ACCY963 Taxation Law Case Study: CGT and Income Tax Assessment T1 2019

VerifiedAdded on 2023/04/06

|7

|929

|144

Case Study

AI Summary

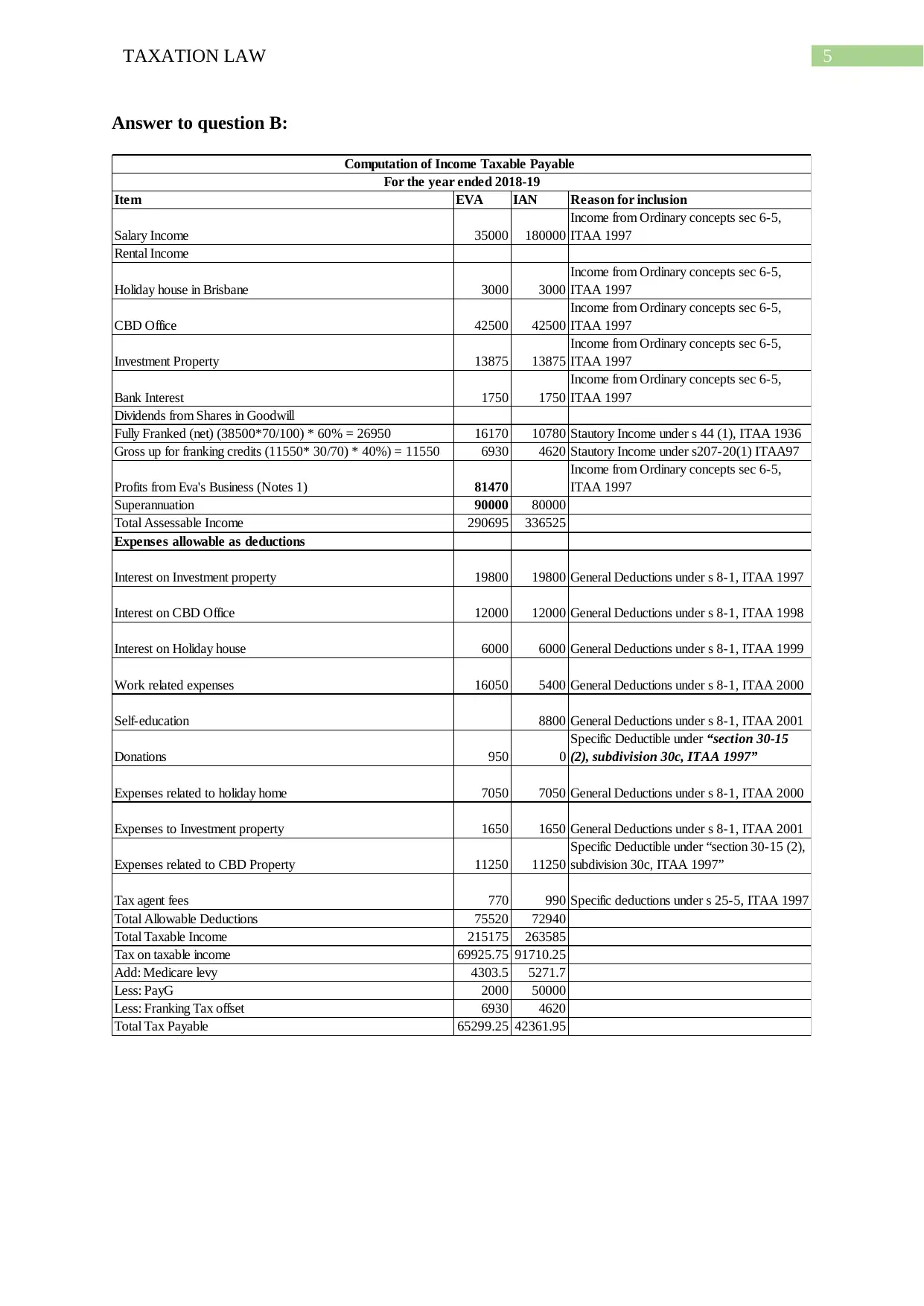

This case study solution addresses key aspects of taxation law, focusing on capital gains tax (CGT) implications and income assessment for a hypothetical couple, Ian and Eva. It identifies CGT events related to the sale of shares and loss of collectibles, calculating capital gains and losses, and determining net capital gains. Furthermore, it computes taxable income for Ian and Eva, considering salary, rental income, dividends, and business profits, while also accounting for allowable deductions such as interest expenses, work-related expenses, and donations. The solution also touches upon the concept of transfer pricing and its potential tax and accounting implications.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.