinite time period because he had not

conclusively stated his choice of residence in Australia as he bought an apartment in Dubai

A person is held to Australian resident on constant or intermittent basis for a

minimum of 183 days or more in the relevant income year.

Superannuation Test:

This test is applied on individuals that are the member of commonwealth superannuation

fund.

Application:

The case study provides that Adam worked in Dubai from 1st November 2017 till 1st

April 2018 and resided in the leased apartment given by the company. Nevertheless, in May

2018 Adam relocated to Dubai for an indefinite time period. Below outlined test is

implemented to determine Adam residency position;

Resides Test: In spite of the fact that Adam has the residence in Australia where his family

resided, this factor cannot be considered significant enough to determine his residency

position. Adam for the first half of 2017/18 was not present in Australia and resided in a

temporary leased apartment in Dubai given by his company. While for 2018/19 he signed the

contract of relocating to Dubai for the indefinite time period. As held in “Joachim v FCT

(2002)” he would not be considered as Australian occupant since Adam was not existent

physically in Australia and only came back for a short visit to spend time with his family.

Domicile Test: Starting from 1st November to 1st April 2017/18, Adam during his

employment visit in Dubai lived in temporary leased apartment that was given by his

employer. This means that his stay was temporary in nature and Adam did not set up any

permanent residence out of Australia. Within the meaning of “section 6 (1), ITAA 1936”,

Adam for 2017/18 will be treated as Australian resident (Thuronyi & Brooks, 2016). Whereas

in 2018/19 after relocating to Dubai for indefinite time period because he had not

conclusively stated his choice of residence in Australia as he bought an apartment in Dubai

5TAXATION LAW

which reflected a durability of association with that place. Referring to “Applegate v FCT

(1979)” Adam will be treated as non-resident of Australia since he only visited for six weeks

all through the year (Chardon et al., 2016). This factor adds weight that Adam within the

provision of “section 6 (1), ITAA 1936” will not be held Australian resident for 2018/19.

183-Days Test:

Starting from 2017/18 and 2018/19 Adam was physically not existent in Australia for

183 days in the concerned income year. Hence, he is not an Australian resident under this

test.

Superannuation Test:

The superannuation test is irrelevant in case of Adam as he does not has membership

with superannuation fund.

Conclusion:

On a conclusive note, Adam for 2017/18 will be treated as Australian resident because

he did not set up any permanent place of abode out of Australia however for 2018/19 Adam

within the provision of “section 6 (1), ITAA 1997” will be held as not an Australian resident

as he successfully passed the residence test.

Answer to question 2:

Issues:

Will the taxpayer be held accountable for tax on earning rental income from renting

out his townhouse on Airbnb? The second issue is whether the taxpayer is under obligation of

registering for GST on renting out the townhouse for Airbnb?

which reflected a durability of association with that place. Referring to “Applegate v FCT

(1979)” Adam will be treated as non-resident of Australia since he only visited for six weeks

all through the year (Chardon et al., 2016). This factor adds weight that Adam within the

provision of “section 6 (1), ITAA 1936” will not be held Australian resident for 2018/19.

183-Days Test:

Starting from 2017/18 and 2018/19 Adam was physically not existent in Australia for

183 days in the concerned income year. Hence, he is not an Australian resident under this

test.

Superannuation Test:

The superannuation test is irrelevant in case of Adam as he does not has membership

with superannuation fund.

Conclusion:

On a conclusive note, Adam for 2017/18 will be treated as Australian resident because

he did not set up any permanent place of abode out of Australia however for 2018/19 Adam

within the provision of “section 6 (1), ITAA 1997” will be held as not an Australian resident

as he successfully passed the residence test.

Answer to question 2:

Issues:

Will the taxpayer be held accountable for tax on earning rental income from renting

out his townhouse on Airbnb? The second issue is whether the taxpayer is under obligation of

registering for GST on renting out the townhouse for Airbnb?

