Taxation Law: A Comprehensive Case Study on Tax Principles

VerifiedAdded on 2022/01/06

|8

|1572

|15

Case Study

AI Summary

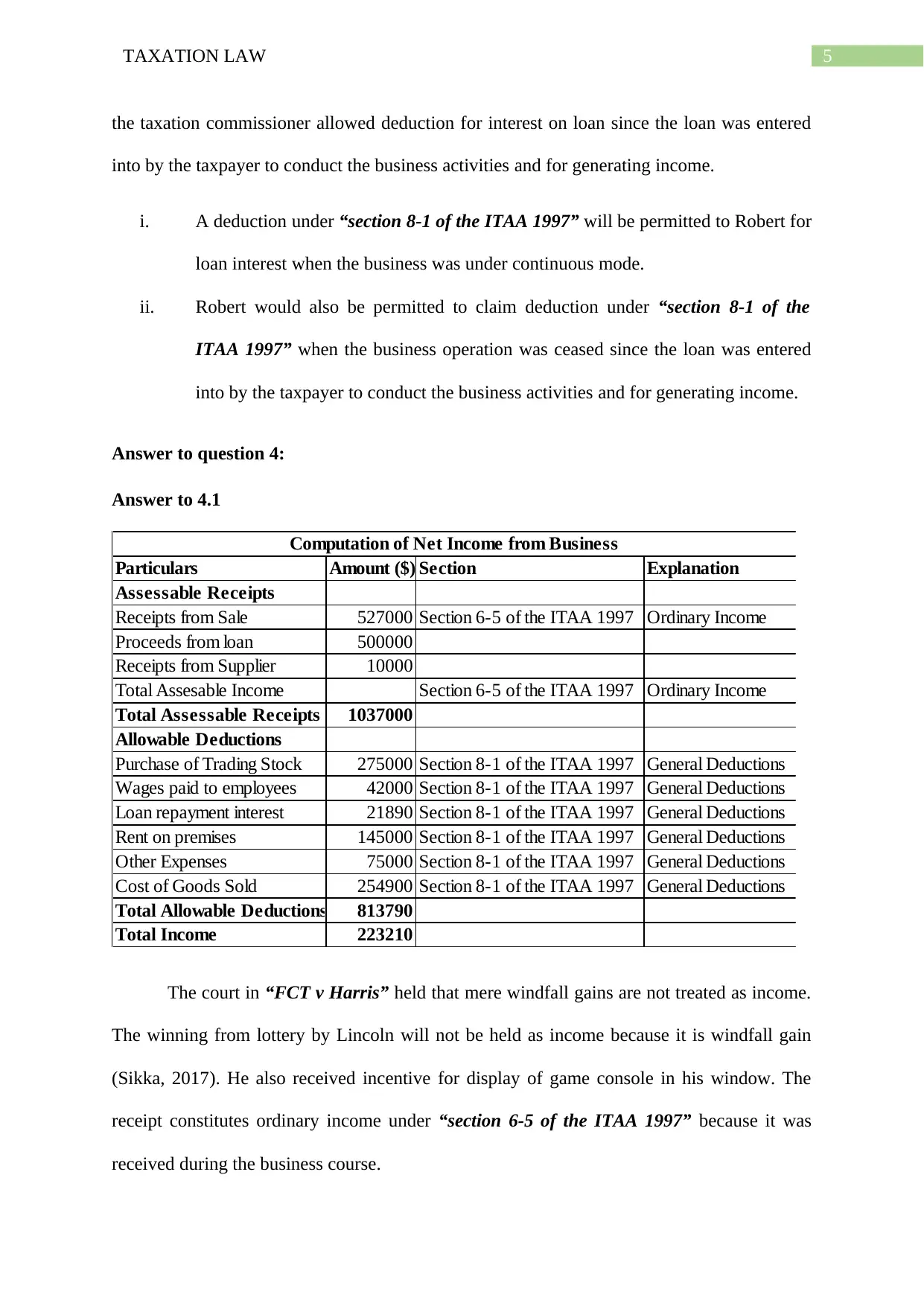

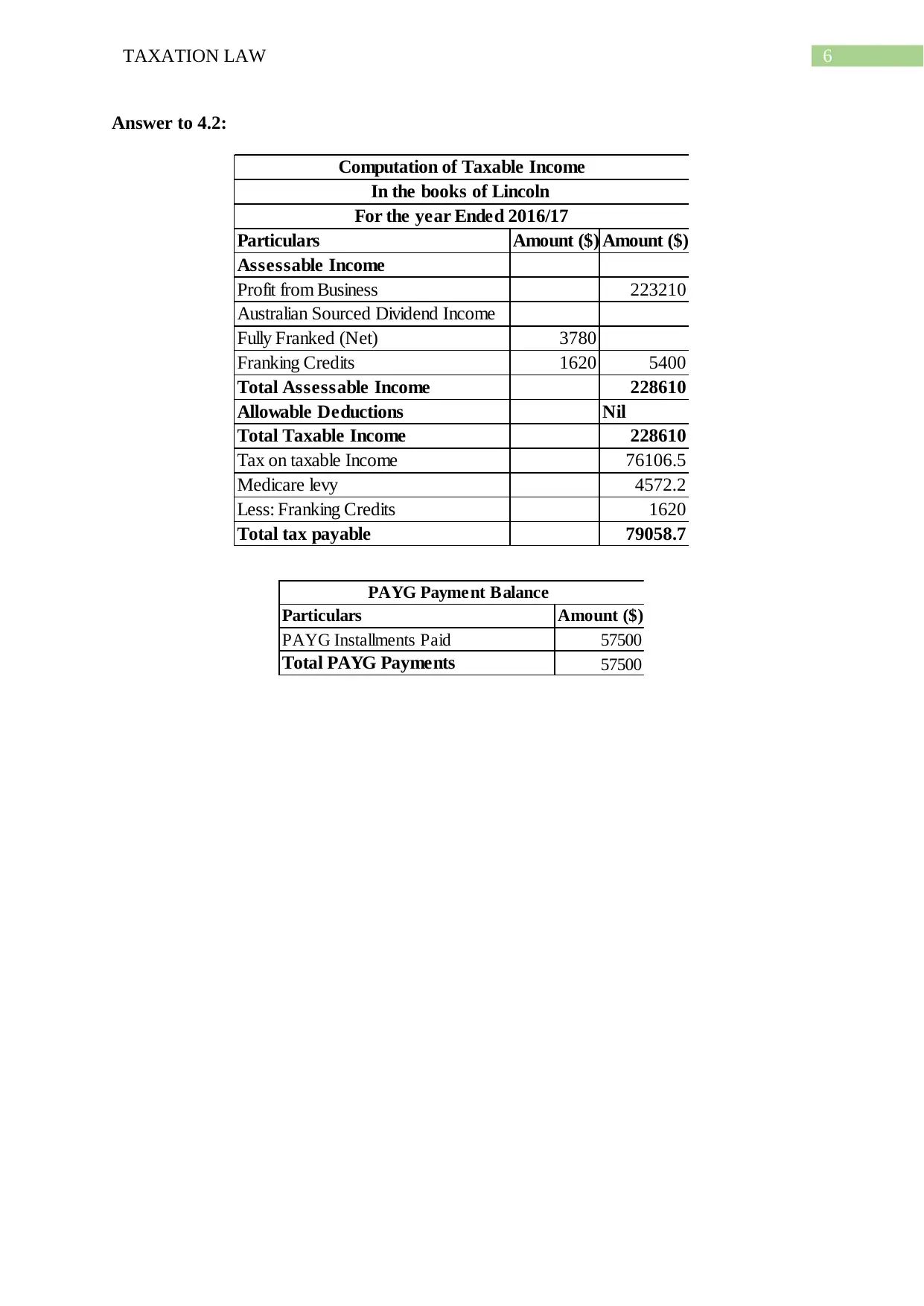

This case study provides a detailed analysis of various aspects of Australian taxation law. It examines the residency status of an individual (Amity) based on the resides test, domicile test, and 183-day test, concluding she is not an Australian resident under section 6(1) of the ITAA 1936. The study also analyzes whether certain receipts constitute ordinary income, such as a computer game received by an employee and a car won as a prize. Furthermore, it discusses the deductibility of loan interest under section 8-1 of the ITAA 1997 for both ongoing and ceased business operations. Finally, it differentiates between windfall gains (lottery winnings) and ordinary income (incentives) in a business context. The document provides detailed answers and is available on Desklib, which offers a range of study tools for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.