HA3042 Taxation Law Assignment: Capital Gains and Depreciation

VerifiedAdded on 2022/12/30

|12

|2914

|54

Homework Assignment

AI Summary

This document provides a detailed solution to a taxation law assignment. The assignment addresses several key areas, including capital gains tax (CGT) implications on the sale of a family home, car, business, furniture, and paintings. It analyzes the application of relevant tax laws and small business concessions. Furthermore, the assignment explores depreciation of assets, specifically a CNC machine, and the associated deductions. The solution meticulously examines the relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and other tax rulings to provide a comprehensive understanding of the tax principles involved. The document offers a clear breakdown of each scenario, demonstrating how to apply the law to specific situations and arrive at the correct tax outcomes. This assignment is a useful resource for students studying taxation law.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

A: The capital gain on sale of the family home:....................................................................2

B: Capital gain or loss made from the car:.............................................................................2

C: The capital gain in relation to the sale of business:...........................................................3

D: The capital gain in relation to selling the furniture:..........................................................4

E: The capital gain in relation to selling the paintings:..........................................................5

Answer to question 2:.................................................................................................................6

Issues:.....................................................................................................................................6

Laws:......................................................................................................................................6

Application:............................................................................................................................7

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

A: The capital gain on sale of the family home:....................................................................2

B: Capital gain or loss made from the car:.............................................................................2

C: The capital gain in relation to the sale of business:...........................................................3

D: The capital gain in relation to selling the furniture:..........................................................4

E: The capital gain in relation to selling the paintings:..........................................................5

Answer to question 2:.................................................................................................................6

Issues:.....................................................................................................................................6

Laws:......................................................................................................................................6

Application:............................................................................................................................7

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

A: The capital gain on sale of the family home:

A gain that is characterised as capital is not always the subject of income tax within

the ordinary concepts. The income tax liability of the taxpayer takes into the account a net

capital gains as well. Capital gains tax started from 20th September 1985 onwards and brings

into the purview the capital receipts in the tax base. The assessable income of the taxpayer

includes the net capital gain (McCluskey and Franzsen 2017). There are basic exemption that

is available to the taxpayer from the capital gains or loss that is made from the CGT event

where dwelling forms the CGT asset. Main residence exemption is allowed only where the

taxpayer is an individual and under “sec 118-110 (1), ITAA 1997” the dwelling was the main

residence all through the entire period of ownership.

Jasmine bought a home during 1981 for $40,000 which presently worth $650,000

when she sold it. The home of Jasmine at first should be treated as pre-CGT asset because the

home was purchased by her before the introduction of the CGT regime. Additionally, under

“sec 118-110 (1), ITAA 1997” all through the entire period of ownership, the dwelling was

the main residence of Jasmine. Therefore, Jasmine is exempted from the capital gains tax

upon the profit made from the sale of dwelling.

B: Capital gain or loss made from the car:

To ascertain whether or not the taxpayer has made the capital gain or capital loss it is

necessary to understand whether any CGT event has occurred to the taxpayer and whether

any CGT asset is involved or not. Under “sec 102-20” a taxpayer only derives capital gain or

loss if any CGT event takes place. Under “sec 104-10(1), ITAA 1997” a “CGT Event A1”

happens when the taxpayer disposes the CGT asset (Sakurai and Braithwaite 2019). While

“sec 108-20 (2)” describes the personal use asset as the asset that is largely kept for personal

Answer to question 1:

A: The capital gain on sale of the family home:

A gain that is characterised as capital is not always the subject of income tax within

the ordinary concepts. The income tax liability of the taxpayer takes into the account a net

capital gains as well. Capital gains tax started from 20th September 1985 onwards and brings

into the purview the capital receipts in the tax base. The assessable income of the taxpayer

includes the net capital gain (McCluskey and Franzsen 2017). There are basic exemption that

is available to the taxpayer from the capital gains or loss that is made from the CGT event

where dwelling forms the CGT asset. Main residence exemption is allowed only where the

taxpayer is an individual and under “sec 118-110 (1), ITAA 1997” the dwelling was the main

residence all through the entire period of ownership.

