Taxation Law Assignment: Fringe Benefits and Capital Gains

VerifiedAdded on 2023/03/31

|8

|2301

|298

Homework Assignment

AI Summary

This taxation law assignment analyzes two main scenarios. The first focuses on car fringe benefits, examining the tax liability of an employer providing a car to an employee, comparing the statutory and log book methods for calculating the taxable value. It recommends the log book method for the employer. The second part delves into capital gains tax, addressing a case involving an individual planning for retirement. This section analyzes the tax implications of selling a house (including a forfeited deposit), a painting, a luxury yacht, and shares, detailing the relevant CGT events, the treatment of personal use assets, and the application of carry-forward losses. The assignment provides a comprehensive overview of tax concepts and their practical application.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................4

Answer to question A:...............................................................................................4

Answer to question B:...............................................................................................6

Answer to question C:...............................................................................................6

References:..................................................................................................................7

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................4

Answer to question A:...............................................................................................4

Answer to question B:...............................................................................................6

Answer to question C:...............................................................................................6

References:..................................................................................................................7

2TAXATION LAW

Answer to question 1:

Issues:

The central problem that will be discussed in this segment is the tax liability of

car fringe benefit that was given to the employee here within the definition given in

the “s7 (1), FBTAA 1986”.

Rule:

The rule that is given in the fringe benefit tax legislation is that fringe benefit

must be viewed as the payment that is given to the employee but most notably those

benefits are not in the form of salary or wages (Black 2018). The legislation of the

FBT explain that the fringe benefit is generally given to the employee in relation to

the employment. One should denote that the benefit is given to the employee

because they are engaged in the employment. The liability of paying the fringe

benefit tax is generally on the employer.

An important explanation has been made in the “sec7(1), FBTAA 1986” that

the car fringe benefit is very much common when the employer is giving the car to

the employee for making his or private usage (Barry and Caron 2015). The car that

is held by them is generally regarded as the car that is owned or leased. On any

given day the fringe benefit relating to car happens when the car is not at the

premises of the employer and the employee is given the complete permission of

using the car for their private purpose. The general rule explains that using the car

for travelling purpose or making private use is regarded as the car fringe benefit.

The taxable charge of the car fringe benefit can be attained by using either of

the following method. The methods generally involve the statutory method and the

operating cost method. Under the “s9-FBTA Act 1986 (cth)” the amount of tax

relating to the car fringe benefit is computed by using the statutory rate which is later

multiplied by the base value of the car (Shiftan, Albert and Keinan 2014). On the

other hand, under the “s10-FBTA Act 1986 (cth)” the chargeable value of the car

fringe benefit under the operating cost method represents the total cost associated to

running the car throughout the fringe benefit tax year (Gutiérrez‐i‐Puigarnau and Van

Ommeren 2013). The percentage of running cost varies depending upon the actual

or the private use of the car made. It is noteworthy to denote that the lower the

incidence of actual use of the car represents the lower the taxable value of the

benefits.

Application:

The case study clearly furnishes the information that the employer here

Spiceco Pty Ltd has given the car to the employee for making the private use of it.

There were several expenses that were occurred for the car usage which ranges

from repairs, fuel and insurance. The overall business use of the car stood 70% by

the employee while the rest portion of the car was for the private purpose.

As the car has been given by Spiceco Pty Ltd the car fringe benefit has

occurred under the “s7 (1), FBTAA 1986” for the employer. The fringe benefit has

happened for the employer because it was given to Lucinda out of the employment

relationship. There was adequate amount of nexus present for the services that were

rendered by Lucinda and the benefit that was given to her (Scott, Currie and

Tivendale 2014). The tax liability of the car fringe benefit falls on Specico Pty Ltd

Answer to question 1:

Issues:

The central problem that will be discussed in this segment is the tax liability of

car fringe benefit that was given to the employee here within the definition given in

the “s7 (1), FBTAA 1986”.

