Taxation Law Assignment: Residency, Income, and Deductions Analysis

VerifiedAdded on 2023/03/17

|11

|2397

|30

Homework Assignment

AI Summary

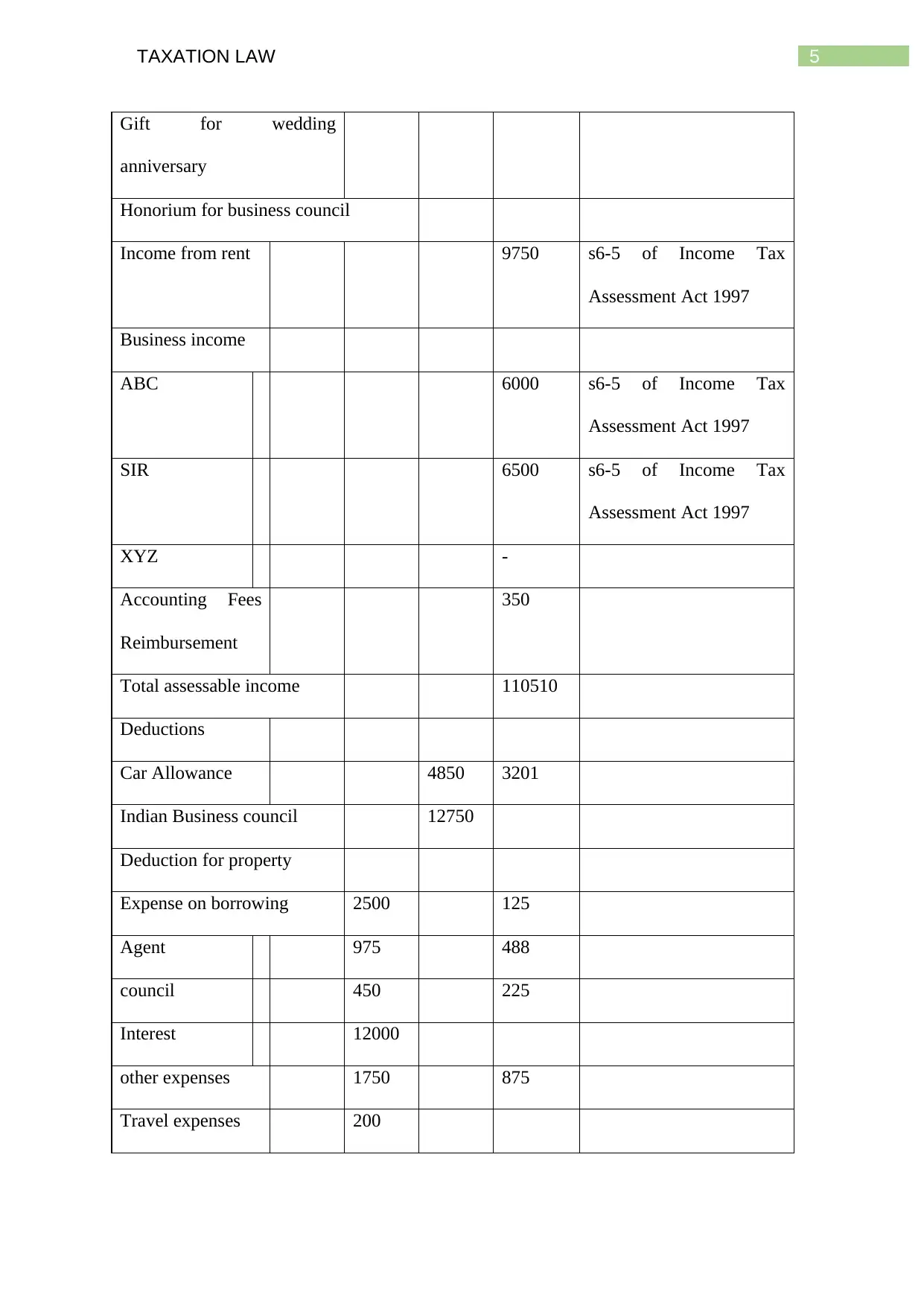

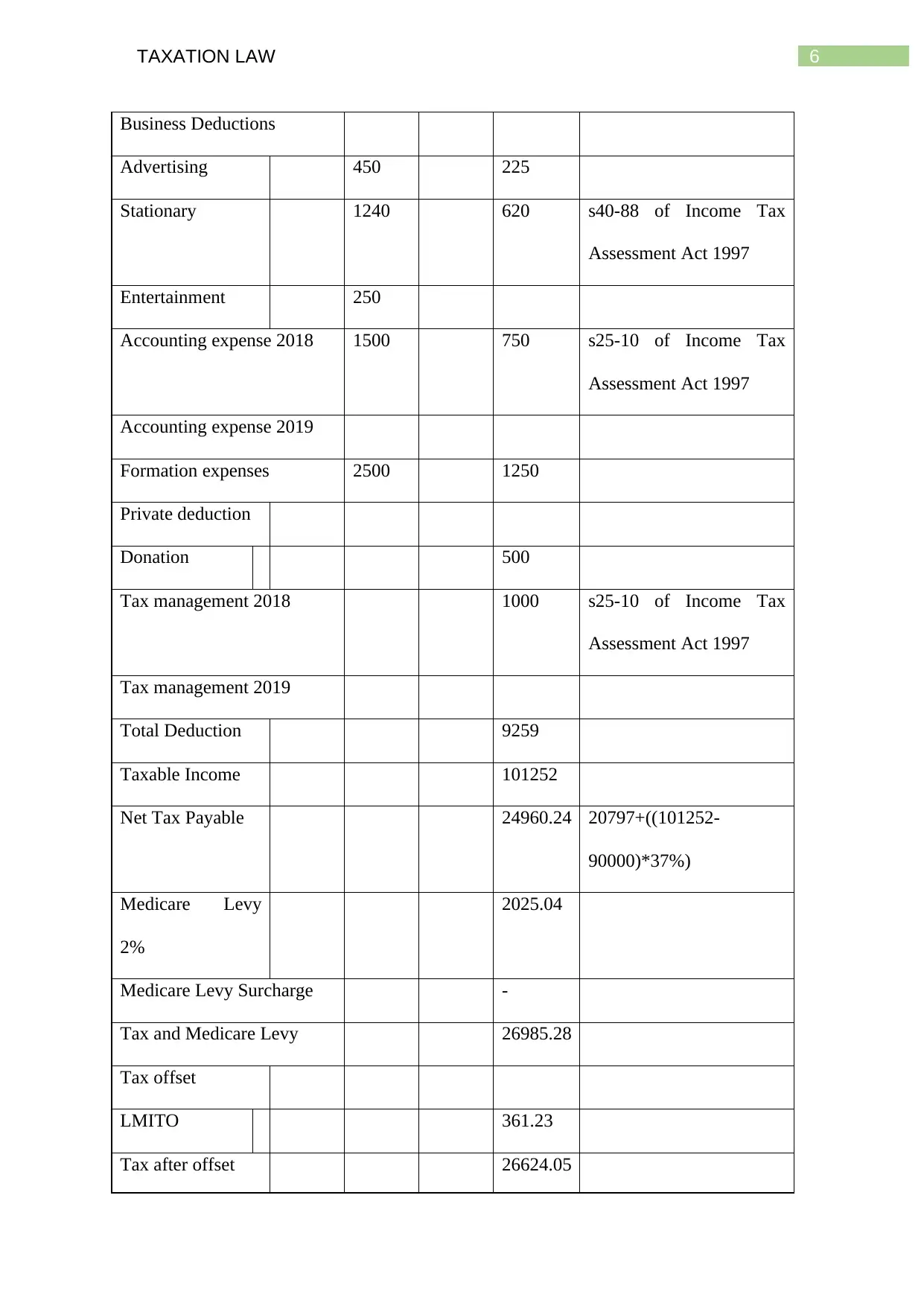

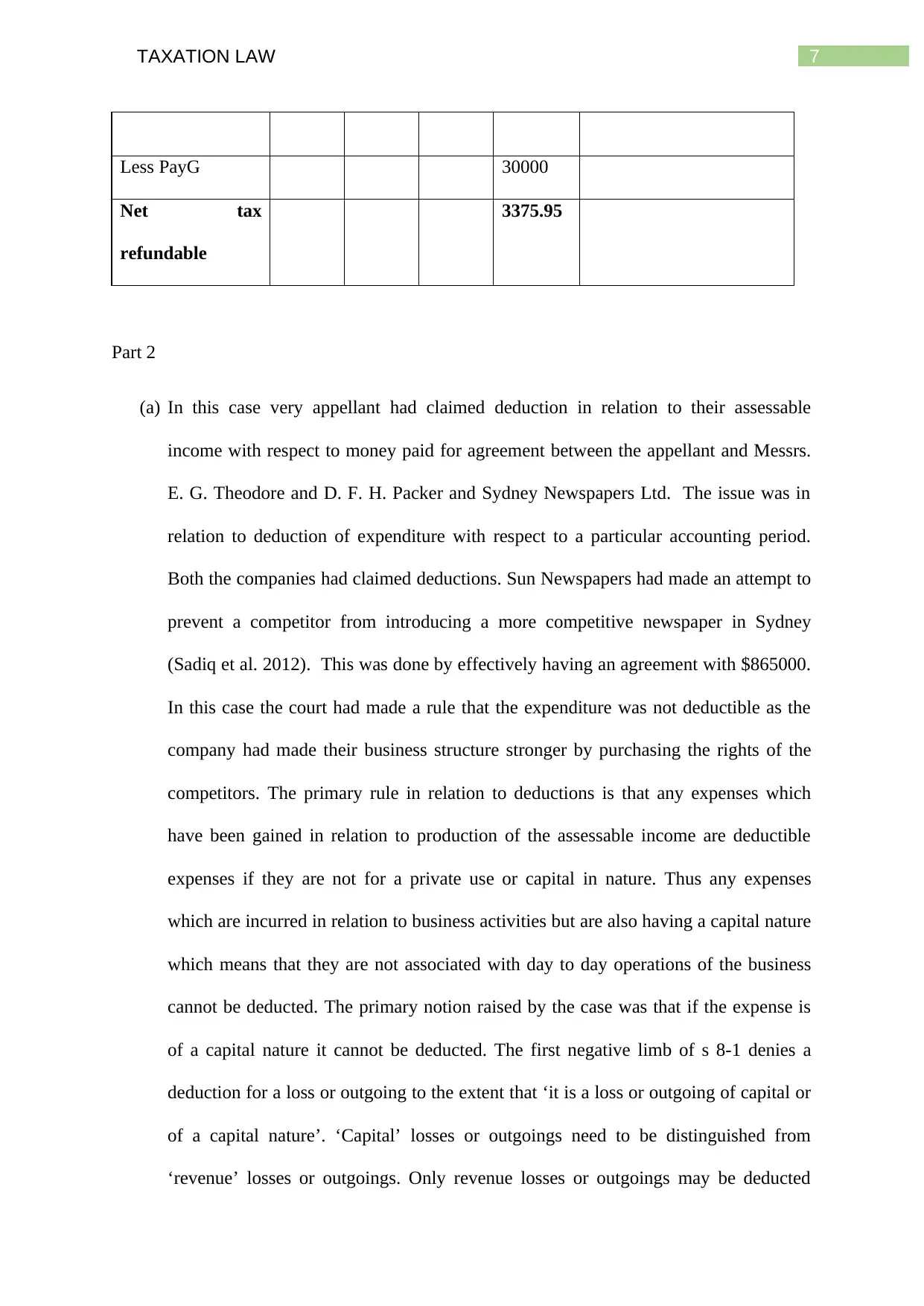

This taxation law assignment addresses the tax residency of an individual, Arun Sharma, and his tax obligations in Australia. It analyzes the relevant factors for determining residency based on the common law reside tests, including physical presence, social and economic ties, and intentions. The assignment then assesses Arun's assessable income, including salary, car allowance, and business income from partnerships, while excluding gifts and non-business related income. It details various deductions, such as those for property expenses, accounting fees, and donations, while disallowing non-deductible items like travel expenses and entertainment. The assignment provides a calculation of Arun's taxable income and net tax payable, including Medicare levy and offsets. Part 2 discusses the deductibility of expenditure, focusing on the Sun Newspapers case and the principles of capital versus revenue expenditure, including the 'once and for all' and 'business entity' tests. The assignment demonstrates an understanding of the Income Tax Assessment Act 1997 and relevant case law.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.