Taxation Law Assignment: Our Earth Pty Ltd & Coffee Bean Pty Ltd

VerifiedAdded on 2023/01/23

|15

|3921

|71

Homework Assignment

AI Summary

This assignment solution addresses two key taxation law questions. The first question examines the tax treatment of compensation received by Our Earth Pty Ltd for patent infringement and lost revenue, including the classification of damages, interest, and legal fee reimbursements under Australian tax law. The analysis considers relevant cases and legislation, determining the assessable income components. The second question focuses on the tax implications of land subdivision and sale, exploring whether profits are considered ordinary income or capital gains, and the application of CGT rules, pre and post CGT assets, and profit making schemes. The solution provides detailed explanations, case references, and calculations to support the conclusions, offering a comprehensive overview of the tax principles involved.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................6

Issues:.....................................................................................................................................6

Laws:......................................................................................................................................6

Application:............................................................................................................................8

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................6

Issues:.....................................................................................................................................6

Laws:......................................................................................................................................6

Application:............................................................................................................................8

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

Is the receipt of compensation or settlement amounts to assessable income under

“Division 6” or “subsection 25 (1) of the ITAA 1936”?

Rule:

A compensation receipts or compensation comprises of the amount that is received by

the taxpayer in relation to the right of seeking compensation or the cause of action or any

kind of proceedings that are instituted by the taxpayer in relation to the right or the cause of

action whether or not it is in respect of the underlying assets, originating out of the

proceedings of court or comprising of the dissected amounts. Receipts derived from the

damages and compensation might be taxable as ordinary earnings under “Division 6 of the

ITAA 1997” or as the statutory income.

According to “section 25 (1), ITAA 1997” receipts of compensation payment is

taxable if the payment is a compensation for the loss of income simply such as the previous

year profits or interest (Grange et al., 2014). As held in “Mc Laurin v FC of T (1961)”

compensation payment was considered assessable under “subsection 25 (1), ITAA 1936” to

the extent that the portion of payment received was identifiable and quantifiable in the form

of income.

To determine whether the compensation damages are categorized as ordinary income

or capital receipts, the response is reliant on the nature of receipts. If the compensation

damages are paid for something that relates to the income in agreement with the ordinary

conceptions then “section 6-5, of the ITAA 1997” would be applied (Jover-Ledesma, 2014).

For instance, if the damages or compensation may be treated as assessable income if it is

Answer to question 1:

Issues:

Is the receipt of compensation or settlement amounts to assessable income under

“Division 6” or “subsection 25 (1) of the ITAA 1936”?

Rule:

A compensation receipts or compensation comprises of the amount that is received by

the taxpayer in relation to the right of seeking compensation or the cause of action or any

kind of proceedings that are instituted by the taxpayer in relation to the right or the cause of

action whether or not it is in respect of the underlying assets, originating out of the

proceedings of court or comprising of the dissected amounts. Receipts derived from the

damages and compensation might be taxable as ordinary earnings under “Division 6 of the

ITAA 1997” or as the statutory income.

According to “section 25 (1), ITAA 1997” receipts of compensation payment is

taxable if the payment is a compensation for the loss of income simply such as the previous

year profits or interest (Grange et al., 2014). As held in “Mc Laurin v FC of T (1961)”

compensation payment was considered assessable under “subsection 25 (1), ITAA 1936” to

the extent that the portion of payment received was identifiable and quantifiable in the form

of income.

To determine whether the compensation damages are categorized as ordinary income

or capital receipts, the response is reliant on the nature of receipts. If the compensation

damages are paid for something that relates to the income in agreement with the ordinary

conceptions then “section 6-5, of the ITAA 1997” would be applied (Jover-Ledesma, 2014).

For instance, if the damages or compensation may be treated as assessable income if it is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

received in the series of recurrent, periodic payments that does not constitute instalments of

the lump sum.

Similarly, the law court in “Californian Oil Products Ltd v Federal Commissioner

of Taxation (1934)” amount of money that is paid in the form of damages, compensation or

to indemnify relating to the loss of profit incurred in the ordinary business course of the

enterprise in no doubt be will be treated as income (Kenny, 2013). This is because it is a

portion of profit obtained from performing business activities, although they are caused by

unusual or exceptional events or conditions.

The court of law in “CT (Vic) v Phillips (1936)” held that if the compensation is paid

relating to the loss of business or undertaking or relating to the loss of basis or foundations of

trading activities, then the compensation would be treated as the loss for capital asset (Krever,

2015). Henceforth, due to the absenteeism of countervailing contemplation, the receipts itself

forms a capital in nature. In another example of “FC of T v Spedley Securities Ltd (1988)”

the court of law held that amount received for damage of goodwill is regarded as the item of

capital. The compensation amount received amounted to injury to the capital asset.