Rule:

The rule that is given in the fringe benefit tax legislation is that fringe benefit

must be viewed as the payment that is given to the employee but most notably those

benefits are not in the form of salary or wages (Black 2018). The legislation of the

FBT explain that the fringe benefit is generally given to the employee in relation to

the employment. One should denote that the benefit is given to the employee

because they are engaged in the employment. The liability of paying the fringe

benefit tax is generally on the employer.

An important explanation has been made in the “sec7(1), FBTAA 1986” that

the car fringe benefit is very much common when the employer is giving the car to

the employee for making his or private usage (Barry and Caron 2015). The car that

is held by them is generally regarded as the car that is owned or leased. On any

given day the fringe benefit relating to car happens when the car is not at the

premises of the employer and the employee is given the complete permission of

using the car for their private purpose. The general rule explains that using the car

for travelling purpose or making private use is regarded as the car fringe benefit.

The taxable charge of the car fringe benefit can be attained by using either of

the following method. The methods generally involve the statutory method and the

operating cost method. Under the “s9-FBTA Act 1986 (cth)” the amount of tax

relating to the car fringe benefit is computed by using the statutory rate which is later

multiplied by the base value of the car (Shiftan, Albert and Keinan 2014). On the

other hand, under the “s10-FBTA Act 1986 (cth)” the chargeable value of the car

fringe benefit under the operating cost method represents the total cost associated to

running the car throughout the fringe benefit tax year (Gutiérrez‐i‐Puigarnau and Van

Ommeren 2013). The percentage of running cost varies depending upon the actual

or the private use of the car made. It is noteworthy to denote that the lower the

incidence of actual use of the car represents the lower the taxable value of the

benefits.

Application:

The case study clearly furnishes the information that the employer here

Spiceco Pty Ltd has given the car to the employee for making the private use of it.

There were several expenses that were occurred for the car usage which ranges

from repairs, fuel and insurance. The overall business use of the car stood 70% by

the employee while the rest portion of the car was for the private purpose.

As the car has been given by Spiceco Pty Ltd the car fringe benefit has

occurred under the “s7 (1), FBTAA 1986” for the employer. The fringe benefit has

happened for the employer because it was given to Lucinda out of the employment

relationship. There was adequate amount of nexus present for the services that were

rendered by Lucinda and the benefit that was given to her (Scott, Currie and

Tivendale 2014). The tax liability of the car fringe benefit falls on Specico Pty Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

