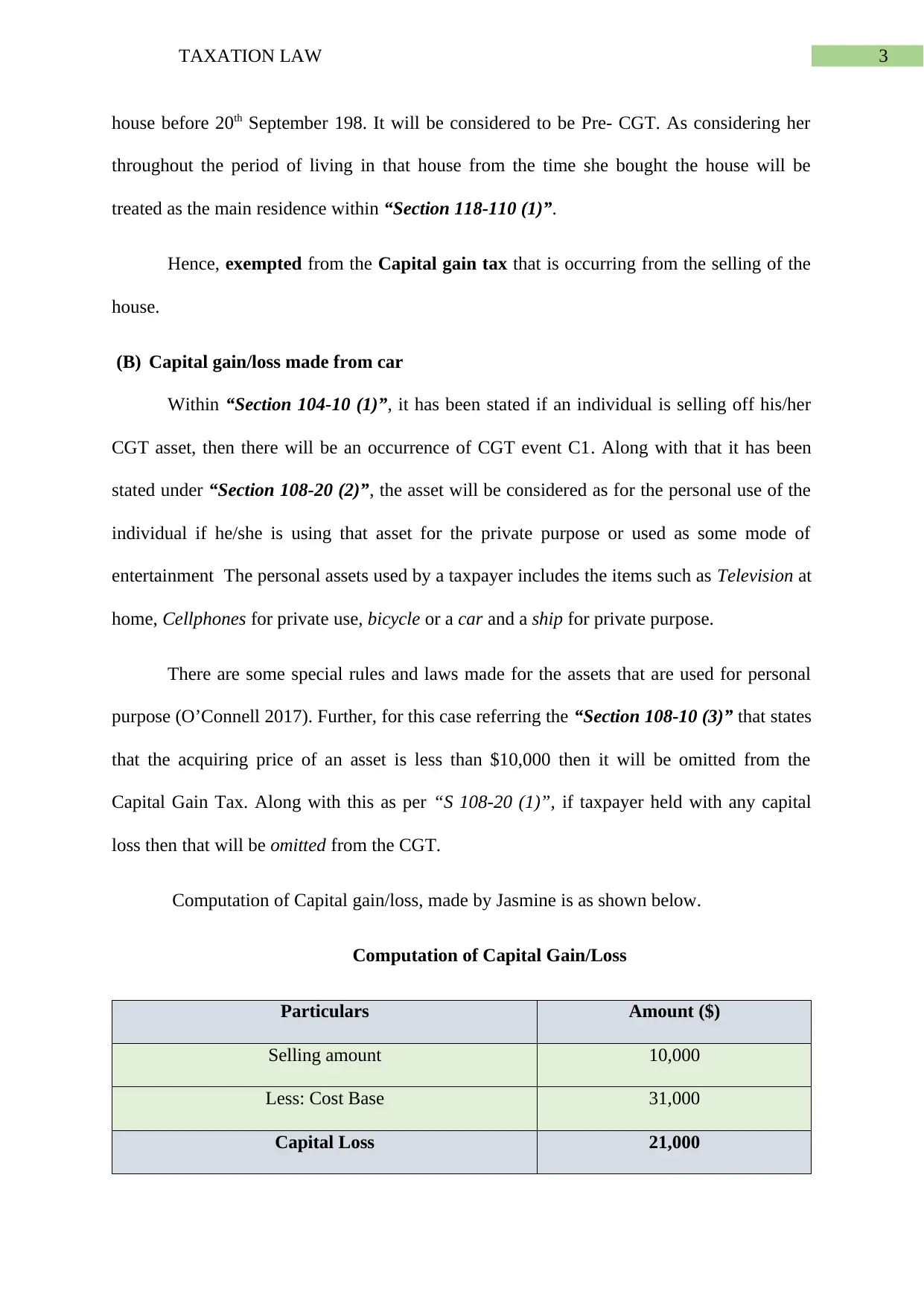

Taxation Law Assignment - Holmes Institute HA3042, T2 2019: Analysis

VerifiedAdded on 2022/11/09

|15

|3315

|337

Homework Assignment

AI Summary

This assignment delves into the intricacies of Australian taxation law, specifically focusing on capital gains tax (CGT) and capital allowances. The assignment presents a case study involving a 65-year-old Australian resident, Jasmine, who is selling various assets, including her family home, a car, a cleaning business, furniture, and paintings. The solution analyzes the CGT implications of each asset sale, considering pre-CGT rules, personal use assets, small business concessions, and collectables. Additionally, the assignment explores capital allowances, using a scenario involving a manufacturing company that has purchased an industrial CNC machine. The solution examines the relevant legislation and applies it to determine the appropriate tax deductions for the depreciation of the machine and associated costs.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Author Note

Taxation Law

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer 1: Capital Gains Tax.........................................................................................2

(A) The Capital gain related to the Family Home..................................................2

(B) Capital gain/loss made from car.......................................................................3

The Capital gain in relation to:...................................................................................4

(C) The Sale of Business........................................................................................4

(D) Selling the Furniture.........................................................................................5

(E) Selling the Paintings.........................................................................................6

Answer 2: Capital Allowance........................................................................................7

Identification of Issues.....................................................................................7

Laws.................................................................................................................7

Application.......................................................................................................8

Conclusion....................................................................................................................10

References....................................................................................................................11

Table of Contents

Answer 1: Capital Gains Tax.........................................................................................2

(A) The Capital gain related to the Family Home..................................................2

(B) Capital gain/loss made from car.......................................................................3

The Capital gain in relation to:...................................................................................4

(C) The Sale of Business........................................................................................4

(D) Selling the Furniture.........................................................................................5

(E) Selling the Paintings.........................................................................................6

Answer 2: Capital Allowance........................................................................................7

Identification of Issues.....................................................................................7

Laws.................................................................................................................7

Application.......................................................................................................8

Conclusion....................................................................................................................10

References....................................................................................................................11