Interest that are awarded as the portion of compensation amount is treated as

assessable income to the taxpayer based on the general provision of income. The law court in

“Whitaker v FCT (1998)” held that post judgement interest holds the nature of interest is

regarded ordinary income (Sadiq & Coleman, 2013). Interest is regarded as ordinary income

where the compensation for the lost incomes is involved, given the claimant did not suffered

damages he may have received the interest that is awarded.

Where a taxpayer is allowed deduction for the legal costs that is accessible to the

receiver under the “section 8-1, ITAA 1997” a payment or the award in relation to the legal

costs would be contained within the recipient’s taxable income as the assessable recoupment

received in the series of recurrent, periodic payments that does not constitute instalments of

the lump sum.

Similarly, the law court in “Californian Oil Products Ltd v Federal Commissioner

of Taxation (1934)” amount of money that is paid in the form of damages, compensation or

to indemnify relating to the loss of profit incurred in the ordinary business course of the

enterprise in no doubt be will be treated as income (Kenny, 2013). This is because it is a

portion of profit obtained from performing business activities, although they are caused by

unusual or exceptional events or conditions.

The court of law in “CT (Vic) v Phillips (1936)” held that if the compensation is paid

relating to the loss of business or undertaking or relating to the loss of basis or foundations of

trading activities, then the compensation would be treated as the loss for capital asset (Krever,

2015). Henceforth, due to the absenteeism of countervailing contemplation, the receipts itself

forms a capital in nature. In another example of “FC of T v Spedley Securities Ltd (1988)”

the court of law held that amount received for damage of goodwill is regarded as the item of

capital. The compensation amount received amounted to injury to the capital asset.

Interest that are awarded as the portion of compensation amount is treated as

assessable income to the taxpayer based on the general provision of income. The law court in

“Whitaker v FCT (1998)” held that post judgement interest holds the nature of interest is

regarded ordinary income (Sadiq & Coleman, 2013). Interest is regarded as ordinary income

where the compensation for the lost incomes is involved, given the claimant did not suffered

damages he may have received the interest that is awarded.

Where a taxpayer is allowed deduction for the legal costs that is accessible to the

receiver under the “section 8-1, ITAA 1997” a payment or the award in relation to the legal

costs would be contained within the recipient’s taxable income as the assessable recoupment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

under the “subdivision 20-A” (Sadiq, 2014). The legal cost award is generally paid to

indemnify the taxpayer or the recipient as the successful party for the cost of the lawsuit and

it is not considered as the ordinary income. The sum is treated as taxable recoupment under

the “subsection 20-20 (2)”, which implies that the sum that is received amounts to

recoupment of loss or outgoings that is assessable recoupment given the taxpayer received as

indemnity and the sum was deductible under the provision of “ITAA 1936 or ITAA 1997”.

Application:

In present case of Our Earth Pty Ltd, the company designed the patent of a bio-

degradable, disposal coffee cup whose design was stolen by Coffee Bean Pty Ltd and sold for

a cheaper price to customers. As the consequence of legal litigation Our Earth Pty Ltd was

successfully awarded with the damages relating to its design patent infringement. The

compensation receipts received by Our Earth Pty Ltd relating to infringement of patent

amounts to compensation that is received by the company in relation to the right of seeking

compensation for the illegal breach of patent by Coffee Been Pty Ltd.

To determine whether the compensation damages are categorized as ordinary income

or capital receipts, the response is reliant on the nature of receipts received by Our Earth Pty

Ltd. Citing the case of “CT (Vic) v Phillips (1936)” the compensation of $300,000 paid to

Our Earth Pty Ltd relates to the loss of business or foundations of trading activities

(Woellner, 2013). As a result, the sum of $300,000 amounts to the compensation for the loss

of capital asset. Furthermore, owing to the absence of countervailing contemplation, the

receipts itself forms a capital in nature.

Citing the case of “FC of T v Spedley Securities Ltd (1988)” in the current case the

amount of $300,000 received includes the recompense for the damage to the patent which

under the “subdivision 20-A” (Sadiq, 2014). The legal cost award is generally paid to

indemnify the taxpayer or the recipient as the successful party for the cost of the lawsuit and

it is not considered as the ordinary income. The sum is treated as taxable recoupment under

the “subsection 20-20 (2)”, which implies that the sum that is received amounts to

recoupment of loss or outgoings that is assessable recoupment given the taxpayer received as

indemnity and the sum was deductible under the provision of “ITAA 1936 or ITAA 1997”.

Application:

In present case of Our Earth Pty Ltd, the company designed the patent of a bio-

degradable, disposal coffee cup whose design was stolen by Coffee Bean Pty Ltd and sold for

a cheaper price to customers. As the consequence of legal litigation Our Earth Pty Ltd was

successfully awarded with the damages relating to its design patent infringement. The

compensation receipts received by Our Earth Pty Ltd relating to infringement of patent

amounts to compensation that is received by the company in relation to the right of seeking

compensation for the illegal breach of patent by Coffee Been Pty Ltd.