6TAXATION LAW

Rule:

Rent must be considered as price which is paid for using another person’s property

particularly land, building, equipment etc. As a general rule, rent is viewed as ordinary

earnings. It is the payment that is provided by one person in exchange of using the another

person’s property for the specified time period (Evans et al., 2015). Receipt of rent must be

treated as ordinary income under the flow concept because rent flows from investment made

in rental property.

As stated by ATO, where a taxpayer rents out the property or makes an investment in

rental property, they would be required to keep track of the records right from the beginning

and compute the sum of expenses one needs to claim as permissible deductions (Miller &

Oats, 2016). The taxpayer is mandatorily required to declare their income while filing tax

return for the rental property.

The ATO guides the taxpayer regarding the sharing economy and tax. When the

taxpayer rents either in full or a portion of their residential house through digital platform

namely the Airbnb, Home Away or Flipkey then the taxpayer is under the obligation of

keeping track of their records for the income that is earned and declare the same in their

taxable income (Bankman et al., 2019). The taxpayer is also under obligation of keeping their

records of outgoings which they can claim as deductions (Freudenberg et al., 2017). The

taxpayers are not necessarily required to pay GST for the sum of residential rent earned.

Alternatively, GST is not applied on the residential property. The residential property owners

do not need to register for GST relating to rent which is charged and cannot claim GST

credits for rental outgoings.

Rule:

Rent must be considered as price which is paid for using another person’s property

particularly land, building, equipment etc. As a general rule, rent is viewed as ordinary

earnings. It is the payment that is provided by one person in exchange of using the another

person’s property for the specified time period (Evans et al., 2015). Receipt of rent must be

treated as ordinary income under the flow concept because rent flows from investment made

in rental property.

As stated by ATO, where a taxpayer rents out the property or makes an investment in

rental property, they would be required to keep track of the records right from the beginning

and compute the sum of expenses one needs to claim as permissible deductions (Miller &

Oats, 2016). The taxpayer is mandatorily required to declare their income while filing tax

return for the rental property.

The ATO guides the taxpayer regarding the sharing economy and tax. When the

taxpayer rents either in full or a portion of their residential house through digital platform

namely the Airbnb, Home Away or Flipkey then the taxpayer is under the obligation of

keeping track of their records for the income that is earned and declare the same in their

taxable income (Bankman et al., 2019). The taxpayer is also under obligation of keeping their

records of outgoings which they can claim as deductions (Freudenberg et al., 2017). The

taxpayers are not necessarily required to pay GST for the sum of residential rent earned.

Alternatively, GST is not applied on the residential property. The residential property owners

do not need to register for GST relating to rent which is charged and cannot claim GST

credits for rental outgoings.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Application:

Accordingly, in the present situation of Orpheus has rented his ground floor of his

townhouse in Sydney. Orpheus partially rented out the property to Airbnb and the total days

the property was rented out stood 150 days. The taxpayer must apportion the claim in relation

to the ownership interest as the property was only partially only rented out. The receipt of

rent here by Orpheus should be viewed as ordinary income under the “section 6-5, ITAA

1997” since it comprises of circular flow of income (Sadiq, 2019). Additionally, Orpheus will

only be allowed to claim the outgoings for the period of 150 days only because the property

was only let for rent during those time period. To claim the expenses for income tax

deduction, Orpheus must keep record of those expenses. The rental income that is earned by

Orpheus will be included into his tax return for renting out a portion of his house since the

rent that is received is an ordinary income under the meaning of “section 6-5, ITAA 1997”.

Additionally, Orpheus do not need to register for GST because no GST is paid for

renting out the residential property which is rented out through digital platform. Additionally,

no GST is chargeable on the rent earned by Orpheus for doing Airbnb. This is because the

taxpayer is not performing any kind of business activities.