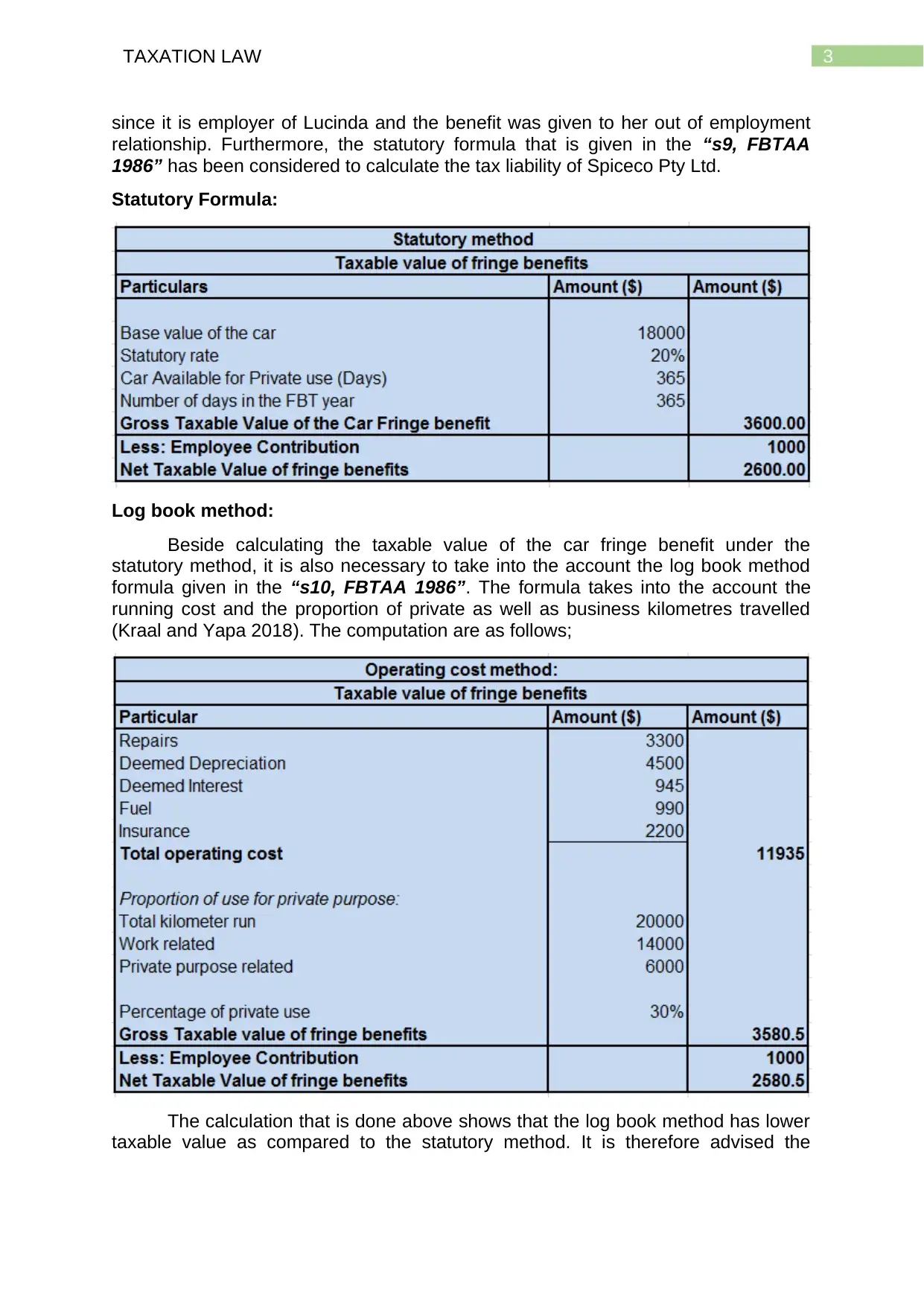

since it is employer of Lucinda and the benefit was given to her out of employment

relationship. Furthermore, the statutory formula that is given in the “s9, FBTAA

1986” has been considered to calculate the tax liability of Spiceco Pty Ltd.

Statutory Formula:

Log book method:

Beside calculating the taxable value of the car fringe benefit under the

statutory method, it is also necessary to take into the account the log book method

formula given in the “s10, FBTAA 1986”. The formula takes into the account the

running cost and the proportion of private as well as business kilometres travelled

(Kraal and Yapa 2018). The computation are as follows;

The calculation that is done above shows that the log book method has lower

taxable value as compared to the statutory method. It is therefore advised the

since it is employer of Lucinda and the benefit was given to her out of employment

relationship. Furthermore, the statutory formula that is given in the “s9, FBTAA

1986” has been considered to calculate the tax liability of Spiceco Pty Ltd.

Statutory Formula:

Log book method:

Beside calculating the taxable value of the car fringe benefit under the

statutory method, it is also necessary to take into the account the log book method

formula given in the “s10, FBTAA 1986”. The formula takes into the account the

running cost and the proportion of private as well as business kilometres travelled

(Kraal and Yapa 2018). The computation are as follows;

The calculation that is done above shows that the log book method has lower

taxable value as compared to the statutory method. It is therefore advised the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

