Taxation Law Assignment - LAWS20060, Semester 1, [University Name]

VerifiedAdded on 2023/01/16

|17

|4064

|76

Homework Assignment

AI Summary

This taxation law assignment provides a detailed analysis of various aspects of Australian taxation law. It addresses questions related to depreciation methods, tax offsets, income tax rates, capital gains tax exemptions, CGT events, and the application of tax formulas. The assignment delves into specific scenarios involving tax deductions, including interest expenses, apportioned business losses, childcare expenses, losses from theft, and legal expenses. It further examines CGT events related to leases and the application of CGT discounts in different situations, including main residence exemptions and the calculation of capital gains and losses on the sale of shares. The assignment incorporates relevant sections of the ITAA 1997, tax rulings, and case laws to support its arguments and provide a comprehensive understanding of the subject matter.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note

Taxation Law

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW

Table of Contents

Answer to Question 1................................................................................................................3

Requirement A...........................................................................................................................3

Requirement B.......................................................................................................................3

Requirement C.......................................................................................................................3

Requirement D.......................................................................................................................3

Requirement E.......................................................................................................................4

Requirement F.......................................................................................................................4

Requirement G.......................................................................................................................4

Requirement H.......................................................................................................................5

Requirement I........................................................................................................................5

Answer to question 2.................................................................................................................5

Requirement A.......................................................................................................................5

Requirement B.......................................................................................................................6

Requirement C.......................................................................................................................6

Requirement D.......................................................................................................................7

Requirement E.......................................................................................................................7

Answer to Question 3................................................................................................................8

Requirement A.......................................................................................................................8

Requirement B.......................................................................................................................8

TAXATION LAW

Table of Contents

Answer to Question 1................................................................................................................3

Requirement A...........................................................................................................................3

Requirement B.......................................................................................................................3

Requirement C.......................................................................................................................3

Requirement D.......................................................................................................................3

Requirement E.......................................................................................................................4

Requirement F.......................................................................................................................4

Requirement G.......................................................................................................................4

Requirement H.......................................................................................................................5

Requirement I........................................................................................................................5

Answer to question 2.................................................................................................................5

Requirement A.......................................................................................................................5

Requirement B.......................................................................................................................6

Requirement C.......................................................................................................................6

Requirement D.......................................................................................................................7

Requirement E.......................................................................................................................7

Answer to Question 3................................................................................................................8

Requirement A.......................................................................................................................8

Requirement B.......................................................................................................................8

2

TAXATION LAW

Requirement C.......................................................................................................................8

Requirement D.......................................................................................................................9

Answer to question 4:..............................................................................................................10

Answer A:............................................................................................................................10

Answer B:............................................................................................................................10

Answer C:............................................................................................................................11

Answer to D:........................................................................................................................11

Answer to E:........................................................................................................................12

Answer to question 5:..............................................................................................................12

Issues:..................................................................................................................................12

Laws:...................................................................................................................................12

Application:.........................................................................................................................13

Conclusion:..........................................................................................................................14

Reference.................................................................................................................................15

TAXATION LAW

Requirement C.......................................................................................................................8

Requirement D.......................................................................................................................9

Answer to question 4:..............................................................................................................10

Answer A:............................................................................................................................10

Answer B:............................................................................................................................10

Answer C:............................................................................................................................11

Answer to D:........................................................................................................................11

Answer to E:........................................................................................................................12

Answer to question 5:..............................................................................................................12

Issues:..................................................................................................................................12

Laws:...................................................................................................................................12

Application:.........................................................................................................................13

Conclusion:..........................................................................................................................14

Reference.................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW

Answer to Question 1

Requirement A

The provisions of taxation rulings of TR 2018/4 deals with the methods which can be

applied by the commissioner of taxation for the purpose of determining effective asset life for the

purpose of charging depreciation within the provisions of “section 40-100 of the ITAA 1997”.

Requirement B

The provisions of “Division 13 of the ITAA 1997” shows disclosures regarding the tax

offsets which is applicable on taxable income of the individual.

