Taxation Law Assignment: Analyzing FBT, CGT & Income Tax Law

VerifiedAdded on 2023/04/03

|9

|2390

|91

Report

AI Summary

This assignment solution delves into various aspects of taxation law, primarily focusing on fringe benefit tax (FBT) and capital gains tax (CGT). It addresses the tax liability of fringe benefits provided by an employer to an employee, specifically examining a case involving a company car and the application of both the statutory formula method and the operating cost (log book) method for calculating taxable value. The analysis concludes that the statutory method is more suitable in the given scenario due to a lower tax payable value. Furthermore, the assignment explores capital gains tax implications related to the sale of different assets, including a house, a painting, a luxury yacht, and shares, identifying relevant CGT events and calculating net capital gains. The solution references relevant sections of the ITAA 1997 to support its analysis and computations. Desklib offers a range of similar solved assignments and past papers for students seeking assistance with their studies.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................5

Answer to question A:...............................................................................................5

Answer to B:..............................................................................................................7

Answer to C:..............................................................................................................7

References...................................................................................................................8

Table of Contents

Answer to question 1:...................................................................................................2

Answer to question 2:...................................................................................................5

Answer to question A:...............................................................................................5

Answer to B:..............................................................................................................7

Answer to C:..............................................................................................................7

References...................................................................................................................8

2TAXATION LAW

Answer to question 1:

Issues:

The current issue that is surrounding this case is the tax liability of the fringe

benefits provided by the employer to the employee in relation to the employment.

Rule:

Fringe benefit should be noted as the payment that is given to the employee

but it is not the same as the salary or the wages. As explained in the legislation of

the FBT, a fringe benefit should be viewed as the benefit that is given to employee in

discharge of his employment relationship. This eventually means under “section

136 (1), FBTAA 1986” the benefit that is provided to the employee since they are

the employee (Hodgson and Pearce 2015). Under the fringe benefit tax, the

employer is accountable for the fringe benefit tax if the employer makes the payment

to the employee, director of the company or the office holder that will be subject to

withholding obligations or if the benefits provided to the employee in respect of such

payments.

As the employer, they are required to pay the fringe benefit tax

notwithstanding of whether they are the sole trader, trustee, partnership or the

government authority. It is irrespective of whether the employer or the another party

provides the fringe benefit. The fringe benefit tax is payable whether or not the

employer is liable for paying other taxes particularly the income tax (Pearce and

Hodgson 2015). The employer can claim the income tax deduction for the cost of

offering benefit and for the amount of fringe benefit tax they pay.

As explained in the “section 7 (1), FBTAA 1986” a car fringe benefit

happens when the employer makes the available for the employee’s private use. An

employer makes the car available for their private use by the employee on any given

day if the car is generally used for the employee’s private purpose by the employee

or making the car available for their private use of the employee. As the general rule,

traveling from home to the work place is regarded as the private use of the car.

To calculate the taxable value of the car fringe benefit there are two methods.

This namely includes the statutory formula method and the operating cost method. A

taxpayer is mandatorily required to choose the statutory formula unless they elect to

make use of the operating cost methods (Braverman, Marsden and Sadiq 2015).

The taxpayer might elect to select the operating cost method for any or for all the

cars, notwithstanding which method they used in the earlier year. As per section 7

(8) of the FBTAA 1986 in order to use the operating cost method it is necessary to

use the log book for keeping records.

Application:

In application of the above stated rules it is noted that Spiceco Pty Ltd gave

his employer Lucinda with the car for making their private use. All through the FBT

year of 2018/19 the car was made available to the Lucinda for her private use. It can

be stated that the car was provided to Lucinda in respect of the employment with the

Spiceco Pty Ltd. With respect to “section 136 (1), FBTAA 1986” the benefit was

provided to Lucinda during the year of taxation by her employer in relation to the

employment (Young and Miles 2015).

Answer to question 1:

Issues:

The current issue that is surrounding this case is the tax liability of the fringe

benefits provided by the employer to the employee in relation to the employment.

