Holmes Institute: HI6028 Taxation Law Individual Assignment

VerifiedAdded on 2023/03/31

|8

|2211

|345

Homework Assignment

AI Summary

This document provides a comprehensive solution to a taxation law assignment, addressing key concepts such as Capital Gains Tax (CGT) and its application to various asset scenarios, including pre-CGT assets, collectables, and personal use assets. The assignment further delves into the characterization of personal exertion income, analyzing the taxability of payments received for services, referencing relevant case law like Eisner v Macomber and Dean & Anor v FCT. The document also examines the tax treatment of one-off lump-sum payments derived from loan agreements, differentiating between ordinary income and genuine gains, supported by cases such as Hochstrasser v Mayes. The solution meticulously applies taxation principles to real-life problems, offering a thorough understanding of Australian income tax law.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................3

Answer to question 3:...................................................................................................5

References:..................................................................................................................7

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................3

Answer to question 3:...................................................................................................5

References:..................................................................................................................7

2TAXATION LAW

Answer to question 1:

Capital gains from antique painting:

Under the regimes of the CGT where it is noticed that the net capital gains is

accrued to the taxpayer in the particular year of income then the capital gains is

included into the taxable income of the taxpayer for that year (Oats 2014). It is worth

mentioning that the capital loss is not permitted for deduction from the taxable

income rather it is permitted for offset in the particular income year from the capital

gains to ascertain the net amount of capital gains.

The system of capital gains tax is generally applicable on the assets that is

purchased or events that happens following the 20 September 85. The taxpayers

must be aware of the concept such as pre-CGT and post-CGT asset that is regularly

used to refer to those assets that are purchased before or after the events. It is noted

that the painting has been purchased by father of Helen during the February 1985.

However, Helen in a bid to fund for her new business of fashion design has sold the

painting for $12,000 and made a capital gain. It is must be noted that the painting is

the pre-CGT asset because it was purchased before the system of CGT was

introduced. As a result, the capital gains will be exempted made by Helen will be

exempted.

Capital gains from sculpture:

The primary step of ascertaining whether the transaction or the event has

taken place is to ascertain whether the CGT event has happened. CGT event

generally applies to assets that is bought after 20/9/85. A CGT event A1 occurs

when the taxpayer sells the CGT asset under “s104-10” (Marshall, Smith and

Armstrong 2015). Accordingly, “s108-10(2)” explains that collectable is anything that

are mainly used by taxpayer for their own enjoyment purpose. They are generally the

artwork, jewellery, antique and coin.

