Taxation Law Assignment: CGT, GST, and Taxation Principles Review

VerifiedAdded on 2022/10/15

|13

|2814

|211

Homework Assignment

AI Summary

This Taxation Law assignment addresses two key questions related to Australian taxation. The first question examines the input tax credit availability for a construction and investment company, focusing on the purchase of vacant land and the use of legal services, applying GST legislation to determine creditable acquisitions. The second question delves into capital gains tax (CGT) implications, analyzing the sale of investment land, shares, a stamp collection, and a piano, with detailed calculations of cost base and application of CGT rules for each asset. The assignment covers relevant sections of the GST Act 1999 and ITAA 1997, providing a comprehensive analysis of taxation principles and their practical application in various scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

The primary matter that will be dealt in this questions is the input tax credit

availability that can be claimed by City Sky Co in regard to the acquisition made.

Laws:

The GST has been introduced as the part of the new tax system by the government.

Usually there are three forms of supplies (Richard 2014). This includes the taxable supplies,

GST-Free supplies and input tax supplies. GST is generally referred as the transaction based

tax. The elements of the transactions generally include the following;

a. Supplier: This includes those that provides the subject matter of supply

b. Recipient: This includes those that obtains the supply and pays the price in

consideration of the supply.

Notably in “sec 9-40” and “sec 13-15, GST Act 1997”, it is understood that the

liability for GST happens when any assessable supply or importation is made by the taxpayer

(Dootson and Suzor 2015). Fundamentally, GST must be viewed as the tax on consumption.

GST is imposed on the sale of goods and services made inside Australia and on goods that

are imported to Australia. GST is usually paid on the value of added to the assessable supply.

Under “sec 9-10, GST Act 1999”, it says that supply is regarded as any type of supply that

includes the goods and services (Jacob 2015). It also includes the provision of advice or

information, financial supply, surrender of real property, or surrender of any right. “Sec 9-5,

GST Act 1999” says that GST is levied on the assessable supply. A taxpayer may make the

assessable supply if;

a. There is any kind of supply

Answer to question 1:

Issues:

The primary matter that will be dealt in this questions is the input tax credit

availability that can be claimed by City Sky Co in regard to the acquisition made.

Laws:

The GST has been introduced as the part of the new tax system by the government.

Usually there are three forms of supplies (Richard 2014). This includes the taxable supplies,

GST-Free supplies and input tax supplies. GST is generally referred as the transaction based

tax. The elements of the transactions generally include the following;

a. Supplier: This includes those that provides the subject matter of supply

b. Recipient: This includes those that obtains the supply and pays the price in

consideration of the supply.

Notably in “sec 9-40” and “sec 13-15, GST Act 1997”, it is understood that the

liability for GST happens when any assessable supply or importation is made by the taxpayer

(Dootson and Suzor 2015). Fundamentally, GST must be viewed as the tax on consumption.

GST is imposed on the sale of goods and services made inside Australia and on goods that

are imported to Australia. GST is usually paid on the value of added to the assessable supply.

Under “sec 9-10, GST Act 1999”, it says that supply is regarded as any type of supply that

includes the goods and services (Jacob 2015). It also includes the provision of advice or

information, financial supply, surrender of real property, or surrender of any right. “Sec 9-5,

GST Act 1999” says that GST is levied on the assessable supply. A taxpayer may make the

assessable supply if;

a. There is any kind of supply

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

b. For consideration

c. During the course of business or progress of the business activities

d. Supplies that are connected with the Australia

e. The taxable supply is made by the registered entity.

On the other hand “sec 11-5”, elucidates that creditable acquisition represents those

acquisition of items that are by taxpayer with the creditable intention (Wiese 2015). When a

company acquires any item that is for the business course of the company then those

acquisitions are viewed as having creditable purpose. A business makes creditable acquisition

provided that the item acquired is;

a. Purchased anything that is absolutely for business purpose

b. The supply of thing to business is regarded as the assessable supply

c. The business is under obligation of providing consideration for supply

d. The business is under obligation of registering for GST or it is registered for GST.

Under “sec 11-15 (1), GST Act 1999” a business is only permitted to get input tax

credit when it purchases anything for the creditable purpose up to the extent that they acquire

it in conducting the enterprise activities (Richards 2015). The ATO has elucidated that when

a taxpayer purchases land it is generally held as the capital asset which may attract capital

gains tax when it is sold. However, when a taxpayer purchases land for making business use

or for making profit, sales proceeds that is earned is held as ordinary earnings and the

business may be required to register for GST.