2TAXATION LAW

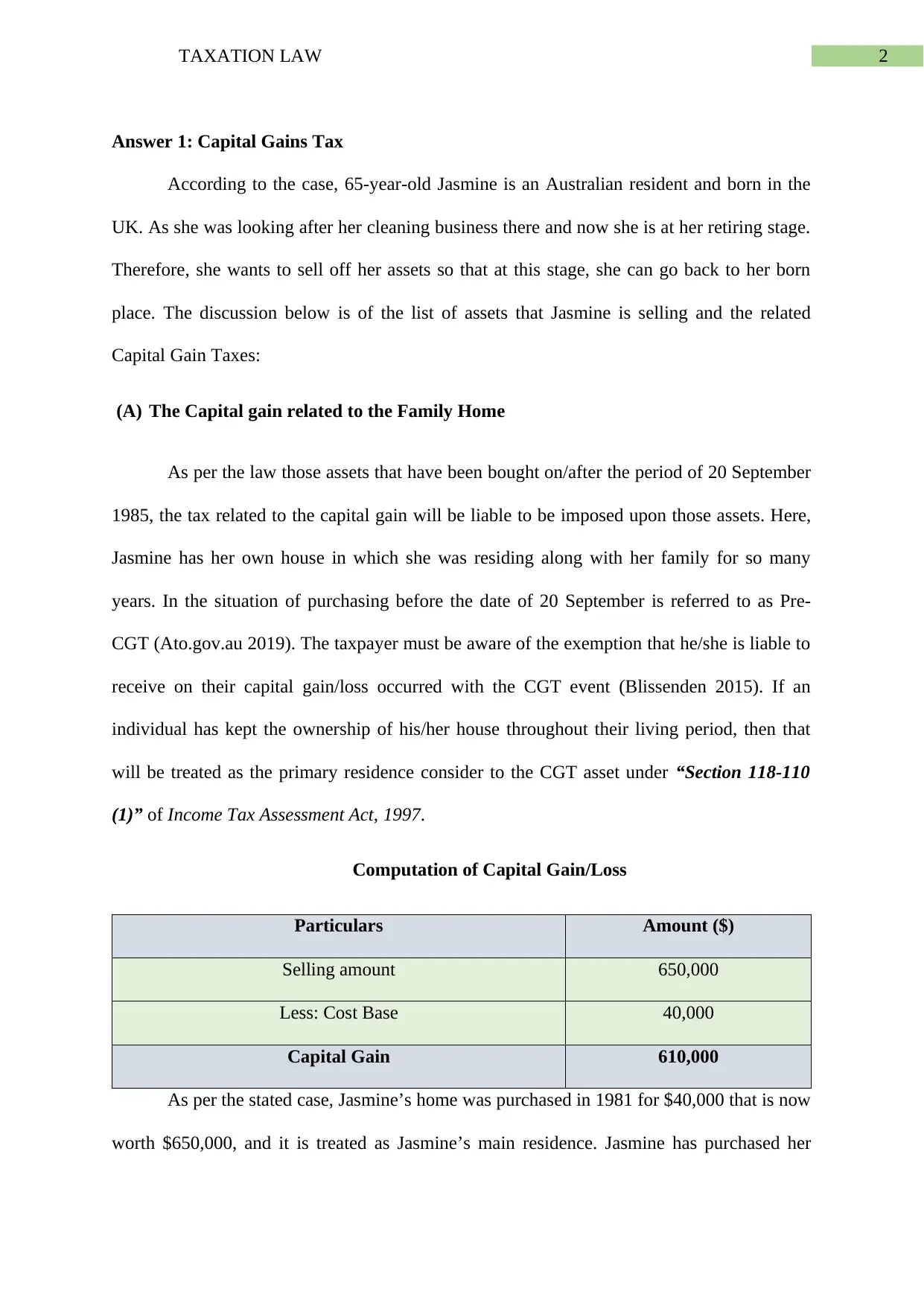

Answer 1: Capital Gains Tax

According to the case, 65-year-old Jasmine is an Australian resident and born in the

UK. As she was looking after her cleaning business there and now she is at her retiring stage.

Therefore, she wants to sell off her assets so that at this stage, she can go back to her born

place. The discussion below is of the list of assets that Jasmine is selling and the related

Capital Gain Taxes:

(A) The Capital gain related to the Family Home

As per the law those assets that have been bought on/after the period of 20 September

1985, the tax related to the capital gain will be liable to be imposed upon those assets. Here,

Jasmine has her own house in which she was residing along with her family for so many

years. In the situation of purchasing before the date of 20 September is referred to as Pre-

CGT (Ato.gov.au 2019). The taxpayer must be aware of the exemption that he/she is liable to

receive on their capital gain/loss occurred with the CGT event (Blissenden 2015). If an

individual has kept the ownership of his/her house throughout their living period, then that

will be treated as the primary residence consider to the CGT asset under “Section 118-110

(1)” of Income Tax Assessment Act, 1997.

Computation of Capital Gain/Loss

Particulars Amount ($)

Selling amount 650,000

Less: Cost Base 40,000

Capital Gain 610,000

As per the stated case, Jasmine’s home was purchased in 1981 for $40,000 that is now

worth $650,000, and it is treated as Jasmine’s main residence. Jasmine has purchased her

Answer 1: Capital Gains Tax

According to the case, 65-year-old Jasmine is an Australian resident and born in the

UK. As she was looking after her cleaning business there and now she is at her retiring stage.

Therefore, she wants to sell off her assets so that at this stage, she can go back to her born

place. The discussion below is of the list of assets that Jasmine is selling and the related

Capital Gain Taxes:

(A) The Capital gain related to the Family Home

As per the law those assets that have been bought on/after the period of 20 September

1985, the tax related to the capital gain will be liable to be imposed upon those assets. Here,

Jasmine has her own house in which she was residing along with her family for so many

years. In the situation of purchasing before the date of 20 September is referred to as Pre-

CGT (Ato.gov.au 2019). The taxpayer must be aware of the exemption that he/she is liable to

receive on their capital gain/loss occurred with the CGT event (Blissenden 2015). If an

individual has kept the ownership of his/her house throughout their living period, then that

will be treated as the primary residence consider to the CGT asset under “Section 118-110

(1)” of Income Tax Assessment Act, 1997.

Computation of Capital Gain/Loss

Particulars Amount ($)

Selling amount 650,000

Less: Cost Base 40,000

Capital Gain 610,000

As per the stated case, Jasmine’s home was purchased in 1981 for $40,000 that is now

worth $650,000, and it is treated as Jasmine’s main residence. Jasmine has purchased her

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

house before 20th September 198. It will be considered to be Pre- CGT. As considering her

throughout the period of living in that house from the time she bought the house will be

treated as the main residence within “Section 118-110 (1)”.

Hence, exempted from the Capital gain tax that is occurring from the selling of the

house.

(B) Capital gain/loss made from car

Within “Section 104-10 (1)”, it has been stated if an individual is selling off his/her

CGT asset, then there will be an occurrence of CGT event C1. Along with that it has been

stated under “Section 108-20 (2)”, the asset will be considered as for the personal use of the

individual if he/she is using that asset for the private purpose or used as some mode of

entertainment The personal assets used by a taxpayer includes the items such as Television at

home, Cellphones for private use, bicycle or a car and a ship for private purpose.

There are some special rules and laws made for the assets that are used for personal

purpose (O’Connell 2017). Further, for this case referring the “Section 108-10 (3)” that states

that the acquiring price of an asset is less than $10,000 then it will be omitted from the

Capital Gain Tax. Along with this as per “S 108-20 (1)”, if taxpayer held with any capital

loss then that will be omitted from the CGT.

Computation of Capital gain/loss, made by Jasmine is as shown below.

Computation of Capital Gain/Loss

Particulars Amount ($)

Selling amount 10,000

Less: Cost Base 31,000

Capital Loss 21,000

house before 20th September 198. It will be considered to be Pre- CGT. As considering her

throughout the period of living in that house from the time she bought the house will be

treated as the main residence within “Section 118-110 (1)”.