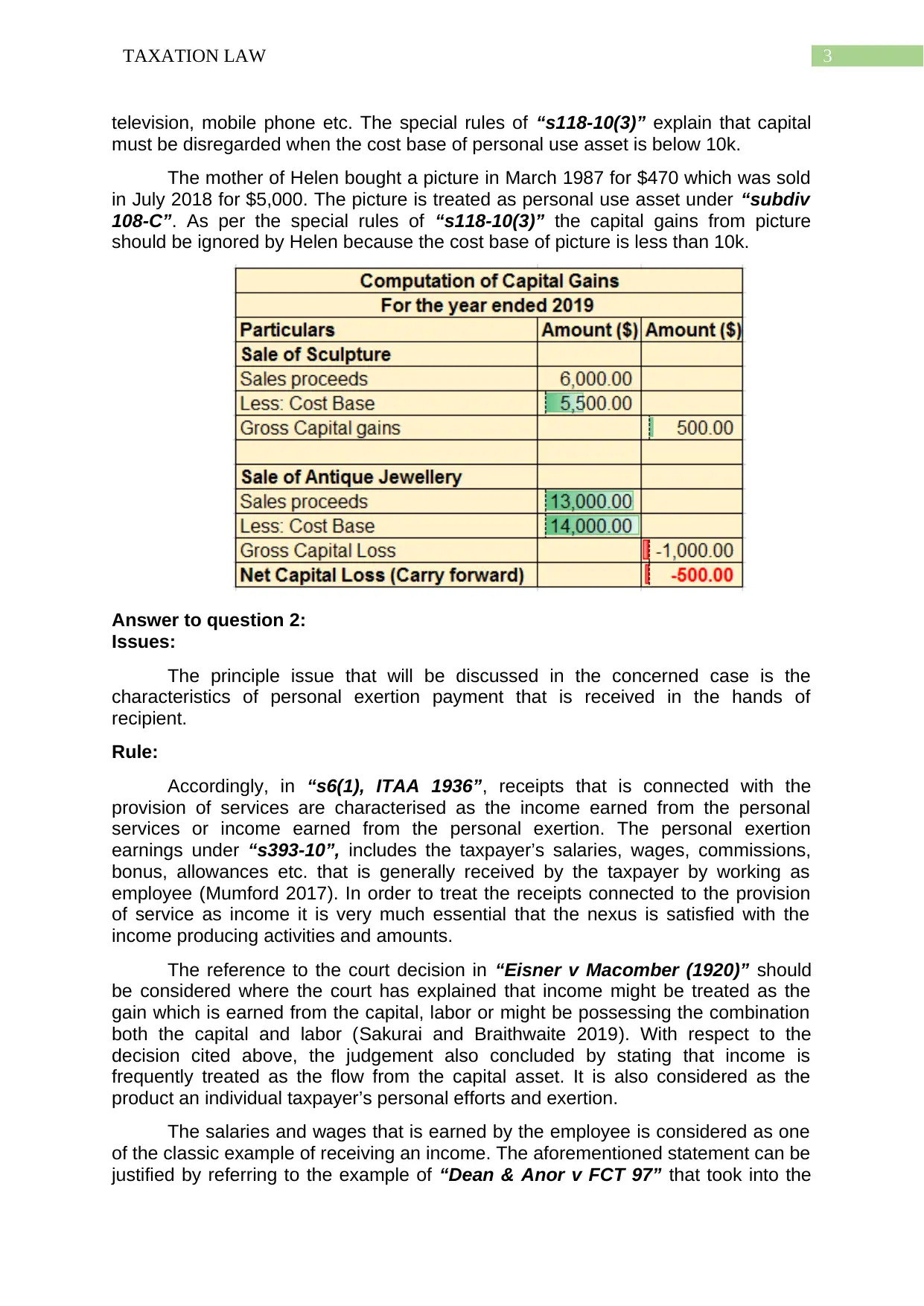

Helen puts forward the information that an artwork sculpture was bought by

her in December 1993 for $5,500 but she sold it for $6,000 in January. A CGT event

A1 occurs when Helen sold the art sculpture under s104-10. The sculpture is

referred as collectable under “s108-10(2)”. The capital gains made from the

sculpture is taxable under the CGT regimes and under “s102-5” it will have included

in the net capital gain for that year as Helen’s assessable income.

Capital gains from jewellery:

Accordingly, the important rule discussed under “s108-10(1)” makes it clear

that capital loss from collectables is only used to offset capital gains from

collectables (Stuckey 2017). The antique jewellery was purchased in October 1987

for $14,000 by Helen was sold in march 2018 for $13,000. Therefore, under the

legislation of under “s108-10(1)” the capital loss that is made from the jewellery is

only allowed to offset from capital gains made from the sculpture.

Capital gains from picture:

The CGT asset also include the personal use assets under “subdiv 108-C”.

A personal use asset is non-collectable asset which is kept for taxpayer’s own use

(Braithwaite 2017). Examples of these assets include the furniture, vehicles,

Answer to question 1:

Capital gains from antique painting:

Under the regimes of the CGT where it is noticed that the net capital gains is

accrued to the taxpayer in the particular year of income then the capital gains is

included into the taxable income of the taxpayer for that year (Oats 2014). It is worth

mentioning that the capital loss is not permitted for deduction from the taxable

income rather it is permitted for offset in the particular income year from the capital

gains to ascertain the net amount of capital gains.

The system of capital gains tax is generally applicable on the assets that is

purchased or events that happens following the 20 September 85. The taxpayers

must be aware of the concept such as pre-CGT and post-CGT asset that is regularly

used to refer to those assets that are purchased before or after the events. It is noted

that the painting has been purchased by father of Helen during the February 1985.

However, Helen in a bid to fund for her new business of fashion design has sold the

painting for $12,000 and made a capital gain. It is must be noted that the painting is

the pre-CGT asset because it was purchased before the system of CGT was

introduced. As a result, the capital gains will be exempted made by Helen will be

exempted.

Capital gains from sculpture:

The primary step of ascertaining whether the transaction or the event has

taken place is to ascertain whether the CGT event has happened. CGT event

generally applies to assets that is bought after 20/9/85. A CGT event A1 occurs

when the taxpayer sells the CGT asset under “s104-10” (Marshall, Smith and

Armstrong 2015). Accordingly, “s108-10(2)” explains that collectable is anything that

are mainly used by taxpayer for their own enjoyment purpose. They are generally the

artwork, jewellery, antique and coin.