Additionally, there could few conditions where the GST is required to be paid by

purchaser. This type of situation is known as reverse charge. Things apart from the GST will

be held subject to GST when the Australian business purchases them and things are made

through the business which is carried on by the seller out of Australia (Krever 2015). Under

b. For consideration

c. During the course of business or progress of the business activities

d. Supplies that are connected with the Australia

e. The taxable supply is made by the registered entity.

On the other hand “sec 11-5”, elucidates that creditable acquisition represents those

acquisition of items that are by taxpayer with the creditable intention (Wiese 2015). When a

company acquires any item that is for the business course of the company then those

acquisitions are viewed as having creditable purpose. A business makes creditable acquisition

provided that the item acquired is;

a. Purchased anything that is absolutely for business purpose

b. The supply of thing to business is regarded as the assessable supply

c. The business is under obligation of providing consideration for supply

d. The business is under obligation of registering for GST or it is registered for GST.

Under “sec 11-15 (1), GST Act 1999” a business is only permitted to get input tax

credit when it purchases anything for the creditable purpose up to the extent that they acquire

it in conducting the enterprise activities (Richards 2015). The ATO has elucidated that when

a taxpayer purchases land it is generally held as the capital asset which may attract capital

gains tax when it is sold. However, when a taxpayer purchases land for making business use

or for making profit, sales proceeds that is earned is held as ordinary earnings and the

business may be required to register for GST.

Additionally, there could few conditions where the GST is required to be paid by

purchaser. This type of situation is known as reverse charge. Things apart from the GST will

be held subject to GST when the Australian business purchases them and things are made

through the business which is carried on by the seller out of Australia (Krever 2015). Under

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

such kind of situation, the taxpayer will be considered as liable for paying the GST even after

the fact that the taxpayer is purchaser and even though the seller is not under obligation of

paying GST on sale. The reverse charge mechanism is generally applied on the purchases that

is made by an enterprise for the business purpose and the entity is registered for GST.

Application:

The City Sky Co is the GST registered investment and construction development

company. The company purchased a vacant property for construction of building apartments

for selling it again. It can be stated that land purchased by City Sky Co is regarded as the

CGT asset and the land here will not be regarded as falling inside the domain of GST. City

Sky Co must note that its land does not attracts any GST in this situation.

The case facts obtained also suggest that City Sky Co is planning to construct fifteen

apartments on the vacant land. The land here further falls under the provision of black credit

(Phillip 2015). This is because the vacant land that is purchased by City Sky Co is for the

construction purpose. The land here is regarded as the immovable property which is mainly

acquired for furthering the business and hence it is not eligible for claiming input tax credit in

this regard.

The company has also engaged with the local lawyer for its service for developmental

purpose. City Sky Co. incurred $33,000 for the legal services. The legal expenses occurred

here will be eligible for reverse charge mechanism (Joanna 2015). Here, the service receiver

is City Sky Co and Maurice being the seller. As the company here is regarded as the

development company since the services here amounts to creditable acquisition under “sec

11-5” which is solely acquired for business purpose of City Sky Co. Therefore, the company

is eligible for claiming input tax credit relating to its legal service that is availed from the

Maurice Blackburn.

such kind of situation, the taxpayer will be considered as liable for paying the GST even after

the fact that the taxpayer is purchaser and even though the seller is not under obligation of

paying GST on sale. The reverse charge mechanism is generally applied on the purchases that

is made by an enterprise for the business purpose and the entity is registered for GST.

Application:

The City Sky Co is the GST registered investment and construction development

company. The company purchased a vacant property for construction of building apartments

for selling it again. It can be stated that land purchased by City Sky Co is regarded as the

CGT asset and the land here will not be regarded as falling inside the domain of GST. City

Sky Co must note that its land does not attracts any GST in this situation.

The case facts obtained also suggest that City Sky Co is planning to construct fifteen

apartments on the vacant land. The land here further falls under the provision of black credit

(Phillip 2015). This is because the vacant land that is purchased by City Sky Co is for the

construction purpose. The land here is regarded as the immovable property which is mainly

acquired for furthering the business and hence it is not eligible for claiming input tax credit in

this regard.

The company has also engaged with the local lawyer for its service for developmental

purpose. City Sky Co. incurred $33,000 for the legal services. The legal expenses occurred

here will be eligible for reverse charge mechanism (Joanna 2015). Here, the service receiver

is City Sky Co and Maurice being the seller. As the company here is regarded as the

development company since the services here amounts to creditable acquisition under “sec

11-5” which is solely acquired for business purpose of City Sky Co. Therefore, the company

is eligible for claiming input tax credit relating to its legal service that is availed from the

Maurice Blackburn.

