HI6028 Taxation Law Assignment: Income Tax and CGT Analysis

VerifiedAdded on 2023/04/04

|8

|2248

|474

Homework Assignment

AI Summary

This assignment provides solutions to three questions related to Australian taxation law. The first question examines capital gains tax (CGT) implications on the sale of various assets, including antique paintings, historical sculptures, antique jewelry, and a picture, referencing relevant sections of the ITAA 1997. The second question analyzes whether monies earned from personal services, specifically writing a book and assigning its copyright, constitute ordinary income under s6.5 of the ITA Act 1997, citing relevant case law. The third question assesses whether interest earned from a loan qualifies as income under s6-25, considering its nature and characteristics based on legal precedents. The assignment applies relevant legislative provisions and case law to provide reasoned conclusions for each scenario.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................3

Answer to question 3:...................................................................................................4

References:..................................................................................................................6

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................3

Answer to question 3:...................................................................................................4

References:..................................................................................................................6

2TAXATION LAW

Answer to question 1:

Capital gains from antique paintings:

“Sec 100-25(1), ITA Act 97” restricts the assets based on which the capital

gains tax regimes are applied for the assets those are acquired on or following the

20/9/85. It is noteworthy to understand that the up to 21 sep 1999 only real gains

were considered for tax under the regimes of CGT (Lawrence 2019). Assets that are

purchased after the 20/9/85 is regarded as post-CGT asset where capital gains tax is

applied. Notably, if the assets are purchased before 20/9/85 then it is treated as pre-

CGT asset and no capital gains tax is imposed when making capital gains.

Helen sells the painting which her father has purchased in February 1985.

She disposed it on 2018 for $12,000. By selling the painting she made capital gains.

As noted the painting is the pre-CGT asset and the capital gains that she has made

will be exempted from the capital gains.

Capital gains from historical sculpture:

Under “s 104-10(1), ITAA 1997” a CGT event A1 happens when the capital

gains are made. Collectables should be referred as the asset that is defined in

“s108-10, ITAA 97”. Assets such as rare stamps, artworks in the form of paintings

and sculptures, antiques usually held as collectables (O’Connell 2017). These assets

are under the passion of taxpayers for their private use purpose. One must denote

that the “s6-10” considers the capital gains as the statutory income which is a

taxable under “s102-5(1)”.