Hence, exempted from the Capital gain tax that is occurring from the selling of the

house.

(B) Capital gain/loss made from car

Within “Section 104-10 (1)”, it has been stated if an individual is selling off his/her

CGT asset, then there will be an occurrence of CGT event C1. Along with that it has been

stated under “Section 108-20 (2)”, the asset will be considered as for the personal use of the

individual if he/she is using that asset for the private purpose or used as some mode of

entertainment The personal assets used by a taxpayer includes the items such as Television at

home, Cellphones for private use, bicycle or a car and a ship for private purpose.

There are some special rules and laws made for the assets that are used for personal

purpose (O’Connell 2017). Further, for this case referring the “Section 108-10 (3)” that states

that the acquiring price of an asset is less than $10,000 then it will be omitted from the

Capital Gain Tax. Along with this as per “S 108-20 (1)”, if taxpayer held with any capital

loss then that will be omitted from the CGT.

Computation of Capital gain/loss, made by Jasmine is as shown below.

Computation of Capital Gain/Loss

Particulars Amount ($)

Selling amount 10,000

Less: Cost Base 31,000

Capital Loss 21,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

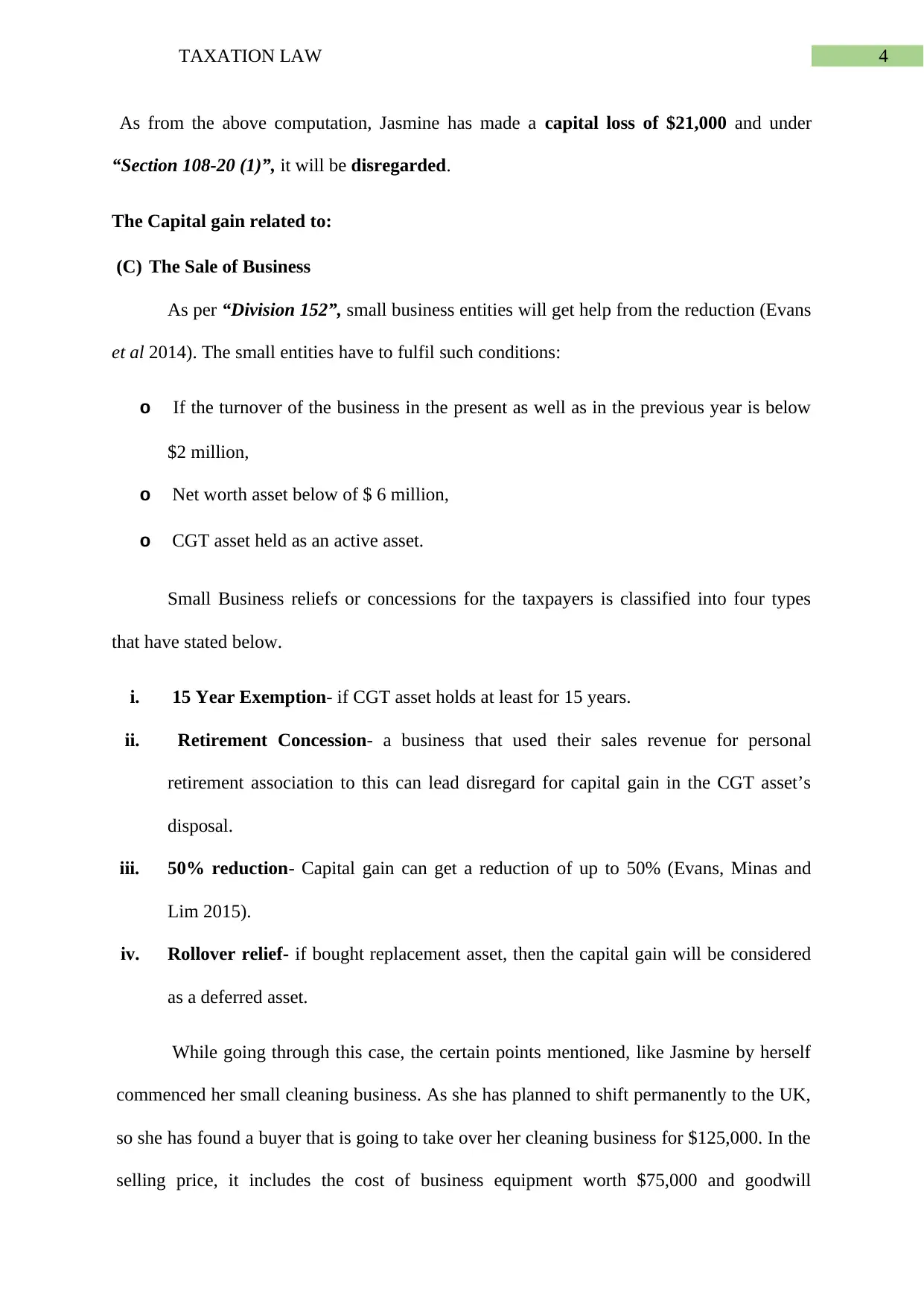

As from the above computation, Jasmine has made a capital loss of $21,000 and under

“Section 108-20 (1)”, it will be disregarded.

The Capital gain related to:

(C) The Sale of Business

As per “Division 152”, small business entities will get help from the reduction (Evans

et al 2014). The small entities have to fulfil such conditions:

o If the turnover of the business in the present as well as in the previous year is below

$2 million,

o Net worth asset below of $ 6 million,

o CGT asset held as an active asset.

Small Business reliefs or concessions for the taxpayers is classified into four types

that have stated below.

i. 15 Year Exemption- if CGT asset holds at least for 15 years.

ii. Retirement Concession- a business that used their sales revenue for personal

retirement association to this can lead disregard for capital gain in the CGT asset’s

disposal.

iii. 50% reduction- Capital gain can get a reduction of up to 50% (Evans, Minas and

Lim 2015).

iv. Rollover relief- if bought replacement asset, then the capital gain will be considered

as a deferred asset.

While going through this case, the certain points mentioned, like Jasmine by herself

commenced her small cleaning business. As she has planned to shift permanently to the UK,

so she has found a buyer that is going to take over her cleaning business for $125,000. In the

selling price, it includes the cost of business equipment worth $75,000 and goodwill

As from the above computation, Jasmine has made a capital loss of $21,000 and under

“Section 108-20 (1)”, it will be disregarded.

The Capital gain related to:

(C) The Sale of Business

As per “Division 152”, small business entities will get help from the reduction (Evans

et al 2014). The small entities have to fulfil such conditions:

o If the turnover of the business in the present as well as in the previous year is below

$2 million,

o Net worth asset below of $ 6 million,

o CGT asset held as an active asset.

Small Business reliefs or concessions for the taxpayers is classified into four types

that have stated below.

i. 15 Year Exemption- if CGT asset holds at least for 15 years.

ii. Retirement Concession- a business that used their sales revenue for personal

retirement association to this can lead disregard for capital gain in the CGT asset’s

disposal.

iii. 50% reduction- Capital gain can get a reduction of up to 50% (Evans, Minas and

Lim 2015).

iv. Rollover relief- if bought replacement asset, then the capital gain will be considered

as a deferred asset.