To determine whether the compensation damages are categorized as ordinary income

or capital receipts, the response is reliant on the nature of receipts received by Our Earth Pty

Ltd. Citing the case of “CT (Vic) v Phillips (1936)” the compensation of $300,000 paid to

Our Earth Pty Ltd relates to the loss of business or foundations of trading activities

(Woellner, 2013). As a result, the sum of $300,000 amounts to the compensation for the loss

of capital asset. Furthermore, owing to the absence of countervailing contemplation, the

receipts itself forms a capital in nature.

Citing the case of “FC of T v Spedley Securities Ltd (1988)” in the current case the

amount of $300,000 received includes the recompense for the damage to the patent which

5TAXATION LAW

itself is an item of capital nature (Woellner et al., 2014). The amount is not assessable as

ordinary income because it is compensation of injury to the capital asset.

Our Earth Pty Ltd also received a sum of $200,000 by Coffee Bean Pty Ltd for

anticipated loss of revenue over the last 12 months. Citing the case of “Californian Oil

Products Ltd v Federal Commissioner of Taxation (1934)” the sum of $200,000 paid in the

form of damages or to compensate relating to the loss of profit incurred in the ordinary

business course of the Our Earth Pty Ltd in no doubt be will be considered as income in terms

of the ordinary conceptions of “section 6-5, of the ITAA 1997”.

A sum of $15,000 as interest was received by Our Earth Pty Ltd. The interest that is

awarded to Our Earth Pty Ltd as the portion of compensation amount is treated as assessable

income for the company under the general provision of income. Referring to the case of

“Whitaker v FCT (1998)” the sum of $15,000 is a post judgement interest which holds the

nature of interest and it is an assessable ordinary income under “section 6-5, of the ITAA

1997”.

Our Earth Pty Ltd was also reimbursed a sum of $40,000 incurred towards legal fees.

The legal cost award is paid to compensate the Our Earth Pty Ltd as the successful party for

the cost of the lawsuit and it is not considered as the ordinary income. The reimbursement of

legal expenses is a payment or the award in relation to the legal costs that should be included

into the Our Earth Pty Ltd assessable income as the taxable recoupment under the

“subdivision 20-A”. The amount is received by Our Earth Pty Ltd as the recoupment of loss

or outgoings which amounts to assessable recoupment.

itself is an item of capital nature (Woellner et al., 2014). The amount is not assessable as

ordinary income because it is compensation of injury to the capital asset.

Our Earth Pty Ltd also received a sum of $200,000 by Coffee Bean Pty Ltd for

anticipated loss of revenue over the last 12 months. Citing the case of “Californian Oil

Products Ltd v Federal Commissioner of Taxation (1934)” the sum of $200,000 paid in the

form of damages or to compensate relating to the loss of profit incurred in the ordinary

business course of the Our Earth Pty Ltd in no doubt be will be considered as income in terms

of the ordinary conceptions of “section 6-5, of the ITAA 1997”.

A sum of $15,000 as interest was received by Our Earth Pty Ltd. The interest that is

awarded to Our Earth Pty Ltd as the portion of compensation amount is treated as assessable

income for the company under the general provision of income. Referring to the case of

“Whitaker v FCT (1998)” the sum of $15,000 is a post judgement interest which holds the

nature of interest and it is an assessable ordinary income under “section 6-5, of the ITAA

1997”.

Our Earth Pty Ltd was also reimbursed a sum of $40,000 incurred towards legal fees.

The legal cost award is paid to compensate the Our Earth Pty Ltd as the successful party for

the cost of the lawsuit and it is not considered as the ordinary income. The reimbursement of

legal expenses is a payment or the award in relation to the legal costs that should be included

into the Our Earth Pty Ltd assessable income as the taxable recoupment under the

“subdivision 20-A”. The amount is received by Our Earth Pty Ltd as the recoupment of loss

or outgoings which amounts to assessable recoupment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