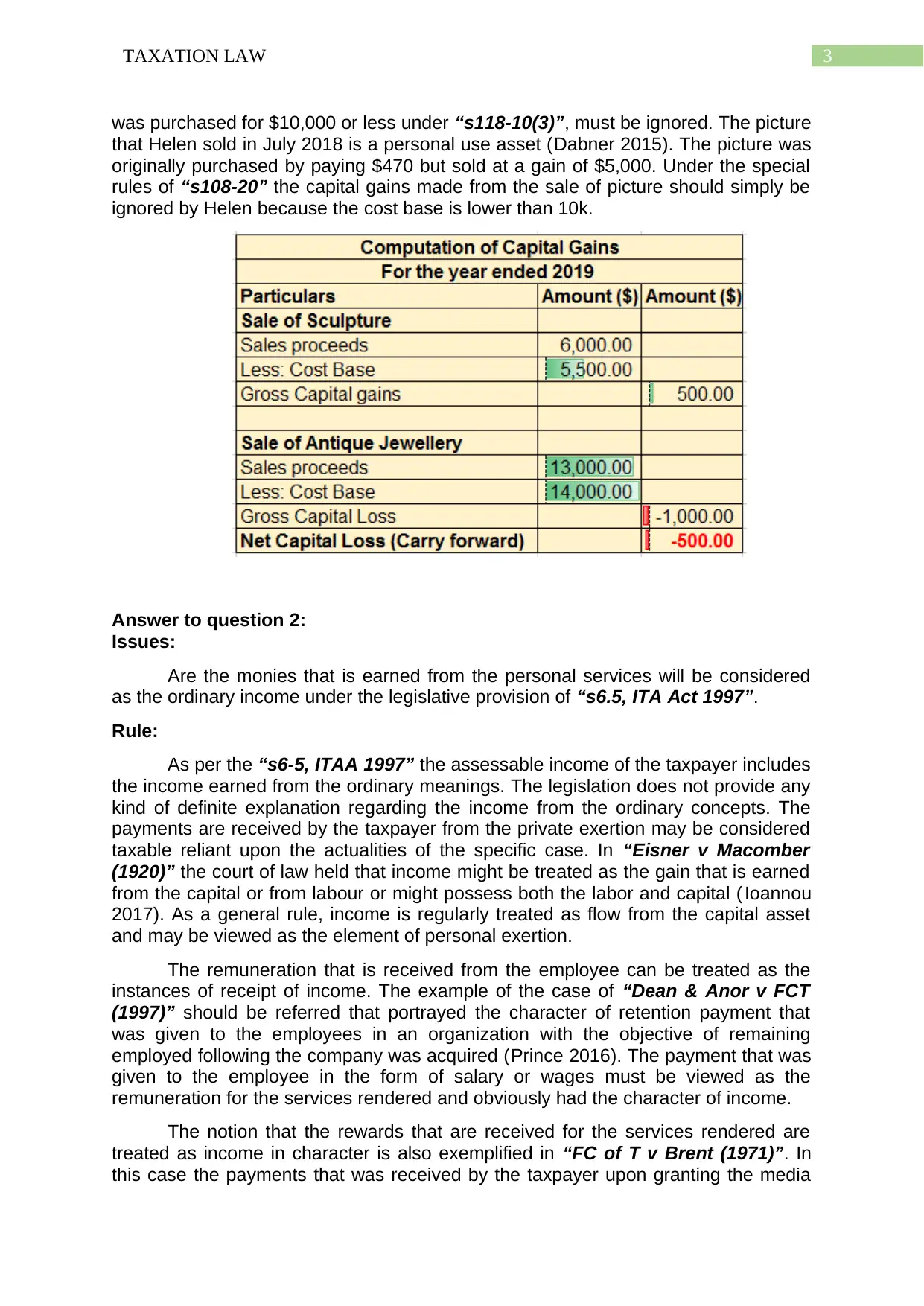

So as the situation unfolds it is noticed that historical sculpture that was

purchased in 2018 was sold for $6,000. The piece of sculpture was purchased in

1993 for $5,500. So when disposing the sculpture, it led to CGT event A1 under

“s104-10(1), ITAA 97”. The sculpture is a collectable defined in “s108-10, ITAA

97”. When she sold the sculpture a capital gains happened and the capital gains

should be denoted as statutory income for Helen which is which is a taxable under

“s102-5(1)”.

Capital gains from antique jewellery:

A noteworthy discussion has been made under the “s108-10(1)” concerning

the collectables (Evans and Krever 2017). This includes that the capital loss that is

made from the collectables are required to be solely offset from the capital gains of

other collectables.

An attention-grabbing situation develops for Helen when the antiques

jewellery that she purchased by paying a price of $14,000 only got $13,000 upon

selling the same. Therefore, the jewellery is treated as collectables under “s108-10,

ITAA 97”. So the jewellery has fetched loss for Helen. Referring to the special rules

given in “s108-10 (1)”, for collectables capital loss that is made from the jewellery

are required to be solely offset from the capital gains of sculpture.