Jasmine bought a home during 1981 for $40,000 which presently worth $650,000

when she sold it. The home of Jasmine at first should be treated as pre-CGT asset because the

home was purchased by her before the introduction of the CGT regime. Additionally, under

“sec 118-110 (1), ITAA 1997” all through the entire period of ownership, the dwelling was

the main residence of Jasmine. Therefore, Jasmine is exempted from the capital gains tax

upon the profit made from the sale of dwelling.

B: Capital gain or loss made from the car:

To ascertain whether or not the taxpayer has made the capital gain or capital loss it is

necessary to understand whether any CGT event has occurred to the taxpayer and whether

any CGT asset is involved or not. Under “sec 102-20” a taxpayer only derives capital gain or

loss if any CGT event takes place. Under “sec 104-10(1), ITAA 1997” a “CGT Event A1”

happens when the taxpayer disposes the CGT asset (Sakurai and Braithwaite 2019). While

“sec 108-20 (2)” describes the personal use asset as the asset that is largely kept for personal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

use and enjoyment but does not takes into account land or building (Thuronyi and Brooks

2016). The examples consist of;

a. TV at home

b. Bicycle

c. Mobile phone

d. Car or yacht for private use

Special rules are applied under “sec 108-20, ITAA 1997” for disregarding capital

gains and loss when under the first element of assets cost base is below $10,000 (Burkhauser,

Hahn and Wilkins 2015). The capital loss from personal use asset are simply ignored.

In 2011 Jasmine purchased a car by paying $31,000. While at the time of sale the

value of car stood $10,000. Under “sec 108-20 (2)” the car of Jasmine is classified as

personal use asset. A CGT Event A1 happened when the car was sold by Jasmine. Under the

special rules of “sec 108-20, ITAA 1997” Jasmine must disregard the capital loss since it

constitute a personal use asset.

C: The capital gain in relation to the sale of business:

Concession is available to the small businesses under “Division 152” (Evans, Minas

and Lim 2015). The basic conditions for the accessing the small business concessions are as

follows;

a. The entity should be the small business with aggregate turnover in the present or

previous year not exceeding greater than $2million or the net value of the assets not

exceeding $6 million.

b. The CGT asset is ought to be an active asset

There are four small business relief available to taxpayers

use and enjoyment but does not takes into account land or building (Thuronyi and Brooks

2016). The examples consist of;

a. TV at home

b. Bicycle

c. Mobile phone

d. Car or yacht for private use

Special rules are applied under “sec 108-20, ITAA 1997” for disregarding capital

gains and loss when under the first element of assets cost base is below $10,000 (Burkhauser,

Hahn and Wilkins 2015). The capital loss from personal use asset are simply ignored.

In 2011 Jasmine purchased a car by paying $31,000. While at the time of sale the

value of car stood $10,000. Under “sec 108-20 (2)” the car of Jasmine is classified as

personal use asset. A CGT Event A1 happened when the car was sold by Jasmine. Under the

special rules of “sec 108-20, ITAA 1997” Jasmine must disregard the capital loss since it

constitute a personal use asset.

C: The capital gain in relation to the sale of business:

Concession is available to the small businesses under “Division 152” (Evans, Minas

and Lim 2015). The basic conditions for the accessing the small business concessions are as

follows;

a. The entity should be the small business with aggregate turnover in the present or

previous year not exceeding greater than $2million or the net value of the assets not

exceeding $6 million.

b. The CGT asset is ought to be an active asset

There are four small business relief available to taxpayers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

a. 15-year exemption: The full amount of capital gains is exempted on sale of CGT

asset where the asset is owned for at least 15 years and taxpayers is 55 years or older.

b. 50% reduction: On meeting the eligibility criteria a 50% reduction in capital gain is

allowed following a general 50% discount percentage.

c. Retirement concession: The taxpayers must disregard the capital gain on the sale of

CGT asset given the sales earnings are used for retirement purpose.

d. Roll-over relief: The capital gains is deferred when the when the taxpayer acquires a

replacement asset.