Rule:

Fringe benefit should be noted as the payment that is given to the employee

but it is not the same as the salary or the wages. As explained in the legislation of

the FBT, a fringe benefit should be viewed as the benefit that is given to employee in

discharge of his employment relationship. This eventually means under “section

136 (1), FBTAA 1986” the benefit that is provided to the employee since they are

the employee (Hodgson and Pearce 2015). Under the fringe benefit tax, the

employer is accountable for the fringe benefit tax if the employer makes the payment

to the employee, director of the company or the office holder that will be subject to

withholding obligations or if the benefits provided to the employee in respect of such

payments.

As the employer, they are required to pay the fringe benefit tax

notwithstanding of whether they are the sole trader, trustee, partnership or the

government authority. It is irrespective of whether the employer or the another party

provides the fringe benefit. The fringe benefit tax is payable whether or not the

employer is liable for paying other taxes particularly the income tax (Pearce and

Hodgson 2015). The employer can claim the income tax deduction for the cost of

offering benefit and for the amount of fringe benefit tax they pay.

As explained in the “section 7 (1), FBTAA 1986” a car fringe benefit

happens when the employer makes the available for the employee’s private use. An

employer makes the car available for their private use by the employee on any given

day if the car is generally used for the employee’s private purpose by the employee

or making the car available for their private use of the employee. As the general rule,

traveling from home to the work place is regarded as the private use of the car.

To calculate the taxable value of the car fringe benefit there are two methods.

This namely includes the statutory formula method and the operating cost method. A

taxpayer is mandatorily required to choose the statutory formula unless they elect to

make use of the operating cost methods (Braverman, Marsden and Sadiq 2015).

The taxpayer might elect to select the operating cost method for any or for all the

cars, notwithstanding which method they used in the earlier year. As per section 7

(8) of the FBTAA 1986 in order to use the operating cost method it is necessary to

use the log book for keeping records.

Application:

In application of the above stated rules it is noted that Spiceco Pty Ltd gave

his employer Lucinda with the car for making their private use. All through the FBT

year of 2018/19 the car was made available to the Lucinda for her private use. It can

be stated that the car was provided to Lucinda in respect of the employment with the

Spiceco Pty Ltd. With respect to “section 136 (1), FBTAA 1986” the benefit was

provided to Lucinda during the year of taxation by her employer in relation to the

employment (Young and Miles 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

