Taxation Law Assignment: Australian Taxation Law Analysis - Semester 1

VerifiedAdded on 2022/12/21

|15

|3642

|1

Homework Assignment

AI Summary

This taxation law assignment delves into various aspects of Australian taxation. It addresses key concepts such as the determination of business actions based on Taxation Ruling 2019/11, deductibility of gifts, and the maximum tax rate for individuals. The assignment explores capital gains tax (CGT) exemptions, the treatment of misplaced assets, and the taxability of income. It examines the legal precedent set by Hayes v FCT (1956) regarding CGT gains and the distinction between ordinary and statutory income. Additionally, the assignment analyzes Medicare Levy and Medicare Levy Surcharge. It further discusses residency tests in Australia, including domicile, resides, and the 183-day test, differentiating between usual and permanent places of abode. Finally, the assignment covers deductible expenditures related to income earning, travel, and professional development expenses, referencing relevant sections of the ITAA 1997.

Running head: TAXATION LAW

TAXATION LAW

Name of the Student

Name of the University

Author Note

TAXATION LAW

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Answer 1

a) When it is apparent that a business action has been said to be carried out by a company

that is the topic which is considered to be dealt with Taxation Ruling 2019/11.

b) In div 30 of ITAA, 972 the deductibility of the gifts or the contributions whether they

can be made are laid down.

c) The maximum tax rate that an individual has to pay for the year 2019-2020 is the

amount of 54097 AUD $ with the addition of 45% on any amount which can exceed 180,000

AUD $3.

d) There can be an exemption of car as well as motorcycle as the provisions which have

been laid down in Sec 118.5 of ITAA ,974 from being subjected to capital gain taxation.

e) Any kind of item or an asset which has been misplaced or has been destroyed that was

in possession of the taxpayer before would be considered to have fallen under CGT as an event

of C1 according to the provisions laid down in 104-20 of ITAA, 975.

f) Any kind of income or revenue earned by the taxpayer which is considered to be under

the amount of 18,200 AUD $ cannot be included in taxation.

g) The legal code which has been considered to develop with the High Court’s decision

can be seen in the case of Hayes v FCT (1956) 96 CLR 476 was that any kind of amount which

1 TR 2019/1.

2 The Income Tax Assessment Act 1997 (Cth), div 30

3www.ato.gov.au,"IndividualIncomeTaxRates",Ato.Gov.Au(Webpage,2019)

<https://www.ato.gov.au/Rates/Individual-income-tax-rates/>.

4 The Income Tax Assessment Act 1997 (Cth), s 118.5

5 The Income Tax Assessment Act 1997 (Cth), s 104.20

6 Hayes v FCT (1956) 96 CLR 47.

Answer 1

a) When it is apparent that a business action has been said to be carried out by a company

that is the topic which is considered to be dealt with Taxation Ruling 2019/11.

b) In div 30 of ITAA, 972 the deductibility of the gifts or the contributions whether they

can be made are laid down.

c) The maximum tax rate that an individual has to pay for the year 2019-2020 is the

amount of 54097 AUD $ with the addition of 45% on any amount which can exceed 180,000

AUD $3.

d) There can be an exemption of car as well as motorcycle as the provisions which have

been laid down in Sec 118.5 of ITAA ,974 from being subjected to capital gain taxation.

e) Any kind of item or an asset which has been misplaced or has been destroyed that was

in possession of the taxpayer before would be considered to have fallen under CGT as an event

of C1 according to the provisions laid down in 104-20 of ITAA, 975.

f) Any kind of income or revenue earned by the taxpayer which is considered to be under

the amount of 18,200 AUD $ cannot be included in taxation.

g) The legal code which has been considered to develop with the High Court’s decision

can be seen in the case of Hayes v FCT (1956) 96 CLR 476 was that any kind of amount which

1 TR 2019/1.

2 The Income Tax Assessment Act 1997 (Cth), div 30

3www.ato.gov.au,"IndividualIncomeTaxRates",Ato.Gov.Au(Webpage,2019)

<https://www.ato.gov.au/Rates/Individual-income-tax-rates/>.