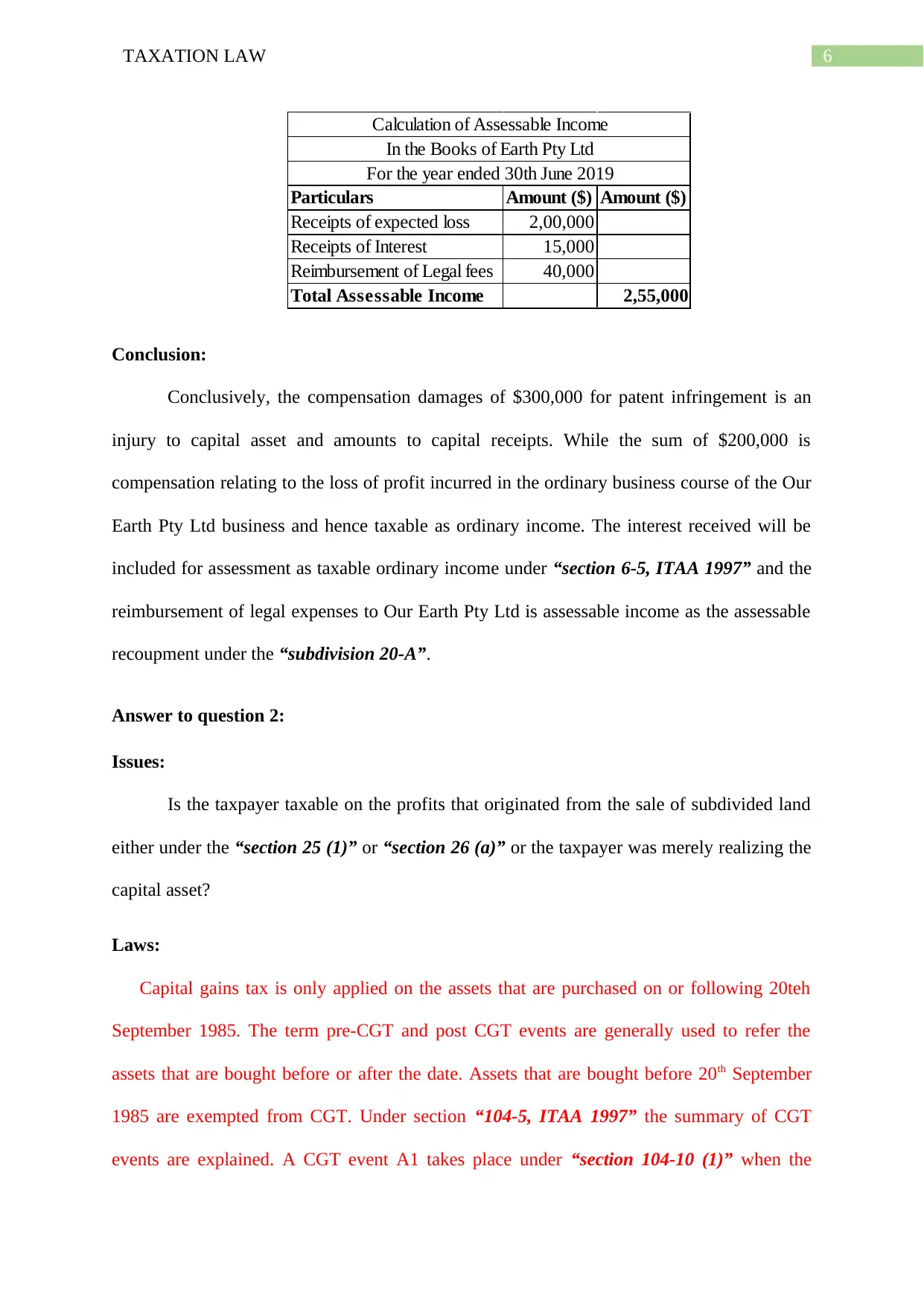

Particulars Amount ($) Amount ($)

Receipts of expected loss 2,00,000

Receipts of Interest 15,000

Reimbursement of Legal fees 40,000

Total Assessable Income 2,55,000

Calculation of Assessable Income

In the Books of Earth Pty Ltd

For the year ended 30th June 2019

Conclusion:

Conclusively, the compensation damages of $300,000 for patent infringement is an

injury to capital asset and amounts to capital receipts. While the sum of $200,000 is

compensation relating to the loss of profit incurred in the ordinary business course of the Our

Earth Pty Ltd business and hence taxable as ordinary income. The interest received will be

included for assessment as taxable ordinary income under “section 6-5, ITAA 1997” and the

reimbursement of legal expenses to Our Earth Pty Ltd is assessable income as the assessable

recoupment under the “subdivision 20-A”.

Answer to question 2:

Issues:

Is the taxpayer taxable on the profits that originated from the sale of subdivided land

either under the “section 25 (1)” or “section 26 (a)” or the taxpayer was merely realizing the

capital asset?

Laws:

Capital gains tax is only applied on the assets that are purchased on or following 20teh

September 1985. The term pre-CGT and post CGT events are generally used to refer the

assets that are bought before or after the date. Assets that are bought before 20th September

1985 are exempted from CGT. Under section “104-5, ITAA 1997” the summary of CGT

events are explained. A CGT event A1 takes place under “section 104-10 (1)” when the

Particulars Amount ($) Amount ($)

Receipts of expected loss 2,00,000

Receipts of Interest 15,000

Reimbursement of Legal fees 40,000

Total Assessable Income 2,55,000

Calculation of Assessable Income

In the Books of Earth Pty Ltd

For the year ended 30th June 2019

Conclusion:

Conclusively, the compensation damages of $300,000 for patent infringement is an

injury to capital asset and amounts to capital receipts. While the sum of $200,000 is

compensation relating to the loss of profit incurred in the ordinary business course of the Our

Earth Pty Ltd business and hence taxable as ordinary income. The interest received will be

included for assessment as taxable ordinary income under “section 6-5, ITAA 1997” and the

reimbursement of legal expenses to Our Earth Pty Ltd is assessable income as the assessable

recoupment under the “subdivision 20-A”.