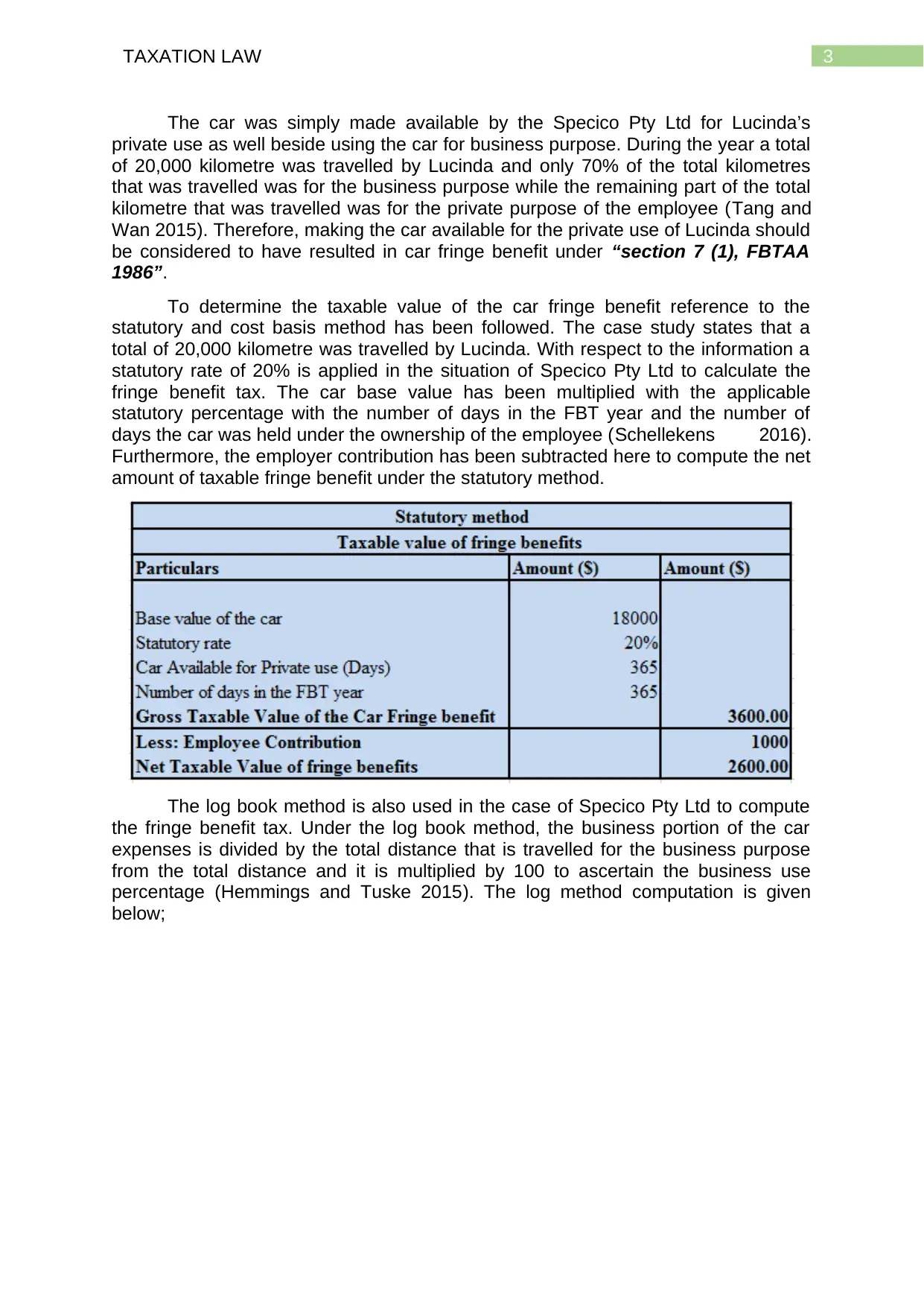

The car was simply made available by the Specico Pty Ltd for Lucinda’s

private use as well beside using the car for business purpose. During the year a total

of 20,000 kilometre was travelled by Lucinda and only 70% of the total kilometres

that was travelled was for the business purpose while the remaining part of the total

kilometre that was travelled was for the private purpose of the employee (Tang and

Wan 2015). Therefore, making the car available for the private use of Lucinda should

be considered to have resulted in car fringe benefit under “section 7 (1), FBTAA

1986”.

To determine the taxable value of the car fringe benefit reference to the

statutory and cost basis method has been followed. The case study states that a

total of 20,000 kilometre was travelled by Lucinda. With respect to the information a

statutory rate of 20% is applied in the situation of Specico Pty Ltd to calculate the

fringe benefit tax. The car base value has been multiplied with the applicable

statutory percentage with the number of days in the FBT year and the number of

days the car was held under the ownership of the employee (Schellekens 2016).

Furthermore, the employer contribution has been subtracted here to compute the net

amount of taxable fringe benefit under the statutory method.

The log book method is also used in the case of Specico Pty Ltd to compute

the fringe benefit tax. Under the log book method, the business portion of the car

expenses is divided by the total distance that is travelled for the business purpose

from the total distance and it is multiplied by 100 to ascertain the business use

percentage (Hemmings and Tuske 2015). The log method computation is given

below;

The car was simply made available by the Specico Pty Ltd for Lucinda’s

private use as well beside using the car for business purpose. During the year a total

of 20,000 kilometre was travelled by Lucinda and only 70% of the total kilometres

that was travelled was for the business purpose while the remaining part of the total

kilometre that was travelled was for the private purpose of the employee (Tang and

Wan 2015). Therefore, making the car available for the private use of Lucinda should

be considered to have resulted in car fringe benefit under “section 7 (1), FBTAA

1986”.

To determine the taxable value of the car fringe benefit reference to the

statutory and cost basis method has been followed. The case study states that a

total of 20,000 kilometre was travelled by Lucinda. With respect to the information a

statutory rate of 20% is applied in the situation of Specico Pty Ltd to calculate the

fringe benefit tax. The car base value has been multiplied with the applicable

statutory percentage with the number of days in the FBT year and the number of

days the car was held under the ownership of the employee (Schellekens 2016).