Helen puts forward the information that an artwork sculpture was bought by

her in December 1993 for $5,500 but she sold it for $6,000 in January. A CGT event

A1 occurs when Helen sold the art sculpture under s104-10. The sculpture is

referred as collectable under “s108-10(2)”. The capital gains made from the

sculpture is taxable under the CGT regimes and under “s102-5” it will have included

in the net capital gain for that year as Helen’s assessable income.

Capital gains from jewellery:

Accordingly, the important rule discussed under “s108-10(1)” makes it clear

that capital loss from collectables is only used to offset capital gains from

collectables (Stuckey 2017). The antique jewellery was purchased in October 1987

for $14,000 by Helen was sold in march 2018 for $13,000. Therefore, under the

legislation of under “s108-10(1)” the capital loss that is made from the jewellery is

only allowed to offset from capital gains made from the sculpture.

Capital gains from picture:

The CGT asset also include the personal use assets under “subdiv 108-C”.

A personal use asset is non-collectable asset which is kept for taxpayer’s own use

(Braithwaite 2017). Examples of these assets include the furniture, vehicles,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

television, mobile phone etc. The special rules of “s118-10(3)” explain that capital

must be disregarded when the cost base of personal use asset is below 10k.

The mother of Helen bought a picture in March 1987 for $470 which was sold

in July 2018 for $5,000. The picture is treated as personal use asset under “subdiv

108-C”. As per the special rules of “s118-10(3)” the capital gains from picture

should be ignored by Helen because the cost base of picture is less than 10k.

Answer to question 2:

Issues:

The principle issue that will be discussed in the concerned case is the

characteristics of personal exertion payment that is received in the hands of

recipient.

Rule:

Accordingly, in “s6(1), ITAA 1936”, receipts that is connected with the

provision of services are characterised as the income earned from the personal

services or income earned from the personal exertion. The personal exertion

earnings under “s393-10”, includes the taxpayer’s salaries, wages, commissions,

bonus, allowances etc. that is generally received by the taxpayer by working as

employee (Mumford 2017). In order to treat the receipts connected to the provision

of service as income it is very much essential that the nexus is satisfied with the

income producing activities and amounts.

The reference to the court decision in “Eisner v Macomber (1920)” should

be considered where the court has explained that income might be treated as the

gain which is earned from the capital, labor or might be possessing the combination

both the capital and labor (Sakurai and Braithwaite 2019). With respect to the

decision cited above, the judgement also concluded by stating that income is

frequently treated as the flow from the capital asset. It is also considered as the

product an individual taxpayer’s personal efforts and exertion.

The salaries and wages that is earned by the employee is considered as one

of the classic example of receiving an income. The aforementioned statement can be

justified by referring to the example of “Dean & Anor v FCT 97” that took into the

television, mobile phone etc. The special rules of “s118-10(3)” explain that capital

must be disregarded when the cost base of personal use asset is below 10k.

The mother of Helen bought a picture in March 1987 for $470 which was sold

in July 2018 for $5,000. The picture is treated as personal use asset under “subdiv

108-C”. As per the special rules of “s118-10(3)” the capital gains from picture

should be ignored by Helen because the cost base of picture is less than 10k.

Answer to question 2:

Issues:

The principle issue that will be discussed in the concerned case is the

characteristics of personal exertion payment that is received in the hands of

recipient.

Rule:

Accordingly, in “s6(1), ITAA 1936”, receipts that is connected with the

provision of services are characterised as the income earned from the personal

services or income earned from the personal exertion. The personal exertion

earnings under “s393-10”, includes the taxpayer’s salaries, wages, commissions,

bonus, allowances etc. that is generally received by the taxpayer by working as

employee (Mumford 2017). In order to treat the receipts connected to the provision

of service as income it is very much essential that the nexus is satisfied with the

income producing activities and amounts.

The reference to the court decision in “Eisner v Macomber (1920)” should

be considered where the court has explained that income might be treated as the

gain which is earned from the capital, labor or might be possessing the combination

both the capital and labor (Sakurai and Braithwaite 2019). With respect to the

decision cited above, the judgement also concluded by stating that income is

frequently treated as the flow from the capital asset. It is also considered as the

product an individual taxpayer’s personal efforts and exertion.