Capital gains from picture:

A CGT asset under “s108-20” is also treated as the personal use asset that

is largely kept by the taxpayer for their personal use and enjoyment but it is different

from the collectables. The capital gains that is made from personal use asset that

Answer to question 1:

Capital gains from antique paintings:

“Sec 100-25(1), ITA Act 97” restricts the assets based on which the capital

gains tax regimes are applied for the assets those are acquired on or following the

20/9/85. It is noteworthy to understand that the up to 21 sep 1999 only real gains

were considered for tax under the regimes of CGT (Lawrence 2019). Assets that are

purchased after the 20/9/85 is regarded as post-CGT asset where capital gains tax is

applied. Notably, if the assets are purchased before 20/9/85 then it is treated as pre-

CGT asset and no capital gains tax is imposed when making capital gains.

Helen sells the painting which her father has purchased in February 1985.

She disposed it on 2018 for $12,000. By selling the painting she made capital gains.

As noted the painting is the pre-CGT asset and the capital gains that she has made

will be exempted from the capital gains.

Capital gains from historical sculpture:

Under “s 104-10(1), ITAA 1997” a CGT event A1 happens when the capital

gains are made. Collectables should be referred as the asset that is defined in

“s108-10, ITAA 97”. Assets such as rare stamps, artworks in the form of paintings

and sculptures, antiques usually held as collectables (O’Connell 2017). These assets

are under the passion of taxpayers for their private use purpose. One must denote

that the “s6-10” considers the capital gains as the statutory income which is a

taxable under “s102-5(1)”.

So as the situation unfolds it is noticed that historical sculpture that was

purchased in 2018 was sold for $6,000. The piece of sculpture was purchased in

1993 for $5,500. So when disposing the sculpture, it led to CGT event A1 under

“s104-10(1), ITAA 97”. The sculpture is a collectable defined in “s108-10, ITAA

97”. When she sold the sculpture a capital gains happened and the capital gains

should be denoted as statutory income for Helen which is which is a taxable under

“s102-5(1)”.

Capital gains from antique jewellery:

A noteworthy discussion has been made under the “s108-10(1)” concerning

the collectables (Evans and Krever 2017). This includes that the capital loss that is

made from the collectables are required to be solely offset from the capital gains of

other collectables.

An attention-grabbing situation develops for Helen when the antiques

jewellery that she purchased by paying a price of $14,000 only got $13,000 upon

selling the same. Therefore, the jewellery is treated as collectables under “s108-10,

ITAA 97”. So the jewellery has fetched loss for Helen. Referring to the special rules

given in “s108-10 (1)”, for collectables capital loss that is made from the jewellery

are required to be solely offset from the capital gains of sculpture.

Capital gains from picture:

A CGT asset under “s108-20” is also treated as the personal use asset that

is largely kept by the taxpayer for their personal use and enjoyment but it is different

from the collectables. The capital gains that is made from personal use asset that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

was purchased for $10,000 or less under “s118-10(3)”, must be ignored. The picture

that Helen sold in July 2018 is a personal use asset (Dabner 2015). The picture was

originally purchased by paying $470 but sold at a gain of $5,000. Under the special

rules of “s108-20” the capital gains made from the sale of picture should simply be

ignored by Helen because the cost base is lower than 10k.

Answer to question 2:

Issues:

Are the monies that is earned from the personal services will be considered

as the ordinary income under the legislative provision of “s6.5, ITA Act 1997”.

Rule:

As per the “s6-5, ITAA 1997” the assessable income of the taxpayer includes

the income earned from the ordinary meanings. The legislation does not provide any

kind of definite explanation regarding the income from the ordinary concepts. The

payments are received by the taxpayer from the private exertion may be considered

taxable reliant upon the actualities of the specific case. In “Eisner v Macomber

(1920)” the court of law held that income might be treated as the gain that is earned

from the capital or from labour or might possess both the labor and capital ( Ioannou

2017). As a general rule, income is regularly treated as flow from the capital asset

and may be viewed as the element of personal exertion.

The remuneration that is received from the employee can be treated as the

instances of receipt of income. The example of the case of “Dean & Anor v FCT

(1997)” should be referred that portrayed the character of retention payment that

was given to the employees in an organization with the objective of remaining

employed following the company was acquired (Prince 2016). The payment that was

given to the employee in the form of salary or wages must be viewed as the

remuneration for the services rendered and obviously had the character of income.