5TAXATION LAW

Conclusion:

The study here can be concluded by stating that the vacant land amounts to CGT asset

and does not attracts GST. While the legal services availed from Maurice Blackburn will be

considered eligible for input tax credit because it was solely sought for business purpose.

Answer to question 2:

Sale of block of land:

In order to raise the CGT liability there must be two conditions that should be satisfied;

a. There should be a CGT-Asset and the asset must be purchased on or following

20/09/1985

b. There should also be a CGT event under “sec (104-5)”. For example, sale of CGT

asset under “CGT event A1”.

The taxpayers must note under “sec 104-10(5)(a), ITAA 1997” that capital gains or loss

must be ignored if the CGT asset is purchased prior to 20/9/1985 (Phan 2016). As the general

rule of CGT if the amount is categorized as ordinary and statutory income, then such amount

must be included in assessable income of the taxpayer under the rules of statutory income.

Under “s.104-10(4), ITAA 1997” The proceeds obtained from the sale of asset is compared

with the cost base of the asset (Armstrong 2016). To determine the CGT it is necessary to

understand the cost base of the CGT assets. Usually, there are five elements of cost base.

These includes

Conclusion:

The study here can be concluded by stating that the vacant land amounts to CGT asset

and does not attracts GST. While the legal services availed from Maurice Blackburn will be

considered eligible for input tax credit because it was solely sought for business purpose.

Answer to question 2:

Sale of block of land:

In order to raise the CGT liability there must be two conditions that should be satisfied;

a. There should be a CGT-Asset and the asset must be purchased on or following

20/09/1985

b. There should also be a CGT event under “sec (104-5)”. For example, sale of CGT

asset under “CGT event A1”.

The taxpayers must note under “sec 104-10(5)(a), ITAA 1997” that capital gains or loss

must be ignored if the CGT asset is purchased prior to 20/9/1985 (Phan 2016). As the general

rule of CGT if the amount is categorized as ordinary and statutory income, then such amount

must be included in assessable income of the taxpayer under the rules of statutory income.

Under “s.104-10(4), ITAA 1997” The proceeds obtained from the sale of asset is compared

with the cost base of the asset (Armstrong 2016). To determine the CGT it is necessary to

understand the cost base of the CGT assets. Usually, there are five elements of cost base.

These includes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

1. Element 1: Under “sec 110-25 (2), ITAA 1997” money that is paid or need to be paid

for acquiring the CGT asset and the market value of any other property that is paid for

purchasing the asset.

2. Element 2: This element is concerned with the incidental cost of acquisition and sale

of CGT asset under “sec 110-25 (3), ITA Act 97” (Mahar 2016). This element

generally includes the agents commission, stamp duty expense, legal expenses, tax

advisor expense or advertisement expenses occurred by taxpayer for purchasing the

asset.

3. Element 3: Under “sec 110-25 (4), ITAA 1997” this element is associated with the

non-capital cost that is related with owning the asset which does not qualifies for

deduction. This includes the rates, land taxes, insurances, interest money borrowed for

acquiring the asset etc. This is usually applicable on assets which is purchased

following 21 August 1991.

4. Element 4: Expenses that is occurred increasing the CGT asset value under “sec 110-

25 (5), ITA Act 1997” is regarded as capital improvement cost. Examples of the cost

include the renovations, extensions etc.

5. Element 5: This element includes the expenses that is occurred for capital

expenditure purpose such as expenses incurred in defending or preserving the title

rights to the CGT-asset under “sec 110-25 (6), ITAA 1997”.