The salaries and wages that is earned by the employee is considered as one

of the classic example of receiving an income. The aforementioned statement can be

justified by referring to the example of “Dean & Anor v FCT 97” that took into the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

consideration the one-off retaining disbursements that was paid to the crucial staffs

of the business (Burman et al. 2016). The staffs were paid as the consideration of

the employees so that they continue to remain employed with the corporation for the

time period of one year even though the corporation was takeover. According the

decision of the federal court it was noticed that the payments were simply the salary

and wages that formed the part of remuneration for the services that was rendered

by the employee and clearly has the character of income.

One should denote the fact the reward for services is also a product of

personal service income or income earned through the personal exertion. To justify

the statement mentioned illustrations of the court decision in the event of “FCT v

Brent 71” can be discussed. The case took into the consideration the payment that

was received by the wife of train robber who granted the media company with the

right of publishing her story in the article of newspaper (Wanless 2018). The

agreement was entered by the wife of train robber with the media company to make

herself available for the interview and in exchange for her experiences she was paid

duly. The decision of court concluded that the amounts received were holding the

character of income and she was simply rewarded for her services.

Application:

Assembled information from the event of Barbara puts forward that she is an

economist researcher as well as commentator. A publisher named Eco Books Ltd

offered Barbara $13,000 for the purpose of writing the books on economics. Though

Barbara did not have any kind of previous experience of writing book, she did not

decline the offer given by Eco Books Ltd and began writing the book. She finally

wrote the book and was paid $13,000. Accordingly, for Barbara, under “s6(1), ITAA

1936”, receipts that is connected with her provision of services for writing the book is

characterised as the income earned from the personal services or income earned

from the personal exertion.

The example of “Dean & Anor v FCT 97” must be considered in case of

Barbara. The amount of $13,000 is a reward for services rendered. The amounts

received by Barbara is holding the character of income and she was simply

rewarded for her services. Accordingly, under “s6.5, ITAA 1997” Barbara will be

taxable for $13,000 as it is an income under ordinary concept.

She also assigns the copyright of her titled book to Eco Books Ltd and she

received a payment of $13,400. With reference to the example of “FCT v Brent 71”

the payment received in the hands of Barbara is having the nature of income. It is

worth mentioning that the neither did Barbara disposed any capital asset nor had she

assigned the copyright of the manuscripts which in, fact was the product of the

publisher. So the special knowledge possessed by Barbara should not be viewed as

the product of property right which resulted in the copyright. On the basis of this

justification, Barbara has been simply rewarded for her services and the payment of

$13,400 must be accordingly assessed under the ordinary meaning of “sec6-5, ITA

Act 1997”.

The manuscripts of the books and interview manuscripts was sold by Barbara

to the library which in return paid her an equivalent amount. By citing the example of

“Eisner v Macomber (1920)” it can be stated that the payment received from selling

the manuscripts amounts to ordinary income which is the flow from the capital asset

consideration the one-off retaining disbursements that was paid to the crucial staffs

of the business (Burman et al. 2016). The staffs were paid as the consideration of

the employees so that they continue to remain employed with the corporation for the

time period of one year even though the corporation was takeover. According the

decision of the federal court it was noticed that the payments were simply the salary

and wages that formed the part of remuneration for the services that was rendered

by the employee and clearly has the character of income.

One should denote the fact the reward for services is also a product of

personal service income or income earned through the personal exertion. To justify

the statement mentioned illustrations of the court decision in the event of “FCT v

Brent 71” can be discussed. The case took into the consideration the payment that

was received by the wife of train robber who granted the media company with the

right of publishing her story in the article of newspaper (Wanless 2018). The

agreement was entered by the wife of train robber with the media company to make

herself available for the interview and in exchange for her experiences she was paid

duly. The decision of court concluded that the amounts received were holding the

character of income and she was simply rewarded for her services.

Application:

Assembled information from the event of Barbara puts forward that she is an

economist researcher as well as commentator. A publisher named Eco Books Ltd

offered Barbara $13,000 for the purpose of writing the books on economics. Though

Barbara did not have any kind of previous experience of writing book, she did not

decline the offer given by Eco Books Ltd and began writing the book. She finally

wrote the book and was paid $13,000. Accordingly, for Barbara, under “s6(1), ITAA

1936”, receipts that is connected with her provision of services for writing the book is

characterised as the income earned from the personal services or income earned

from the personal exertion.