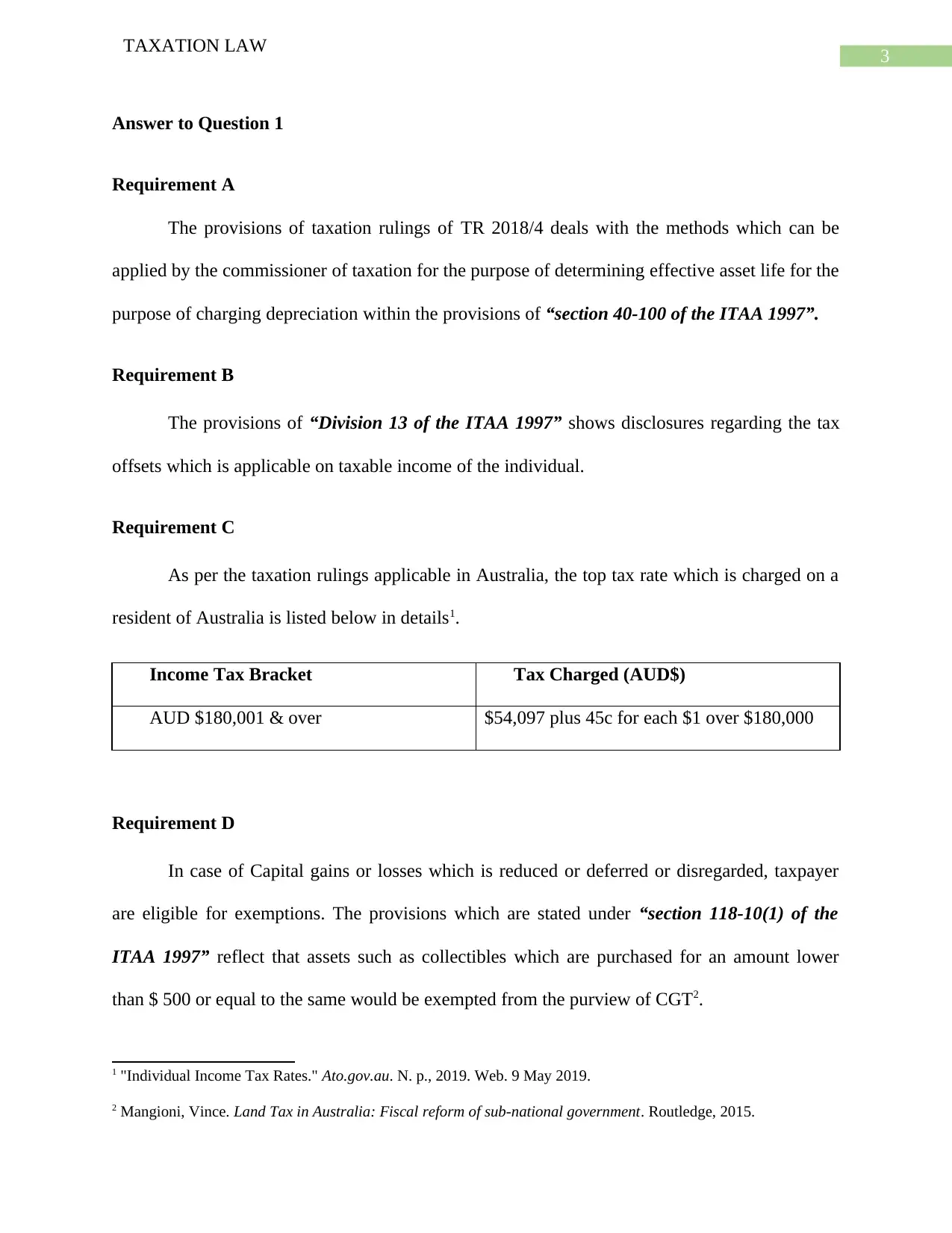

Requirement C

As per the taxation rulings applicable in Australia, the top tax rate which is charged on a

resident of Australia is listed below in details1.

Income Tax Bracket Tax Charged (AUD$)

AUD $180,001 & over $54,097 plus 45c for each $1 over $180,000

Requirement D

In case of Capital gains or losses which is reduced or deferred or disregarded, taxpayer

are eligible for exemptions. The provisions which are stated under “section 118-10(1) of the

ITAA 1997” reflect that assets such as collectibles which are purchased for an amount lower

than $ 500 or equal to the same would be exempted from the purview of CGT2.

1 "Individual Income Tax Rates." Ato.gov.au. N. p., 2019. Web. 9 May 2019.

2 Mangioni, Vince. Land Tax in Australia: Fiscal reform of sub-national government. Routledge, 2015.

TAXATION LAW

Answer to Question 1

Requirement A

The provisions of taxation rulings of TR 2018/4 deals with the methods which can be

applied by the commissioner of taxation for the purpose of determining effective asset life for the

purpose of charging depreciation within the provisions of “section 40-100 of the ITAA 1997”.

Requirement B

The provisions of “Division 13 of the ITAA 1997” shows disclosures regarding the tax

offsets which is applicable on taxable income of the individual.

Requirement C

As per the taxation rulings applicable in Australia, the top tax rate which is charged on a

resident of Australia is listed below in details1.

Income Tax Bracket Tax Charged (AUD$)

AUD $180,001 & over $54,097 plus 45c for each $1 over $180,000

Requirement D

In case of Capital gains or losses which is reduced or deferred or disregarded, taxpayer

are eligible for exemptions. The provisions which are stated under “section 118-10(1) of the

ITAA 1997” reflect that assets such as collectibles which are purchased for an amount lower

than $ 500 or equal to the same would be exempted from the purview of CGT2.

1 "Individual Income Tax Rates." Ato.gov.au. N. p., 2019. Web. 9 May 2019.