Conclusion:

Conclusively, rent received from letting out a portion of house is regarded as the

ordinary income and will be taxable as ordinary income under “section 6-5, ITAA 1997”.

Furthermore, Orpheus is not required to register for GST because no GST is payable for

renting out the property through digital platform.

Application:

Accordingly, in the present situation of Orpheus has rented his ground floor of his

townhouse in Sydney. Orpheus partially rented out the property to Airbnb and the total days

the property was rented out stood 150 days. The taxpayer must apportion the claim in relation

to the ownership interest as the property was only partially only rented out. The receipt of

rent here by Orpheus should be viewed as ordinary income under the “section 6-5, ITAA

1997” since it comprises of circular flow of income (Sadiq, 2019). Additionally, Orpheus will

only be allowed to claim the outgoings for the period of 150 days only because the property

was only let for rent during those time period. To claim the expenses for income tax

deduction, Orpheus must keep record of those expenses. The rental income that is earned by

Orpheus will be included into his tax return for renting out a portion of his house since the

rent that is received is an ordinary income under the meaning of “section 6-5, ITAA 1997”.

Additionally, Orpheus do not need to register for GST because no GST is paid for

renting out the residential property which is rented out through digital platform. Additionally,

no GST is chargeable on the rent earned by Orpheus for doing Airbnb. This is because the

taxpayer is not performing any kind of business activities.

Conclusion:

Conclusively, rent received from letting out a portion of house is regarded as the

ordinary income and will be taxable as ordinary income under “section 6-5, ITAA 1997”.

Furthermore, Orpheus is not required to register for GST because no GST is payable for

renting out the property through digital platform.

8TAXATION LAW

Answer to question 3:

Issues:

Will the taxpayer be held assessable under “section 25 (1)” or the “section 26 (a)” for

the income earned from selling the sub-divided land in small blocks which was originally

purchased for farming purpose.

Rule:

The land must be viewed as CGT asset and its sale would lead to CGT event A1. As

given in “section 108-10, ITAA 1997” a CGT event A1 happens when the taxpayer sells the

CGT asset. Sub-dividing the land do not lead to sale of land within “section 104-10, ITAA

1997” (Butler, 2019). Accordingly, if the disposal of land by taxpayer results in business or

the part of business then the revenue that is earned from selling the land will be taxable as

ordinary income under the provision of “section 6-5 of the ITAA 1997”. Whereas if the sale

constitutes a mere realisation of capital asset then the sales proceeds derived would be held as

capital in nature.

As defined in “Taxation Determination of TR 97/3” if the profits which is earned

from isolated transaction then it will be treated as income and therefore it will be considered

assessable under “subsection 25 (1) of the ITAA 1936” (Murray et al., 2018). Referring to

the case of “Moana Sand Pty Ltd v FC of T (1988)” both within “section 25 (1)” and the

“section 26 (a)” was applicable to include the sum into the assessable income of the taxpayer

and the sum which was received by the taxpayer during the year as the outcome of single sale

and under the isolated transaction (Woellner et al., 2016). Hence, the profit which was earned

was held as ordinary income. While in another event of “Crow v FC of T (1988)” the

commissioner held that the taxpayer was assessable relating to profits which was derived

from carrying on the business of land development.

Answer to question 3:

Issues:

Will the taxpayer be held assessable under “section 25 (1)” or the “section 26 (a)” for

the income earned from selling the sub-divided land in small blocks which was originally

purchased for farming purpose.

Rule:

The land must be viewed as CGT asset and its sale would lead to CGT event A1. As

given in “section 108-10, ITAA 1997” a CGT event A1 happens when the taxpayer sells the

CGT asset. Sub-dividing the land do not lead to sale of land within “section 104-10, ITAA

1997” (Butler, 2019). Accordingly, if the disposal of land by taxpayer results in business or

the part of business then the revenue that is earned from selling the land will be taxable as

ordinary income under the provision of “section 6-5 of the ITAA 1997”. Whereas if the sale

constitutes a mere realisation of capital asset then the sales proceeds derived would be held as

capital in nature.