The example of “Dean & Anor v FCT 97” must be considered in case of

Barbara. The amount of $13,000 is a reward for services rendered. The amounts

received by Barbara is holding the character of income and she was simply

rewarded for her services. Accordingly, under “s6.5, ITAA 1997” Barbara will be

taxable for $13,000 as it is an income under ordinary concept.

She also assigns the copyright of her titled book to Eco Books Ltd and she

received a payment of $13,400. With reference to the example of “FCT v Brent 71”

the payment received in the hands of Barbara is having the nature of income. It is

worth mentioning that the neither did Barbara disposed any capital asset nor had she

assigned the copyright of the manuscripts which in, fact was the product of the

publisher. So the special knowledge possessed by Barbara should not be viewed as

the product of property right which resulted in the copyright. On the basis of this

justification, Barbara has been simply rewarded for her services and the payment of

$13,400 must be accordingly assessed under the ordinary meaning of “sec6-5, ITA

Act 1997”.

The manuscripts of the books and interview manuscripts was sold by Barbara

to the library which in return paid her an equivalent amount. By citing the example of

“Eisner v Macomber (1920)” it can be stated that the payment received from selling

the manuscripts amounts to ordinary income which is the flow from the capital asset

5TAXATION LAW

and it constituted the product of Barbara’s personal exertion. The payment will be

taxable under the ordinary meaning of “sec6-5, ITAA 1997”.

Alternative case scenario for Barbara can be referred as well to treat the

payment as income. If the taxpayer here Barbara decides to write the book

whenever she was free and then selling the book to receive income, the payment

would have been characterised as personal exertion income which is taxable under

“sec6-5”.

Conclusion:

The nature of the payment that is received by Barbara is significant and was

not just to meet the taxpayer cost. The monies received were the personal exertion

income which is taxable under “sec6-5”.

Answer to question 3:

Issues:

The principle issue that will be discussed in the concerned case is the

characteristics of one-off lump sum payment that is received in the hands of recipient

from the loan agreement.

Rule:

According to the “sec6.5, ITA Act 1997” the taxable income of the taxpayer

comprises of the income earned with respect to the ordinary concept. It must be

noted by the taxpayer that the assessable income usually attracts tax liability and

commonly added into the taxable earnings of the taxpayer (Stiglitz 2015). The

assessable includes the statutory income as well as the ordinary income. The

statutory income is classified as the taxable earnings under the numerous provision

of the tax acts. This generally includes the net capital gains. It is worth mentioning

that the statutory income is taken into the consideration prior to implementing the

ordinary income as the amount that must be assessed under the most important

provision of “sec 6-25 (2)”.

A receipt is generally not considered as the genuine gain until it exhibits the

character of ordinary income. The court in “Hochstrasser v Mayes (1960)”

explained that for a receipts to be classified as gain it must be holding the character

of income (Robin 2019). The lump sum gains might be treated as the ordinary

income if it constitutes a real gain of the taxpayer. This usually comprises of the one-

off receipts of interest that is earned under the agreement of loan.

Application:

The application of the rules that is mentioned above can be referred in the

situation of Patrick. Gathered circumstances from the case facts states that Patrick

loaned his son David $52,000. There was no type of written agreement between the

father and the son but the son agreed to return his father the principle amount of

loan together with the interest of $6000 within five years. The son paid his father with

the full amount along with the five interest as interest on loan through a single

cheque within two years.

The receipt of loan interest by Patrick is a genuine gain here for the taxpayer.

Even though the amount was paid through a single cheque the interest that is

and it constituted the product of Barbara’s personal exertion. The payment will be

taxable under the ordinary meaning of “sec6-5, ITAA 1997”.

Alternative case scenario for Barbara can be referred as well to treat the

payment as income. If the taxpayer here Barbara decides to write the book

whenever she was free and then selling the book to receive income, the payment

would have been characterised as personal exertion income which is taxable under

“sec6-5”.

Conclusion:

The nature of the payment that is received by Barbara is significant and was

not just to meet the taxpayer cost. The monies received were the personal exertion

income which is taxable under “sec6-5”.

Answer to question 3:

Issues:

The principle issue that will be discussed in the concerned case is the

characteristics of one-off lump sum payment that is received in the hands of recipient

from the loan agreement.