2 Mangioni, Vince. Land Tax in Australia: Fiscal reform of sub-national government. Routledge, 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW

Requirement E

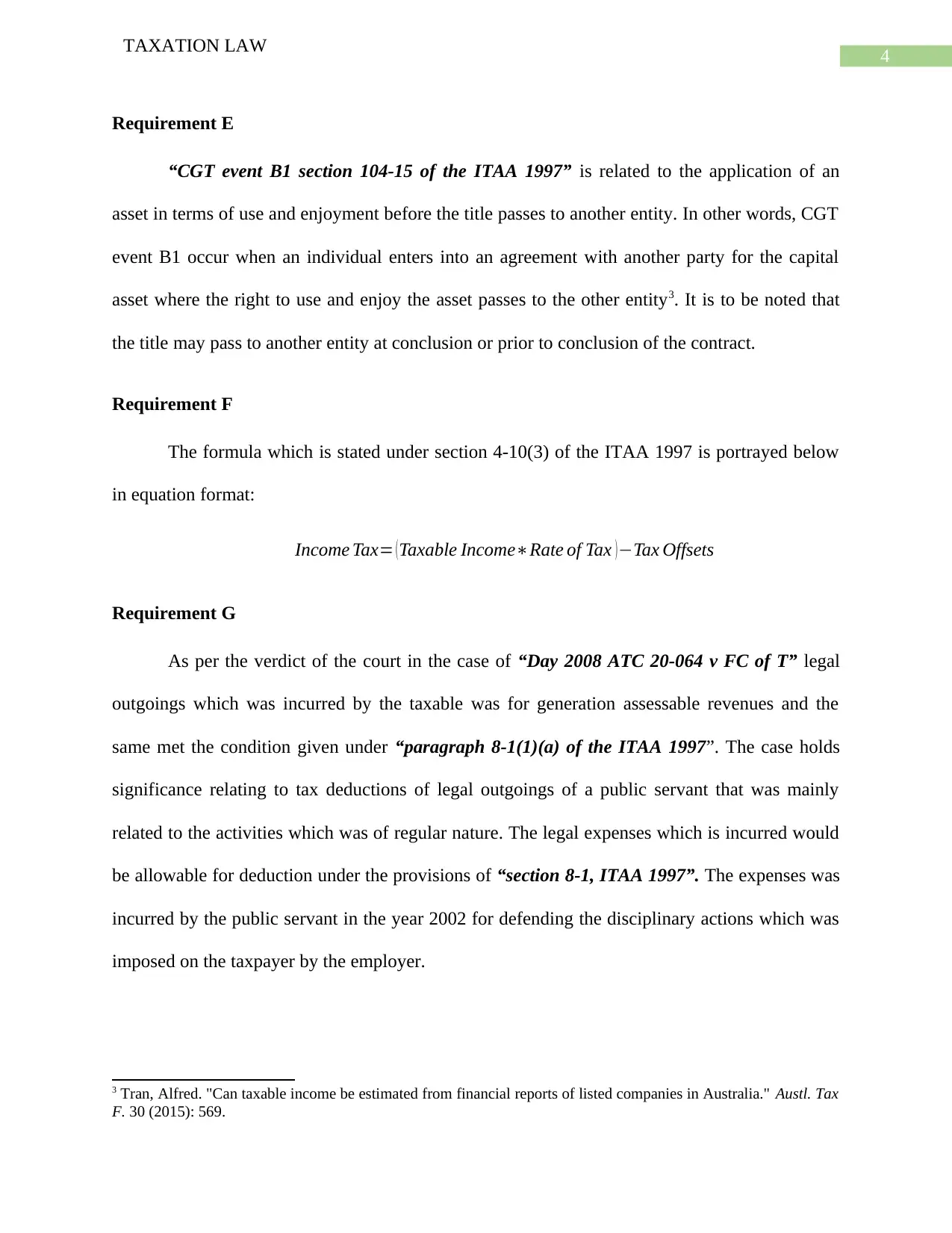

“CGT event B1 section 104-15 of the ITAA 1997” is related to the application of an

asset in terms of use and enjoyment before the title passes to another entity. In other words, CGT

event B1 occur when an individual enters into an agreement with another party for the capital

asset where the right to use and enjoy the asset passes to the other entity3. It is to be noted that

the title may pass to another entity at conclusion or prior to conclusion of the contract.

Requirement F

The formula which is stated under section 4-10(3) of the ITAA 1997 is portrayed below

in equation format:

Income Tax= ( Taxable Income∗Rate of Tax ) −Tax Offsets

Requirement G

As per the verdict of the court in the case of “Day 2008 ATC 20-064 v FC of T” legal

outgoings which was incurred by the taxable was for generation assessable revenues and the

same met the condition given under “paragraph 8-1(1)(a) of the ITAA 1997”. The case holds

significance relating to tax deductions of legal outgoings of a public servant that was mainly

related to the activities which was of regular nature. The legal expenses which is incurred would

be allowable for deduction under the provisions of “section 8-1, ITAA 1997”. The expenses was

incurred by the public servant in the year 2002 for defending the disciplinary actions which was

imposed on the taxpayer by the employer.