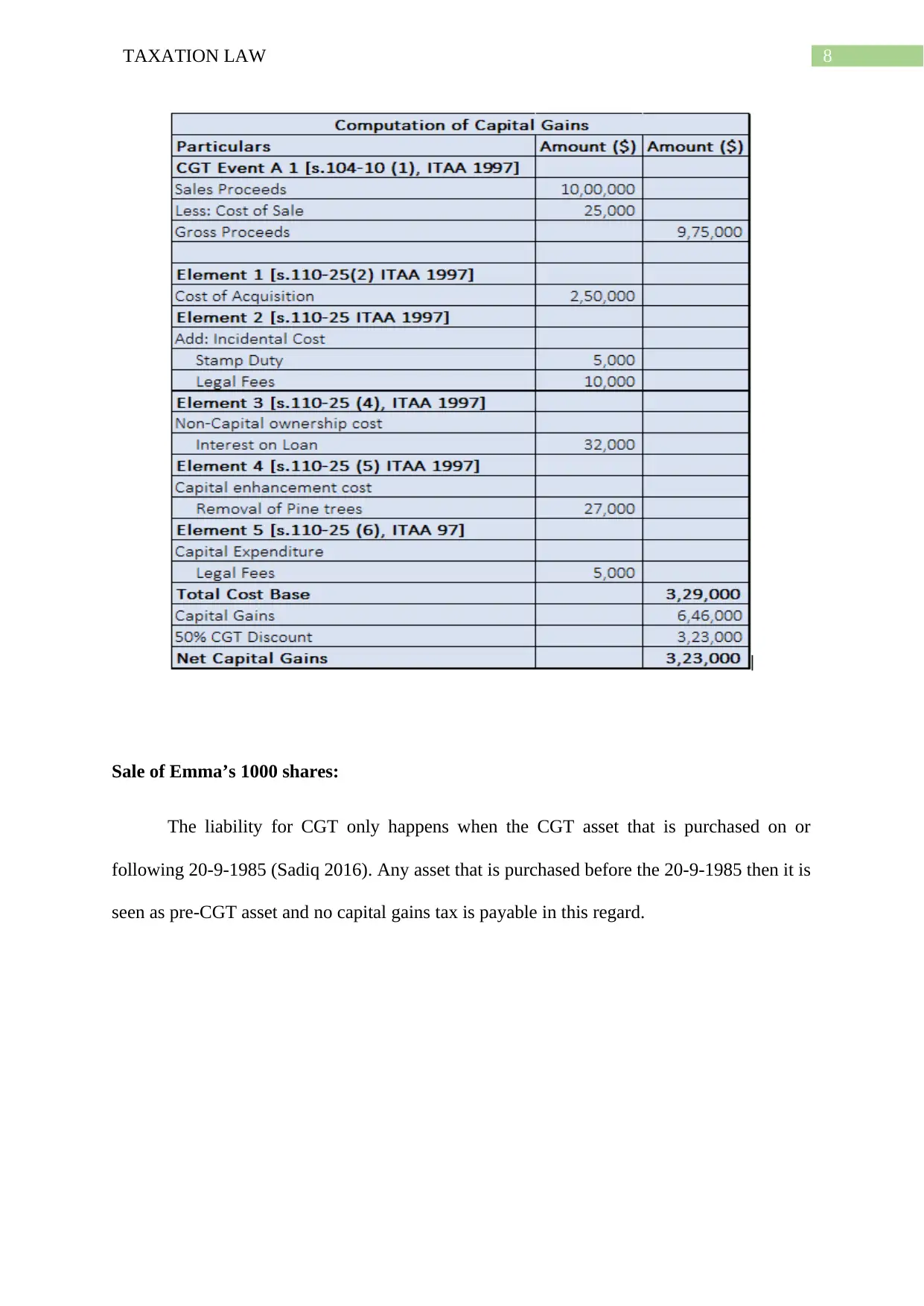

In the current case Emma being the owner of investment land bought in 1991 for

$250,000 was eventually sold for $1,000,000. Prior to making the sale of property there were

several expenses incurred by Emma. The purchase price paid for acquiring the asset is

included under the Element 1 of “sec 110-25 (2), ITA Act 1997” since it represents the

money paid by her to purchase the asset (Ingram 2016). Emma further incurred outgoings on

1. Element 1: Under “sec 110-25 (2), ITAA 1997” money that is paid or need to be paid

for acquiring the CGT asset and the market value of any other property that is paid for

purchasing the asset.

2. Element 2: This element is concerned with the incidental cost of acquisition and sale

of CGT asset under “sec 110-25 (3), ITA Act 97” (Mahar 2016). This element

generally includes the agents commission, stamp duty expense, legal expenses, tax

advisor expense or advertisement expenses occurred by taxpayer for purchasing the

asset.

3. Element 3: Under “sec 110-25 (4), ITAA 1997” this element is associated with the

non-capital cost that is related with owning the asset which does not qualifies for

deduction. This includes the rates, land taxes, insurances, interest money borrowed for

acquiring the asset etc. This is usually applicable on assets which is purchased

following 21 August 1991.