As defined in “Taxation Determination of TR 97/3” if the profits which is earned

from isolated transaction then it will be treated as income and therefore it will be considered

assessable under “subsection 25 (1) of the ITAA 1936” (Murray et al., 2018). Referring to

the case of “Moana Sand Pty Ltd v FC of T (1988)” both within “section 25 (1)” and the

“section 26 (a)” was applicable to include the sum into the assessable income of the taxpayer

and the sum which was received by the taxpayer during the year as the outcome of single sale

and under the isolated transaction (Woellner et al., 2016). Hence, the profit which was earned

was held as ordinary income. While in another event of “Crow v FC of T (1988)” the

commissioner held that the taxpayer was assessable relating to profits which was derived

from carrying on the business of land development.

9TAXATION LAW

Application:

Joe disposed the land which he had kept it as retirement nest egg for a sum of

$700,000. But when a real-estate agent approached Joe with the offer of constructing eight

townhouse on land, Joe readily accepted the offer and decided to construct eight townhouses

on the subdivided land. Joe also engaged the service of real estate agent and sold each

townhouse for a sum of $650,000. Joe initially bought the land with the intention of keeping

the land as the retirement nest egg. Referring to the decision made in “Moana Sand Pty Ltd v

FC of T (1988)” the profits which was earned from the disposal of land within the ordinary

concepts.

Joe here will be considered assessable for the profits which is earned from selling the

several sub-divided lots. Accordingly, the profits which is earned is generally taxable within

the meaning of “section 25 (1) of the ITAA 1936” as income derived from conducting the

business of land development or under “section 26 (a)” as the profit arising from conducting

the profit making undertaking (Qureshi & Kumar, 2019). The taxpayer here Joe disposed the

land in the enterprising way by undertaking extensive amount work on the land in order to

obtain the best price of the land.

Joe here will be considered for tax relating to profits which is earned from the sale of

land under “section 25 (1)” since he has gone a step ahead of realizing the capital asset and

subdividing as well as sale of land constitutes carrying on the business of land development

(Morgan et al., 2018). In the present case, the extensive development and subdivision of land

by Joe is greater than simple realisation of the asset. It constituted work done in the course of

business activities.

Application:

Joe disposed the land which he had kept it as retirement nest egg for a sum of

$700,000. But when a real-estate agent approached Joe with the offer of constructing eight

townhouse on land, Joe readily accepted the offer and decided to construct eight townhouses

on the subdivided land. Joe also engaged the service of real estate agent and sold each

townhouse for a sum of $650,000. Joe initially bought the land with the intention of keeping

the land as the retirement nest egg. Referring to the decision made in “Moana Sand Pty Ltd v

FC of T (1988)” the profits which was earned from the disposal of land within the ordinary

concepts.

Joe here will be considered assessable for the profits which is earned from selling the

several sub-divided lots. Accordingly, the profits which is earned is generally taxable within

the meaning of “section 25 (1) of the ITAA 1936” as income derived from conducting the

business of land development or under “section 26 (a)” as the profit arising from conducting

the profit making undertaking (Qureshi & Kumar, 2019). The taxpayer here Joe disposed the

land in the enterprising way by undertaking extensive amount work on the land in order to

obtain the best price of the land.

Joe here will be considered for tax relating to profits which is earned from the sale of

land under “section 25 (1)” since he has gone a step ahead of realizing the capital asset and

subdividing as well as sale of land constitutes carrying on the business of land development

(Morgan et al., 2018). In the present case, the extensive development and subdivision of land

by Joe is greater than simple realisation of the asset. It constituted work done in the course of

business activities.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

Conclusion:

On a concluding note, Joe will be treated taxable for the profits obtained from selling

the several lots under “section 25 (1), ITAA 1936” since it amounted to carrying on the

business of land development or profit deriving scheme.

