Taxation Law Assignment: Income Tax Liability and Legal Principles

VerifiedAdded on 2023/01/11

|12

|2995

|36

Homework Assignment

AI Summary

This assignment solution addresses key concepts in taxation law, including assessable income, allowable deductions, and income tax liability. Part A analyzes the tax implications for an individual, Arun Sharma, considering various income sources such as salary, reimbursements, gifts, business income, and rental income, along with related deductions. It applies relevant sections of the ITAA 1936 and ITAA 1997, and relevant case law to determine Arun's total assessable income and tax payable. Part B examines the case of Sun Newspaper Ltd v FCT (1938), discussing the facts, judgment, and the significance of the principles involved. The assignment demonstrates an understanding of income tax principles and their application in practical scenarios, offering a comprehensive overview of taxation law.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part A:........................................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................7

Part B: Sun Newspaper Ltd v FCT (1938).................................................................................8

Facts:......................................................................................................................................8

Judgement and reason for Judgement:.......................................................................................8

Significance of Principles in Case:........................................................................................8

References:...............................................................................................................................10

Table of Contents

Part A:........................................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................7

Part B: Sun Newspaper Ltd v FCT (1938).................................................................................8

Facts:......................................................................................................................................8

Judgement and reason for Judgement:.......................................................................................8

Significance of Principles in Case:........................................................................................8

References:...............................................................................................................................10

2TAXATION LAW

Part A:

Issues:

a. Will the taxpayer will be considered assessable for deriving income from the personal

exertion on the basis of ordinary meaning of “section 6-5, ITAA 1997”?

b. Whether or not the gains that are made from the business activities of the taxpayer

will be considered taxable during the course of business?

c. Whether or not the expenses that are incurred at the time of generating taxable

earnings is allowed for income tax deduction under “sec 8-1, ITAA 1997”?

Rule:

As defined in sec “6 (1) of the ITAA 1936”, income derived from an individual

private effort’s following the execution of the contract or conducting any personal services

generally includes the wages, salaries, bonus, fees, gratuities etc. The most important part is

to determine the nature of receipts that is received in the hands of taxpayer (Barkoczy, 2014).

The income earned from the private efforts is usually treated as income if it exhibits

satisfactory nexus with the income generating activities of the taxpayer. The decision of court

in “Hayes v FCT (1956)” explained that income derived from the personal exertion is

generally held as related to employment or receiving a reward in exchange of performing

service.

Certain circumstances explain that employers often pay the employee with the

expenses which is incurred by them. Where the employee is reimbursed by employer for any

kind of expenditure occurred by them then the reimbursed amount is held as non-taxable

earnings for employee (Grange et al., 2014). The employer on the other hand is held taxable

under the fringe benefit rules given in “section 23L of the ITAA 1936”.

Part A:

Issues:

a. Will the taxpayer will be considered assessable for deriving income from the personal

exertion on the basis of ordinary meaning of “section 6-5, ITAA 1997”?

b. Whether or not the gains that are made from the business activities of the taxpayer

will be considered taxable during the course of business?

c. Whether or not the expenses that are incurred at the time of generating taxable

earnings is allowed for income tax deduction under “sec 8-1, ITAA 1997”?

Rule:

As defined in sec “6 (1) of the ITAA 1936”, income derived from an individual

private effort’s following the execution of the contract or conducting any personal services

generally includes the wages, salaries, bonus, fees, gratuities etc. The most important part is

to determine the nature of receipts that is received in the hands of taxpayer (Barkoczy, 2014).

The income earned from the private efforts is usually treated as income if it exhibits

satisfactory nexus with the income generating activities of the taxpayer. The decision of court

in “Hayes v FCT (1956)” explained that income derived from the personal exertion is

generally held as related to employment or receiving a reward in exchange of performing

service.