As Jasmine is planning to return UK, she is presently retiring from her cleaning

business and sold the business to a buyer for $125,000. Jasmine sold the asset for $65,000

while her business goodwill was sold for $60,000. Referring to “Division-152” Jasmine

qualifies for the small business concession as her total turnover does not exceeds greater than

$2million and the value of her business asset is not greater than $6million. Jasmine can avail

15-year CGT exemption from the disposal of her asset since she has held the asset for 15

years and currently ages more than 55 years.

The “Taxation ruling of TR 1999/16” explains that where a business is permanently

ceased the goodwill of the business is lost or destroyed. The sale of goodwill by Jasmine

gives rise to “CGT event C1” since the business ceased permanently. Under the “SubDiv-

152-C” Jasmine can avail 50% CGT reduction from CGT following the sale of her business

her goodwill.

D: The capital gain in relation to selling the furniture:

A furniture that was bought by Jasmine for $2,000 was eventually sold for $5,000.

According to “section 118-10(3), ITAA 1997” there are special rules that are applied on the

personal use asset, capital gains and losses must be ignored when the first element of personal

a. 15-year exemption: The full amount of capital gains is exempted on sale of CGT

asset where the asset is owned for at least 15 years and taxpayers is 55 years or older.

b. 50% reduction: On meeting the eligibility criteria a 50% reduction in capital gain is

allowed following a general 50% discount percentage.

c. Retirement concession: The taxpayers must disregard the capital gain on the sale of

CGT asset given the sales earnings are used for retirement purpose.

d. Roll-over relief: The capital gains is deferred when the when the taxpayer acquires a

replacement asset.

As Jasmine is planning to return UK, she is presently retiring from her cleaning

business and sold the business to a buyer for $125,000. Jasmine sold the asset for $65,000

while her business goodwill was sold for $60,000. Referring to “Division-152” Jasmine

qualifies for the small business concession as her total turnover does not exceeds greater than

$2million and the value of her business asset is not greater than $6million. Jasmine can avail

15-year CGT exemption from the disposal of her asset since she has held the asset for 15

years and currently ages more than 55 years.

The “Taxation ruling of TR 1999/16” explains that where a business is permanently

ceased the goodwill of the business is lost or destroyed. The sale of goodwill by Jasmine

gives rise to “CGT event C1” since the business ceased permanently. Under the “SubDiv-

152-C” Jasmine can avail 50% CGT reduction from CGT following the sale of her business

her goodwill.

D: The capital gain in relation to selling the furniture:

A furniture that was bought by Jasmine for $2,000 was eventually sold for $5,000.

According to “section 118-10(3), ITAA 1997” there are special rules that are applied on the

personal use asset, capital gains and losses must be ignored when the first element of personal

5TAXATION LAW

use asset cost base is not higher than $10,000 (Harding 2014). Ideally, in case of Jasmine, the

cost price of furniture under the first element of “section 118-10(3), ITAA 1997” does not

exceed $10,000. The capital gains made from the sale of furniture must be disregarded by

Jasmine in this case.

E: The capital gain in relation to selling the paintings:

The description of collectibles under “sec 108-10(2), ITAA 1997” includes;

a. An antique, artwork, coin or medallion or jewellery

b. A manuscript or book, rare folio; or

c. A first day cover or the postage stamp

That the taxpayer has principally held for his own enjoyment and usage.

Special rules are applicable on the collectibles. This includes;

a. Capital gains and losses under the “sec 118-10 (1), ITAA 1997” must be disregarded

when the first element of the collectible’s cost base is lower than $500.

b. The quarantining rule under “sec108-10 (1), ITAA 1997” explains that the capital loss

from the collectibles is only permitted to use it for reducing the capital gains from

collectibles (Zucman 2014).

During the year Jasmine held numerous paintings. The paintings has been classified as the

collectible under “sec 108-10(2), ITAA 1997”. Jasmine sold all her paintings for $35,000

however no single painting had the cost greater than $500. The capital gains that is made by

Jasmine upon selling the painting is ignored under “sec 118-10 (1), ITAA 1997” since the

first element of the painting’s cost base is lower than $500.

use asset cost base is not higher than $10,000 (Harding 2014). Ideally, in case of Jasmine, the

cost price of furniture under the first element of “section 118-10(3), ITAA 1997” does not

exceed $10,000. The capital gains made from the sale of furniture must be disregarded by

Jasmine in this case.