4. Element 4: Expenses that is occurred increasing the CGT asset value under “sec 110-

25 (5), ITA Act 1997” is regarded as capital improvement cost. Examples of the cost

include the renovations, extensions etc.

5. Element 5: This element includes the expenses that is occurred for capital

expenditure purpose such as expenses incurred in defending or preserving the title

rights to the CGT-asset under “sec 110-25 (6), ITAA 1997”.

In the current case Emma being the owner of investment land bought in 1991 for

$250,000 was eventually sold for $1,000,000. Prior to making the sale of property there were

several expenses incurred by Emma. The purchase price paid for acquiring the asset is

included under the Element 1 of “sec 110-25 (2), ITA Act 1997” since it represents the

money paid by her to purchase the asset (Ingram 2016). Emma further incurred outgoings on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

stamp duty and legal fees. These expenses are classified as incidental cost under “sec 110-25

(3)” and it is included under second element of cost base of land.

An interest on loan was occurred by Emma that amounted to $32,000 for the land.

Additionally, Emma further occurred expenses on council rates, insurance and water rates.

The interest amount paid for borrowed money along with council rates, water and insurance

expenses is regarded as the non-capital cost. Under “sec 110-25 (4), ITA Act 1997” these

expenses will be included under the third element cost base of land.

Emma also reported a sum of $5,000 on settling the dispute with the neighbour over

the land use. These expense should be viewed as capital expense for Emma under “sec 110-

25 (6) ITA Act 1997” because the expenses were incurred in defending the title to the CGT

asset. The amount will be included in fifth element cost base of the land.

Meanwhile, Emma also paid $25,000 for clearing the hazardous pine trees that were

on the land. These expenses will be viewed as capital improvement cost under “sec 110-25

(5)”, occurred mainly by Emma for improving the value of land. The land clearing expense

will be included in fourth element cost base.

stamp duty and legal fees. These expenses are classified as incidental cost under “sec 110-25

(3)” and it is included under second element of cost base of land.

An interest on loan was occurred by Emma that amounted to $32,000 for the land.

Additionally, Emma further occurred expenses on council rates, insurance and water rates.

The interest amount paid for borrowed money along with council rates, water and insurance

expenses is regarded as the non-capital cost. Under “sec 110-25 (4), ITA Act 1997” these

expenses will be included under the third element cost base of land.

Emma also reported a sum of $5,000 on settling the dispute with the neighbour over

the land use. These expense should be viewed as capital expense for Emma under “sec 110-

25 (6) ITA Act 1997” because the expenses were incurred in defending the title to the CGT

asset. The amount will be included in fifth element cost base of the land.

Meanwhile, Emma also paid $25,000 for clearing the hazardous pine trees that were

on the land. These expenses will be viewed as capital improvement cost under “sec 110-25

(5)”, occurred mainly by Emma for improving the value of land. The land clearing expense

will be included in fourth element cost base.

8TAXATION LAW

Sale of Emma’s 1000 shares:

The liability for CGT only happens when the CGT asset that is purchased on or

following 20-9-1985 (Sadiq 2016). Any asset that is purchased before the 20-9-1985 then it is

seen as pre-CGT asset and no capital gains tax is payable in this regard.

Sale of Emma’s 1000 shares:

The liability for CGT only happens when the CGT asset that is purchased on or

following 20-9-1985 (Sadiq 2016). Any asset that is purchased before the 20-9-1985 then it is

seen as pre-CGT asset and no capital gains tax is payable in this regard.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