3 Tran, Alfred. "Can taxable income be estimated from financial reports of listed companies in Australia." Austl. Tax

F. 30 (2015): 569.

TAXATION LAW

Requirement E

“CGT event B1 section 104-15 of the ITAA 1997” is related to the application of an

asset in terms of use and enjoyment before the title passes to another entity. In other words, CGT

event B1 occur when an individual enters into an agreement with another party for the capital

asset where the right to use and enjoy the asset passes to the other entity3. It is to be noted that

the title may pass to another entity at conclusion or prior to conclusion of the contract.

Requirement F

The formula which is stated under section 4-10(3) of the ITAA 1997 is portrayed below

in equation format:

Income Tax= ( Taxable Income∗Rate of Tax ) −Tax Offsets

Requirement G

As per the verdict of the court in the case of “Day 2008 ATC 20-064 v FC of T” legal

outgoings which was incurred by the taxable was for generation assessable revenues and the

same met the condition given under “paragraph 8-1(1)(a) of the ITAA 1997”. The case holds

significance relating to tax deductions of legal outgoings of a public servant that was mainly

related to the activities which was of regular nature. The legal expenses which is incurred would

be allowable for deduction under the provisions of “section 8-1, ITAA 1997”. The expenses was

incurred by the public servant in the year 2002 for defending the disciplinary actions which was

imposed on the taxpayer by the employer.

3 Tran, Alfred. "Can taxable income be estimated from financial reports of listed companies in Australia." Austl. Tax

F. 30 (2015): 569.

5

TAXATION LAW

Requirement H

The average rate of taxes is obtained by dividing the total amount of taxes chargeable

with the total income which is generated by the taxpayer. On the other hand, marginal tax rate is

determined by applying tax rate on the incremental income which is generated by the taxpayer.

The average rate of taxes assesses the burden of taxes while marginal rate of taxes assesses the

effect of tax of incentives to save, invest or spend.

Requirement I

Consumption tax may be regarded as the tax which is incurred on consumption of goods

and services. It is the system of taxation where people are levied taxes according to how much

they consume instead the contribution they make to the economy.

Answer to question 2

Requirement A

As per the explanation provided by Australian Taxation Office, a taxpayer would be

eligible for deductions in the form of interest expenses incurred for loans while generating the

assessable income for the business or individual. The provisions of “section 8-1, ITAA 1997”

makes it clear that interest on loan that is incurred for the business purposes would be considered

as deductions which is allowed.

As per the case interest on loan which is incurred by Brent for paying wages of

employees would be considered as allowable deductions within the meaning of positive limbs of

“section 8-1, ITAA 1997”. The case laws of “Amalgamated Zinc Ltd v FC of T (1935)” makes

it clear that Brent had incurred the interest on loan amount for generating taxable income in the

business.

TAXATION LAW

Requirement H

The average rate of taxes is obtained by dividing the total amount of taxes chargeable

with the total income which is generated by the taxpayer. On the other hand, marginal tax rate is

determined by applying tax rate on the incremental income which is generated by the taxpayer.

The average rate of taxes assesses the burden of taxes while marginal rate of taxes assesses the

effect of tax of incentives to save, invest or spend.

Requirement I

Consumption tax may be regarded as the tax which is incurred on consumption of goods

and services. It is the system of taxation where people are levied taxes according to how much

they consume instead the contribution they make to the economy.

Answer to question 2

Requirement A

As per the explanation provided by Australian Taxation Office, a taxpayer would be

eligible for deductions in the form of interest expenses incurred for loans while generating the

assessable income for the business or individual. The provisions of “section 8-1, ITAA 1997”

makes it clear that interest on loan that is incurred for the business purposes would be considered

as deductions which is allowed.

As per the case interest on loan which is incurred by Brent for paying wages of

employees would be considered as allowable deductions within the meaning of positive limbs of

“section 8-1, ITAA 1997”. The case laws of “Amalgamated Zinc Ltd v FC of T (1935)” makes

it clear that Brent had incurred the interest on loan amount for generating taxable income in the

business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW

Requirement B

The losses or outgoings which is incurred in regards to business can be apportioned or the

same can be partially deductible. In the case of “Ronpibon Tin NL v FC of T (1949)” the court

required the commissioner to identify the portion of expenses which are work related and which

are private. In case a expenses which includes both private and work related expenses than

deduction would be allowed only on work related expenses of the business.

Julie incurred mobile expenses of $ 500 which included both work related and private use

and the ratio for the same was 60% to 40%. Referring the case of “Ronpibon Tin NL v FC of T

(1949)” Julie would be allowed deduction for the 60% part of the phone expenses and the 40%

would not be allowed as deduction as per the negative limbs of “section 8-1(2)”4.