Answer to question 4:

As explained in “section 104-10, ITAA 1997”, a CGT event A1 takes place when a

taxpayer sells the CGT asset. The decision made in “Sara Lee Household & Body Care

(Aust) Pty Ltd v FCT (2000)” held that when an is disposed under a contract, the time of

contract takes place when the CGT event takes place (Morgan & Castelyn, 2018). On the

other hand, when an asset is not disposed under the contract, then the CGT event takes place

when the change in the ownership takes place.

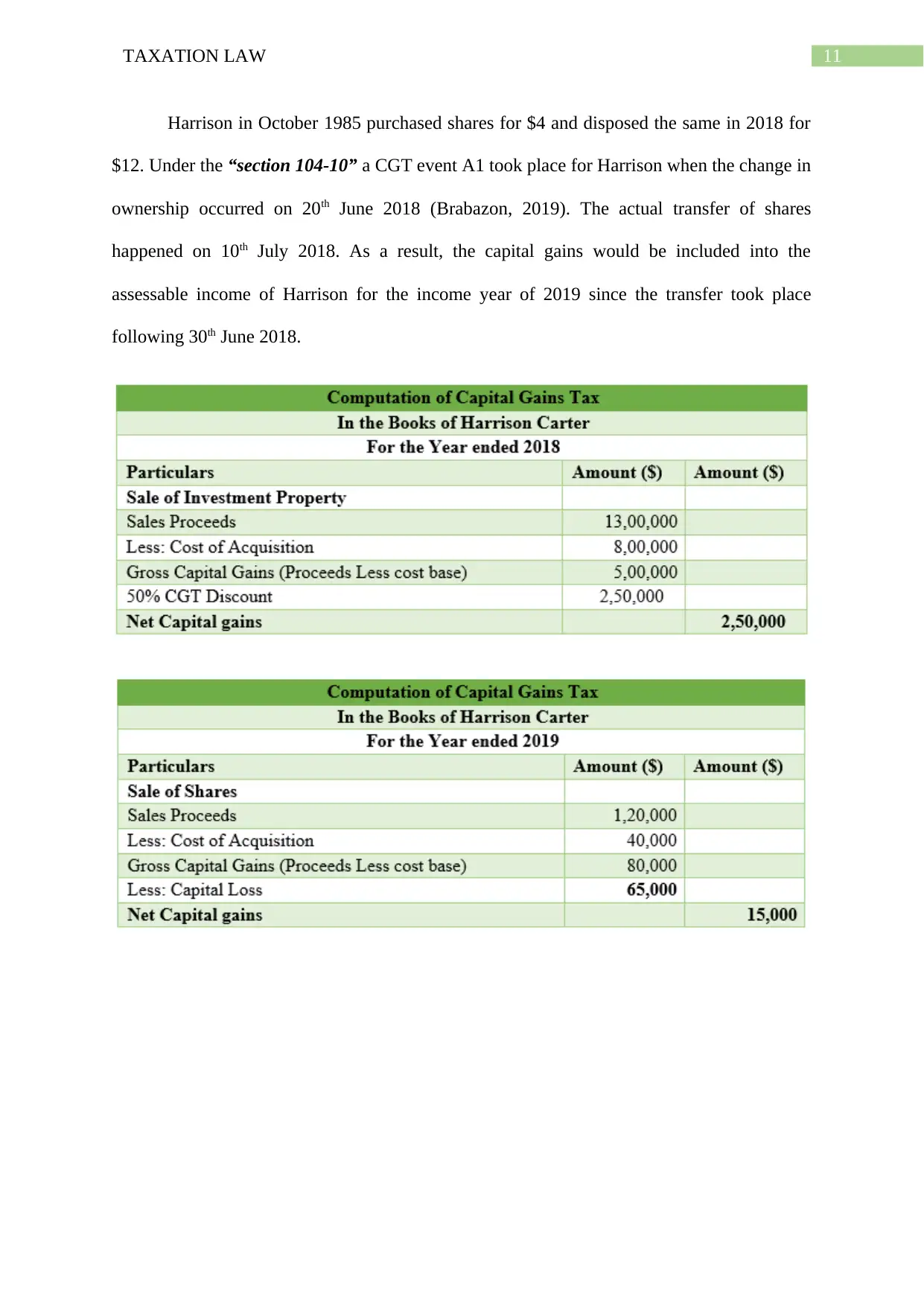

In light of the current case, a contract was entered into by Harrison to sell the

investment property on 14 June 2018 for a price of $1.3 million. Referring to the case of

“Sara Lee Household & Body Care (Aust) Pty Ltd v FCT (2000)” the disposal of

investment property by Harrison resulted in CGT event A1 under the “section 104-10, ITAA

1997” (Pert et al., 2018).

As stated by the ATO if a taxpayer disposes the capital asset especially the real estate

or the shares, they usually make capital gains or loss. A taxpayer in this case is under

obligation of reporting the capital gains and losses in their tax return and pay the taxes on the

capital gains (Robin & Barkoczy, 2019). According to the ATO, acquisition of shares in the

company or in units are held as capital asset just like any other asset for the purpose of CGT.

Capital gains tax is applied on the shares when the CGT event happens or when the asset is

sold by them.

Conclusion:

On a concluding note, Joe will be treated taxable for the profits obtained from selling

the several lots under “section 25 (1), ITAA 1936” since it amounted to carrying on the

business of land development or profit deriving scheme.

Answer to question 4:

As explained in “section 104-10, ITAA 1997”, a CGT event A1 takes place when a

taxpayer sells the CGT asset. The decision made in “Sara Lee Household & Body Care

(Aust) Pty Ltd v FCT (2000)” held that when an is disposed under a contract, the time of

contract takes place when the CGT event takes place (Morgan & Castelyn, 2018). On the