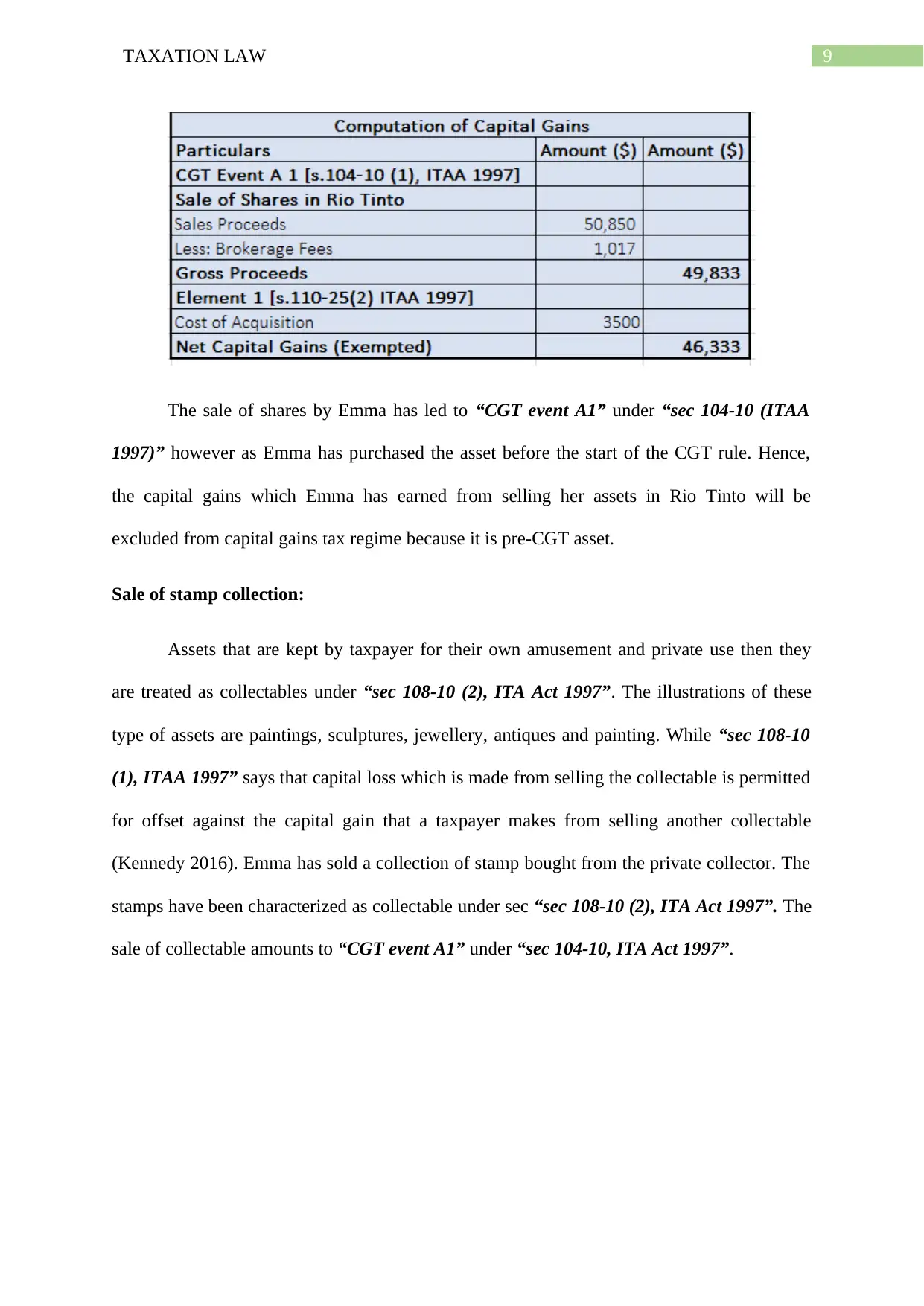

The sale of shares by Emma has led to “CGT event A1” under “sec 104-10 (ITAA

1997)” however as Emma has purchased the asset before the start of the CGT rule. Hence,

the capital gains which Emma has earned from selling her assets in Rio Tinto will be

excluded from capital gains tax regime because it is pre-CGT asset.

Sale of stamp collection:

Assets that are kept by taxpayer for their own amusement and private use then they

are treated as collectables under “sec 108-10 (2), ITA Act 1997”. The illustrations of these

type of assets are paintings, sculptures, jewellery, antiques and painting. While “sec 108-10

(1), ITAA 1997” says that capital loss which is made from selling the collectable is permitted

for offset against the capital gain that a taxpayer makes from selling another collectable

(Kennedy 2016). Emma has sold a collection of stamp bought from the private collector. The

stamps have been characterized as collectable under sec “sec 108-10 (2), ITA Act 1997”. The

sale of collectable amounts to “CGT event A1” under “sec 104-10, ITA Act 1997”.

The sale of shares by Emma has led to “CGT event A1” under “sec 104-10 (ITAA

1997)” however as Emma has purchased the asset before the start of the CGT rule. Hence,

the capital gains which Emma has earned from selling her assets in Rio Tinto will be

excluded from capital gains tax regime because it is pre-CGT asset.