Certain circumstances explain that employers often pay the employee with the

expenses which is incurred by them. Where the employee is reimbursed by employer for any

kind of expenditure occurred by them then the reimbursed amount is held as non-taxable

earnings for employee (Grange et al., 2014). The employer on the other hand is held taxable

under the fringe benefit rules given in “section 23L of the ITAA 1936”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Certain circumstances explain that receipts of prize money that holds satisfactory

nexus with the employment are treated as income. The decision in “Kelly v FCT (1985)”

explained that receiving the award for the best player was perceived as having the nexus with

the income producing acts of the taxpayer (Krever, 2015). The amount was taxable under

“section 6-5, ITAA 1997” since it was related to taxpayer’s skill and employment. On the

other hand, “section 21A, ITAA 1936” lay down that benefits that are non-convertible to cash

may be having relationship with the personal service of the taxpayer however, if the benefit

cannot be converted into cash then it is not held as income (Morgan et al., 2013). The court in

“Cooke & Sherden v FCT (1980)” noted that benefits which cannot be converted into

monies or monetary value hardly possess the income characteristics.

Gift that are simple gain do not have any kind of characteristics of income. The

verdict given in “Scott v FC of T (1966)” stated that gifts when it is received by taxpayer

because of their personal relation then the gift will be considered as having income character

(Sadiq & Coleman, 2013). The ATO further explains that a taxpayer is permitted to deduction

for the expenditure that are occurred while taking business trips. This includes the airfares,

taxi fares, accommodations etc. Taxpayers often receive voluntary payments that has

satisfactory relationship with their income generating activities. The voluntary payments are

treated as taxable income under ordinary meaning of “sec 6-5, ITAA 1997”. The court in

“Calvert v Wainwright (1947)” held that tips which is received by taxi driver was treated

taxable income under ordinary sense.

Where a taxpayer incurs any expenses that are related to the purchase price of the

acquiring or selling an investment property, no deduction is allowed to taxpayer in this

situation. Examples of such cost involves the purchase price of property, bank fees or stamp

duty etc. instead these costs are added to the cost base of the investment property for the

purpose of CGT (Sadiq, 2014). The taxpayers within the “sec 8-1, ITAA 1997” is only

Certain circumstances explain that receipts of prize money that holds satisfactory

nexus with the employment are treated as income. The decision in “Kelly v FCT (1985)”

explained that receiving the award for the best player was perceived as having the nexus with

the income producing acts of the taxpayer (Krever, 2015). The amount was taxable under

“section 6-5, ITAA 1997” since it was related to taxpayer’s skill and employment. On the

other hand, “section 21A, ITAA 1936” lay down that benefits that are non-convertible to cash

may be having relationship with the personal service of the taxpayer however, if the benefit

cannot be converted into cash then it is not held as income (Morgan et al., 2013). The court in

“Cooke & Sherden v FCT (1980)” noted that benefits which cannot be converted into

monies or monetary value hardly possess the income characteristics.

Gift that are simple gain do not have any kind of characteristics of income. The

verdict given in “Scott v FC of T (1966)” stated that gifts when it is received by taxpayer

because of their personal relation then the gift will be considered as having income character

(Sadiq & Coleman, 2013). The ATO further explains that a taxpayer is permitted to deduction

for the expenditure that are occurred while taking business trips. This includes the airfares,

taxi fares, accommodations etc. Taxpayers often receive voluntary payments that has

satisfactory relationship with their income generating activities. The voluntary payments are

treated as taxable income under ordinary meaning of “sec 6-5, ITAA 1997”. The court in

“Calvert v Wainwright (1947)” held that tips which is received by taxi driver was treated

taxable income under ordinary sense.

Where a taxpayer incurs any expenses that are related to the purchase price of the

acquiring or selling an investment property, no deduction is allowed to taxpayer in this

situation. Examples of such cost involves the purchase price of property, bank fees or stamp

duty etc. instead these costs are added to the cost base of the investment property for the

purpose of CGT (Sadiq, 2014). The taxpayers within the “sec 8-1, ITAA 1997” is only

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

entitled to claim deduction for expenses when the property is sub-let for producing rental

income.