The notion that the rewards that are received for the services rendered are

treated as income in character is also exemplified in “FC of T v Brent (1971)”. In

this case the payments that was received by the taxpayer upon granting the media

was purchased for $10,000 or less under “s118-10(3)”, must be ignored. The picture

that Helen sold in July 2018 is a personal use asset (Dabner 2015). The picture was

originally purchased by paying $470 but sold at a gain of $5,000. Under the special

rules of “s108-20” the capital gains made from the sale of picture should simply be

ignored by Helen because the cost base is lower than 10k.

Answer to question 2:

Issues:

Are the monies that is earned from the personal services will be considered

as the ordinary income under the legislative provision of “s6.5, ITA Act 1997”.

Rule:

As per the “s6-5, ITAA 1997” the assessable income of the taxpayer includes

the income earned from the ordinary meanings. The legislation does not provide any

kind of definite explanation regarding the income from the ordinary concepts. The

payments are received by the taxpayer from the private exertion may be considered

taxable reliant upon the actualities of the specific case. In “Eisner v Macomber

(1920)” the court of law held that income might be treated as the gain that is earned

from the capital or from labour or might possess both the labor and capital ( Ioannou

2017). As a general rule, income is regularly treated as flow from the capital asset

and may be viewed as the element of personal exertion.

The remuneration that is received from the employee can be treated as the

instances of receipt of income. The example of the case of “Dean & Anor v FCT

(1997)” should be referred that portrayed the character of retention payment that

was given to the employees in an organization with the objective of remaining

employed following the company was acquired (Prince 2016). The payment that was

given to the employee in the form of salary or wages must be viewed as the

remuneration for the services rendered and obviously had the character of income.

The notion that the rewards that are received for the services rendered are

treated as income in character is also exemplified in “FC of T v Brent (1971)”. In

this case the payments that was received by the taxpayer upon granting the media

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

organization with the right of printing and publishing the story in the newspaper

article was held as income (Boccabella 2015). The taxpayer formed the agreement

of entering into the transaction of providing her personal service by appearing in the

interview with the journalist. The taxpayer in this case did not disposed the capital

asset neither had the taxpayer assigned any kind of copyright of the manuscript that

was in fact produced by the journalist. The taxpayer was clearly paid for her services

and the payment must be treated as income under ordinary concepts.

Applications:

The case here clearly explains that Barbara is a professional economist and

primarily engaged in the work of research. With vast amount of knowledge in

economics she is approached by a publisher who asked Barbara to share her

knowledge by writing a book in economics. The publisher offered $13,000 to Barbara

to write the book and she eventually wrote the book on economics. She was

successfully paid by the publisher for writing book.

The example of “Brent v FCT (1971)” must be citied in this situation. The

monies that is received by Barbara from writing the book is a personal exertion

income under “s6(1), ITAA 1936”. The amount was paid to her because it involved

her personal efforts. Barbara entered into the agreement with the publisher pursuant

to which she was duly paid as the consideration for making herself available for

writing the book. The amount will be treated as the reward for her services and must

be assessed consequently.

Secondly, Barbara assigns the copyright of the book that she had written. The

publisher in return paid her with the amount of $13,400. Reference here must be

essentially made to the case of “Dean & Anor v FCT (1997)” by explaining that the

amount of selling the copyright cannot be viewed as the disposal of capital asset.

Rather the payments are for the services that Barbara has rendered (Strano and

Pinto 2016). The amount received in exchange must be considered taxable as

income under “s6.5, ITA Act 1997”.

She sells the manuscript and the interview manuscript to the library and she

was paid in return by the library. In this situation references to court’s verdict made in

“Eisner v Macomber (1920)” can be referred to treat the payment. The monies

received from selling the manuscripts should be treated as income that is earned

from the combination of capital and effort. It is a product of Barbara’s personal

exertion income and taxable under “s6-5, ITAA 1997”.