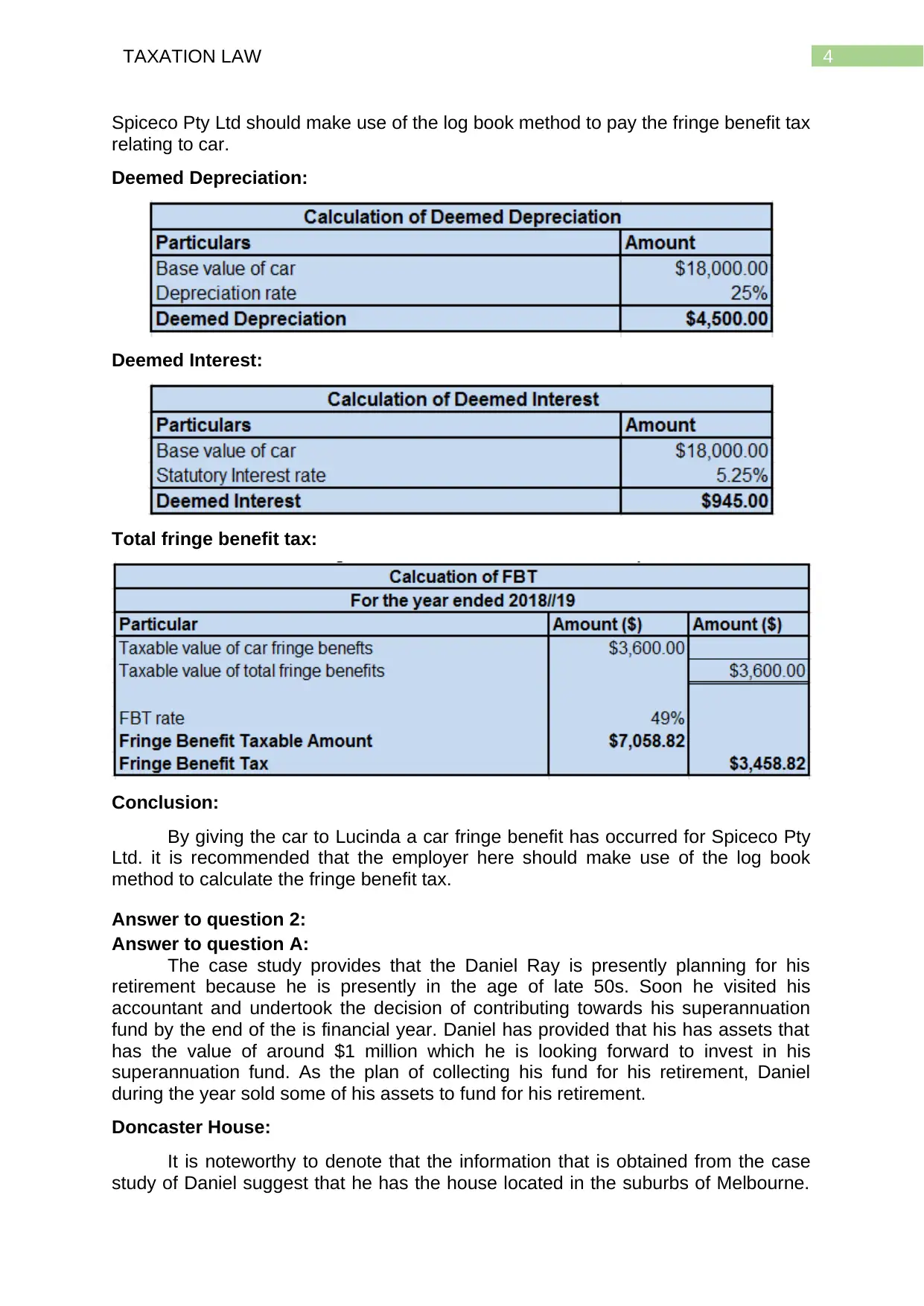

Spiceco Pty Ltd should make use of the log book method to pay the fringe benefit tax

relating to car.

Deemed Depreciation:

Deemed Interest:

Total fringe benefit tax:

Conclusion:

By giving the car to Lucinda a car fringe benefit has occurred for Spiceco Pty

Ltd. it is recommended that the employer here should make use of the log book

method to calculate the fringe benefit tax.

Answer to question 2:

Answer to question A:

The case study provides that the Daniel Ray is presently planning for his

retirement because he is presently in the age of late 50s. Soon he visited his

accountant and undertook the decision of contributing towards his superannuation

fund by the end of the is financial year. Daniel has provided that his has assets that

has the value of around $1 million which he is looking forward to invest in his

superannuation fund. As the plan of collecting his fund for his retirement, Daniel

during the year sold some of his assets to fund for his retirement.