There are two positive limbs given under “sec 8-1, ITAA 1997” which allows the

taxpayer claim for income tax deduction. Under the positive limbs the taxpayer is permitted

to deduction for outgoings that are incurred at the time of generating chargeable earnings.

While the negative limbs prohibit the taxpayer from claiming deductions for expenses that

are capital, private or domestic in nature (Weltman, 2013). Expenses that are preliminary to

the income generating activities of the taxpayer are not permitted for deduction under the

general provision of “sec 8-1, ITAA 1997”. The court in “Softwood Pulp and Paper v FC of

T (1976)” denied the taxpayer with deduction for expenses that were preliminary in the

income generating activities of the taxpayer since the expenses occurred at a point too soon.

For an expenses to qualify as income tax deduction must have satisfactory relation

with outgoings. In “Amalgamated Zinc v FCT (1935)” expenses that are occurred in the

course of producing or gaining income must be viewed as in the course of deriving proceeds

(Woellner, 2013). As per “section 6-5, ITAA 1997” gains earned from the normal business

proceeds are treated as taxable income. To characterise the business receipts it is necessary

that the taxpayer is conducting business activities and the proceeds forms the part of that

business activity.

As per the ATO, a taxpayer is permitted to obtain deduction for gifts that are given to

gift deductible recipients. Deduction for gifts and donation is only permitted if it is made to

the approved organizations.

Application:

The case study provides that Arun was employed with the Bell Computers Pty Ltd

and draws a salary of $85,000. Referring to “sec 6 (1) of the ITAA 1936” the employment

entitled to claim deduction for expenses when the property is sub-let for producing rental

income.

There are two positive limbs given under “sec 8-1, ITAA 1997” which allows the

taxpayer claim for income tax deduction. Under the positive limbs the taxpayer is permitted

to deduction for outgoings that are incurred at the time of generating chargeable earnings.

While the negative limbs prohibit the taxpayer from claiming deductions for expenses that

are capital, private or domestic in nature (Weltman, 2013). Expenses that are preliminary to

the income generating activities of the taxpayer are not permitted for deduction under the

general provision of “sec 8-1, ITAA 1997”. The court in “Softwood Pulp and Paper v FC of

T (1976)” denied the taxpayer with deduction for expenses that were preliminary in the

income generating activities of the taxpayer since the expenses occurred at a point too soon.

For an expenses to qualify as income tax deduction must have satisfactory relation

with outgoings. In “Amalgamated Zinc v FCT (1935)” expenses that are occurred in the

course of producing or gaining income must be viewed as in the course of deriving proceeds

(Woellner, 2013). As per “section 6-5, ITAA 1997” gains earned from the normal business

proceeds are treated as taxable income. To characterise the business receipts it is necessary

that the taxpayer is conducting business activities and the proceeds forms the part of that

business activity.

As per the ATO, a taxpayer is permitted to obtain deduction for gifts that are given to

gift deductible recipients. Deduction for gifts and donation is only permitted if it is made to

the approved organizations.

Application:

The case study provides that Arun was employed with the Bell Computers Pty Ltd

and draws a salary of $85,000. Referring to “sec 6 (1) of the ITAA 1936” the employment

5TAXATION LAW

receipt should be viewed as income from personal services. Citing “Hayes v FCT (1956)”

the income earned from the employment is treated as income since it exhibits satisfactory

nexus with the income generating activities of Arun (Woellner et al., 2014). The salary will

be considered taxable under ordinary meaning of “section 6-5, ITAA 1997”.

Arun was also reimbursed a sum of $2,910 for using his car for work related purpose.

The reimbursed expenditure occurred by Arun is held as non-taxable earnings for employee.

The employer on the other hand is held taxable under the fringe benefit rules given in

“section 23L of the ITAA 1936”.