Furthermore, the employer contribution has been subtracted here to compute the net

amount of taxable fringe benefit under the statutory method.

The log book method is also used in the case of Specico Pty Ltd to compute

the fringe benefit tax. Under the log book method, the business portion of the car

expenses is divided by the total distance that is travelled for the business purpose

from the total distance and it is multiplied by 100 to ascertain the business use

percentage (Hemmings and Tuske 2015). The log method computation is given

below;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

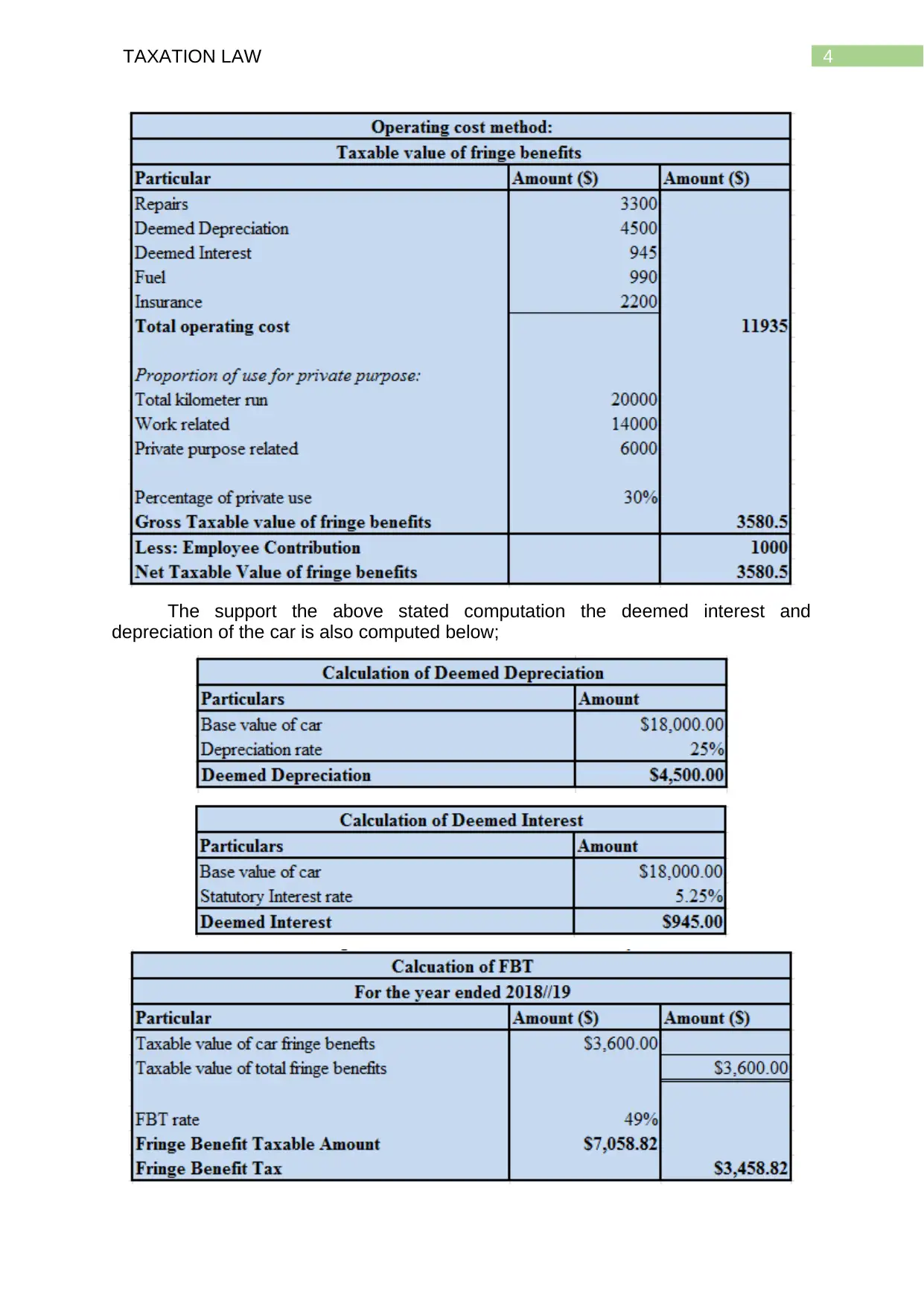

The support the above stated computation the deemed interest and

depreciation of the car is also computed below;