In the turn of events if the books are alternatively written by Barbara as her

relaxation time and simply selling it in the market for the publication purpose the

money that will be earned from the book publication should be viewed as personal

efforts or exertion income. The money will be considered ordinary income under

“s6.5, ITA Act 1997”.

Conclusion:

The aforementioned case of Barbara can be concluded by stating that she

has been rewarded for her personal service income and it is taxable as the ordinary

earnings which is taxable under “s6-5, ITAA 1997”.

Answer to question 3:

Issues:

organization with the right of printing and publishing the story in the newspaper

article was held as income (Boccabella 2015). The taxpayer formed the agreement

of entering into the transaction of providing her personal service by appearing in the

interview with the journalist. The taxpayer in this case did not disposed the capital

asset neither had the taxpayer assigned any kind of copyright of the manuscript that

was in fact produced by the journalist. The taxpayer was clearly paid for her services

and the payment must be treated as income under ordinary concepts.

Applications:

The case here clearly explains that Barbara is a professional economist and

primarily engaged in the work of research. With vast amount of knowledge in

economics she is approached by a publisher who asked Barbara to share her

knowledge by writing a book in economics. The publisher offered $13,000 to Barbara

to write the book and she eventually wrote the book on economics. She was

successfully paid by the publisher for writing book.

The example of “Brent v FCT (1971)” must be citied in this situation. The

monies that is received by Barbara from writing the book is a personal exertion

income under “s6(1), ITAA 1936”. The amount was paid to her because it involved

her personal efforts. Barbara entered into the agreement with the publisher pursuant

to which she was duly paid as the consideration for making herself available for

writing the book. The amount will be treated as the reward for her services and must

be assessed consequently.

Secondly, Barbara assigns the copyright of the book that she had written. The

publisher in return paid her with the amount of $13,400. Reference here must be

essentially made to the case of “Dean & Anor v FCT (1997)” by explaining that the

amount of selling the copyright cannot be viewed as the disposal of capital asset.

Rather the payments are for the services that Barbara has rendered (Strano and

Pinto 2016). The amount received in exchange must be considered taxable as

income under “s6.5, ITA Act 1997”.

She sells the manuscript and the interview manuscript to the library and she

was paid in return by the library. In this situation references to court’s verdict made in

“Eisner v Macomber (1920)” can be referred to treat the payment. The monies

received from selling the manuscripts should be treated as income that is earned

from the combination of capital and effort. It is a product of Barbara’s personal

exertion income and taxable under “s6-5, ITAA 1997”.

In the turn of events if the books are alternatively written by Barbara as her

relaxation time and simply selling it in the market for the publication purpose the

money that will be earned from the book publication should be viewed as personal

efforts or exertion income. The money will be considered ordinary income under

“s6.5, ITA Act 1997”.

Conclusion:

The aforementioned case of Barbara can be concluded by stating that she

has been rewarded for her personal service income and it is taxable as the ordinary

earnings which is taxable under “s6-5, ITAA 1997”.

Answer to question 3:

Issues:

5TAXATION LAW

Is the interest that is earned from the loan amounts to income under the

statutory concepts of s6-25?

Rule:

The rule that is given in the “s6-5, ITAA 97” explains that the income that is

earned by the taxpayer must be viewed under the ordinary meaning and should be

considered taxable accordingly (Voogt 2019). It is necessary to characterise the

gains as income in terms of the ordinary concepts. Gains needs the characterisation

of the courts to ascertain that if the gain possess the nature of income. the taxpayer

should also denote that the receipts will not be held as the ordinary earnings except

it satisfies the eligibility of the prerequisites. This mainly includes that it must be cash

or should amount to a real gain for the taxpayer.