Arun was awarded as the best employee of the year and was gifted with Sony TV that

has the market value of $6,000. The reward would be considered as the non-cash benefit for

Arun. Citing the event of “Cooke & Sherden v FCT (1980)” even though the award is

having relationship with the personal service of the taxpayer however, as the benefit cannot

be converted into cash it is not held as income (Klein et al., 2013). Arun also received a cash

gift of $2,000 from one of his friend as a wedding anniversary gift. Referring to “Scott v FC

of T (1966)” the gift of $2,000 received by Arun from his friend as wedding anniversary gift

cannot be considered income because the amount is purely received out of personal

relationship.

Arun reports expenses relating to airfares, accommodations and taxi trips that

amounted to $12,750. With respect to the guidelines of the ATO the expenses will be allowed

as deduction for Arun because it was incurred for business travel purpose. He later received

$880 as the token of honorarium for the year from the executive committee of Indian

Business. Quoting “Calvert v Wainwright (1947)” the token of honorarium is a voluntary

payment that is treated as taxable income under ordinary meaning of “sec 6-5, ITAA 1997”

(Bankman et al., 2018).

receipt should be viewed as income from personal services. Citing “Hayes v FCT (1956)”

the income earned from the employment is treated as income since it exhibits satisfactory

nexus with the income generating activities of Arun (Woellner et al., 2014). The salary will

be considered taxable under ordinary meaning of “section 6-5, ITAA 1997”.

Arun was also reimbursed a sum of $2,910 for using his car for work related purpose.

The reimbursed expenditure occurred by Arun is held as non-taxable earnings for employee.

The employer on the other hand is held taxable under the fringe benefit rules given in

“section 23L of the ITAA 1936”.

Arun was awarded as the best employee of the year and was gifted with Sony TV that

has the market value of $6,000. The reward would be considered as the non-cash benefit for

Arun. Citing the event of “Cooke & Sherden v FCT (1980)” even though the award is

having relationship with the personal service of the taxpayer however, as the benefit cannot

be converted into cash it is not held as income (Klein et al., 2013). Arun also received a cash

gift of $2,000 from one of his friend as a wedding anniversary gift. Referring to “Scott v FC

of T (1966)” the gift of $2,000 received by Arun from his friend as wedding anniversary gift

cannot be considered income because the amount is purely received out of personal

relationship.

Arun reports expenses relating to airfares, accommodations and taxi trips that

amounted to $12,750. With respect to the guidelines of the ATO the expenses will be allowed

as deduction for Arun because it was incurred for business travel purpose. He later received

$880 as the token of honorarium for the year from the executive committee of Indian

Business. Quoting “Calvert v Wainwright (1947)” the token of honorarium is a voluntary

payment that is treated as taxable income under ordinary meaning of “sec 6-5, ITAA 1997”

(Bankman et al., 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Arun also bought an investment property and incurred cost such as stamp duty, loan

application fees and solicitor cost while acquiring the property. Arun will not be permitted

deduction is in this situation because these costs are added to the cost base of the investment

property for the purpose of CGT.

He later rented out the property for $750 per week. The rental income that is received

from the investment property by Arun will be considered as taxable income under ordinary

meaning of “sec 6-5, ITAA 1997”. While the rental expenses such as council rates, property

agent fees, interest on loan and other expenses are allowed as general deduction under the

provision of “sec 8-1, ITAA 1997” (Oishi et al., 2018). This is because the expenses were

incurred while producing the taxable earnings.

Arun later opened a home based business however prior to opening business he

sought advice from their accountant regarding the formation of business and paid a sum of

$2,500 for that advice. Citing “Softwood Pulp and Paper v FC of T (1976)” the expenses are

preliminary to the income generating activities of Arun business operation and are not

permitted for deduction under the general provision of “sec 8-1, ITAA 1997”.

The cash receipts reported by Arun from his home based business included the

receipts from ABC Petrol Station Pty Ltd and Sweet Indian Restaurant. The receipts from his

home based business should be characterised as the ordinary gains from business and will be

included for assessment purpose within the ordinary meaning of “sec 6-5, ITAA 1997”

(Schmalbeck et al., 2015). Furthermore, a sum of $15,000 was accrued but only received on

10th July 2019. As the business receipts of Arun has been accounted under the cash basis the

sum of $15,000 will be included for taxable purpose in the current income year.