E: The capital gain in relation to selling the paintings:

The description of collectibles under “sec 108-10(2), ITAA 1997” includes;

a. An antique, artwork, coin or medallion or jewellery

b. A manuscript or book, rare folio; or

c. A first day cover or the postage stamp

That the taxpayer has principally held for his own enjoyment and usage.

Special rules are applicable on the collectibles. This includes;

a. Capital gains and losses under the “sec 118-10 (1), ITAA 1997” must be disregarded

when the first element of the collectible’s cost base is lower than $500.

b. The quarantining rule under “sec108-10 (1), ITAA 1997” explains that the capital loss

from the collectibles is only permitted to use it for reducing the capital gains from

collectibles (Zucman 2014).

During the year Jasmine held numerous paintings. The paintings has been classified as the

collectible under “sec 108-10(2), ITAA 1997”. Jasmine sold all her paintings for $35,000

however no single painting had the cost greater than $500. The capital gains that is made by

Jasmine upon selling the painting is ignored under “sec 118-10 (1), ITAA 1997” since the

first element of the painting’s cost base is lower than $500.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

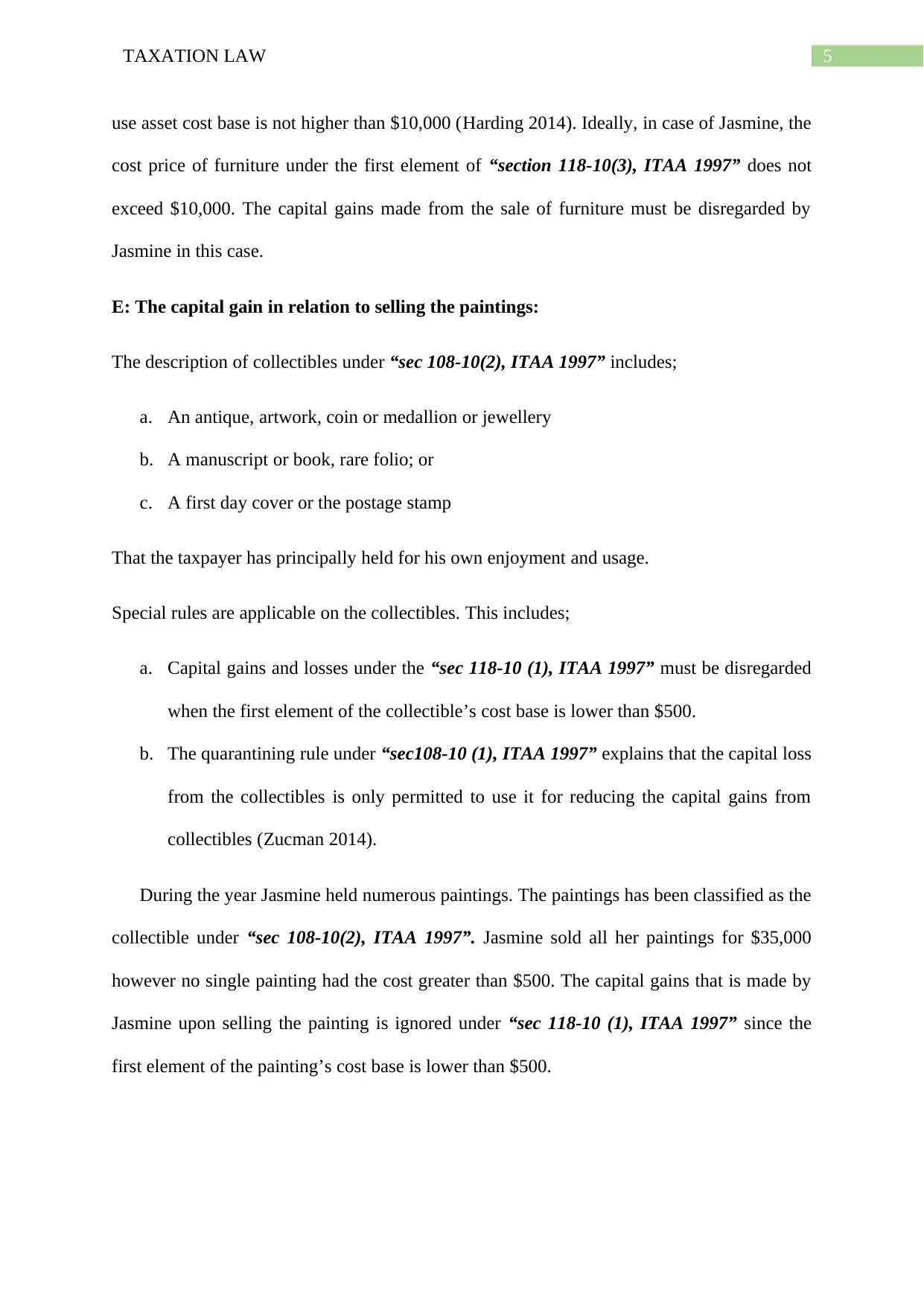

While there was one exception where one painting that Jasmine bought for $1,000 was

sold for $5,000. The sale of painting has given rise to capital gains. As a result, a capital gains

tax liability will be imposed from the capital gains made from the painting.

Answer to question 2:

Issues:

Is the taxpayer permitted to claim deduction equivalent to the “decline in value” of the

depreciating asset which is held under “sec 40-25, ITAA 1997”?

Laws:

The provision of general deduction forbids a deduction for the capital item under “sec

8-1 (2) (a), ITAA 1997”. A taxpayer is permitted to claim deduction that is equal to the

“decline in value” relating to a “depreciating asset” which is held under “sec 40-25, ITAA

1997”. “Sec 40-30 (1), ITAA 1997” defines the depreciating asset. An asset that has very

limited effective life and it is practically anticipated to fall in terms of value based on the time

of its usage (Duffy and Morgan 2018). In order to claim deduction under “sec 40-25” for the