4 The Income Tax Assessment Act 1997 (Cth), s 118.5

5 The Income Tax Assessment Act 1997 (Cth), s 104.20

6 Hayes v FCT (1956) 96 CLR 47.

2TAXATION LAW

has been received by the taxpayer which has been against any kind of services rendered by him

in the past instances needs to be used as or seen as a kind of CGT gain which is for the purpose

of assessability. It can be understood, in this situation that the amount or the price received from

the employer by the employee after providing the services which needed to be performed before

receiving the same amount for doing it again would be considered to be assessable income as a

capital gain of that employee. In case of deciding upon an instance where there is a difficulty in

the treatment of any kind of receipt which has been accepted from the previous employer for the

services rendered by the employee before where the difficulty is to whether to use the amount as

a capital gain or use it as an ordinary income. The income has been received because of personal

effort is considered to be treated as just another ordinary income. Nevertheless, if a receipt has

been accepted from the employer for whom the employee worked before and it has already been

accumulated but it has not been received by the taxpayer this would only be considered to be

received by the taxpayer and has been obtained as nature of an asset because the same thing has

not been obtained by the taxpayer as a lot of amount which has been accumulated by the

taxpayer for a succeeding period.

h) There are two kinds of income that can be earned by an individual who is a taxpayer

under the taxation law which has delivered categories of the taxable income. The ordinary

income is considered to be the first category under the taxation law. The statutory income would

be considered to be the second category under taxation law. The income which falls under the

category of general definitions of an income which is known to public who do not have any legal

understanding would be considered as the ordinary income. In order to evaluate such kind of

incomes there are no strict rules that needs to be conformed with which are also provided in the

statutes. If there is an absence of an y express which has not been mentioned in the statutory

has been received by the taxpayer which has been against any kind of services rendered by him

in the past instances needs to be used as or seen as a kind of CGT gain which is for the purpose

of assessability. It can be understood, in this situation that the amount or the price received from

the employer by the employee after providing the services which needed to be performed before

receiving the same amount for doing it again would be considered to be assessable income as a

capital gain of that employee. In case of deciding upon an instance where there is a difficulty in

the treatment of any kind of receipt which has been accepted from the previous employer for the

services rendered by the employee before where the difficulty is to whether to use the amount as

a capital gain or use it as an ordinary income. The income has been received because of personal

effort is considered to be treated as just another ordinary income. Nevertheless, if a receipt has

been accepted from the employer for whom the employee worked before and it has already been

accumulated but it has not been received by the taxpayer this would only be considered to be

received by the taxpayer and has been obtained as nature of an asset because the same thing has

not been obtained by the taxpayer as a lot of amount which has been accumulated by the

taxpayer for a succeeding period.

h) There are two kinds of income that can be earned by an individual who is a taxpayer

under the taxation law which has delivered categories of the taxable income. The ordinary

income is considered to be the first category under the taxation law. The statutory income would

be considered to be the second category under taxation law. The income which falls under the

category of general definitions of an income which is known to public who do not have any legal

understanding would be considered as the ordinary income. In order to evaluate such kind of

incomes there are no strict rules that needs to be conformed with which are also provided in the

statutes. If there is an absence of an y express which has not been mentioned in the statutory

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

provisions which is in connection to taxation the ordinary income would be considered to be

evaluated as an income. Therefore, from the above discussion, it can be understood, that income

that can be used as an income in the ordinary course would be considered to be an ordinary

income. Any income that has been specifically mentioned in the statutory provisions that is in

connection with taxation which is considered to be an income of a specific nature is necessary to

be considered as a statutory income. These income would be taxable only if these kind of income

has been mentioned as a legal provision which are confined in a statute. These are the type of

income which are not monitored as ordinary income but they need statutory acknowledgement in

order to be considered as an income7.

i) There are two different additional charges that are levied upon the taxpayers which are

the Medicare Levy and the Medicare levy surcharge. Some of the taxpayers are considered to

pay additional charges and also additional taxes which are to be paid by those taxpayers. The

Medicare Levy is considered to be presented for the health system of the public which is

prevailing in Australia. It is also imposed on the individual as a taxable income. It is to be paid at

a rate of 2%. The Medicare Levy Act, 19868 along with the ITAA9 imposed it. The Medicare

Levy Surcharge has been established for the individuals who have high income rate to spend

their money on their private health by investing in private health insurance for trying to decrease

the weight of Medicare. In this form of taxation it is only applied on the taxpayers who do not

have any kind of health insurance. This kind of levy is essentially executed on the total of the

income which is taxable and also on the Fringe Benefits which are relating to an single taxpayer.