The support the above stated computation the deemed interest and

depreciation of the car is also computed below;

5TAXATION LAW

As evident from the above stated computation it can be stated that the log

book method of fringe benefit tax is more suitable for the Specico Pty Ltd because

the taxable value of the fringe is lower under the statutory method than the log book

method.

Conclusion:

As evident from the above stated computations it can be stated that providing

the car to Lucinda by Specico Pty Ltd should be considered as the car fringe benefit.

The statutory method of calculating the fringe benefit is more appropriate than the

log book method since the value of tax payable is lower under the statutory method.

Answer to question 2:

Answer to question A:

The provision of the capital gains is generally applied on the actual or the

realised gains. Capital gains is regarded as taxable under the statutory income

based on the “section 6-10, ITAA 1997” and it is included into the taxable income

of the taxpayer under the “section 102-5 (1) of the ITAA 1997”. The capital gains

are regarded taxable based on the marginal rate of tax however the discount may

imply that only 50% of the capital gains is taxable (White and Townsend 2018). CGT

events can be defined as the different type of event of the transaction or events that

may lead to capital gains or loss. As explained under the “section 104-10, ITAA

1997” a CGT event A1 happens when the assets are disposed by the taxpayer

(Burman et al. 2016). A CGT event A1 is applied only when the CGT asset is

purchased after the 19/09/1985.

In order to apply the CGT event A1 the CGT asset must be disposed to the

another entity. When the sale of asset happens under the contract the time of the

contract when the CGT event happens is considered important.

Sale of House and CGT:

“Section 104-150 of the ITAA 1997” is associated with the forfeiture of the

deposit. According to the “section 104-150 of the ITAA 1997” a CGT event H1

happens when the deposit on the prospective sale or other forms of transaction is

forfeited since the transaction does not proceed (Wanless 2018). A transaction for

selling the Doncaster property was entered by Daniel. The buyer agreed to buy the

property and deposited a sum of $85,000 however the transaction was failed and the

deposit was forfeited since no sale took place. Therefore, a CGT event H1 took

place since the deposit on the prospective sale was forfeited by Daniel due to the

non-execution of the transaction (Thuronyi and Brooks 2016). The amount of

$85,000 should be considered as the capital gain for Daniel less the cost of agent

fees that is paid with the failed transaction.

Sale of painting:

As explained in the “sec 108-10 to the sec 108-17” a collectable is referred

as one of the items that are listed in the “sec 108-10 (2)” mainly used or kept for the

use of the private use of the taxpayer (Lang et al. 2018). The above stated definition

of collectable includes the Antiques, art works such as paintings, jewellery, rare

books and the manuscripts. It should be noted that the capital loss from the

collectables should be separated and the capital loss is permitted for offset from the

capital gains that are made from the other collectables.

As evident from the above stated computation it can be stated that the log

book method of fringe benefit tax is more suitable for the Specico Pty Ltd because

the taxable value of the fringe is lower under the statutory method than the log book

method.

Conclusion:

As evident from the above stated computations it can be stated that providing

the car to Lucinda by Specico Pty Ltd should be considered as the car fringe benefit.

The statutory method of calculating the fringe benefit is more appropriate than the

log book method since the value of tax payable is lower under the statutory method.

Answer to question 2:

Answer to question A:

The provision of the capital gains is generally applied on the actual or the

realised gains. Capital gains is regarded as taxable under the statutory income

based on the “section 6-10, ITAA 1997” and it is included into the taxable income

of the taxpayer under the “section 102-5 (1) of the ITAA 1997”. The capital gains

are regarded taxable based on the marginal rate of tax however the discount may

imply that only 50% of the capital gains is taxable (White and Townsend 2018). CGT

events can be defined as the different type of event of the transaction or events that

may lead to capital gains or loss. As explained under the “section 104-10, ITAA

1997” a CGT event A1 happens when the assets are disposed by the taxpayer

(Burman et al. 2016). A CGT event A1 is applied only when the CGT asset is

purchased after the 19/09/1985.