Answer to question 2:

Issues:

Is the taxpayer taxable on the profits that originated from the sale of subdivided land

either under the “section 25 (1)” or “section 26 (a)” or the taxpayer was merely realizing the

capital asset?

Laws:

Capital gains tax is only applied on the assets that are purchased on or following 20teh

September 1985. The term pre-CGT and post CGT events are generally used to refer the

assets that are bought before or after the date. Assets that are bought before 20th September

1985 are exempted from CGT. Under section “104-5, ITAA 1997” the summary of CGT

events are explained. A CGT event A1 takes place under “section 104-10 (1)” when the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

taxpayer sells the CGT asset. A CGT asset is generally defined as the any form of property or

the legal or equitable right that are not considered property.

There are numerous occasions where the land owners have the prospect of subdividing

and selling the land which is kept by them for an extended time. This generally happens

where the land is owned by the primary producers on the outskirts of urban and residential

expansion signifies that the best treatment of land is for the housing purpose instead of

agriculture (Barkoczy, 2016). In some of the cases, these kind of property developments may

be considered substantial with the prospect of deriving large profits from the project. This

results in question of how the profits must be characterised. Generally, there are three

alternatives;

a. The subdivision and selling of land might qualify as mere realisation of the capital

asset.

b. The extent of development may be such that it amounts to carrying on of the business

of property development (Oishi et al., 2018).

c. The development may go further than mere realisation of the land but may be short of

requirements relating to carrying on the business, in such case it would be treated as

profit making schemes or undertaking.

As per the “Taxation Determination TD 97/3” subdivision of land does not amount

to disposal of land under “section 104-10, ITAA 1997” (Freudenberg et al., 2017). The ruling

provides guidance in establishing whether the proceeds obtained from the isolated

transactions amounts to earnings and therefore chargeable under the “subsection 25 (1),

ITAA 1936”. Prior to embarking on the detailed analysis it is necessary to determine that the

development of land is regarded as mere realisation (Butler, 2019). However, it is vital to

appreciate that the if the land was originally bought for the purpose of resale at the profit or

taxpayer sells the CGT asset. A CGT asset is generally defined as the any form of property or

the legal or equitable right that are not considered property.

There are numerous occasions where the land owners have the prospect of subdividing

and selling the land which is kept by them for an extended time. This generally happens

where the land is owned by the primary producers on the outskirts of urban and residential

expansion signifies that the best treatment of land is for the housing purpose instead of

agriculture (Barkoczy, 2016). In some of the cases, these kind of property developments may

be considered substantial with the prospect of deriving large profits from the project. This

results in question of how the profits must be characterised. Generally, there are three

alternatives;

a. The subdivision and selling of land might qualify as mere realisation of the capital

asset.

b. The extent of development may be such that it amounts to carrying on of the business

of property development (Oishi et al., 2018).

c. The development may go further than mere realisation of the land but may be short of

requirements relating to carrying on the business, in such case it would be treated as

profit making schemes or undertaking.

As per the “Taxation Determination TD 97/3” subdivision of land does not amount

to disposal of land under “section 104-10, ITAA 1997” (Freudenberg et al., 2017). The ruling

provides guidance in establishing whether the proceeds obtained from the isolated

transactions amounts to earnings and therefore chargeable under the “subsection 25 (1),

ITAA 1936”. Prior to embarking on the detailed analysis it is necessary to determine that the

development of land is regarded as mere realisation (Butler, 2019). However, it is vital to

appreciate that the if the land was originally bought for the purpose of resale at the profit or

8TAXATION LAW

for expansion purpose, the profit from the sale or development of land would be considered

as taxable ordinary income, regardless of the sale project.

The profits that arise from the carrying on or executing the profit making undertaking

or the plan in respect of the property that are acquired before the introduction of CGT or Pre-

CGT assets is particularly included into the taxable income under the “section 15-15 of the

ITAA 1997”. The capital improvements made on the pre-CGT asset is subjected to CGT.

While a taxpayer when acquires the land and makes any significant capital improvements

following the date of acquisition would be treated taxable.