“depreciating asset” it is vital to ascertain when the taxpayer has held the asset and a

deduction equal to its fall in value after considering for taxable purpose. As per “sec 40-25

(2), ITAA 1997” a decline in value of the asset is only permitted for claim in respect of the

While there was one exception where one painting that Jasmine bought for $1,000 was

sold for $5,000. The sale of painting has given rise to capital gains. As a result, a capital gains

tax liability will be imposed from the capital gains made from the painting.

Answer to question 2:

Issues:

Is the taxpayer permitted to claim deduction equivalent to the “decline in value” of the

depreciating asset which is held under “sec 40-25, ITAA 1997”?

Laws:

The provision of general deduction forbids a deduction for the capital item under “sec

8-1 (2) (a), ITAA 1997”. A taxpayer is permitted to claim deduction that is equal to the

“decline in value” relating to a “depreciating asset” which is held under “sec 40-25, ITAA

1997”. “Sec 40-30 (1), ITAA 1997” defines the depreciating asset. An asset that has very

limited effective life and it is practically anticipated to fall in terms of value based on the time

of its usage (Duffy and Morgan 2018). In order to claim deduction under “sec 40-25” for the

“depreciating asset” it is vital to ascertain when the taxpayer has held the asset and a

deduction equal to its fall in value after considering for taxable purpose. As per “sec 40-25

(2), ITAA 1997” a decline in value of the asset is only permitted for claim in respect of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

depreciating assets which is used by taxpayer for taxable purpose (Faccio and Xu 2015).

Accordingly, under “sec 40-25 (7)”, the taxable purpose usually exist when the taxpayer uses

the asset for generating income.

Under the “sec 40-60 (1), ITAA 1997”, a depreciating asset that the taxpayer has

started to hold begins to decline in terms of value when the start time happens (Auerbach and

Hassett 2015). Most importantly under “sec 40-60 (2), ITAA 1997” the start time of the

depreciating asset begins when the first use of asset is made by the taxpayer or has installed

the asset for ready use.