Rule:

According to the “sec6.5, ITA Act 1997” the taxable income of the taxpayer

comprises of the income earned with respect to the ordinary concept. It must be

noted by the taxpayer that the assessable income usually attracts tax liability and

commonly added into the taxable earnings of the taxpayer (Stiglitz 2015). The

assessable includes the statutory income as well as the ordinary income. The

statutory income is classified as the taxable earnings under the numerous provision

of the tax acts. This generally includes the net capital gains. It is worth mentioning

that the statutory income is taken into the consideration prior to implementing the

ordinary income as the amount that must be assessed under the most important

provision of “sec 6-25 (2)”.

A receipt is generally not considered as the genuine gain until it exhibits the

character of ordinary income. The court in “Hochstrasser v Mayes (1960)”

explained that for a receipts to be classified as gain it must be holding the character

of income (Robin 2019). The lump sum gains might be treated as the ordinary

income if it constitutes a real gain of the taxpayer. This usually comprises of the one-

off receipts of interest that is earned under the agreement of loan.

Application:

The application of the rules that is mentioned above can be referred in the

situation of Patrick. Gathered circumstances from the case facts states that Patrick

loaned his son David $52,000. There was no type of written agreement between the

father and the son but the son agreed to return his father the principle amount of

loan together with the interest of $6000 within five years. The son paid his father with

the full amount along with the five interest as interest on loan through a single

cheque within two years.

The receipt of loan interest by Patrick is a genuine gain here for the taxpayer.

Even though the amount was paid through a single cheque the interest that is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

received by Patrick is a product of one-off receipt of interest based on the loan given.

Mentioning the verdict of “Hochstrasser v Mayes (1960)” the interest amount

constitutes a real gain for the taxpayer. The interest amount is classified as statutory

income it is taxable under the provision of “s6-25(2)”.

Conclusion:

The receipt of interest is considered as the genuine gain for Patrick because it

exhibits the character of ordinary income. It is a one-off receipts of interest that is

earned under the agreement of loan.

received by Patrick is a product of one-off receipt of interest based on the loan given.

Mentioning the verdict of “Hochstrasser v Mayes (1960)” the interest amount

constitutes a real gain for the taxpayer. The interest amount is classified as statutory

income it is taxable under the provision of “s6-25(2)”.

Conclusion:

The receipt of interest is considered as the genuine gain for Patrick because it

exhibits the character of ordinary income. It is a one-off receipts of interest that is

earned under the agreement of loan.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

References:

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016.

Financial transaction taxes in theory and practice. National Tax Journal, 69(1),

p.171.

Marshall, R., Smith, M. and Armstrong, R.W., 2015. Self-assessment and the tax

audit lottery: the Australian experience. Managerial Auditing Journal, 12(1), pp.9-15.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge.

Oats, L. ed., 2014. Taxation: a fieldwork research handbook. Routledge.

Robin, H., 2019. Australian Taxation Law 2019. Oxford University Press.

Sakurai, Y. and Braithwaite, V., 2019. Taxpayers' perceptions of the ideal tax

adviser: Playing safe or saving dollars?. Centre for Tax System Integrity (CTSI),

Research School of Social Sciences, The Australian National University.

Stiglitz, J.E., 2015. In praise of frank Ramsey's contribution to the theory of

taxation. The Economic Journal, 125(583), pp.235-268.

Stuckey, R., 2017. Best practices for legal education.

Wanless, P.T., 2018. Taxation in centrally planned economies. Routledge.

References:

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016.

Financial transaction taxes in theory and practice. National Tax Journal, 69(1),

p.171.

Marshall, R., Smith, M. and Armstrong, R.W., 2015. Self-assessment and the tax

audit lottery: the Australian experience. Managerial Auditing Journal, 12(1), pp.9-15.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge.

Oats, L. ed., 2014. Taxation: a fieldwork research handbook. Routledge.

Robin, H., 2019. Australian Taxation Law 2019. Oxford University Press.

Sakurai, Y. and Braithwaite, V., 2019. Taxpayers' perceptions of the ideal tax

adviser: Playing safe or saving dollars?. Centre for Tax System Integrity (CTSI),

Research School of Social Sciences, The Australian National University.

Stiglitz, J.E., 2015. In praise of frank Ramsey's contribution to the theory of

taxation. The Economic Journal, 125(583), pp.235-268.

Stuckey, R., 2017. Best practices for legal education.

Wanless, P.T., 2018. Taxation in centrally planned economies. Routledge.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.