While referring to “Amalgamated Zinc v FCT (1935)” expenses that are occurred in

the course of producing or gaining income must be viewed as in the course of deriving

Arun also bought an investment property and incurred cost such as stamp duty, loan

application fees and solicitor cost while acquiring the property. Arun will not be permitted

deduction is in this situation because these costs are added to the cost base of the investment

property for the purpose of CGT.

He later rented out the property for $750 per week. The rental income that is received

from the investment property by Arun will be considered as taxable income under ordinary

meaning of “sec 6-5, ITAA 1997”. While the rental expenses such as council rates, property

agent fees, interest on loan and other expenses are allowed as general deduction under the

provision of “sec 8-1, ITAA 1997” (Oishi et al., 2018). This is because the expenses were

incurred while producing the taxable earnings.

Arun later opened a home based business however prior to opening business he

sought advice from their accountant regarding the formation of business and paid a sum of

$2,500 for that advice. Citing “Softwood Pulp and Paper v FC of T (1976)” the expenses are

preliminary to the income generating activities of Arun business operation and are not

permitted for deduction under the general provision of “sec 8-1, ITAA 1997”.

The cash receipts reported by Arun from his home based business included the

receipts from ABC Petrol Station Pty Ltd and Sweet Indian Restaurant. The receipts from his

home based business should be characterised as the ordinary gains from business and will be

included for assessment purpose within the ordinary meaning of “sec 6-5, ITAA 1997”

(Schmalbeck et al., 2015). Furthermore, a sum of $15,000 was accrued but only received on

10th July 2019. As the business receipts of Arun has been accounted under the cash basis the

sum of $15,000 will be included for taxable purpose in the current income year.

While referring to “Amalgamated Zinc v FCT (1935)” expenses that are occurred in

the course of producing or gaining income must be viewed as in the course of deriving