It varies on the income of the different taxpayers which may be between 1%, 1.25% and 1.5%10.

7 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

8 The Medicare Levy Act 1986

9 The Income Tax Assessment Act 1936 (Cth)

10Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

provisions which is in connection to taxation the ordinary income would be considered to be

evaluated as an income. Therefore, from the above discussion, it can be understood, that income

that can be used as an income in the ordinary course would be considered to be an ordinary

income. Any income that has been specifically mentioned in the statutory provisions that is in

connection with taxation which is considered to be an income of a specific nature is necessary to

be considered as a statutory income. These income would be taxable only if these kind of income

has been mentioned as a legal provision which are confined in a statute. These are the type of

income which are not monitored as ordinary income but they need statutory acknowledgement in

order to be considered as an income7.

i) There are two different additional charges that are levied upon the taxpayers which are

the Medicare Levy and the Medicare levy surcharge. Some of the taxpayers are considered to

pay additional charges and also additional taxes which are to be paid by those taxpayers. The

Medicare Levy is considered to be presented for the health system of the public which is

prevailing in Australia. It is also imposed on the individual as a taxable income. It is to be paid at

a rate of 2%. The Medicare Levy Act, 19868 along with the ITAA9 imposed it. The Medicare

Levy Surcharge has been established for the individuals who have high income rate to spend

their money on their private health by investing in private health insurance for trying to decrease

the weight of Medicare. In this form of taxation it is only applied on the taxpayers who do not

have any kind of health insurance. This kind of levy is essentially executed on the total of the

income which is taxable and also on the Fringe Benefits which are relating to an single taxpayer.

It varies on the income of the different taxpayers which may be between 1%, 1.25% and 1.5%10.

7 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

8 The Medicare Levy Act 1986

9 The Income Tax Assessment Act 1936 (Cth)

10Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer 2

In the Sec 6.1 of the ITAA 3611 , there are a requirement of three kind of tests which

involves the valuation of the residency in Australia of an individual. First is the domicile test, the

second is considered to be the resides test and the third is considered to be the super admission

test which is also the one eighty three day test which are required in order to evaluate an

individual’s taxability rate who is living in Australia or any individual who has any kind of

connection with the country. There are two kinds of notions which are to be discovered in this

segment while there is a discussion about the above-mentioned tests. There is a difference

between the usual place of abode and the permanent place of abode even though it may sound

quite similar regarding the taxation law in the country. These two have a certain similarity as

both are considered to be a place of abode. In order to evaluate these two concepts the meaning

needs to be clear. The idea of a place of abode needs to be evaluated under the rule which has

been provided in the case of I.R.C. v. Lysaght (1928) A.C.23412. In this particular case the place

of abode would be considered to be any kind of residential property, where the taxpayers have

been using the land or property by possessing it or by lending it where the main intention was to

dwell or lodge with the surroundings of the place along with the family. The intention behind

residing in a property would be evaluated and it would be for the reason for residence and thus, it

is considered to be a place of abode.

The idea of permanent place of abode which can be described as it can be seen in the case

of FC of T v Applegate 79 ATC 430713. In this case which has been established as per the

provisions a permanent place of abode is considered to be a place where the person who is the

11 The Income Tax Assessment Act 1936 (Cth), s 6.1

12 I.R.C. v. Lysaght (1928) A.C.234

13 FC of T v Applegate 79 ATC 4307

Answer 2

In the Sec 6.1 of the ITAA 3611 , there are a requirement of three kind of tests which

involves the valuation of the residency in Australia of an individual. First is the domicile test, the

second is considered to be the resides test and the third is considered to be the super admission

test which is also the one eighty three day test which are required in order to evaluate an

individual’s taxability rate who is living in Australia or any individual who has any kind of

connection with the country. There are two kinds of notions which are to be discovered in this

segment while there is a discussion about the above-mentioned tests. There is a difference

between the usual place of abode and the permanent place of abode even though it may sound

quite similar regarding the taxation law in the country. These two have a certain similarity as

both are considered to be a place of abode. In order to evaluate these two concepts the meaning

needs to be clear. The idea of a place of abode needs to be evaluated under the rule which has

been provided in the case of I.R.C. v. Lysaght (1928) A.C.23412. In this particular case the place

of abode would be considered to be any kind of residential property, where the taxpayers have

been using the land or property by possessing it or by lending it where the main intention was to

dwell or lodge with the surroundings of the place along with the family. The intention behind

residing in a property would be evaluated and it would be for the reason for residence and thus, it

is considered to be a place of abode.