While going through this case, the certain points mentioned, like Jasmine by herself

commenced her small cleaning business. As she has planned to shift permanently to the UK,

so she has found a buyer that is going to take over her cleaning business for $125,000. In the

selling price, it includes the cost of business equipment worth $75,000 and goodwill

5TAXATION LAW

amounted to $60,000 (Hemmings and Tuske 2015). Jasmine’s Net worth of business assets is

above $6 million that is sold by her. Therefore, Jasmine is liable to get concessions under

“Division 152”.

o Jasmine was residing in Australia for more than 15 years and was busy in her

business. Thus, the assets she is having with her there is also more than 15 years old.

Therefore, she is eligible to get 15 Year deduction for the CGT.

o She is going to shut down her business permanently and moving back to her born

country, UK. Hence, the existence of CGT event F1 with respect to her Goodwill

(O’Connell 2017).

o In the situation of closing of a business (planned or unplanned) if goodwill has to

face any loss, then it comes within “Taxation ruling of TR 1999/16”.

o Jasmine is now at her age of retiring as she has decided to move permanently to the

UK after selling off her assets. In this case, she is eligible to come under

“Subdivision 152-C”. Under this division, she will be liable to get a deduction of

50% on closing her business permanently.

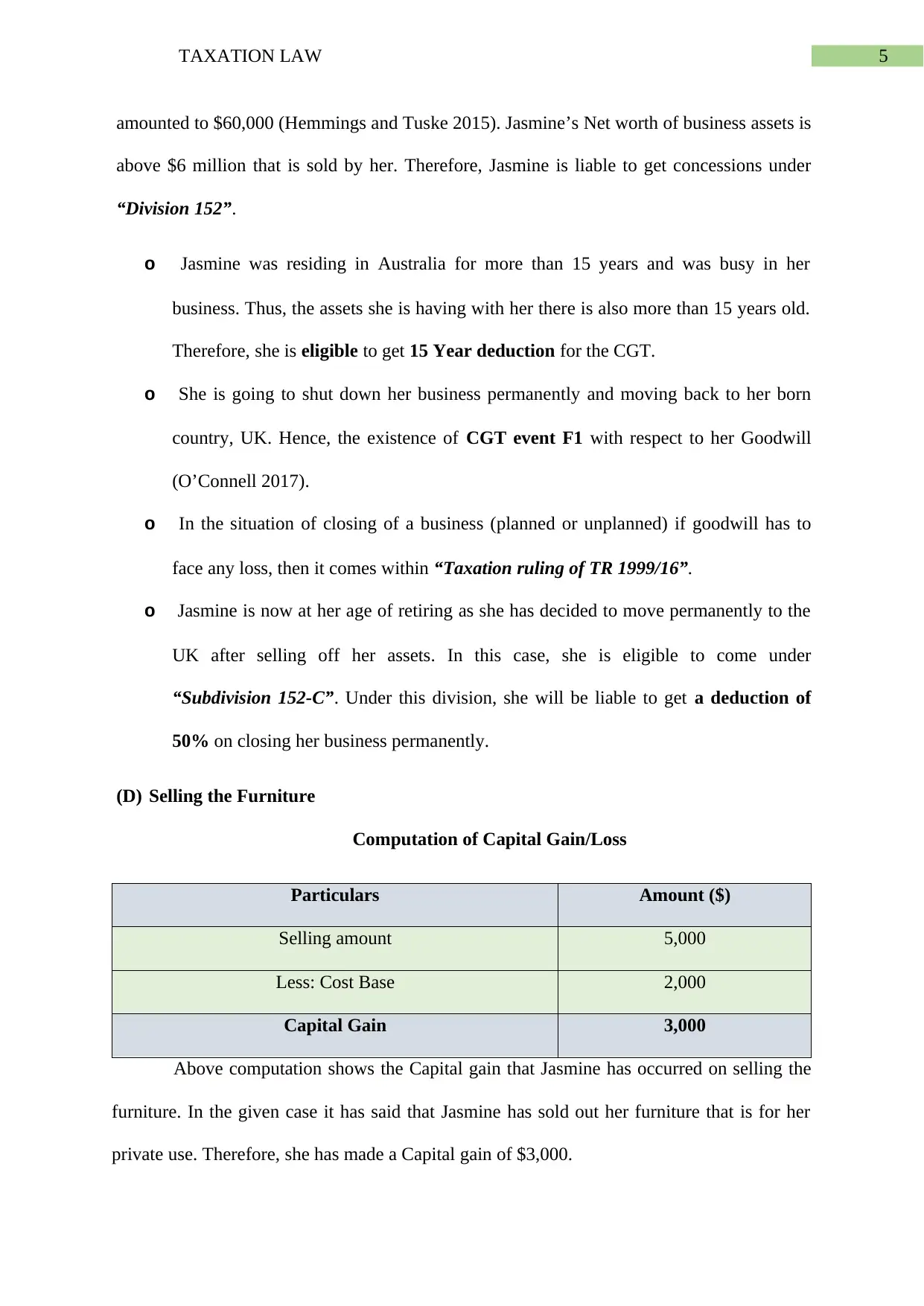

(D) Selling the Furniture

Computation of Capital Gain/Loss

Particulars Amount ($)

Selling amount 5,000

Less: Cost Base 2,000

Capital Gain 3,000

Above computation shows the Capital gain that Jasmine has occurred on selling the

furniture. In the given case it has said that Jasmine has sold out her furniture that is for her

private use. Therefore, she has made a Capital gain of $3,000.

amounted to $60,000 (Hemmings and Tuske 2015). Jasmine’s Net worth of business assets is

above $6 million that is sold by her. Therefore, Jasmine is liable to get concessions under

“Division 152”.

o Jasmine was residing in Australia for more than 15 years and was busy in her

business. Thus, the assets she is having with her there is also more than 15 years old.

Therefore, she is eligible to get 15 Year deduction for the CGT.

o She is going to shut down her business permanently and moving back to her born

country, UK. Hence, the existence of CGT event F1 with respect to her Goodwill

(O’Connell 2017).

o In the situation of closing of a business (planned or unplanned) if goodwill has to

face any loss, then it comes within “Taxation ruling of TR 1999/16”.

o Jasmine is now at her age of retiring as she has decided to move permanently to the

UK after selling off her assets. In this case, she is eligible to come under

“Subdivision 152-C”. Under this division, she will be liable to get a deduction of

50% on closing her business permanently.