Requirement C

As per the provisions of “section 8-1, ITAA 1997” child care expenses are considered to

be no-allowable expenses for tax purposes. As per the verdict given in the case of “Lodge v FC

of T (1972)” the taxpayer was not allowed to claim deduction for childcare expenses which was

incurred during the work but the same are not incidental to work.

As per the case which is shown in the assessment, Sally organised a baby-sitting service

while she attended work for her child. These expenses would not be allowable for deduction as

the nature of the expenses is domestic or private. The expenses neither meets the positive or

negative limb as per the criteria of “section 8-1 (2)(b) of the ITAA 1997”.

4 Devos, Ken, and Marcus Zackrisson. "Tax compliance and the public disclosure of tax information: An

Australia/Norway comparison." eJTR 13 (2015): 108.

TAXATION LAW

Requirement B

The losses or outgoings which is incurred in regards to business can be apportioned or the

same can be partially deductible. In the case of “Ronpibon Tin NL v FC of T (1949)” the court

required the commissioner to identify the portion of expenses which are work related and which

are private. In case a expenses which includes both private and work related expenses than

deduction would be allowed only on work related expenses of the business.

Julie incurred mobile expenses of $ 500 which included both work related and private use

and the ratio for the same was 60% to 40%. Referring the case of “Ronpibon Tin NL v FC of T

(1949)” Julie would be allowed deduction for the 60% part of the phone expenses and the 40%

would not be allowed as deduction as per the negative limbs of “section 8-1(2)”4.

Requirement C

As per the provisions of “section 8-1, ITAA 1997” child care expenses are considered to

be no-allowable expenses for tax purposes. As per the verdict given in the case of “Lodge v FC

of T (1972)” the taxpayer was not allowed to claim deduction for childcare expenses which was

incurred during the work but the same are not incidental to work.

As per the case which is shown in the assessment, Sally organised a baby-sitting service

while she attended work for her child. These expenses would not be allowable for deduction as

the nature of the expenses is domestic or private. The expenses neither meets the positive or

negative limb as per the criteria of “section 8-1 (2)(b) of the ITAA 1997”.

4 Devos, Ken, and Marcus Zackrisson. "Tax compliance and the public disclosure of tax information: An

Australia/Norway comparison." eJTR 13 (2015): 108.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

Requirement D

The provisions of “Section 8-1, ITAA 1997” is applicable for outgoings and losses which

is incurred by taxpayers. The court in the case of “Charles Moore & Co (WA) Pty Ltd v FC of T

(1956)” allowed taxpayer deductions for the losses which is incurred from theft when the

taxpayer was going to bank.

As per the positive limb of “section 8-1, ITAA 1997” Jerry would be eligible for

claiming deduction for goods which was stolen and thereby he incurred a loss for the same5. The

loss was incurred while carrying on operations of the business for the purpose of generating

taxable revenues.

Requirement E

Ongoing or legal expenses of the that are incurred at the initial stages of revenue

generation would not be treated as expenses which occurred during the course of business

operations and the same are not treated as deductions under “section 8-1, ITAA 1997”6. As per

the case laws of “Maddalena v FCT (1971)” outgoings incurred for the purpose of getting the

new job were not incurred during the course of business operations and therefore the same would

not be held taxable “section 8-1”

The outgoings incurred in contesting the local government election were preliminary for

the beginning of the revenue producing acts and it is during the course of producing assessable

5 Smith, Marcus, and Russell G. Smith. "Procedural impediments to effective unexplained wealth legislation in

Australia." Trends and Issues in Crime and Criminal Justice523 (2016): 1.

6Ato.gov.au. Legal Database. [online] (2019). Available at: https://www.ato.gov.au/law/view/document?

Docid=TXR/TR977/NAT/ATO/00001 [Accessed 9 May 2019].

TAXATION LAW

Requirement D

The provisions of “Section 8-1, ITAA 1997” is applicable for outgoings and losses which

is incurred by taxpayers. The court in the case of “Charles Moore & Co (WA) Pty Ltd v FC of T

(1956)” allowed taxpayer deductions for the losses which is incurred from theft when the

taxpayer was going to bank.

As per the positive limb of “section 8-1, ITAA 1997” Jerry would be eligible for

claiming deduction for goods which was stolen and thereby he incurred a loss for the same5. The

loss was incurred while carrying on operations of the business for the purpose of generating

taxable revenues.

Requirement E

Ongoing or legal expenses of the that are incurred at the initial stages of revenue

generation would not be treated as expenses which occurred during the course of business

operations and the same are not treated as deductions under “section 8-1, ITAA 1997”6. As per

the case laws of “Maddalena v FCT (1971)” outgoings incurred for the purpose of getting the

new job were not incurred during the course of business operations and therefore the same would

not be held taxable “section 8-1”

The outgoings incurred in contesting the local government election were preliminary for

the beginning of the revenue producing acts and it is during the course of producing assessable

5 Smith, Marcus, and Russell G. Smith. "Procedural impediments to effective unexplained wealth legislation in

Australia." Trends and Issues in Crime and Criminal Justice523 (2016): 1.