Doncaster House:

It is noteworthy to denote that the information that is obtained from the case

study of Daniel suggest that he has the house located in the suburbs of Melbourne.

Spiceco Pty Ltd should make use of the log book method to pay the fringe benefit tax

relating to car.

Deemed Depreciation:

Deemed Interest:

Total fringe benefit tax:

Conclusion:

By giving the car to Lucinda a car fringe benefit has occurred for Spiceco Pty

Ltd. it is recommended that the employer here should make use of the log book

method to calculate the fringe benefit tax.

Answer to question 2:

Answer to question A:

The case study provides that the Daniel Ray is presently planning for his

retirement because he is presently in the age of late 50s. Soon he visited his

accountant and undertook the decision of contributing towards his superannuation

fund by the end of the is financial year. Daniel has provided that his has assets that

has the value of around $1 million which he is looking forward to invest in his

superannuation fund. As the plan of collecting his fund for his retirement, Daniel

during the year sold some of his assets to fund for his retirement.

Doncaster House:

It is noteworthy to denote that the information that is obtained from the case

study of Daniel suggest that he has the house located in the suburbs of Melbourne.

5TAXATION LAW

He has been living in the house for thirty years and in the presently tax year he sold

the house for $865,000. A sum of $15,000 was also paid by Daniel to his real estate

agent and later a buyer agreed to purchase the house. The buyer had deposited the

amount of $85,000 for the property. But in the recent change of events the buyer

decided against the purchase of the Doncaster house. The amount that was

deposited by the buyer was eventually forfeited to Daniel.

It is worth mentioning that “sec-104-150” provides the explanation regarding

the circumstances when there is a forfeiture of deposit (Marks and Bernard 2015).

Whenever there is a forfeiture of deposit a CGT event H1 come about in scenario.

This kind of event normally occurs when the prospective buyer makes a deposit on

the prospective sale or the other transaction is forfeited since the transaction failed to

proceed further.

From the aforementioned situation the “CGT event H1” has occurred for Daniel

under “s-104-150” because the buyer that agreed to purchase the house eventually

decided against proceeding the transaction and eventually the deposit was forfeited

(Poterba and Weisbenner 2014).

Painting by Margaret Preston:

A CGT event A1 under “sec 104-10” happens when the sale of the CGT

asset happens. This is generally applicable to the sale of the assets that is

purchased following 19/09/1985 (Poterba 2014). The taxpayers should denote that in

order to originate the CGT event A1 the CGT asset should be disposed to the

another entity. It is noteworthy to denote that the collectables are something that is

kept by the taxpayer for their personal purpose and enjoyment. There are items that

are listed in the s108-10 which includes, antiques, works of art, jewellery,

manuscripts and rare stamps. It is also necessary to denote that the taxpayers are

required to declare the capital gains that is made by them for taxable purpose in their

assessable income. According to the sec 6-10 the capital gains are considered

taxable as the statutory income and the gains are considered taxable as income

under “sec 105-5(1)”.

The evidence that is gained from situation of Daniel here it is understood that

the artistic piece of painting by Margaret Preston was kept under his possession.

The painting was mainly held by Daniel for his use and enjoyment purpose. Later in

the year 2019 the painting was sold by Daniel for $125,000 in the auction which he

originally purchased on the sept 20 1985 for an acquisition value of $15,000. It is

worth mentioning that the painting should be treated as the post-CGT asset because

it was bought after the scheme of CGT was introduced.

There is a CGT event A1 under “sec 104-10” when Daniel sold the painting.

It is noteworthy to denote that the painting is categorized as the collectable under

“s108-10” because it was Daniel personal enjoyment purpose. The capital gains

that is earned from the painting will be considered as the statutory income and the

gains is considered taxable as income under “sec 105-5(1)”.