The idea of permanent place of abode which can be described as it can be seen in the case

of FC of T v Applegate 79 ATC 430713. In this case which has been established as per the

provisions a permanent place of abode is considered to be a place where the person who is the

11 The Income Tax Assessment Act 1936 (Cth), s 6.1

12 I.R.C. v. Lysaght (1928) A.C.234

13 FC of T v Applegate 79 ATC 4307

5TAXATION LAW

taxpayer has been residing with the intention to reside in that place for a continuous period of

time with no intention of leaving that place. There is a specific time period in which the person

has to reside in a place can be indefinite but it cannot be infinite or for whole eternity. The time

period of more than three years without the intention of moving would be considered to be the

permanent place of abode. It can also be supported by in the case of F.C. of T. v. Jenkins 82

ATC 409814.

The idea of the usual place of abode needs to be evaluated in connection to domicile.

This also necessitates the person or an individual to live in a place as a habit or a part of the

custom. There can be a rented accommodation existing in the usual place of abode of an

individual. This kind of stay should not be confused with the permanent place of abode. It can be

seen in the case of Levene v. I.R.C.(1928) A.C.21715.

Answer 3

a) With respect to a person’s income earning process the expenditure which is

considered to be arising can be easily available and is considered to be a deduction of the income

of that individual as per the provision confined in Sec 8.1 of the ITAA, 9716. For the persistence

of claiming such kind of deduction the individual who is considered to be a taxpayer would be

obligated to signify that the expenditure was not relating to any kind of domestic purpose and it

was based only on the income earning process. In this situation the expenditure which is

amounting to a total of eight hundred and fifty dollars for HECS-HELP has been acquired with

respect to a student loan which was personal. This does not have anything to do with quantifiable

income of a person. Therefore, it cannot be considered to be a deduction.

14 F.C. of T. v. Jenkins 82 ATC 4098

15 Levene v. I.R.C.(1928) A.C.217

16 The Income Tax Assessment Act 1997 (Cth), s 8.1

taxpayer has been residing with the intention to reside in that place for a continuous period of

time with no intention of leaving that place. There is a specific time period in which the person

has to reside in a place can be indefinite but it cannot be infinite or for whole eternity. The time

period of more than three years without the intention of moving would be considered to be the

permanent place of abode. It can also be supported by in the case of F.C. of T. v. Jenkins 82

ATC 409814.

The idea of the usual place of abode needs to be evaluated in connection to domicile.

This also necessitates the person or an individual to live in a place as a habit or a part of the

custom. There can be a rented accommodation existing in the usual place of abode of an

individual. This kind of stay should not be confused with the permanent place of abode. It can be

seen in the case of Levene v. I.R.C.(1928) A.C.21715.

Answer 3

a) With respect to a person’s income earning process the expenditure which is

considered to be arising can be easily available and is considered to be a deduction of the income

of that individual as per the provision confined in Sec 8.1 of the ITAA, 9716. For the persistence

of claiming such kind of deduction the individual who is considered to be a taxpayer would be

obligated to signify that the expenditure was not relating to any kind of domestic purpose and it

was based only on the income earning process. In this situation the expenditure which is

amounting to a total of eight hundred and fifty dollars for HECS-HELP has been acquired with

respect to a student loan which was personal. This does not have anything to do with quantifiable

income of a person. Therefore, it cannot be considered to be a deduction.