The taxpayers or the holder of assets must know that the basis of depreciation is based

on the cost of the depreciating asset and the rules for ascertaining the asset cost is given under

“Subdivision 40-C” (Armenter and Hnatkovska 2017). The cost will not only take into the

account the purchase price of the asset but includes the incidental costs of installation and

delivery. Furthermore, the decision given by federal court in “Broken Hill Pty Co Ltd v FCT

(1970)” held that minor expenditure that occurs in rearranging or removing the other plant for

accommodating the new plant should be included into the cost as well.

“Section 40-175” specifies that the cost of depreciating asset comprises of two

elements. Accordingly under the “sub-section 40-180 (1)” the first element generally takes

into the account the purchase price of asset. Whereas “sec 40-190” is mainly related with the

second element which widely takes into account the costs of delivery, installation cost and

cost of improvement made in the asset.

Application:

John on 1st November 2014 went to Germany to purchase CNC machine. John

purchased the machine at an acquisition value of $300,000. The CNC machine is referred as

depreciating asset under the legislative provision of “sec 40-30 (1), ITAA 1997”. This is

depreciating assets which is used by taxpayer for taxable purpose (Faccio and Xu 2015).

Accordingly, under “sec 40-25 (7)”, the taxable purpose usually exist when the taxpayer uses

the asset for generating income.

Under the “sec 40-60 (1), ITAA 1997”, a depreciating asset that the taxpayer has

started to hold begins to decline in terms of value when the start time happens (Auerbach and

Hassett 2015). Most importantly under “sec 40-60 (2), ITAA 1997” the start time of the

depreciating asset begins when the first use of asset is made by the taxpayer or has installed

the asset for ready use.

The taxpayers or the holder of assets must know that the basis of depreciation is based

on the cost of the depreciating asset and the rules for ascertaining the asset cost is given under

“Subdivision 40-C” (Armenter and Hnatkovska 2017). The cost will not only take into the

account the purchase price of the asset but includes the incidental costs of installation and

delivery. Furthermore, the decision given by federal court in “Broken Hill Pty Co Ltd v FCT

(1970)” held that minor expenditure that occurs in rearranging or removing the other plant for

accommodating the new plant should be included into the cost as well.

“Section 40-175” specifies that the cost of depreciating asset comprises of two

elements. Accordingly under the “sub-section 40-180 (1)” the first element generally takes

into the account the purchase price of asset. Whereas “sec 40-190” is mainly related with the

second element which widely takes into account the costs of delivery, installation cost and

cost of improvement made in the asset.

Application:

John on 1st November 2014 went to Germany to purchase CNC machine. John

purchased the machine at an acquisition value of $300,000. The CNC machine is referred as

depreciating asset under the legislative provision of “sec 40-30 (1), ITAA 1997”. This is

8TAXATION LAW

because the CNC machine carries the limited effective life which is practically expected to

fall in value on the basis of its usage for taxable purpose.

After importing the machine from Germany to Australia, the machine was installed as

ready for use on 15th January 2015 for taxable purpose. As per “sec 40-25 (2), ITAA 1997” a

decline in value of the CNC machine is only permitted for claim by John in respect of its

taxable purpose. Accordingly, under “sec 40-25 (7)”, the taxable purpose usually exist when

John first started using the asset for generating income (Saez and Stantcheva 2018). For

depreciation purpose, under “sec 40-60 (1), ITAA 1997” the start time of the CNC machine

commences from 15th January 2015 since the machine was installed as ready for use for

taxable purpose from the aforementioned date.

On 1st February 2015, John incurred an added cost when he installed a guiding rod on

the machine so that the performance of the machine becomes more effective. Citing the

decision of “FC of T v Broken Hill Pty Co Ltd (1970)” to determine the overall cost base of

CNC machine under “Sub-div 40-C”, John must include the expenses incurred installing a

guiding rod in the machine together with its purchase price.