Luxury Yacht:

In an attempt to fund for his retirement fund Daniel has a luxury yacht. The

information furnished suggest that the Yacht has the acquisition value of $110,000

while the sales was conducted by him for $60,000. Personal use asset can be

He has been living in the house for thirty years and in the presently tax year he sold

the house for $865,000. A sum of $15,000 was also paid by Daniel to his real estate

agent and later a buyer agreed to purchase the house. The buyer had deposited the

amount of $85,000 for the property. But in the recent change of events the buyer

decided against the purchase of the Doncaster house. The amount that was

deposited by the buyer was eventually forfeited to Daniel.

It is worth mentioning that “sec-104-150” provides the explanation regarding

the circumstances when there is a forfeiture of deposit (Marks and Bernard 2015).

Whenever there is a forfeiture of deposit a CGT event H1 come about in scenario.

This kind of event normally occurs when the prospective buyer makes a deposit on

the prospective sale or the other transaction is forfeited since the transaction failed to

proceed further.

From the aforementioned situation the “CGT event H1” has occurred for Daniel

under “s-104-150” because the buyer that agreed to purchase the house eventually

decided against proceeding the transaction and eventually the deposit was forfeited

(Poterba and Weisbenner 2014).

Painting by Margaret Preston:

A CGT event A1 under “sec 104-10” happens when the sale of the CGT

asset happens. This is generally applicable to the sale of the assets that is

purchased following 19/09/1985 (Poterba 2014). The taxpayers should denote that in

order to originate the CGT event A1 the CGT asset should be disposed to the

another entity. It is noteworthy to denote that the collectables are something that is

kept by the taxpayer for their personal purpose and enjoyment. There are items that

are listed in the s108-10 which includes, antiques, works of art, jewellery,

manuscripts and rare stamps. It is also necessary to denote that the taxpayers are

required to declare the capital gains that is made by them for taxable purpose in their

assessable income. According to the sec 6-10 the capital gains are considered

taxable as the statutory income and the gains are considered taxable as income

under “sec 105-5(1)”.

The evidence that is gained from situation of Daniel here it is understood that

the artistic piece of painting by Margaret Preston was kept under his possession.

The painting was mainly held by Daniel for his use and enjoyment purpose. Later in

the year 2019 the painting was sold by Daniel for $125,000 in the auction which he

originally purchased on the sept 20 1985 for an acquisition value of $15,000. It is

worth mentioning that the painting should be treated as the post-CGT asset because

it was bought after the scheme of CGT was introduced.

There is a CGT event A1 under “sec 104-10” when Daniel sold the painting.

It is noteworthy to denote that the painting is categorized as the collectable under

“s108-10” because it was Daniel personal enjoyment purpose. The capital gains

that is earned from the painting will be considered as the statutory income and the

gains is considered taxable as income under “sec 105-5(1)”.

Luxury Yacht:

In an attempt to fund for his retirement fund Daniel has a luxury yacht. The

information furnished suggest that the Yacht has the acquisition value of $110,000

while the sales was conducted by him for $60,000. Personal use asset can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

classified as the type of asset under “s108-20” that is different from the collectables

and these assets are under the ownership of the taxpayer for their private enjoyment

purpose (Jin 2016). Some examples include the television, boats, yacht, electronic

items etc. It is noteworthy to denote for the taxpayers that under the legislation of

“s108-20(1)”, the capital losses that is suffered by the taxpayer from selling the

personal use assets are considered to be simply ignored. This is because capital

loss from the personal use assets is not allowed for offset against any other gains.

The aforementioned examples explain that the yacht is the personal use asset

under “s108-20” (Burman 2013). The disposal of yacht led Daniel to suffer loss.

Therefore, it is advised that the Daniel should simply ignore the capital loss from the

sale of the personal use asset under the legislative provision of “s108-20 (1)”.

BHP shares:

Daniel also in a bid to fund for his retirement fund has decided to sale the

shares that he has kept under his ownership. The shares are from the mining

company named BHP. The acquisition value of the shares stood $75,000 during the

January 2019. On the other hand, the sales value stood $80,000 5 June 2019. There

were some added expenses that has happened during the acquisition and the sale

of shares. This include the stamp duty that was paid while purchasing the shares

and the brokerage cost while selling the shares.

