ACCT3002 Taxation Law Assignment: Assessable Income Issues Analysis

VerifiedAdded on 2023/04/08

|6

|683

|426

Homework Assignment

AI Summary

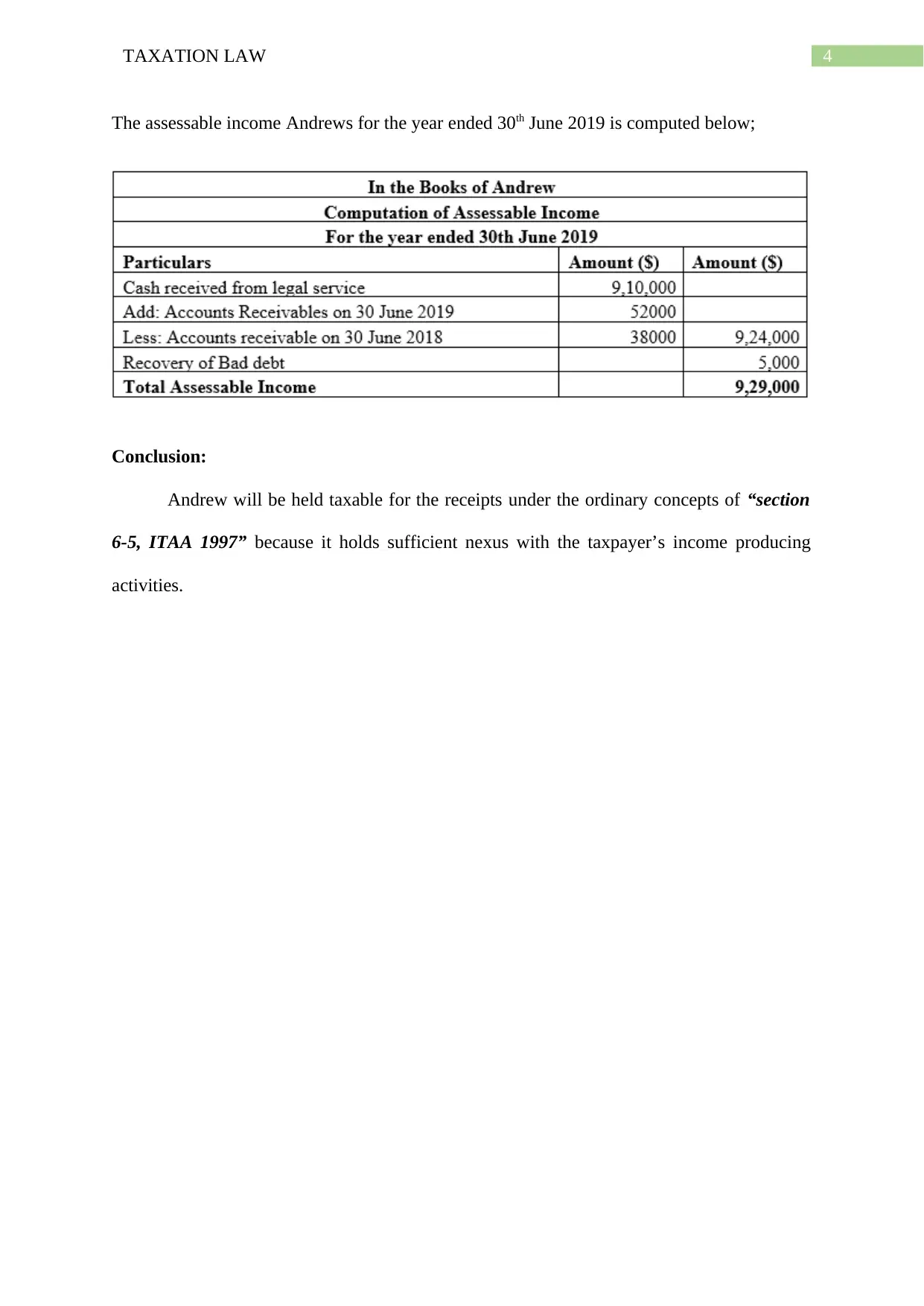

This assignment analyzes the assessable income of an individual providing legal services. It addresses the key legal issue of whether business receipts from services constitute ordinary income under section 6-5 of the ITAA 1997. The solution applies the cash method of accounting, referencing cases like Carden v F C of T and FC of T v Dixon to determine the character of income from services. The assignment also covers the tax treatment of a recovered bad debt, citing subsection 63(3) of the ITAA 1997. The conclusion affirms the taxability of receipts due to their nexus with income-producing activities, supported by relevant case law and legislative provisions. The assignment demonstrates the application of tax principles to a practical scenario, including the computation of assessable income.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.