other hand, when an asset is not disposed under the contract, then the CGT event takes place

when the change in the ownership takes place.

In light of the current case, a contract was entered into by Harrison to sell the

investment property on 14 June 2018 for a price of $1.3 million. Referring to the case of

“Sara Lee Household & Body Care (Aust) Pty Ltd v FCT (2000)” the disposal of

investment property by Harrison resulted in CGT event A1 under the “section 104-10, ITAA

1997” (Pert et al., 2018).

As stated by the ATO if a taxpayer disposes the capital asset especially the real estate

or the shares, they usually make capital gains or loss. A taxpayer in this case is under

obligation of reporting the capital gains and losses in their tax return and pay the taxes on the

capital gains (Robin & Barkoczy, 2019). According to the ATO, acquisition of shares in the

company or in units are held as capital asset just like any other asset for the purpose of CGT.

Capital gains tax is applied on the shares when the CGT event happens or when the asset is

sold by them.

11TAXATION LAW

Harrison in October 1985 purchased shares for $4 and disposed the same in 2018 for

$12. Under the “section 104-10” a CGT event A1 took place for Harrison when the change in

ownership occurred on 20th June 2018 (Brabazon, 2019). The actual transfer of shares

happened on 10th July 2018. As a result, the capital gains would be included into the

assessable income of Harrison for the income year of 2019 since the transfer took place

following 30th June 2018.

Harrison in October 1985 purchased shares for $4 and disposed the same in 2018 for

$12. Under the “section 104-10” a CGT event A1 took place for Harrison when the change in

ownership occurred on 20th June 2018 (Brabazon, 2019). The actual transfer of shares

happened on 10th July 2018. As a result, the capital gains would be included into the

assessable income of Harrison for the income year of 2019 since the transfer took place

following 30th June 2018.

12TAXATION LAW

References:

Bankman, J., Shaviro, D. N., Stark, K. J., & Kleinbard, E. D. (2018). Federal Income

Taxation. Aspen Publishers.