The stamp duty is added to the cost base of the asset while the brokerage

represents the cost of selling the asset and the same has been subtracted. On

selling the BHP shares there was a capital gain for Daniel. While Daniel apart from

the BHP shares also had shares in AZJ company. The shares were the only asset

that was sold by Daniel in 2017 and thereby he suffered a loss of $10,000 from that

shares. It is noteworthy to denote that the carry forward loss from the AZJ shares

can be permitted for offset from the BHP shares. Similarly, the left over amount of

capital gains can be carry forward to the future year by Daniel which can be offset

against the future gains made from the sale of shares.

Answer to question B:

The occurrences from the case study suggest that Daniel reported the capital

gains from the personal use asset namely the painting that he has sold and the

capital gains from the forfeited deposit of his Melbourne house. The capital gains

that is reported by Daniel should be used by him to fund the retirement fund and will

contribute further towards his goal of $1 million super fund.

Answer to question C:

The disposal of yacht led Daniel to suffer loss. Therefore, it is advised that the

Daniel should simply ignore the capital loss from the sale of the personal use asset

under the legislative provision of “s108-20 (1)” (Poterba 2015). In addition to this, it

is noteworthy to denote that the carry forward loss from the AZJ shares can be

permitted for offset from the BHP shares. Similarly, the left over amount of capital

gains can be carry forward to the future year by Daniel which can be offset against

the future gains made from the sale of shares.

classified as the type of asset under “s108-20” that is different from the collectables

and these assets are under the ownership of the taxpayer for their private enjoyment

purpose (Jin 2016). Some examples include the television, boats, yacht, electronic

items etc. It is noteworthy to denote for the taxpayers that under the legislation of

“s108-20(1)”, the capital losses that is suffered by the taxpayer from selling the

personal use assets are considered to be simply ignored. This is because capital

loss from the personal use assets is not allowed for offset against any other gains.

The aforementioned examples explain that the yacht is the personal use asset

under “s108-20” (Burman 2013). The disposal of yacht led Daniel to suffer loss.

Therefore, it is advised that the Daniel should simply ignore the capital loss from the

sale of the personal use asset under the legislative provision of “s108-20 (1)”.

BHP shares:

Daniel also in a bid to fund for his retirement fund has decided to sale the

shares that he has kept under his ownership. The shares are from the mining

company named BHP. The acquisition value of the shares stood $75,000 during the

January 2019. On the other hand, the sales value stood $80,000 5 June 2019. There

were some added expenses that has happened during the acquisition and the sale

of shares. This include the stamp duty that was paid while purchasing the shares

and the brokerage cost while selling the shares.

The stamp duty is added to the cost base of the asset while the brokerage

represents the cost of selling the asset and the same has been subtracted. On

selling the BHP shares there was a capital gain for Daniel. While Daniel apart from

the BHP shares also had shares in AZJ company. The shares were the only asset

that was sold by Daniel in 2017 and thereby he suffered a loss of $10,000 from that

shares. It is noteworthy to denote that the carry forward loss from the AZJ shares

can be permitted for offset from the BHP shares. Similarly, the left over amount of

capital gains can be carry forward to the future year by Daniel which can be offset

against the future gains made from the sale of shares.

Answer to question B:

The occurrences from the case study suggest that Daniel reported the capital

gains from the personal use asset namely the painting that he has sold and the

capital gains from the forfeited deposit of his Melbourne house. The capital gains

that is reported by Daniel should be used by him to fund the retirement fund and will

contribute further towards his goal of $1 million super fund.

Answer to question C:

The disposal of yacht led Daniel to suffer loss. Therefore, it is advised that the

Daniel should simply ignore the capital loss from the sale of the personal use asset

under the legislative provision of “s108-20 (1)” (Poterba 2015). In addition to this, it

is noteworthy to denote that the carry forward loss from the AZJ shares can be

permitted for offset from the BHP shares. Similarly, the left over amount of capital

gains can be carry forward to the future year by Daniel which can be offset against

the future gains made from the sale of shares.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

References:

Barry, J.M. and Caron, P.L., 2015. Tax regulation, transportation innovation, and the

sharing economy. U. Chi. L. Rev. Dialogue, 82, p.69.