Sale of stamp collection:

Assets that are kept by taxpayer for their own amusement and private use then they

are treated as collectables under “sec 108-10 (2), ITA Act 1997”. The illustrations of these

type of assets are paintings, sculptures, jewellery, antiques and painting. While “sec 108-10

(1), ITAA 1997” says that capital loss which is made from selling the collectable is permitted

for offset against the capital gain that a taxpayer makes from selling another collectable

(Kennedy 2016). Emma has sold a collection of stamp bought from the private collector. The

stamps have been characterized as collectable under sec “sec 108-10 (2), ITA Act 1997”. The

sale of collectable amounts to “CGT event A1” under “sec 104-10, ITA Act 1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

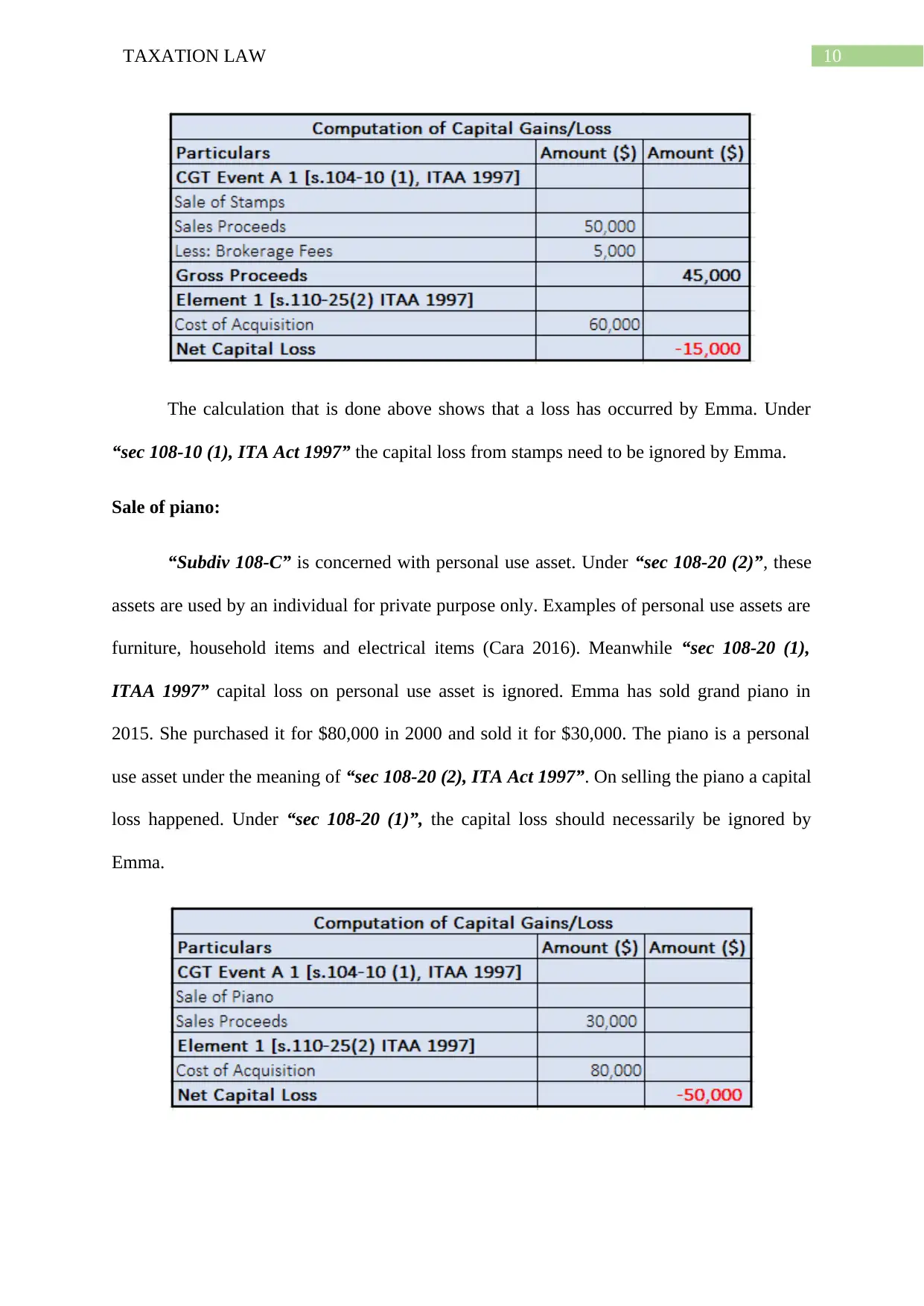

The calculation that is done above shows that a loss has occurred by Emma. Under

“sec 108-10 (1), ITA Act 1997” the capital loss from stamps need to be ignored by Emma.