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

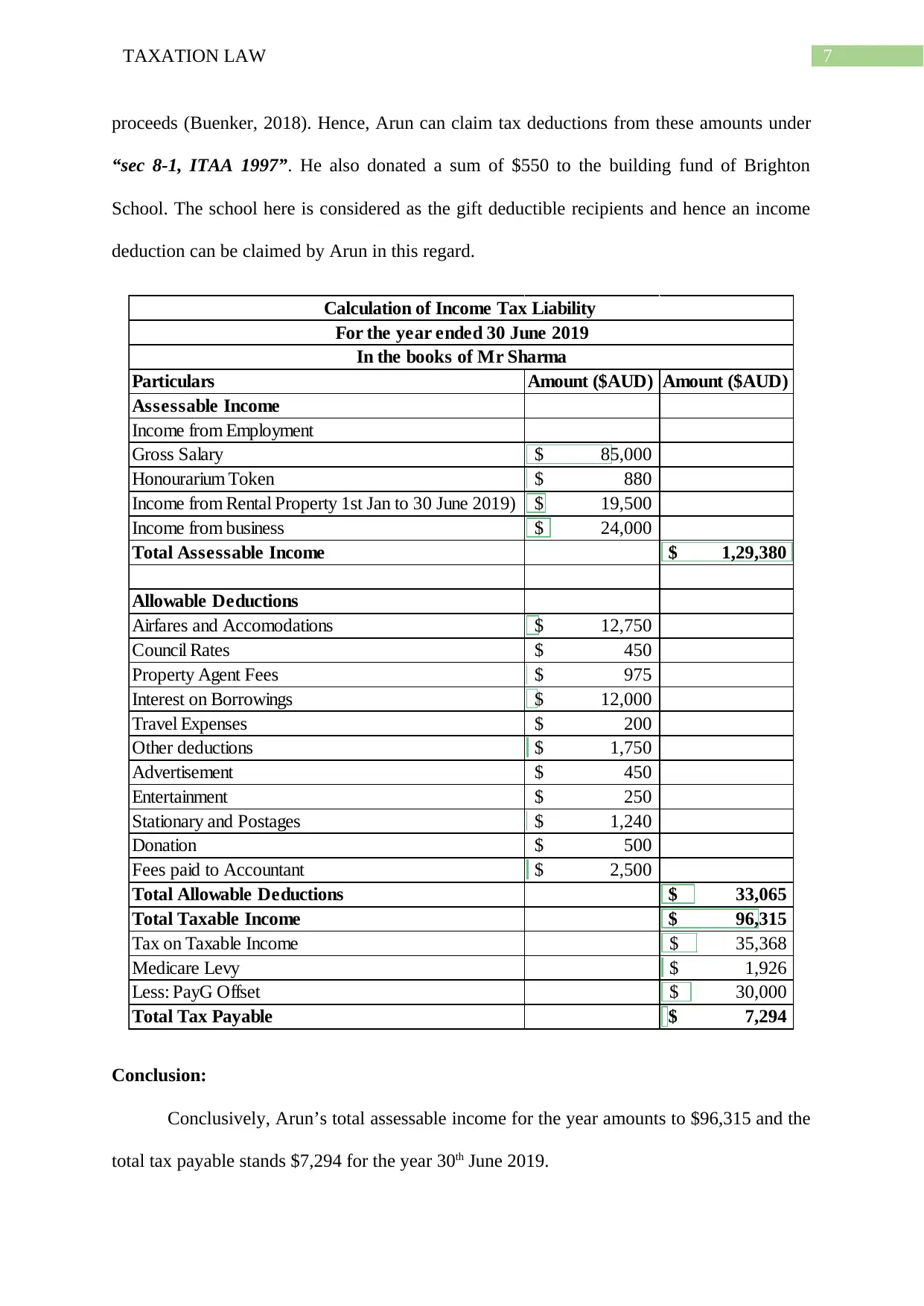

proceeds (Buenker, 2018). Hence, Arun can claim tax deductions from these amounts under

“sec 8-1, ITAA 1997”. He also donated a sum of $550 to the building fund of Brighton

School. The school here is considered as the gift deductible recipients and hence an income

deduction can be claimed by Arun in this regard.

Particulars Amount ($AUD) Amount ($AUD)

Assessable Income

Income from Employment

Gross Salary 85,000$

Honourarium Token 880$

Income from Rental Property 1st Jan to 30 June 2019) 19,500$

Income from business 24,000$

Total Assessable Income 1,29,380$

Allowable Deductions

Airfares and Accomodations 12,750$

Council Rates 450$

Property Agent Fees 975$

Interest on Borrowings 12,000$

Travel Expenses 200$

Other deductions 1,750$

Advertisement 450$

Entertainment 250$

Stationary and Postages 1,240$

Donation 500$

Fees paid to Accountant 2,500$

Total Allowable Deductions 33,065$

Total Taxable Income 96,315$

Tax on Taxable Income 35,368$

Medicare Levy 1,926$

Less: PayG Offset 30,000$

Total Tax Payable 7,294$

Calculation of Income Tax Liability

For the year ended 30 June 2019

In the books of Mr Sharma

Conclusion:

Conclusively, Arun’s total assessable income for the year amounts to $96,315 and the

total tax payable stands $7,294 for the year 30th June 2019.

proceeds (Buenker, 2018). Hence, Arun can claim tax deductions from these amounts under

“sec 8-1, ITAA 1997”. He also donated a sum of $550 to the building fund of Brighton

School. The school here is considered as the gift deductible recipients and hence an income

deduction can be claimed by Arun in this regard.