By following the “sec 40-25, ITAA 1997” a deduction for decline in value of CNC

machine can be claimed by John which is used for taxable purpose. Accordingly, under “sec

40-25 (7)”, the taxable purpose is existent in case of John when the he started the asset for

generating income. The first element of cost base under “sec 110-25, ITAA 1997” includes

the purchase price of CNC machine. While under the “sec 40-190” the second element of

CNC machine would include the cost of installation, incidental cost of inspecting the machine

and capital improvement cost of adding the guiding rod to increase the value of machine.

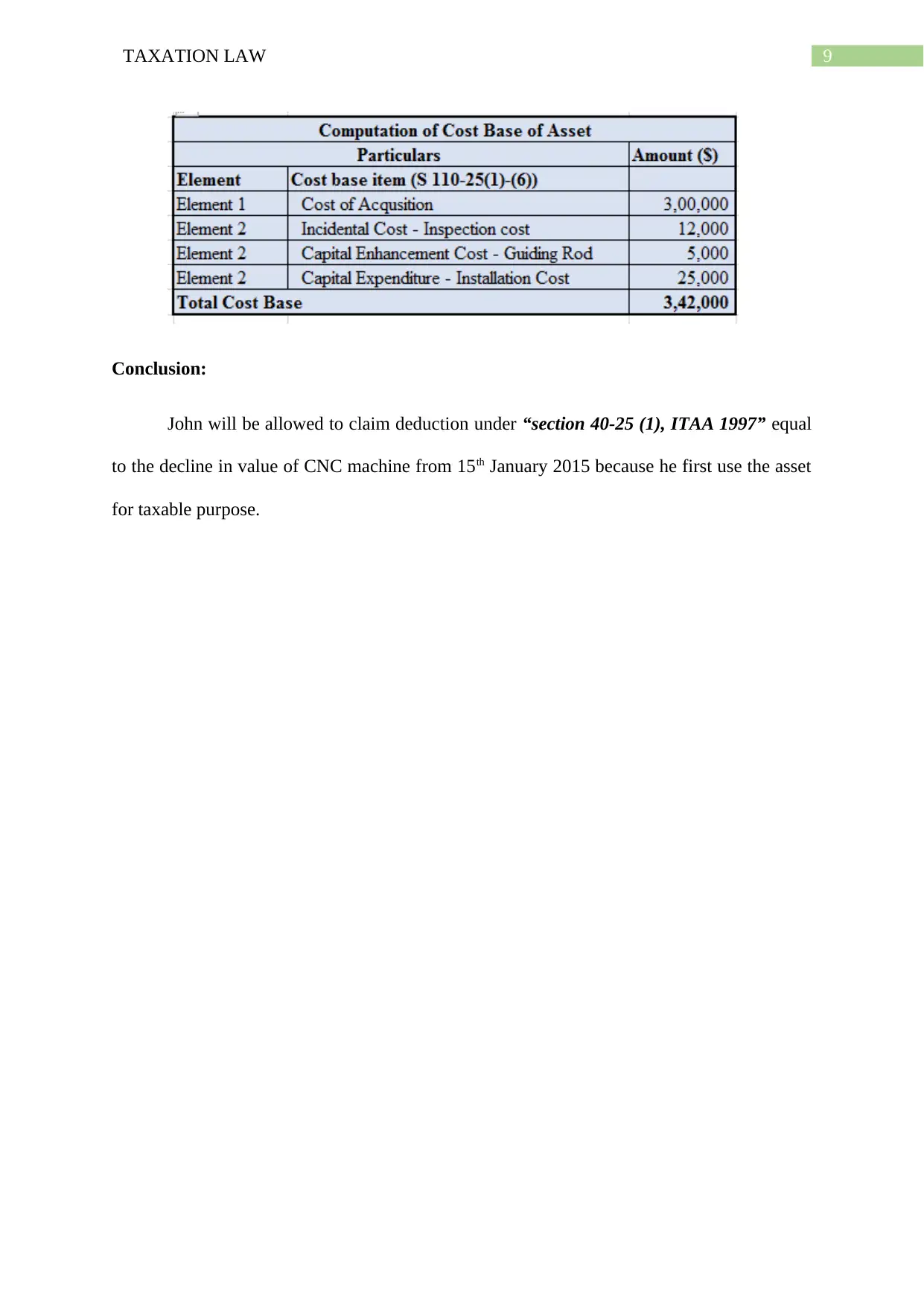

The cost base of machine for depreciation purpose is computed below;

because the CNC machine carries the limited effective life which is practically expected to

fall in value on the basis of its usage for taxable purpose.