In order to apply the CGT event A1 the CGT asset must be disposed to the

another entity. When the sale of asset happens under the contract the time of the

contract when the CGT event happens is considered important.

Sale of House and CGT:

“Section 104-150 of the ITAA 1997” is associated with the forfeiture of the

deposit. According to the “section 104-150 of the ITAA 1997” a CGT event H1

happens when the deposit on the prospective sale or other forms of transaction is

forfeited since the transaction does not proceed (Wanless 2018). A transaction for

selling the Doncaster property was entered by Daniel. The buyer agreed to buy the

property and deposited a sum of $85,000 however the transaction was failed and the

deposit was forfeited since no sale took place. Therefore, a CGT event H1 took

place since the deposit on the prospective sale was forfeited by Daniel due to the

non-execution of the transaction (Thuronyi and Brooks 2016). The amount of

$85,000 should be considered as the capital gain for Daniel less the cost of agent

fees that is paid with the failed transaction.

Sale of painting:

As explained in the “sec 108-10 to the sec 108-17” a collectable is referred

as one of the items that are listed in the “sec 108-10 (2)” mainly used or kept for the

use of the private use of the taxpayer (Lang et al. 2018). The above stated definition

of collectable includes the Antiques, art works such as paintings, jewellery, rare

books and the manuscripts. It should be noted that the capital loss from the

collectables should be separated and the capital loss is permitted for offset from the

capital gains that are made from the other collectables.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

As evident in the current situation an artistic painting was purchased for

$15,000 on 20th September 1985. The painting will be considered as the post-CGT

asset because it was purchased following the introduction of the CGT regime. The

painting was disposed on 31st May 2019 for sales value of $125,000. The sale of

painting has resulted in the capital gains. The capital gains made from the painting

should be regarded as the statutory income and will be included into the net income

of Daniel taxable earnings.

Sale of Luxury Yacht:

The personal use asset is explained in the “sec 108-20 to 108-30, ITAA

1997”. This implies the asset that is kept for personal enjoyment by taxpayers

(Santhanam 2016). These assets include the boats, racehorses, furniture etc. It is

noteworthy to denote that the capital gains that is derived from the sale of the

personal use asset are ignored if the acquisition cost of assets is lower than the

$10,000. On the other hand, “sec 108-20 (1), ITAA 1997” describes that when there

is a capital loss originating from sale of personal use asset then it should be

completely ignored.

A luxury yacht was acquired by Daniel in 2004 for $110,000. A luxury yacht

was sold for $60,000 on 1st June 2019. The sale of yacht has led to capital loss. On

the basis of “sec 108-20 (1), ITAA 1997” the capital loss that is suffered from the

sale of yacht by Daniel should be disregarded from his personal use asset (Pogge

and Mehta 2016).

Sale of Shares:

Referring “sec 108-5, ITAA 1997”, shares in the listed companies are also

regarded as the CGT asset (Cooper 2016). The ATO explains that the shares in the

company or the units in the unit trust are considered taxable in the similar manner as

the other asset for the capital gains tax purpose.

For the investor, the CGT is applied on the capital gains made on shares

when the CGT event happens (Buenker 2018). However, capital loss from shares is

only allowed to be offset against the capital gains from shares. Upon selling the BHP

shares the capital gains were made by the taxpayer. However, it also has the capital

loss from the AZJ shares that is carried forward to the current year for offset. The

shares have been offset to lower the net capital gains from the shares.