Particulars Amount ($AUD) Amount ($AUD)

Assessable Income

Income from Employment

Gross Salary 85,000$

Honourarium Token 880$

Income from Rental Property 1st Jan to 30 June 2019) 19,500$

Income from business 24,000$

Total Assessable Income 1,29,380$

Allowable Deductions

Airfares and Accomodations 12,750$

Council Rates 450$

Property Agent Fees 975$

Interest on Borrowings 12,000$

Travel Expenses 200$

Other deductions 1,750$

Advertisement 450$

Entertainment 250$

Stationary and Postages 1,240$

Donation 500$

Fees paid to Accountant 2,500$

Total Allowable Deductions 33,065$

Total Taxable Income 96,315$

Tax on Taxable Income 35,368$

Medicare Levy 1,926$

Less: PayG Offset 30,000$

Total Tax Payable 7,294$

Calculation of Income Tax Liability

For the year ended 30 June 2019

In the books of Mr Sharma

Conclusion:

Conclusively, Arun’s total assessable income for the year amounts to $96,315 and the

total tax payable stands $7,294 for the year 30th June 2019.

8TAXATION LAW

Part B: Sun Newspaper Ltd v FCT (1938)

Facts:

The taxpayer in the current case paid a lump sum amount in the form of instalment

over the period of three years to the competitor as the consideration for the competitor not

being related with the production of the daily paper inside the 300 miles of Sydney. Sun

Newspaper Ltd published in Sydney an evening newspaper (Mertens & Montiel Olea, 2018).

The company when became aware regarding the intention of the rival publisher decided to

publish a new evening paper but sold it a cheaper cost than its own newspaper. Sun

Newspaper agreed to pay a sum of $86,000 in the form of instalment to the rival publisher

based on the condition that the rival newspaper would not be publishing paper in Sydney for

three years. Sun Newspaper claimed the amount as deduction.

Judgement and reason for Judgement:

The high court held that the lump sum cannot be considered deductible since it was

capital in nature. The main reason for judgement was that the expenses were directed towards

strengthening and preserving the profit making structure. Therefore, the expenses was

considered as capital in nature.

Significance of Principles in Case:

An important test that originated from the case of “Sun Newspaper Ltd v FCT

(1938)” was to differentiate the expenses among the profit making structure and the profit

deriving procedure (Lieuallen & Shurtz, 2018). The significance of principles in this case was

dependent on three factors;

a. The nature of advantage that was sought

b. The way in which it would be used and enjoyed upon, and;

Part B: Sun Newspaper Ltd v FCT (1938)

Facts:

The taxpayer in the current case paid a lump sum amount in the form of instalment

over the period of three years to the competitor as the consideration for the competitor not

being related with the production of the daily paper inside the 300 miles of Sydney. Sun

Newspaper Ltd published in Sydney an evening newspaper (Mertens & Montiel Olea, 2018).

The company when became aware regarding the intention of the rival publisher decided to

publish a new evening paper but sold it a cheaper cost than its own newspaper. Sun

Newspaper agreed to pay a sum of $86,000 in the form of instalment to the rival publisher

based on the condition that the rival newspaper would not be publishing paper in Sydney for

three years. Sun Newspaper claimed the amount as deduction.

Judgement and reason for Judgement:

The high court held that the lump sum cannot be considered deductible since it was

capital in nature. The main reason for judgement was that the expenses were directed towards

strengthening and preserving the profit making structure. Therefore, the expenses was

considered as capital in nature.

Significance of Principles in Case:

An important test that originated from the case of “Sun Newspaper Ltd v FCT

(1938)” was to differentiate the expenses among the profit making structure and the profit

deriving procedure (Lieuallen & Shurtz, 2018). The significance of principles in this case was

dependent on three factors;

a. The nature of advantage that was sought

b. The way in which it would be used and enjoyed upon, and;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

c. The method undertaken to obtain it.

Expenditure might be capital where it is incurred to defend or acquire structural

assets. Referring to example of “BP Australia Ltd v FCT (1965)” expenses may be

considered capital if the resulted in advantage over the competitors (Woellner, 2013). While

the court in “John Fairfax and Sons Ltd v FC of T (1969)” held that expenses incurred in

acquiring or removing competitors are considered capital in nature because it is mainly

incurred to prevent or protect the business against the threat of extinction.

c. The method undertaken to obtain it.