After importing the machine from Germany to Australia, the machine was installed as

ready for use on 15th January 2015 for taxable purpose. As per “sec 40-25 (2), ITAA 1997” a

decline in value of the CNC machine is only permitted for claim by John in respect of its

taxable purpose. Accordingly, under “sec 40-25 (7)”, the taxable purpose usually exist when

John first started using the asset for generating income (Saez and Stantcheva 2018). For

depreciation purpose, under “sec 40-60 (1), ITAA 1997” the start time of the CNC machine

commences from 15th January 2015 since the machine was installed as ready for use for

taxable purpose from the aforementioned date.

On 1st February 2015, John incurred an added cost when he installed a guiding rod on

the machine so that the performance of the machine becomes more effective. Citing the

decision of “FC of T v Broken Hill Pty Co Ltd (1970)” to determine the overall cost base of

CNC machine under “Sub-div 40-C”, John must include the expenses incurred installing a

guiding rod in the machine together with its purchase price.

By following the “sec 40-25, ITAA 1997” a deduction for decline in value of CNC

machine can be claimed by John which is used for taxable purpose. Accordingly, under “sec

40-25 (7)”, the taxable purpose is existent in case of John when the he started the asset for

generating income. The first element of cost base under “sec 110-25, ITAA 1997” includes

the purchase price of CNC machine. While under the “sec 40-190” the second element of

CNC machine would include the cost of installation, incidental cost of inspecting the machine

and capital improvement cost of adding the guiding rod to increase the value of machine.

The cost base of machine for depreciation purpose is computed below;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Conclusion:

John will be allowed to claim deduction under “section 40-25 (1), ITAA 1997” equal

to the decline in value of CNC machine from 15th January 2015 because he first use the asset

for taxable purpose.

Conclusion:

John will be allowed to claim deduction under “section 40-25 (1), ITAA 1997” equal

to the decline in value of CNC machine from 15th January 2015 because he first use the asset

for taxable purpose.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Armenter, R. and Hnatkovska, V., 2017. Taxes and capital structure: Understanding firms’

savings. Journal of Monetary Economics, 87, pp.13-33.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Duffy, C. and Morgan, J., 2018. For personal use only. NSW, 2292, p.17.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Harding, M., 2014. Personal tax treatment of company cars and commuting expenses.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Saez, E. and Stantcheva, S., 2018. A simpler theory of optimal capital taxation. Journal of

Public Economics, 162, pp.120-142.

Sakurai, Y. and Braithwaite, V., 2019. Taxpayers' perceptions of the ideal tax adviser:

Playing safe or saving dollars?. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

References:

Armenter, R. and Hnatkovska, V., 2017. Taxes and capital structure: Understanding firms’

savings. Journal of Monetary Economics, 87, pp.13-33.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Duffy, C. and Morgan, J., 2018. For personal use only. NSW, 2292, p.17.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Harding, M., 2014. Personal tax treatment of company cars and commuting expenses.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

Saez, E. and Stantcheva, S., 2018. A simpler theory of optimal capital taxation. Journal of

Public Economics, 162, pp.120-142.

Sakurai, Y. and Braithwaite, V., 2019. Taxpayers' perceptions of the ideal tax adviser:

Playing safe or saving dollars?. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

11TAXATION LAW

Zucman, G., 2014. Taxing across borders: Tracking personal wealth and corporate

profits. Journal of economic perspectives, 28(4), pp.121-48.

Zucman, G., 2014. Taxing across borders: Tracking personal wealth and corporate

profits. Journal of economic perspectives, 28(4), pp.121-48.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.