As held in “Scottish Australian Mining Co Ltd v FC of T (1950)” the taxpayer

obtained a considerable amount of profit from the sale of subdivided allotments (Morgan et

al., 2018). The taxation officer assessed the taxpayer forb the profits that is obtained from the

disposal of land in numerous lots. As per the taxation commissioner, the profits were held as

assessable income under either “section 25 (1), ITAA 1936” as income derived from carrying

on of the business activities of land development or under “section 26 (a)” as the profits

originated from the profit deriving scheme (Schmalbeck et al., 2015).

Likewise, in “Federal Commissioner of Taxation v Whitfords Beach Pty Ltd

(1982)” the law court assessed the taxpayer for the profits derived from the deal of numerous

lots (Morgan & Castelyn, 2018). The taxation official held that the profits was taxable under

either “section 25 (1), ITAA 1936” as income from conducting the business of land

development or under “section 26 (a)” as the profits originated from carrying on of the profit

making scheme.

Once it is understood that the activity of purchase and sale results in the generation of

profit was not the activity in the ordinary business course or for the matter of ordinary

occurrence of a business activity, the income that is in question will be treated as taxable

for expansion purpose, the profit from the sale or development of land would be considered

as taxable ordinary income, regardless of the sale project.

The profits that arise from the carrying on or executing the profit making undertaking

or the plan in respect of the property that are acquired before the introduction of CGT or Pre-

CGT assets is particularly included into the taxable income under the “section 15-15 of the

ITAA 1997”. The capital improvements made on the pre-CGT asset is subjected to CGT.

While a taxpayer when acquires the land and makes any significant capital improvements

following the date of acquisition would be treated taxable.

As held in “Scottish Australian Mining Co Ltd v FC of T (1950)” the taxpayer

obtained a considerable amount of profit from the sale of subdivided allotments (Morgan et

al., 2018). The taxation officer assessed the taxpayer forb the profits that is obtained from the

disposal of land in numerous lots. As per the taxation commissioner, the profits were held as

assessable income under either “section 25 (1), ITAA 1936” as income derived from carrying

on of the business activities of land development or under “section 26 (a)” as the profits

originated from the profit deriving scheme (Schmalbeck et al., 2015).

Likewise, in “Federal Commissioner of Taxation v Whitfords Beach Pty Ltd

(1982)” the law court assessed the taxpayer for the profits derived from the deal of numerous

lots (Morgan & Castelyn, 2018). The taxation official held that the profits was taxable under

either “section 25 (1), ITAA 1936” as income from conducting the business of land

development or under “section 26 (a)” as the profits originated from carrying on of the profit

making scheme.

Once it is understood that the activity of purchase and sale results in the generation of

profit was not the activity in the ordinary business course or for the matter of ordinary

occurrence of a business activity, the income that is in question will be treated as taxable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

income of the taxpayer by virtue of being income under the ordinary conceptions given the

appellant has the objective of deriving profit during the time of acquisition (Bankman et al.,

2018).

Application:

As evident in the current situation Sam bought a farm land of 80 acres and an

additional 20 acres of land for expansion of business operation. However, the taxpayer was

not anymore interest in the farmland and because of ongoing drought conditions Sam decided

to sell the land and retire from the farming business. Sam engaged the service of real estate

agent to subdivide the land in order to realize best worth of the subdivided land. As

understood Sam being the primary producer engaged in the activities of sub-division for

residential expansion to signify that the best use of land amounts to residential purpose rather

than farming.

The 80 acres of farmland is bought on 1984 which is before the introduction of CGT

and hence it will be considered as the pre-CGT asset. Therefore, it is exempted from the

capital gains tax. Later an adjoining land of 20 acres was bought on February 1995 which is a

post-CGT asset. The sub-division began in 2017 before the land was eventually sold in April

2018. Any kind of capital gains made from the 80 acres’ land should be ignored from capital

gains tax because it is pre-CGT.

In the case of Sam, such kind of property developments may be considered substantial

with the prospect of deriving large profits from the project. Reference to “Taxation

Determination TD 97/3” can be made to ascertain whether the profits obtained from the

subdivided land by Sam amounts to income and therefore taxable under the “subsection 25

(1), ITAA 1936” (Robin, 2019). Prior to engaging in detailed analysis, it is important to

income of the taxpayer by virtue of being income under the ordinary conceptions given the

appellant has the objective of deriving profit during the time of acquisition (Bankman et al.,

2018).

Application:

As evident in the current situation Sam bought a farm land of 80 acres and an

additional 20 acres of land for expansion of business operation. However, the taxpayer was

not anymore interest in the farmland and because of ongoing drought conditions Sam decided

to sell the land and retire from the farming business. Sam engaged the service of real estate

agent to subdivide the land in order to realize best worth of the subdivided land. As

understood Sam being the primary producer engaged in the activities of sub-division for

residential expansion to signify that the best use of land amounts to residential purpose rather

than farming.