Most notably the gains should not be viewed as ordinary income if it not

convertible in to cash. The decision of the high court in the example of “Mayes v

Hochstrasser (1960)” denoted that receipts should not be viewed as the genuine

gain if it does not meet the concepts of ordinary income (Tran 2015). Provided that

the prerequisite of the income is met by the taxpayer then the gains is treated as the

ordinary income because it represents the satisfactory characteristics of income.

The taxpayers are also required to denote that the gains which are very much

in the nature of periodic or regular then they would most likely have the

characteristics of ordinary income than those gains that are received as the lump

sum. However, an instance that was denote in the case of “FCT v Harris (1980)”

explained that the one-off receipts cannot be treated as the ordinary income (Chan

2016).

Evidently, it must be noted that the lump sum gains might be treated as the

ordinary earrings. The examples of such receipts include the singe receipt of interest

that is received by the taxpayer under the agreement of loan.

Application:

By gauging into the situation of Patrick’s case study, one can understand that

he loaned a sum of $52,000 during the year to his son David as the assistance for

his fresh start-up company. There was no such kind of written contract between the

father and the son but there verbally it was agreed that the son would be repaying

the full amount of loan to his father inside the time period of five years (McKenzie

2018). Beside paying the principle loan amount the son was required by his father to

pay a sum of $6,000 as the interest on loan. The loan was duly paid in full inside two

years through cheque which also contained an amount of 5% as the interest on loan.

By referring to the example of “Mayes v Hochstrasser (1960)” the receipt of

interest by father must be viewed as the real gain. The amount of interest satisfies

both the prerequisite of income and it is also convertible in to cash as well ( Mintz et

al. 2017). Though the amount was paid as the lump sum but the single mode of

payment of interest with the loan principle amount with respect to the loan

agreement must be considered as income. The interest that is received shows

adequate characteristics of the gain and it is taxable under statutory income under

legislative provision of “s6-25, ITAA 1997”.

Conclusion:

Is the interest that is earned from the loan amounts to income under the

statutory concepts of s6-25?

Rule:

The rule that is given in the “s6-5, ITAA 97” explains that the income that is

earned by the taxpayer must be viewed under the ordinary meaning and should be

considered taxable accordingly (Voogt 2019). It is necessary to characterise the

gains as income in terms of the ordinary concepts. Gains needs the characterisation

of the courts to ascertain that if the gain possess the nature of income. the taxpayer

should also denote that the receipts will not be held as the ordinary earnings except

it satisfies the eligibility of the prerequisites. This mainly includes that it must be cash

or should amount to a real gain for the taxpayer.

Most notably the gains should not be viewed as ordinary income if it not

convertible in to cash. The decision of the high court in the example of “Mayes v

Hochstrasser (1960)” denoted that receipts should not be viewed as the genuine

gain if it does not meet the concepts of ordinary income (Tran 2015). Provided that

the prerequisite of the income is met by the taxpayer then the gains is treated as the

ordinary income because it represents the satisfactory characteristics of income.

The taxpayers are also required to denote that the gains which are very much

in the nature of periodic or regular then they would most likely have the

characteristics of ordinary income than those gains that are received as the lump

sum. However, an instance that was denote in the case of “FCT v Harris (1980)”

explained that the one-off receipts cannot be treated as the ordinary income (Chan

2016).

Evidently, it must be noted that the lump sum gains might be treated as the

ordinary earrings. The examples of such receipts include the singe receipt of interest

that is received by the taxpayer under the agreement of loan.

Application:

By gauging into the situation of Patrick’s case study, one can understand that

he loaned a sum of $52,000 during the year to his son David as the assistance for

his fresh start-up company. There was no such kind of written contract between the

father and the son but there verbally it was agreed that the son would be repaying

the full amount of loan to his father inside the time period of five years (McKenzie

2018). Beside paying the principle loan amount the son was required by his father to

pay a sum of $6,000 as the interest on loan. The loan was duly paid in full inside two

years through cheque which also contained an amount of 5% as the interest on loan.