(D) Selling the Furniture

Computation of Capital Gain/Loss

Particulars Amount ($)

Selling amount 5,000

Less: Cost Base 2,000

Capital Gain 3,000

Above computation shows the Capital gain that Jasmine has occurred on selling the

furniture. In the given case it has said that Jasmine has sold out her furniture that is for her

private use. Therefore, she has made a Capital gain of $3,000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

As per “Section 118-10 (3)” the asset that is used by the taxpayer for his/her personal

use and bought below $10,000 will be disregarded from Capital gain tax. In this case,

Jasmine has bought the furniture below $10,000 for her private use (O’Connell 2017). Hence,

Capital gain of $3,000 will be disregarded that comes within “section 118-10 (3)”.

(E) Selling the Paintings

According to “Section 108-10” of Income Tax Assessment Act, 1997”, the asset that

is used as private or entertainment purpose comes under Collectables items. Collectable items

include Jewellery, antiques, paintings, art, coins and stamps (Ato.gov.au 2019). As per this

“Section 108-10, ITAA 1997”, the collectable that has purchased below $500 will be

disregarded from Capital gain tax. Further, if there is made any loss on selling those

collectables, then it allowed for an offset with the capital gains.

As the acquisition cost of the paintings that have been bought by Jasmine was less

than $500; therefore, she will be exempted from the capital gain tax within “Section 108-10

(1)”.

However, there is one exceptional case in her selling of paintings as one of the

paintings that she has purchased directly from the artist was amount $1,000. Here she will not

get any exemption for her collectable item and be liable for the Capital gains tax (Clark

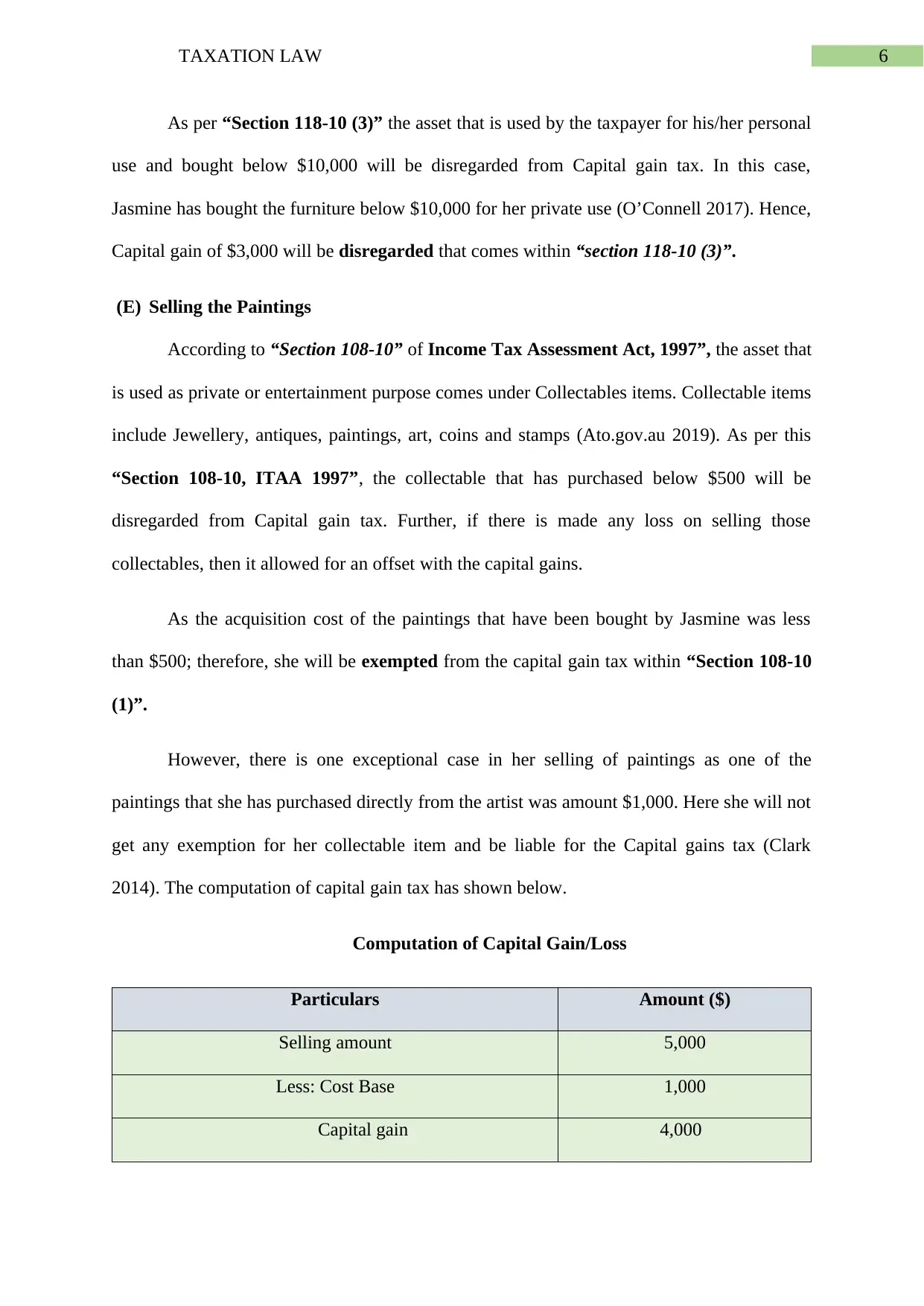

2014). The computation of capital gain tax has shown below.

Computation of Capital Gain/Loss

Particulars Amount ($)

Selling amount 5,000

Less: Cost Base 1,000

Capital gain 4,000

As per “Section 118-10 (3)” the asset that is used by the taxpayer for his/her personal

use and bought below $10,000 will be disregarded from Capital gain tax. In this case,

Jasmine has bought the furniture below $10,000 for her private use (O’Connell 2017). Hence,

Capital gain of $3,000 will be disregarded that comes within “section 118-10 (3)”.

(E) Selling the Paintings

According to “Section 108-10” of Income Tax Assessment Act, 1997”, the asset that

is used as private or entertainment purpose comes under Collectables items. Collectable items

include Jewellery, antiques, paintings, art, coins and stamps (Ato.gov.au 2019). As per this

“Section 108-10, ITAA 1997”, the collectable that has purchased below $500 will be

disregarded from Capital gain tax. Further, if there is made any loss on selling those

collectables, then it allowed for an offset with the capital gains.

As the acquisition cost of the paintings that have been bought by Jasmine was less

than $500; therefore, she will be exempted from the capital gain tax within “Section 108-10

(1)”.

However, there is one exceptional case in her selling of paintings as one of the

paintings that she has purchased directly from the artist was amount $1,000. Here she will not

get any exemption for her collectable item and be liable for the Capital gains tax (Clark

2014). The computation of capital gain tax has shown below.

Computation of Capital Gain/Loss

Particulars Amount ($)

Selling amount 5,000

Less: Cost Base 1,000

Capital gain 4,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Less: Reduction of 50% 2,000

Net Taxable Capital Gain 2,000

Answer 2: Capital Allowance

Identification of Issues

As per the case, John owns a motor vehicle parts and accessories manufacturing

company. Further, he has purchased industrial Computer Numerical Control (CNC) machine

that is imported from Germany needs a guiding rod after sometime (Yussof, Isa and Mohdali

2014). The case states trip cost and machine installation charge for the period.