14 F.C. of T. v. Jenkins 82 ATC 4098

15 Levene v. I.R.C.(1928) A.C.217

16 The Income Tax Assessment Act 1997 (Cth), s 8.1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

b) An individual taxpayer has the right to have an expenditure while travelling in the

workplace has to be permitted an expense which can be deducted in the rule which is mentioned

under Sec 25.100 of ITAA 9717. In the current scenario the expenditure that has been acquired

for travelling from the workplace to the university is amounting up to 110 AUD$ which would

be considered to be deductible.

c) With respect to the expenditure of an individual which is for the income earning

process is measureable and needs to be deducted which is towards the income of the individual

stated in the provisions of Sec 8-1 of ITAA, 9718. To claim any kind of deduction the taxpayer

needs to be able to denote that it was not having any kind of relation with the domestic purpose

and is only based on the income earning process. In the current scenario the 200 dollars book

which has been obtained by the taxpayer for the betterment of his skills relating to his accounting

profession and hence, is considered to be deducted as the expenditure had been incurred.

d) With respect to the expenditure of an individual which is due to the increase in the

income earning process of an individual is considered to be a deduction under Sec 8.1 of ITAA,

9719. For the purpose of such deduction which was being claimed the expenditure was not having

any kind of domestic purpose but was based on the income earning process. It can be seen in the

case of Lodge v Federal Commissioner of Taxation [1972] HCA 4920. The cost of 250 AUD$

which was taken to repair the piece of refrigerator at home cannot be considered to be a

professional expense. It is a private expense therefore it would not be deductible.

f) The expenditure which has been sustained for a piece of clothing which would be worn

in the workplace of the taxpayer would not be considered to be deductible as in the provisions of

17 The Income Tax Assessment Act 1997 (Cth), s 25.100

18 The Income Tax Assessment Act 1997 (Cth), s 8.1

19The Income Tax Assessment Act 1997 (Cth), s 8.1

20 Lodge v Federal Commissioner of Taxation [1972] HCA 49

b) An individual taxpayer has the right to have an expenditure while travelling in the

workplace has to be permitted an expense which can be deducted in the rule which is mentioned

under Sec 25.100 of ITAA 9717. In the current scenario the expenditure that has been acquired

for travelling from the workplace to the university is amounting up to 110 AUD$ which would

be considered to be deductible.

c) With respect to the expenditure of an individual which is for the income earning

process is measureable and needs to be deducted which is towards the income of the individual

stated in the provisions of Sec 8-1 of ITAA, 9718. To claim any kind of deduction the taxpayer

needs to be able to denote that it was not having any kind of relation with the domestic purpose

and is only based on the income earning process. In the current scenario the 200 dollars book

which has been obtained by the taxpayer for the betterment of his skills relating to his accounting

profession and hence, is considered to be deducted as the expenditure had been incurred.

d) With respect to the expenditure of an individual which is due to the increase in the

income earning process of an individual is considered to be a deduction under Sec 8.1 of ITAA,

9719. For the purpose of such deduction which was being claimed the expenditure was not having

any kind of domestic purpose but was based on the income earning process. It can be seen in the

case of Lodge v Federal Commissioner of Taxation [1972] HCA 4920. The cost of 250 AUD$

which was taken to repair the piece of refrigerator at home cannot be considered to be a

professional expense. It is a private expense therefore it would not be deductible.

f) The expenditure which has been sustained for a piece of clothing which would be worn

in the workplace of the taxpayer would not be considered to be deductible as in the provisions of

17 The Income Tax Assessment Act 1997 (Cth), s 25.100

18 The Income Tax Assessment Act 1997 (Cth), s 8.1

19The Income Tax Assessment Act 1997 (Cth), s 8.1

20 Lodge v Federal Commissioner of Taxation [1972] HCA 49

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Sec 8.1 Of the ITAA, 9721. Thus, the amount of One hundred and forty five dollars which was

used to buy black trousers and shirts would not be considered as a deductible amount.

g) The expenditure that has been ascending due to the income earning process of an

individual that is measureable is considered to be a deduction as per the provisions in Sec 8.1 of

ITAA, 9722. In the current scenario the three hundred dollars have been expended with the

employment contract which is existing with the new proprietor. It is not considered to be

deductible as it was not for the purpose of earning income and it would not be treated as

deduction since it is directly not considered to be related to income.