Black, C., 2018. Fringe benefits tax and the company car: aligning the tax with

environmental policy. Environmental and Planning Law Journal, 25(3), pp.182-195.

Burman, L.E., 2013. The labyrinth of capital gains tax policy: A guide for the

perplexed. Brookings Institution Press.

Gutiérrez‐i‐Puigarnau, E. and Van Ommeren, J.N., 2013. Welfare Effects of

Distortionary Fringe Benefits Taxation: The Case of Employer‐provided

Cars. International Economic Review, 52(4), pp.1105-1122.

Jin, L., 2016. Capital gains tax overhang and price pressure. The Journal of

Finance, 61(3), pp.1399-1431.

Kraal, D. and Yapa, P.W., 2018. The impact of Australia's fringe benefits tax for cars

on petrol consumption and greenhouse emissions. Austl. Tax F., 23, p.191.

Marks, B. and Bernard, M., 2015. Understanding Fringe Benefits Tax in Australia.

CCH Australia.

Poterba, J.M. and Weisbenner, S.J., 2014. Capital gains tax rules, tax‐loss trading,

and turn‐of‐the‐year returns. The Journal of Finance, 56(1), pp.353-368.

Poterba, J.M., 2014. Capital gains tax policy toward entrepreneurship. National Tax

Journal, 42(3), pp.375-389.

Poterba, J.M., 2015. Venture capital and capital gains taxation. Tax policy and the

economy, 3, pp.47-67.

Scott, R.A., Currie, G.V. and Tivendale, K.J., 2014. Company cars and fringe benefit

tax: understanding the impacts on strategic transport targets.

Shiftan, Y., Albert, G. and Keinan, T., 2014. The impact of company-car taxation

policy on travel behavior. Transport Policy, 19(1), pp.139-146.

References:

Barry, J.M. and Caron, P.L., 2015. Tax regulation, transportation innovation, and the

sharing economy. U. Chi. L. Rev. Dialogue, 82, p.69.

Black, C., 2018. Fringe benefits tax and the company car: aligning the tax with

environmental policy. Environmental and Planning Law Journal, 25(3), pp.182-195.

Burman, L.E., 2013. The labyrinth of capital gains tax policy: A guide for the

perplexed. Brookings Institution Press.

Gutiérrez‐i‐Puigarnau, E. and Van Ommeren, J.N., 2013. Welfare Effects of

Distortionary Fringe Benefits Taxation: The Case of Employer‐provided

Cars. International Economic Review, 52(4), pp.1105-1122.

Jin, L., 2016. Capital gains tax overhang and price pressure. The Journal of

Finance, 61(3), pp.1399-1431.

Kraal, D. and Yapa, P.W., 2018. The impact of Australia's fringe benefits tax for cars

on petrol consumption and greenhouse emissions. Austl. Tax F., 23, p.191.

Marks, B. and Bernard, M., 2015. Understanding Fringe Benefits Tax in Australia.

CCH Australia.

Poterba, J.M. and Weisbenner, S.J., 2014. Capital gains tax rules, tax‐loss trading,

and turn‐of‐the‐year returns. The Journal of Finance, 56(1), pp.353-368.

Poterba, J.M., 2014. Capital gains tax policy toward entrepreneurship. National Tax

Journal, 42(3), pp.375-389.

Poterba, J.M., 2015. Venture capital and capital gains taxation. Tax policy and the

economy, 3, pp.47-67.

Scott, R.A., Currie, G.V. and Tivendale, K.J., 2014. Company cars and fringe benefit

tax: understanding the impacts on strategic transport targets.

Shiftan, Y., Albert, G. and Keinan, T., 2014. The impact of company-car taxation

policy on travel behavior. Transport Policy, 19(1), pp.139-146.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.