In the Act within “Section 40-25 (1)” it has been stated about the price to be deducted

in the devaluing assets. As per this section if an individual owes a devaluing asset that is part

of the value of the decrease in asset or the owner of that asset has installed it as ready or to

use other than any taxable purpose then the taxpayer will be allowed to claim for a tax

deduction (McGregor-Lowndes and Critall 2017).

Laws

It has been mentioned in the ITAA Act 1997 within “Division 40”, an individual is

liable for the entitlement of deduction for the amount identical to the decreasing rate of a

depreciating asset. The decreasing price of the asset reflects the value decreasing because of

the actual amount, that taxpayer received (Hichliffe 2014).

An individual within the provision of chief operating of “Section 40-25 (1)” is liable

to get the deduction for the whole year for the amount that is equal to:

the value of depreciating asset or use of it leads to earning income and ready for use

installation or,

the use of an asset by the taxpayer is generating any income to him, or

Less: Reduction of 50% 2,000

Net Taxable Capital Gain 2,000

Answer 2: Capital Allowance

Identification of Issues

As per the case, John owns a motor vehicle parts and accessories manufacturing

company. Further, he has purchased industrial Computer Numerical Control (CNC) machine

that is imported from Germany needs a guiding rod after sometime (Yussof, Isa and Mohdali

2014). The case states trip cost and machine installation charge for the period.

In the Act within “Section 40-25 (1)” it has been stated about the price to be deducted

in the devaluing assets. As per this section if an individual owes a devaluing asset that is part

of the value of the decrease in asset or the owner of that asset has installed it as ready or to

use other than any taxable purpose then the taxpayer will be allowed to claim for a tax

deduction (McGregor-Lowndes and Critall 2017).

Laws

It has been mentioned in the ITAA Act 1997 within “Division 40”, an individual is

liable for the entitlement of deduction for the amount identical to the decreasing rate of a

depreciating asset. The decreasing price of the asset reflects the value decreasing because of

the actual amount, that taxpayer received (Hichliffe 2014).

An individual within the provision of chief operating of “Section 40-25 (1)” is liable

to get the deduction for the whole year for the amount that is equal to:

the value of depreciating asset or use of it leads to earning income and ready for use

installation or,

the use of an asset by the taxpayer is generating any income to him, or

8TAXATION LAW

any asset that is installed as all set that is ready for use.

According to “Section 40-60 (1)”, at the starting period, the taxpayer having those

depreciating assets starts decreasing its actual value. The starting period refers to that time on

which the taxpayer starts using the assets that are installed as ready for use. Considering

ITAA Act 1997, it has been mentioned in the “Section 40-25 (2)”, that the taxpayer will not

be liable to get any deduction until the asset is for private purpose (Black 2018). Further,

“Section40-30 (1)” states depreciating assets as the assets having their limited time for use

that is expected to drop down its value until the use.

Referring to the case of the Law Court of the “Broken Hill Pty Ltd v. FCT” (1969-

70), it has stated the purchase price or the cost of acquiring the asset includes some other

prices. These costs include amount such as the incidental cost and installation charge that

linked with the time of conveyance along with its installation period (Wheelahan 2016).

Other costs will also be included for the expenses such as the arrangement cost, and cost

occurred in removing the plant so that can make space to install the new plant these. The

depreciation is approved on the asset’s cost under “Sub-division 40-C”.

“Section 110-25” of Income Tax Assessment Act 1997, states that the acquiring

cost of an asset comprises of the element like the cost or the money incurred for the first time

so that the asset can be purchased along with the \asset’s market value (Augustinos 2014).

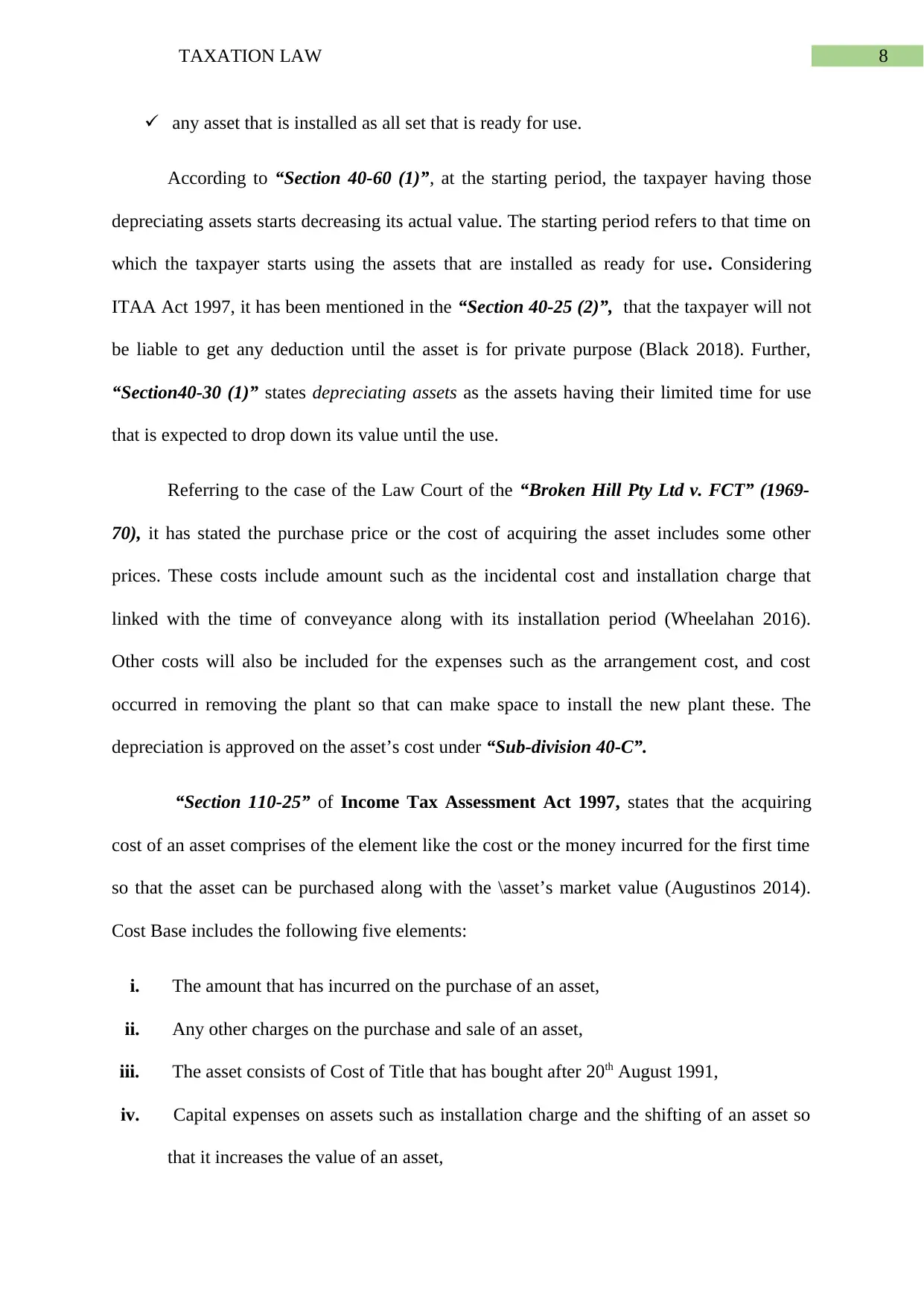

Cost Base includes the following five elements:

i. The amount that has incurred on the purchase of an asset,

ii. Any other charges on the purchase and sale of an asset,

iii. The asset consists of Cost of Title that has bought after 20th August 1991,

iv. Capital expenses on assets such as installation charge and the shifting of an asset so

that it increases the value of an asset,

any asset that is installed as all set that is ready for use.