By referring to the example of “Mayes v Hochstrasser (1960)” the receipt of

interest by father must be viewed as the real gain. The amount of interest satisfies

both the prerequisite of income and it is also convertible in to cash as well ( Mintz et

al. 2017). Though the amount was paid as the lump sum but the single mode of

payment of interest with the loan principle amount with respect to the loan

agreement must be considered as income. The interest that is received shows

adequate characteristics of the gain and it is taxable under statutory income under

legislative provision of “s6-25, ITAA 1997”.

Conclusion:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

The interest loan has been considered as the statutory income for Patrick.

The amount will be treated as real gain for Patrick.

The interest loan has been considered as the statutory income for Patrick.

The amount will be treated as real gain for Patrick.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

References:

Boccabella, D., 2015. Reconciling the overlap of charging provisions in regard to

non-cash benefits from employment, personal exertion and business. J. Austl.

Tax'n, 17, p.85.

Chan, C., 2016. A case for statutory simplification. Tax Specialist, 19(3), p.118.

Dabner, J., 2015. Tax Simplification–An Accident Looking for a Place to

Happen?. Available at SSRN 2707910.

Evans, C. and Krever, R., 2017. Taxing Capital Gains: A Comparative Analysis and

Lessons for New Zealand.

Ioannou, J., 2017. Income from property, partnerships and planning. Taxation in

Australia, 52(4), p.198.

Lawrence, S., 2019. Separate SMSFs for collectables. Taxation in Australia, 53(9),

p.480.

McKenzie, M., 2018. The erosion of minimum wage policy in Australia and labour's

shrinking share of total income. Journal of Australian Political Economy, The, (81),

p.52.

Mintz, J., Bazel, P., Chen, D. and Crisan, D., 2017. With global company tax reform

in the air, will Australia finally respond?. Minerals Council of Australia, Melbourne,

Australia, March.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

Prince, J.B., 2016. Tax for Australians for Dummies. John Wiley & Sons.

Strano, C. and Pinto, D., 2016. A comparative analysis of Australian and Hong Kong

retirement systems. eJTR, 14, p.34.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed

companies in Australia. Austl. Tax F., 30, p.569.

Voogt, T., 2019. Income tax and trust law perspectives of the practical disregard of

legal form in discretionary family trading trusts.

References:

Boccabella, D., 2015. Reconciling the overlap of charging provisions in regard to

non-cash benefits from employment, personal exertion and business. J. Austl.

Tax'n, 17, p.85.

Chan, C., 2016. A case for statutory simplification. Tax Specialist, 19(3), p.118.

Dabner, J., 2015. Tax Simplification–An Accident Looking for a Place to

Happen?. Available at SSRN 2707910.

Evans, C. and Krever, R., 2017. Taxing Capital Gains: A Comparative Analysis and

Lessons for New Zealand.

Ioannou, J., 2017. Income from property, partnerships and planning. Taxation in

Australia, 52(4), p.198.

Lawrence, S., 2019. Separate SMSFs for collectables. Taxation in Australia, 53(9),

p.480.

McKenzie, M., 2018. The erosion of minimum wage policy in Australia and labour's

shrinking share of total income. Journal of Australian Political Economy, The, (81),

p.52.

Mintz, J., Bazel, P., Chen, D. and Crisan, D., 2017. With global company tax reform

in the air, will Australia finally respond?. Minerals Council of Australia, Melbourne,

Australia, March.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

Prince, J.B., 2016. Tax for Australians for Dummies. John Wiley & Sons.

Strano, C. and Pinto, D., 2016. A comparative analysis of Australian and Hong Kong

retirement systems. eJTR, 14, p.34.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed

companies in Australia. Austl. Tax F., 30, p.569.

Voogt, T., 2019. Income tax and trust law perspectives of the practical disregard of

legal form in discretionary family trading trusts.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.