6Ato.gov.au. Legal Database. [online] (2019). Available at: https://www.ato.gov.au/law/view/document?

Docid=TXR/TR977/NAT/ATO/00001 [Accessed 9 May 2019].

8

TAXATION LAW

income and therefore the same would not be considered as non-deductible under legislative

provision of “section 8-1, ITAA 1997”7.

Answer to Question 3

Requirement A

A “CGT event F2” is eligible when the taxpayer renews extends or grants the long-term leases.

It is generally applied on a taxpayer who is the owner of the underlying asset or the taxpayer is

granted sublease. As per the case of Andy who is a the owner of land, grants a lease of five years

to Brain at a premium of $ 5,000. This led to applicability of “CGT event F2”. This is the main

reason that Andy would not be getting 50% of CGT discount as the same is not applicable in

CGT event F2.

Requirement B

As per the provisions which are stated in ATO a “CGT event B1” takes place when the

use of land is mainly acquired by a new owner. The use of land takes place when the land is

actually acquired by the taxpayer and he is permitted to enjoy the profits or rents pertaining to

the same. In the case, a farm land of $ 40,000 was given a option of purchasing the 100 acres

farm for a sum of $ 800,000. In this case a CGT event B1 takes place and a 50% CGT discount

would be applicable to the transaction.

Requirement C

As per the explanation provide by ATO, if a taxpayer abode is not permanent residence

for the period of ownership and for generating income then in such a situation a partial main

7 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’ view." Procedia-Social and

Behavioral Sciences 109 (2014): 1069-1075.

TAXATION LAW

income and therefore the same would not be considered as non-deductible under legislative

provision of “section 8-1, ITAA 1997”7.

Answer to Question 3

Requirement A

A “CGT event F2” is eligible when the taxpayer renews extends or grants the long-term leases.

It is generally applied on a taxpayer who is the owner of the underlying asset or the taxpayer is

granted sublease. As per the case of Andy who is a the owner of land, grants a lease of five years

to Brain at a premium of $ 5,000. This led to applicability of “CGT event F2”. This is the main

reason that Andy would not be getting 50% of CGT discount as the same is not applicable in

CGT event F2.

Requirement B

As per the provisions which are stated in ATO a “CGT event B1” takes place when the

use of land is mainly acquired by a new owner. The use of land takes place when the land is

actually acquired by the taxpayer and he is permitted to enjoy the profits or rents pertaining to

the same. In the case, a farm land of $ 40,000 was given a option of purchasing the 100 acres

farm for a sum of $ 800,000. In this case a CGT event B1 takes place and a 50% CGT discount

would be applicable to the transaction.

Requirement C

As per the explanation provide by ATO, if a taxpayer abode is not permanent residence

for the period of ownership and for generating income then in such a situation a partial main

7 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’ view." Procedia-Social and

Behavioral Sciences 109 (2014): 1069-1075.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW

residence exemption is allowed to the taxpayer. As per the case, the property which is being

considered was let out for generating income and was also used as main residence till the same

was sold out in 2018. A partial main residence exemption would be provided to Jamie and Olivia

when the property was sold off. Therefore a 50% discount on CGT method can be used by Jamie

and Olivia for determining the capital gains taxes.