The 80 acres of farmland is bought on 1984 which is before the introduction of CGT

and hence it will be considered as the pre-CGT asset. Therefore, it is exempted from the

capital gains tax. Later an adjoining land of 20 acres was bought on February 1995 which is a

post-CGT asset. The sub-division began in 2017 before the land was eventually sold in April

2018. Any kind of capital gains made from the 80 acres’ land should be ignored from capital

gains tax because it is pre-CGT.

In the case of Sam, such kind of property developments may be considered substantial

with the prospect of deriving large profits from the project. Reference to “Taxation

Determination TD 97/3” can be made to ascertain whether the profits obtained from the

subdivided land by Sam amounts to income and therefore taxable under the “subsection 25

(1), ITAA 1936” (Robin, 2019). Prior to engaging in detailed analysis, it is important to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

appreciate that Sam originally did not buy the property for the purpose of resale at profit or

for the development purpose. The profit motive intention developed in the later stages.

Referring to the case of “Scottish Australian Mining Co Ltd v FC of T (1950)” Sam

here derived a considerable amount of profit from the sale of subdivided allotments. Sam

under this circumstances will be assessed relating to the profits that is obtained from the

disposal of land in numerous lots (Robin & Barkoczy, 2019). In light of the Sam’s situation,

the profits will be taxable profits under either “section 25 (1) of the ITAA 1936” as income

derived from performing the business activities of land development or under “section 26

(a)” as the profits originated from the carrying out of the profit deriving scheme.

Sam will be held liable for capital gains tax on the profits derived from the disposal of

20 blocks of land under “section 25 (1)” because Sam had gone further than simply realizing

the capital asset and his activities constitutes carrying the business activities of land

development (Gashenko et al., 2019). Mentioning the decision stated in “Federal

Commissioner of Taxation v Whitfords Beach Pty Ltd (1982)” the extensive development in

the form of rezoning and subdivision of land by Sam was more than simple sale of the

prevailing asset. It amounted to work done by Sam in an enterprising manner to realize the

asset in terms of best advantage.

The amount will be included into the Sam’s gross income under “section 25 (1)” as

assessable capital gains being profit from the sale of land determined in agreement with the

general accounting principle (Miller & Oats, 2016). More specifically, Sam can calculate the

profits by subtracting the legal fees that was payable to the agent from the gross proceeds of

sale value of the relevant land that was ventured out of profit making scheme or undertaking.

appreciate that Sam originally did not buy the property for the purpose of resale at profit or

for the development purpose. The profit motive intention developed in the later stages.

Referring to the case of “Scottish Australian Mining Co Ltd v FC of T (1950)” Sam

here derived a considerable amount of profit from the sale of subdivided allotments. Sam

under this circumstances will be assessed relating to the profits that is obtained from the

disposal of land in numerous lots (Robin & Barkoczy, 2019). In light of the Sam’s situation,

the profits will be taxable profits under either “section 25 (1) of the ITAA 1936” as income

derived from performing the business activities of land development or under “section 26

(a)” as the profits originated from the carrying out of the profit deriving scheme.

Sam will be held liable for capital gains tax on the profits derived from the disposal of

20 blocks of land under “section 25 (1)” because Sam had gone further than simply realizing

the capital asset and his activities constitutes carrying the business activities of land

development (Gashenko et al., 2019). Mentioning the decision stated in “Federal

Commissioner of Taxation v Whitfords Beach Pty Ltd (1982)” the extensive development in

the form of rezoning and subdivision of land by Sam was more than simple sale of the

prevailing asset. It amounted to work done by Sam in an enterprising manner to realize the

asset in terms of best advantage.

The amount will be included into the Sam’s gross income under “section 25 (1)” as

assessable capital gains being profit from the sale of land determined in agreement with the

general accounting principle (Miller & Oats, 2016). More specifically, Sam can calculate the

profits by subtracting the legal fees that was payable to the agent from the gross proceeds of

sale value of the relevant land that was ventured out of profit making scheme or undertaking.