According to “Section 40-60 (1)”, at the starting period, the taxpayer having those

depreciating assets starts decreasing its actual value. The starting period refers to that time on

which the taxpayer starts using the assets that are installed as ready for use. Considering

ITAA Act 1997, it has been mentioned in the “Section 40-25 (2)”, that the taxpayer will not

be liable to get any deduction until the asset is for private purpose (Black 2018). Further,

“Section40-30 (1)” states depreciating assets as the assets having their limited time for use

that is expected to drop down its value until the use.

Referring to the case of the Law Court of the “Broken Hill Pty Ltd v. FCT” (1969-

70), it has stated the purchase price or the cost of acquiring the asset includes some other

prices. These costs include amount such as the incidental cost and installation charge that

linked with the time of conveyance along with its installation period (Wheelahan 2016).

Other costs will also be included for the expenses such as the arrangement cost, and cost

occurred in removing the plant so that can make space to install the new plant these. The

depreciation is approved on the asset’s cost under “Sub-division 40-C”.

“Section 110-25” of Income Tax Assessment Act 1997, states that the acquiring

cost of an asset comprises of the element like the cost or the money incurred for the first time

so that the asset can be purchased along with the \asset’s market value (Augustinos 2014).

Cost Base includes the following five elements:

i. The amount that has incurred on the purchase of an asset,

ii. Any other charges on the purchase and sale of an asset,

iii. The asset consists of Cost of Title that has bought after 20th August 1991,

iv. Capital expenses on assets such as installation charge and the shifting of an asset so

that it increases the value of an asset,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

v. Further, capital expenses for protecting the Asset’s Right for the title.

The cost of purchase and sale of an asset relates to the acquisition cost under “section

110-35” expenses like shifting the cost, professional charges like stamp duty and

advertisement cost.

Application

As the case states that, John has traded in the CNC machine from Germany. The

amount of machine costs $300,000. The CNC machine started its work doing after its

installation. Further, John has started using from 15 January, but later on, he discovered that

that machine is needed a guiding rod. It has been mentioned under “Section 40-30 (1)”, the

time period of operating the machine considered as the depreciation of an asset. Hence, it is

expected to decrease its value of cost until the time that is used by John as for the motive of

taxation.

With the reference of “section 110-35”, on the date of 15th January, the CNC machine

starts for its use. It is that time when John has finished his installation for the machine, and he

is going to use the CNC machine for the very first time. Addition to this it also includes the

guiding rod. Referring to “Broken Hill Pty Co Ltd v. FCT” (1969-70), the cost of acquiring

the CNC machine includes the cost related to capital enhancement that is $5000 for the

guiding rod.

As per the Chief Operating Provision under “Section 40-25 (1)”, the income tax

deduction is permissible on the equal of the value to the declining price of CNC machine.

Cost base referring to “Section 110-25, ITAA 1997”, also includes the amount that is paid for

the CNC Machine. John has made expense on the inspection of the machine while going

Germany that relates the acquisition cost to the incidental as well as inspection, but this

v. Further, capital expenses for protecting the Asset’s Right for the title.

The cost of purchase and sale of an asset relates to the acquisition cost under “section

110-35” expenses like shifting the cost, professional charges like stamp duty and

advertisement cost.

Application

As the case states that, John has traded in the CNC machine from Germany. The

amount of machine costs $300,000. The CNC machine started its work doing after its

installation. Further, John has started using from 15 January, but later on, he discovered that

that machine is needed a guiding rod. It has been mentioned under “Section 40-30 (1)”, the

time period of operating the machine considered as the depreciation of an asset. Hence, it is

expected to decrease its value of cost until the time that is used by John as for the motive of

taxation.

With the reference of “section 110-35”, on the date of 15th January, the CNC machine

starts for its use. It is that time when John has finished his installation for the machine, and he

is going to use the CNC machine for the very first time. Addition to this it also includes the

guiding rod. Referring to “Broken Hill Pty Co Ltd v. FCT” (1969-70), the cost of acquiring

the CNC machine includes the cost related to capital enhancement that is $5000 for the

guiding rod.

As per the Chief Operating Provision under “Section 40-25 (1)”, the income tax

deduction is permissible on the equal of the value to the declining price of CNC machine.

Cost base referring to “Section 110-25, ITAA 1997”, also includes the amount that is paid for

the CNC Machine. John has made expense on the inspection of the machine while going

Germany that relates the acquisition cost to the incidental as well as inspection, but this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