Answer 4

a)The category of F2 in the CGT events is considered to be dealt with the lending o or

renting of any kind of property or land which is in possession of an individual. It also includes a

fresh grant of lease which can be renewed or extended with the previous lease. Nevertheless,

there would be no availability of fifty percent discount in any CGT event. Therefore, the seven

thousand dollars received by John who is the owner of the land or the property is considered to

be CGT event F2 from David which would be exposed to CGT without any kind of discount

which is fifty percent23.

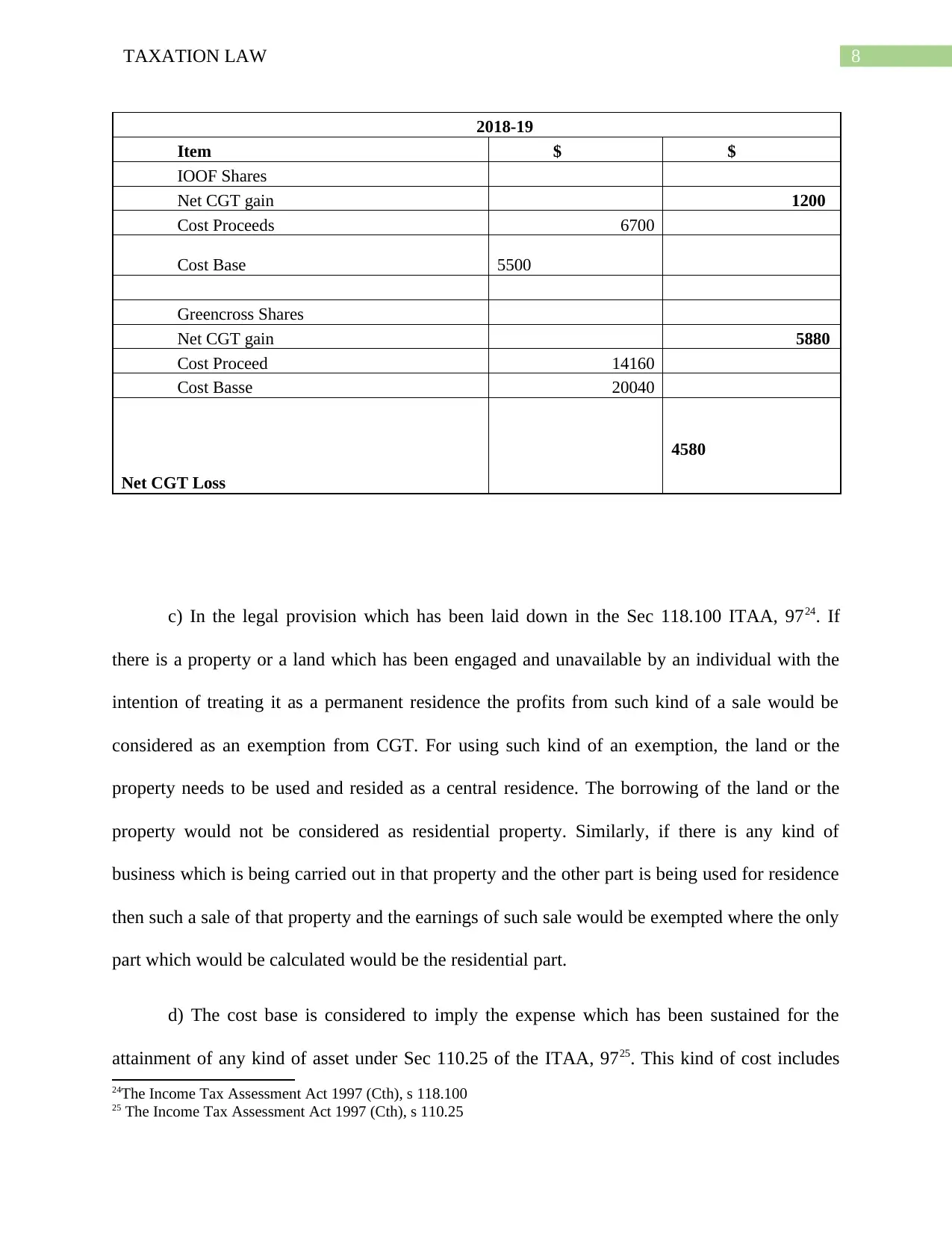

b)

Computation of CGT

21 The Income Tax Assessment Act 1997 (Cth), s 8.1

22 Ibid

23 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016)

Sec 8.1 Of the ITAA, 9721. Thus, the amount of One hundred and forty five dollars which was

used to buy black trousers and shirts would not be considered as a deductible amount.

g) The expenditure that has been ascending due to the income earning process of an

individual that is measureable is considered to be a deduction as per the provisions in Sec 8.1 of

ITAA, 9722. In the current scenario the three hundred dollars have been expended with the

employment contract which is existing with the new proprietor. It is not considered to be

deductible as it was not for the purpose of earning income and it would not be treated as

deduction since it is directly not considered to be related to income.