11TAXATION LAW

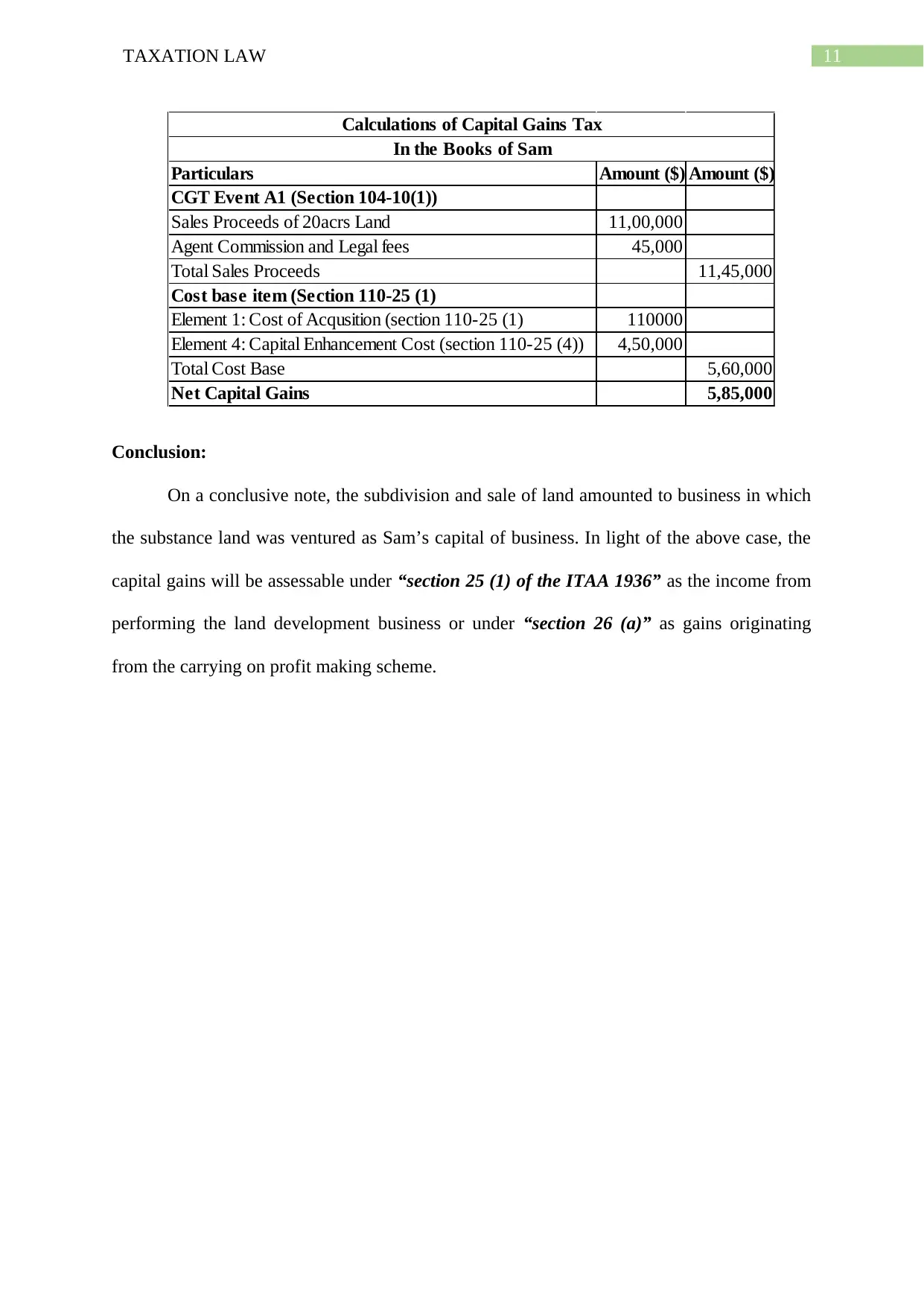

Particulars Amount ($) Amount ($)

CGT Event A1 (Section 104-10(1))

Sales Proceeds of 20acrs Land 11,00,000

Agent Commission and Legal fees 45,000

Total Sales Proceeds 11,45,000

Cost base item (Section 110-25 (1)

Element 1: Cost of Acqusition (section 110-25 (1) 110000

Element 4: Capital Enhancement Cost (section 110-25 (4)) 4,50,000

Total Cost Base 5,60,000

Net Capital Gains 5,85,000

Calculations of Capital Gains Tax

In the Books of Sam

Conclusion:

On a conclusive note, the subdivision and sale of land amounted to business in which

the substance land was ventured as Sam’s capital of business. In light of the above case, the

capital gains will be assessable under “section 25 (1) of the ITAA 1936” as the income from

performing the land development business or under “section 26 (a)” as gains originating

from the carrying on profit making scheme.

Particulars Amount ($) Amount ($)

CGT Event A1 (Section 104-10(1))

Sales Proceeds of 20acrs Land 11,00,000

Agent Commission and Legal fees 45,000

Total Sales Proceeds 11,45,000

Cost base item (Section 110-25 (1)

Element 1: Cost of Acqusition (section 110-25 (1) 110000

Element 4: Capital Enhancement Cost (section 110-25 (4)) 4,50,000

Total Cost Base 5,60,000

Net Capital Gains 5,85,000

Calculations of Capital Gains Tax

In the Books of Sam

Conclusion:

On a conclusive note, the subdivision and sale of land amounted to business in which

the substance land was ventured as Sam’s capital of business. In light of the above case, the

capital gains will be assessable under “section 25 (1) of the ITAA 1936” as the income from

performing the land development business or under “section 26 (a)” as gains originating

from the carrying on profit making scheme.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.