Calculations of Capital Gains Tax

For the year ended June 2019

Particulars Amount ($) Amount ($)

Capital gains from Doncaster House

Net Proceeds 85000

Less: Sales Commission 15000

Net Capital gains from Doncaster House 70000

Net Capital Gains on Sale of Painting

Proceeds from sell of Painting 125000

Cost base 15000

Gross Capital Gains (proceeds less cost base) 110000

As evident in the current situation an artistic painting was purchased for

$15,000 on 20th September 1985. The painting will be considered as the post-CGT

asset because it was purchased following the introduction of the CGT regime. The

painting was disposed on 31st May 2019 for sales value of $125,000. The sale of

painting has resulted in the capital gains. The capital gains made from the painting

should be regarded as the statutory income and will be included into the net income

of Daniel taxable earnings.

Sale of Luxury Yacht:

The personal use asset is explained in the “sec 108-20 to 108-30, ITAA

1997”. This implies the asset that is kept for personal enjoyment by taxpayers

(Santhanam 2016). These assets include the boats, racehorses, furniture etc. It is

noteworthy to denote that the capital gains that is derived from the sale of the

personal use asset are ignored if the acquisition cost of assets is lower than the

$10,000. On the other hand, “sec 108-20 (1), ITAA 1997” describes that when there

is a capital loss originating from sale of personal use asset then it should be

completely ignored.

A luxury yacht was acquired by Daniel in 2004 for $110,000. A luxury yacht

was sold for $60,000 on 1st June 2019. The sale of yacht has led to capital loss. On

the basis of “sec 108-20 (1), ITAA 1997” the capital loss that is suffered from the

sale of yacht by Daniel should be disregarded from his personal use asset (Pogge

and Mehta 2016).

Sale of Shares:

Referring “sec 108-5, ITAA 1997”, shares in the listed companies are also

regarded as the CGT asset (Cooper 2016). The ATO explains that the shares in the

company or the units in the unit trust are considered taxable in the similar manner as

the other asset for the capital gains tax purpose.

For the investor, the CGT is applied on the capital gains made on shares

when the CGT event happens (Buenker 2018). However, capital loss from shares is

only allowed to be offset against the capital gains from shares. Upon selling the BHP

shares the capital gains were made by the taxpayer. However, it also has the capital

loss from the AZJ shares that is carried forward to the current year for offset. The

shares have been offset to lower the net capital gains from the shares.

Calculations of Capital Gains Tax

For the year ended June 2019

Particulars Amount ($) Amount ($)

Capital gains from Doncaster House

Net Proceeds 85000

Less: Sales Commission 15000

Net Capital gains from Doncaster House 70000

Net Capital Gains on Sale of Painting

Proceeds from sell of Painting 125000

Cost base 15000

Gross Capital Gains (proceeds less cost base) 110000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

50% CGT Discount 55000

Taxable Capital Gains 55000

Capital gains on sale of shares

Gross Proceeds from Shares in BHP 80000

Less: Brokerage Fees 750

Net Proceeds 79250

Cost base

Less: Acquisition Cost 75000

Add: Stamp Duty on Purchase 250

Total Cost Base 75250

Capital gains on sale of BHP shares 4000

Less: Carry forward loss 10000

Net capital loss -6000

Net Capital gains 1,19,000

Answer to B:

Daniel has derived capital gains from the sale of antique painting and also

reported capital from the forfeited deposit of his Doncaster house. The net amount of

capital gains that is made during the year by Daniel can be used to fund his

superannuation fund.

Answer to C:

As understood, Daniel has incurred a capital loss from the sale of Yacht and

remaining amount of carry forward loss from the sale of AZJ shares. As a result, it is

recommended that the capital loss from AZJ shares should be carried forward to

subsequent years while the personal asset capital loss should be ignored.

50% CGT Discount 55000

Taxable Capital Gains 55000

Capital gains on sale of shares

Gross Proceeds from Shares in BHP 80000

Less: Brokerage Fees 750

Net Proceeds 79250

Cost base

Less: Acquisition Cost 75000

Add: Stamp Duty on Purchase 250

Total Cost Base 75250

Capital gains on sale of BHP shares 4000

Less: Carry forward loss 10000

Net capital loss -6000

Net Capital gains 1,19,000

Answer to B:

Daniel has derived capital gains from the sale of antique painting and also

reported capital from the forfeited deposit of his Doncaster house. The net amount of

capital gains that is made during the year by Daniel can be used to fund his

superannuation fund.