Answer 4

a)The category of F2 in the CGT events is considered to be dealt with the lending o or

renting of any kind of property or land which is in possession of an individual. It also includes a

fresh grant of lease which can be renewed or extended with the previous lease. Nevertheless,

there would be no availability of fifty percent discount in any CGT event. Therefore, the seven

thousand dollars received by John who is the owner of the land or the property is considered to

be CGT event F2 from David which would be exposed to CGT without any kind of discount

which is fifty percent23.

b)

Computation of CGT

21 The Income Tax Assessment Act 1997 (Cth), s 8.1

22 Ibid

23 Barkoczy, Stephen. "Foundations of taxation law 2016." (OUP Catalogue 2016)

8TAXATION LAW

2018-19

Item $ $

IOOF Shares

Net CGT gain 1200

Cost Proceeds 6700

Cost Base 5500

Greencross Shares

Net CGT gain 5880

Cost Proceed 14160

Cost Basse 20040

Net CGT Loss

4580

c) In the legal provision which has been laid down in the Sec 118.100 ITAA, 9724. If

there is a property or a land which has been engaged and unavailable by an individual with the

intention of treating it as a permanent residence the profits from such kind of a sale would be

considered as an exemption from CGT. For using such kind of an exemption, the land or the

property needs to be used and resided as a central residence. The borrowing of the land or the

property would not be considered as residential property. Similarly, if there is any kind of

business which is being carried out in that property and the other part is being used for residence

then such a sale of that property and the earnings of such sale would be exempted where the only

part which would be calculated would be the residential part.

d) The cost base is considered to imply the expense which has been sustained for the

attainment of any kind of asset under Sec 110.25 of the ITAA, 9725. This kind of cost includes

24The Income Tax Assessment Act 1997 (Cth), s 118.100

25 The Income Tax Assessment Act 1997 (Cth), s 110.25

2018-19

Item $ $

IOOF Shares

Net CGT gain 1200

Cost Proceeds 6700

Cost Base 5500

Greencross Shares

Net CGT gain 5880

Cost Proceed 14160

Cost Basse 20040

Net CGT Loss

4580

c) In the legal provision which has been laid down in the Sec 118.100 ITAA, 9724. If

there is a property or a land which has been engaged and unavailable by an individual with the

intention of treating it as a permanent residence the profits from such kind of a sale would be

considered as an exemption from CGT. For using such kind of an exemption, the land or the

property needs to be used and resided as a central residence. The borrowing of the land or the

property would not be considered as residential property. Similarly, if there is any kind of

business which is being carried out in that property and the other part is being used for residence

then such a sale of that property and the earnings of such sale would be exempted where the only

part which would be calculated would be the residential part.

d) The cost base is considered to imply the expense which has been sustained for the

attainment of any kind of asset under Sec 110.25 of the ITAA, 9725. This kind of cost includes

24The Income Tax Assessment Act 1997 (Cth), s 118.100

25 The Income Tax Assessment Act 1997 (Cth), s 110.25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

the value or the price of that asset and additionally it also includes the cost or the value of

holding and the cost of disposal which is relating to the asset or the property. There are five

components available which are the acquisition cost, owning cost, preservation cost, incidental

cost and conversion cost.

The reduced cost base is different and distinct from cost base and is considered to be

intended to be calculated by transaction or transfer of capital nature which has not presented any

kind of gain. The amount needs to be evaluated to discover any kind of loss which has been

sustained from such transaction. It has been laid down under Sec 110.55 ITAA, 9726.

Answer 5

a)Income, which can be earned through illegal ventures, might not be evaluated.