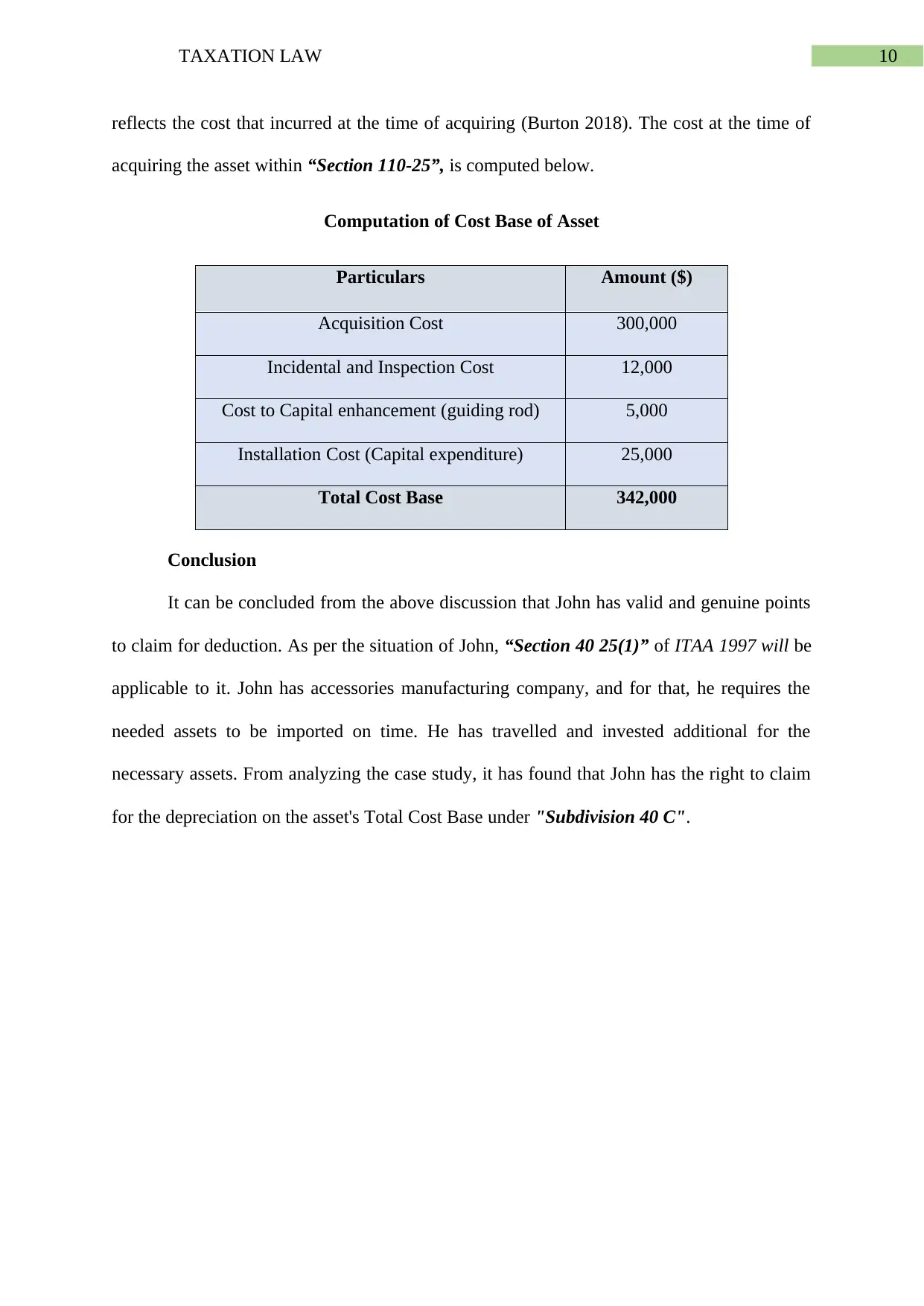

reflects the cost that incurred at the time of acquiring (Burton 2018). The cost at the time of

acquiring the asset within “Section 110-25”, is computed below.

Computation of Cost Base of Asset

Particulars Amount ($)

Acquisition Cost 300,000

Incidental and Inspection Cost 12,000

Cost to Capital enhancement (guiding rod) 5,000

Installation Cost (Capital expenditure) 25,000

Total Cost Base 342,000

Conclusion

It can be concluded from the above discussion that John has valid and genuine points

to claim for deduction. As per the situation of John, “Section 40 25(1)” of ITAA 1997 will be

applicable to it. John has accessories manufacturing company, and for that, he requires the

needed assets to be imported on time. He has travelled and invested additional for the

necessary assets. From analyzing the case study, it has found that John has the right to claim

for the depreciation on the asset's Total Cost Base under "Subdivision 40 C".

reflects the cost that incurred at the time of acquiring (Burton 2018). The cost at the time of

acquiring the asset within “Section 110-25”, is computed below.

Computation of Cost Base of Asset

Particulars Amount ($)

Acquisition Cost 300,000

Incidental and Inspection Cost 12,000

Cost to Capital enhancement (guiding rod) 5,000

Installation Cost (Capital expenditure) 25,000

Total Cost Base 342,000

Conclusion

It can be concluded from the above discussion that John has valid and genuine points

to claim for deduction. As per the situation of John, “Section 40 25(1)” of ITAA 1997 will be

applicable to it. John has accessories manufacturing company, and for that, he requires the

needed assets to be imported on time. He has travelled and invested additional for the

necessary assets. From analyzing the case study, it has found that John has the right to claim

for the depreciation on the asset's Total Cost Base under "Subdivision 40 C".

11TAXATION LAW

References

Ato.gov.au 2019. online Ato.gov.au. Available at:

https://www.ato.gov.au/misc/downloads/pdf/qc22147.pdf Accessed 17 Sep. 2019.

Ato.gov.au 2019. online Ato.gov.au. Available at:

https://www.ato.gov.au/misc/downloads/pdf/qc22147.pdf Accessed 17 Sep. 2019.

Ato.gov.au 2019. online Ato.gov.au. Available at:

https://www.ato.gov.au/misc/downloads/pdf/qc20300.pdf Accessed 17 Sep. 2019.

Ato.gov.au 2019. Legal Database. online Ato.gov.au. Available at:

https://www.ato.gov.au/law/view/document?docid=TXR/TR199916/NAT/ATO/00001

Accessed 17 Sep. 2019.

Ato.gov.au 2019. Your main residence. online Ato.gov.au. Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/Your-

main-residence/ Accessed 17 Sep. 2019.

Augustinos, N., 2014. The Meaning of Market Value in Australia's Income Tax Assessment

Act 1997. J. Australasian Tax Tchrs. Ass'n, 9, p.103.

Black, C., 2018. Taxation of Intellectual Property Under Domestic Law and Tax Treaties:

Australia. Taxation of Intellectual Property under Domestic Law, EU Law and Tax Treaties",

IBFD: Amsterdam.

Blissenden, M., 2015. The income tax and CGT consequences of property

disposals. Taxation in Australia, 49(7), p.385.

Burton, M., 2018. Extending the tax expenditure concept in Australia.

References

Ato.gov.au 2019. online Ato.gov.au. Available at:

https://www.ato.gov.au/misc/downloads/pdf/qc22147.pdf Accessed 17 Sep. 2019.

Ato.gov.au 2019. online Ato.gov.au. Available at:

https://www.ato.gov.au/misc/downloads/pdf/qc22147.pdf Accessed 17 Sep. 2019.

Ato.gov.au 2019. online Ato.gov.au. Available at:

https://www.ato.gov.au/misc/downloads/pdf/qc20300.pdf Accessed 17 Sep. 2019.

Ato.gov.au 2019. Legal Database. online Ato.gov.au. Available at:

https://www.ato.gov.au/law/view/document?docid=TXR/TR199916/NAT/ATO/00001

Accessed 17 Sep. 2019.

Ato.gov.au 2019. Your main residence. online Ato.gov.au. Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/Your-

main-residence/ Accessed 17 Sep. 2019.

Augustinos, N., 2014. The Meaning of Market Value in Australia's Income Tax Assessment

Act 1997. J. Australasian Tax Tchrs. Ass'n, 9, p.103.

Black, C., 2018. Taxation of Intellectual Property Under Domestic Law and Tax Treaties:

Australia. Taxation of Intellectual Property under Domestic Law, EU Law and Tax Treaties",

IBFD: Amsterdam.

Blissenden, M., 2015. The income tax and CGT consequences of property

disposals. Taxation in Australia, 49(7), p.385.

Burton, M., 2018. Extending the tax expenditure concept in Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.