Sale of piano:

“Subdiv 108-C” is concerned with personal use asset. Under “sec 108-20 (2)”, these

assets are used by an individual for private purpose only. Examples of personal use assets are

furniture, household items and electrical items (Cara 2016). Meanwhile “sec 108-20 (1),

ITAA 1997” capital loss on personal use asset is ignored. Emma has sold grand piano in

2015. She purchased it for $80,000 in 2000 and sold it for $30,000. The piano is a personal

use asset under the meaning of “sec 108-20 (2), ITA Act 1997”. On selling the piano a capital

loss happened. Under “sec 108-20 (1)”, the capital loss should necessarily be ignored by

Emma.

The calculation that is done above shows that a loss has occurred by Emma. Under

“sec 108-10 (1), ITA Act 1997” the capital loss from stamps need to be ignored by Emma.

Sale of piano:

“Subdiv 108-C” is concerned with personal use asset. Under “sec 108-20 (2)”, these

assets are used by an individual for private purpose only. Examples of personal use assets are

furniture, household items and electrical items (Cara 2016). Meanwhile “sec 108-20 (1),

ITAA 1997” capital loss on personal use asset is ignored. Emma has sold grand piano in

2015. She purchased it for $80,000 in 2000 and sold it for $30,000. The piano is a personal

use asset under the meaning of “sec 108-20 (2), ITA Act 1997”. On selling the piano a capital

loss happened. Under “sec 108-20 (1)”, the capital loss should necessarily be ignored by

Emma.

11TAXATION LAW

References:

Armstrong, M., 2016. CGT withholding on real estate transactions in Australia. Mondaq

Business Briefing, pp.Mondaq Business Briefing, March 11, 2016.

Cara W, 2016. Tax breaks on super, capital gains cost $380 billion. The Sydney Morning

Herald (Sydney, Australia), p.11.

Dootson, P and Suzor, N, 2015. The game of clones and the Australia tax: Divergent views

about copyright business models and the willingness of Australian consumers to infringe.

University of New South Wales Law Journal, The, 38(1), pp.206–239.

Ingram, P, 2016. Tax files: More than meets the eye - the new 'foreign resident capital gains

tax withholding regime'. Bulletin (Law Society of South Australia), 38(5), pp.36–37.

Jacob G, 2015. GST reform inevitable: CPD group. , pp.Australasian Business Intelligence,

April 13, 2015.

Joanna M, 2015. Revamp vital for revenue raising. , pp.Australasian Business Intelligence,

March 5, 2015.

Kennedy, A., 2016. New regime for withholding CGT when purchasing Australian land.

Mondaq Business Briefing, pp.Mondaq Business Briefing, Feb 8, 2016.

Krever, R, 2015. GST and death: the puzzle is missing some pieces.(Goods and Service Tax)

(Brief Article). Australasian Business Intelligence, pp.Australasian Business Intelligence,

March 23, 2015.

Mahar, F, 2016. The distortive effects of the capital gains tax regime. Tax Specialist, 20(1),

pp.16–20.

References:

Armstrong, M., 2016. CGT withholding on real estate transactions in Australia. Mondaq

Business Briefing, pp.Mondaq Business Briefing, March 11, 2016.

Cara W, 2016. Tax breaks on super, capital gains cost $380 billion. The Sydney Morning

Herald (Sydney, Australia), p.11.

Dootson, P and Suzor, N, 2015. The game of clones and the Australia tax: Divergent views

about copyright business models and the willingness of Australian consumers to infringe.

University of New South Wales Law Journal, The, 38(1), pp.206–239.

Ingram, P, 2016. Tax files: More than meets the eye - the new 'foreign resident capital gains

tax withholding regime'. Bulletin (Law Society of South Australia), 38(5), pp.36–37.

Jacob G, 2015. GST reform inevitable: CPD group. , pp.Australasian Business Intelligence,

April 13, 2015.

Joanna M, 2015. Revamp vital for revenue raising. , pp.Australasian Business Intelligence,

March 5, 2015.

Kennedy, A., 2016. New regime for withholding CGT when purchasing Australian land.

Mondaq Business Briefing, pp.Mondaq Business Briefing, Feb 8, 2016.

Krever, R, 2015. GST and death: the puzzle is missing some pieces.(Goods and Service Tax)

(Brief Article). Australasian Business Intelligence, pp.Australasian Business Intelligence,

March 23, 2015.

Mahar, F, 2016. The distortive effects of the capital gains tax regime. Tax Specialist, 20(1),

pp.16–20.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.