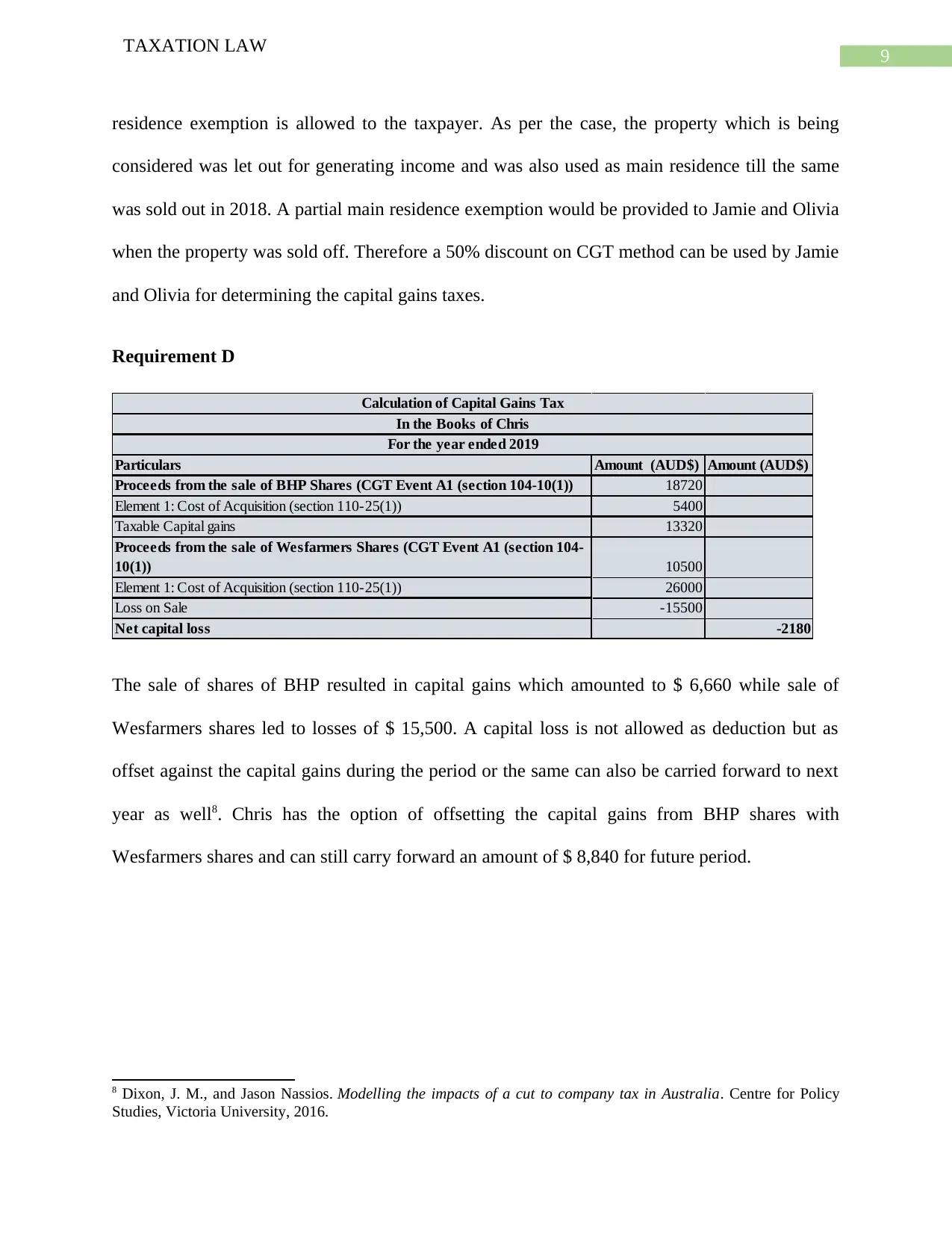

Requirement D

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18720

Element 1: Cost of Acquisition (section 110-25(1)) 5400

Taxable Capital gains 13320

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10500

Element 1: Cost of Acquisition (section 110-25(1)) 26000

Loss on Sale -15500

Net capital loss -2180

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

The sale of shares of BHP resulted in capital gains which amounted to $ 6,660 while sale of

Wesfarmers shares led to losses of $ 15,500. A capital loss is not allowed as deduction but as

offset against the capital gains during the period or the same can also be carried forward to next

year as well8. Chris has the option of offsetting the capital gains from BHP shares with

Wesfarmers shares and can still carry forward an amount of $ 8,840 for future period.

8 Dixon, J. M., and Jason Nassios. Modelling the impacts of a cut to company tax in Australia. Centre for Policy

Studies, Victoria University, 2016.

TAXATION LAW

residence exemption is allowed to the taxpayer. As per the case, the property which is being

considered was let out for generating income and was also used as main residence till the same

was sold out in 2018. A partial main residence exemption would be provided to Jamie and Olivia

when the property was sold off. Therefore a 50% discount on CGT method can be used by Jamie

and Olivia for determining the capital gains taxes.

Requirement D

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18720

Element 1: Cost of Acquisition (section 110-25(1)) 5400

Taxable Capital gains 13320

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10500

Element 1: Cost of Acquisition (section 110-25(1)) 26000

Loss on Sale -15500

Net capital loss -2180

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

The sale of shares of BHP resulted in capital gains which amounted to $ 6,660 while sale of

Wesfarmers shares led to losses of $ 15,500. A capital loss is not allowed as deduction but as

offset against the capital gains during the period or the same can also be carried forward to next

year as well8. Chris has the option of offsetting the capital gains from BHP shares with

Wesfarmers shares and can still carry forward an amount of $ 8,840 for future period.

8 Dixon, J. M., and Jason Nassios. Modelling the impacts of a cut to company tax in Australia. Centre for Policy

Studies, Victoria University, 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW

Answer to question 4:

Answer A:

Prizes and chance winnings are considered non-taxable if the windfall gain is earned by

way of luck. On the other hand, prizes are considered ordinary income if it is earned by using

extent of personal skill which evidently overshadows luck. In “Kelly v FCT (1985)” winnings by

the professional sports people was considered as taxable income because the earnings were

derived by using personal skills9.

Receiving prize of $2000 for best TV advertisement is an ordinary income under

“section 6-5, ITAA 1997”. Citing “Kelly v FCT (1985)” the amount is assumed to have been

received by use of taxpayer’s income earning activity by way of personal service10.