Nonetheless, it can only be considered to be evaluated if it is implemented in such a way which

would denote that it is for business.

b) Any kind of interest that might have been earned by fixed amount of money would be

considered to be ordinary income. In the case of Adelaide Fruit and Produce Exchange Co Ltd v

DFC of T (1932) 2 ATD 127the income that has been earned by exploiting a property by renting it

would be considered as an ordinary income. In this situation, from a bank if there is five hundred

dollars it is considered to be measurable but the rent amount which is two thousand dollars

would be measured as an income as well as any winnings from a casino.

26 The Income Tax Assessment Act 1997 (Cth), s 110.55

27 Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

the value or the price of that asset and additionally it also includes the cost or the value of

holding and the cost of disposal which is relating to the asset or the property. There are five

components available which are the acquisition cost, owning cost, preservation cost, incidental

cost and conversion cost.

The reduced cost base is different and distinct from cost base and is considered to be

intended to be calculated by transaction or transfer of capital nature which has not presented any

kind of gain. The amount needs to be evaluated to discover any kind of loss which has been

sustained from such transaction. It has been laid down under Sec 110.55 ITAA, 9726.

Answer 5

a)Income, which can be earned through illegal ventures, might not be evaluated.

Nonetheless, it can only be considered to be evaluated if it is implemented in such a way which

would denote that it is for business.

b) Any kind of interest that might have been earned by fixed amount of money would be

considered to be ordinary income. In the case of Adelaide Fruit and Produce Exchange Co Ltd v

DFC of T (1932) 2 ATD 127the income that has been earned by exploiting a property by renting it

would be considered as an ordinary income. In this situation, from a bank if there is five hundred

dollars it is considered to be measurable but the rent amount which is two thousand dollars

would be measured as an income as well as any winnings from a casino.

26 The Income Tax Assessment Act 1997 (Cth), s 110.55

27 Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

c) If an amount is handed over to any employee as an allowance by the employer of that

company for the employment it will be a measured within the taxable income for the employee

as stated in sec 15.2 ITAA, 9728. Therefore, it is a taxable as an income.

d) For the income of $ 20,000,

no imposition of Medicare Levy

For the income of $ 24900,

2% Levy amounting to $ 498

For the taxable income $100,000

2% Levy amounting to $ 2000.

e) For income amounting to $ 25,000, tax rate applicable will be 19 percent over $18,200

($25000 – $18200) * 19% = $6800 * 19% = $ 1,292

The gross payable tax = $1292.

For income amounting to $ 40,000, tax rate applicable will be 3,572 and 32.5 percent over $

37,000

$3572 + (40000-37000) * 32.5% = $ 3572 + 32.5% * $3000 = ($3572 + $975)

The gross payable tax = $ 4547.

For income amounting to $ 95,000, tax rate applicable will be 20,797 and 37 percent over $

90,000

$ 20,797 + (95,000-90,000)* 37% = $20,797 + 37% * $5000 = ($20,797 + $1850)

28 The Income Tax Assessment Act 1997 (Cth), s 15.2

c) If an amount is handed over to any employee as an allowance by the employer of that

company for the employment it will be a measured within the taxable income for the employee

as stated in sec 15.2 ITAA, 9728. Therefore, it is a taxable as an income.

d) For the income of $ 20,000,

no imposition of Medicare Levy

For the income of $ 24900,

2% Levy amounting to $ 498

For the taxable income $100,000

2% Levy amounting to $ 2000.

e) For income amounting to $ 25,000, tax rate applicable will be 19 percent over $18,200

($25000 – $18200) * 19% = $6800 * 19% = $ 1,292

The gross payable tax = $1292.

For income amounting to $ 40,000, tax rate applicable will be 3,572 and 32.5 percent over $

37,000

$3572 + (40000-37000) * 32.5% = $ 3572 + 32.5% * $3000 = ($3572 + $975)

The gross payable tax = $ 4547.

For income amounting to $ 95,000, tax rate applicable will be 20,797 and 37 percent over $

90,000

$ 20,797 + (95,000-90,000)* 37% = $20,797 + 37% * $5000 = ($20,797 + $1850)

28 The Income Tax Assessment Act 1997 (Cth), s 15.2

11TAXATION LAW

The gross payable tax = $ 22647.

The gross payable tax = $ 22647.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.