Answer to C:

As understood, Daniel has incurred a capital loss from the sale of Yacht and

remaining amount of carry forward loss from the sale of AZJ shares. As a result, it is

recommended that the capital loss from AZJ shares should be carried forward to

subsequent years while the personal asset capital loss should be ignored.

8TAXATION LAW

References

Braverman, D., Marsden, S. and Sadiq, K., 2015. Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl.

Tax'n, 17, p.1.

Buenker, J.D., 2018. The Income Tax and the Progressive Era. Routledge.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016.

Financial transaction taxes in theory and practice. National Tax Journal, 69(1),

p.171.

Cooper, R., 2016. Making sense of SA's tax and labour laws around labour brokers

and personal service providers: tax law. Tax Professional, 2016(28), pp.18-19.

Hemmings, P. and Tuske, A., 2015. Improving Taxes and Transfers in Australia.

Hodgson, H. and Pearce, P., 2015. TravelSmart of Travel Tax Breaks: Is the Fringe

Benefits Tax a Barrier to Active Commuting in Australia. eJTR, 13, p.819.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. eds., 2018. Introduction to

European tax law on direct taxation. Linde Verlag GmbH.

Pearce, P. and Hodgson, H., 2015. Promoting smart travel through tax policy. The

Tax Specialist, 19, pp.2-8.

Pogge, T. and Mehta, K. eds., 2016. Global tax fairness. Oxford University Press.

Santhanam, R., 2016. 51_Salaries and Income-Tax.

Schellekens, M., 2016. Global Corporate Tax Handbook 2016. Internat. Belasting

Documentatie.

Tang, R. and Wan, J., 2015. Fringe benefits tax and fly-in fly-out arrangements: John

Holland Group Pty Ltd v Commissioner of Taxation. Australian Resources and

Energy Law Journal, 34(1), p.17.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International

BV.

Wanless, P.T., 2018. Taxation in centrally planned economies. Routledge.

White, J. and Townsend, A., 2018. Deductibility of employee travel expenses: The

ATO's guidance. Taxation in Australia, 52(11), p.608.

Young, W. and Miles, C.F., 2015. A spatial study of parking policy and usage in

Melbourne, Australia. Case Studies on Transport Policy, 3(1), pp.23-32.

References

Braverman, D., Marsden, S. and Sadiq, K., 2015. Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl.

Tax'n, 17, p.1.

Buenker, J.D., 2018. The Income Tax and the Progressive Era. Routledge.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016.

Financial transaction taxes in theory and practice. National Tax Journal, 69(1),

p.171.

Cooper, R., 2016. Making sense of SA's tax and labour laws around labour brokers

and personal service providers: tax law. Tax Professional, 2016(28), pp.18-19.

Hemmings, P. and Tuske, A., 2015. Improving Taxes and Transfers in Australia.

Hodgson, H. and Pearce, P., 2015. TravelSmart of Travel Tax Breaks: Is the Fringe

Benefits Tax a Barrier to Active Commuting in Australia. eJTR, 13, p.819.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. eds., 2018. Introduction to

European tax law on direct taxation. Linde Verlag GmbH.

Pearce, P. and Hodgson, H., 2015. Promoting smart travel through tax policy. The

Tax Specialist, 19, pp.2-8.

Pogge, T. and Mehta, K. eds., 2016. Global tax fairness. Oxford University Press.

Santhanam, R., 2016. 51_Salaries and Income-Tax.

Schellekens, M., 2016. Global Corporate Tax Handbook 2016. Internat. Belasting

Documentatie.

Tang, R. and Wan, J., 2015. Fringe benefits tax and fly-in fly-out arrangements: John

Holland Group Pty Ltd v Commissioner of Taxation. Australian Resources and

Energy Law Journal, 34(1), p.17.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International

BV.

Wanless, P.T., 2018. Taxation in centrally planned economies. Routledge.

White, J. and Townsend, A., 2018. Deductibility of employee travel expenses: The

ATO's guidance. Taxation in Australia, 52(11), p.608.

Young, W. and Miles, C.F., 2015. A spatial study of parking policy and usage in

Melbourne, Australia. Case Studies on Transport Policy, 3(1), pp.23-32.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.