Barkoczy, S. (2016). Foundations of taxation law 2016. OUP Catalogue.

Brabazon, M. (2019). International Taxation of Trust Income: Principles, Planning and

Design. Cambridge University Press.

Braithwaite, V., & Reinhart, M. (2019). The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research

School of Social Sciences, The Australian National University.

Burton, H.A. & Karlinsky, S., 2016. Tax professionals' perception of large and mid-size

business US tax law complexity. eJTR, 14, p.61.

Butler, D. (2019). Who can provide taxation advice?. Taxation in Australia, 53(7), 381.

Chardon, T., Freudenberg, B., & Brimble, M. (2016). Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, 321.

Evans, C., Minas, J., & Lim, Y. (2015). Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, 735.

Freudenberg, B., Chardon, T., Brimble, M., & Isle, M. B. (2017). Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, 21.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., & Castelyn, D. (2018). Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, 307.

References:

Bankman, J., Shaviro, D. N., Stark, K. J., & Kleinbard, E. D. (2018). Federal Income

Taxation. Aspen Publishers.

Barkoczy, S. (2016). Foundations of taxation law 2016. OUP Catalogue.

Brabazon, M. (2019). International Taxation of Trust Income: Principles, Planning and

Design. Cambridge University Press.

Braithwaite, V., & Reinhart, M. (2019). The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research

School of Social Sciences, The Australian National University.

Burton, H.A. & Karlinsky, S., 2016. Tax professionals' perception of large and mid-size

business US tax law complexity. eJTR, 14, p.61.

Butler, D. (2019). Who can provide taxation advice?. Taxation in Australia, 53(7), 381.

Chardon, T., Freudenberg, B., & Brimble, M. (2016). Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, 321.

Evans, C., Minas, J., & Lim, Y. (2015). Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, 735.

Freudenberg, B., Chardon, T., Brimble, M., & Isle, M. B. (2017). Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, 21.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., & Castelyn, D. (2018). Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, 307.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13TAXATION LAW

Morgan, A., Mortimer, C., & Pinto, D. (2018). A practical introduction to Australian

taxation law 2018. Oxford University Press.

Murray, I., Taylor, J., Walpole, M., Burton, M., & Ciro, T. (2018). Understanding Taxation

Law 2019.

Pert, A., Chen, H., & Carvosso, R. (2018). 'Federal Commissioner of Taxation v

Jayasinghe'(2016) 247 FCR 40. Australian Year Book of International Law, 35, 260.

Qureshi, A. H., & Kumar, A. (2019). The public international law of taxation: text, cases and

materials. Kluwer Law International BV.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). (2019). Australian

Taxation Law Select 2019: Legislation And Commentary. Oxford University Press.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Sadiq, K. (2019). Australian Taxation Law Cases 2019. Thomson Reuters.

Thuronyi, V., & Brooks, K. (2016). Comparative tax law. Kluwer Law International BV.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

Morgan, A., Mortimer, C., & Pinto, D. (2018). A practical introduction to Australian

taxation law 2018. Oxford University Press.

Murray, I., Taylor, J., Walpole, M., Burton, M., & Ciro, T. (2018). Understanding Taxation

Law 2019.

Pert, A., Chen, H., & Carvosso, R. (2018). 'Federal Commissioner of Taxation v

Jayasinghe'(2016) 247 FCR 40. Australian Year Book of International Law, 35, 260.

Qureshi, A. H., & Kumar, A. (2019). The public international law of taxation: text, cases and

materials. Kluwer Law International BV.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). (2019). Australian

Taxation Law Select 2019: Legislation And Commentary. Oxford University Press.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Sadiq, K. (2019). Australian Taxation Law Cases 2019. Thomson Reuters.

Thuronyi, V., & Brooks, K. (2016). Comparative tax law. Kluwer Law International BV.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.