Answer B:

According to the “section 6-1 of the ITAA 1936” income earned from the personal

efforts includes the allowances, salaries, wages or gratuities etc. that is received by an employee

is regarded as an income11. Reimbursement of expenses incurred by the employee from the

employer is not an income. The employee here receives a sum of $500 as the reimbursement of

travel expenses for work purpose. The employee however bought the return flight ticket on sale

for less cost of $120. Therefore, the remaining amount of $380 constitute real gain for the

employee and has the characteristics of income. The amount will be taxable as ordinary income

under “section 6-5, ITAA 1997”.

9 Braithwaite, Valerie. "Responsive regulation and taxation: Introduction." Law & Policy 29.1 (2017): 3-10.

10 Kelly V FCT (1985) 80 FLR 155.

11 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

TAXATION LAW

Answer to question 4:

Answer A:

Prizes and chance winnings are considered non-taxable if the windfall gain is earned by

way of luck. On the other hand, prizes are considered ordinary income if it is earned by using

extent of personal skill which evidently overshadows luck. In “Kelly v FCT (1985)” winnings by

the professional sports people was considered as taxable income because the earnings were

derived by using personal skills9.

Receiving prize of $2000 for best TV advertisement is an ordinary income under

“section 6-5, ITAA 1997”. Citing “Kelly v FCT (1985)” the amount is assumed to have been

received by use of taxpayer’s income earning activity by way of personal service10.

Answer B:

According to the “section 6-1 of the ITAA 1936” income earned from the personal

efforts includes the allowances, salaries, wages or gratuities etc. that is received by an employee

is regarded as an income11. Reimbursement of expenses incurred by the employee from the

employer is not an income. The employee here receives a sum of $500 as the reimbursement of

travel expenses for work purpose. The employee however bought the return flight ticket on sale

for less cost of $120. Therefore, the remaining amount of $380 constitute real gain for the

employee and has the characteristics of income. The amount will be taxable as ordinary income

under “section 6-5, ITAA 1997”.

9 Braithwaite, Valerie. "Responsive regulation and taxation: Introduction." Law & Policy 29.1 (2017): 3-10.

10 Kelly V FCT (1985) 80 FLR 155.

11 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

11

TAXATION LAW

Answer C:

Gifts that is received for rendering personal services are not treated as income in

accordance with ordinary income under “section 6-5, ITAA 1997”. As held in “Scott v FCT

(1966)” gifts received by taxpayer from the client out of personal relationships among the parties

was not held as income12.

The taxpayer reporting the receipt of iphone as the gift from the client that has the value

of $1,000. Mentioning the decision in “Scott v FCT (1966)” the receipt of iphone as the gift is

not an income under ordinary concepts of “section 6-5, ITAA 1997” because it is received as the

personal relationship among the parties.

Answer to D:

Denoting the explanation that is made in the “paragraph 118-37 (1) (b) of the ITAA

1997” taxpayers are advised to ignore the capital gains that is made from the compensation or

damages relating to personal injury or wrong13. Compensation amount received by the taxpayer

for personal injury are usually exempted from tax.

As evident, a compensation amount of $10,000 has been received by the taxpayer for

sustaining injuries from car accident. The compensation amount that is received is owing to

personal injury. Hence, it is not an income and no tax is payable on those amount.

Answer to E:

Where the taxpayers anticipates a certain amount of money in future in the form of being

entitled to income in the future year cannot be considered as income because it is very much

12 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

13 Freudenberg, Brett, et al. "Tax literacy of Australian small businesses." J. Austl. Tax'n 19 (2017): 21.

TAXATION LAW

Answer C:

Gifts that is received for rendering personal services are not treated as income in

accordance with ordinary income under “section 6-5, ITAA 1997”. As held in “Scott v FCT

(1966)” gifts received by taxpayer from the client out of personal relationships among the parties

was not held as income12.

The taxpayer reporting the receipt of iphone as the gift from the client that has the value

of $1,000. Mentioning the decision in “Scott v FCT (1966)” the receipt of iphone as the gift is

not an income under ordinary concepts of “section 6-5, ITAA 1997” because it is received as the

personal relationship among the parties.

Answer to D:

Denoting the explanation that is made in the “paragraph 118-37 (1) (b) of the ITAA

1997” taxpayers are advised to ignore the capital gains that is made from the compensation or

damages relating to personal injury or wrong13. Compensation amount received by the taxpayer

for personal injury are usually exempted from tax.

As evident, a compensation amount of $10,000 has been received by the taxpayer for

sustaining injuries from car accident. The compensation amount that is received is owing to

personal injury. Hence, it is not an income and no tax is payable on those amount.

Answer to E:

Where the taxpayers anticipates a certain amount of money in future in the form of being

entitled to income in the future year cannot be considered as income because it is very much

12 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

13 Freudenberg, Brett, et al. "Tax literacy of Australian small businesses." J. Austl. Tax'n 19 (2017): 21.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.