Expenditure might be capital where it is incurred to defend or acquire structural

assets. Referring to example of “BP Australia Ltd v FCT (1965)” expenses may be

considered capital if the resulted in advantage over the competitors (Woellner, 2013). While

the court in “John Fairfax and Sons Ltd v FC of T (1969)” held that expenses incurred in

acquiring or removing competitors are considered capital in nature because it is mainly

incurred to prevent or protect the business against the threat of extinction.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Bankman, J., Shaviro, D. N., Stark, K. J., & Kleinbard, E. D. (2018). Federal Income

Taxation. Aspen Publishers.

Barkoczy, S. (2014). Foundations of taxation law 2014.

Buenker, J. D. (2018). The Income Tax and the Progressive Era. Routledge.

Grange, J., Jover-Ledesma, G., & Maydew, G. (2014). Principles of business taxation.

Klein, W. A., Bankman, J., & Shaviro, D. N. (2013). Federal income taxation (pp. 184-86).

Aspen Publishers.

Krever, R. (2015). Australian taxation law cases.

Lieuallen, G. G., & Shurtz, N. E. (2018). Emanuel Law Outlines for Basic Federal Income

Tax. Aspen Publishers.

Mertens, K., & Montiel Olea, J. L. (2018). Marginal tax rates and income: New time series

evidence. The Quarterly Journal of Economics, 133(4), 1803-1884.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Oishi, S., Kushlev, K., & Schimmack, U. (2018). Progressive taxation, income inequality,

and happiness. American Psychologist, 73(2), 157.

Sadiq, K. (2014). Principles of taxation law.

Sadiq, K., & Coleman, C. (2013). Principles of taxation law 2013. Sydney, N.S.W.: Lawbook

Co./Thomson Reuters.

References:

Bankman, J., Shaviro, D. N., Stark, K. J., & Kleinbard, E. D. (2018). Federal Income

Taxation. Aspen Publishers.

Barkoczy, S. (2014). Foundations of taxation law 2014.

Buenker, J. D. (2018). The Income Tax and the Progressive Era. Routledge.

Grange, J., Jover-Ledesma, G., & Maydew, G. (2014). Principles of business taxation.

Klein, W. A., Bankman, J., & Shaviro, D. N. (2013). Federal income taxation (pp. 184-86).

Aspen Publishers.

Krever, R. (2015). Australian taxation law cases.

Lieuallen, G. G., & Shurtz, N. E. (2018). Emanuel Law Outlines for Basic Federal Income

Tax. Aspen Publishers.

Mertens, K., & Montiel Olea, J. L. (2018). Marginal tax rates and income: New time series

evidence. The Quarterly Journal of Economics, 133(4), 1803-1884.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Oishi, S., Kushlev, K., & Schimmack, U. (2018). Progressive taxation, income inequality,

and happiness. American Psychologist, 73(2), 157.

Sadiq, K. (2014). Principles of taxation law.

Sadiq, K., & Coleman, C. (2013). Principles of taxation law 2013. Sydney, N.S.W.: Lawbook

Co./Thomson Reuters.

11TAXATION LAW

Schmalbeck, R., Zelenak, L., & Lawsky, S. B. (2015). Federal Income Taxation. Wolters

Kluwer Law & Business.

Weltman, B. (2013). J.K. Lasser's 1001 deductions and tax breaks 2013. Hoboken, N.J: John

Wiley & Sons.

Woellner, R. (2013). Australian taxation law select 2013. North Ryde, N.S.W.: CCH

Australia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2014). Australian taxation

law 2014.

Schmalbeck, R., Zelenak, L., & Lawsky, S. B. (2015). Federal Income Taxation. Wolters

Kluwer Law & Business.

Weltman, B. (2013). J.K. Lasser's 1001 deductions and tax breaks 2013. Hoboken, N.J: John

Wiley & Sons.

Woellner, R. (2013). Australian taxation law select 2013. North Ryde, N.S.W.: CCH

Australia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2014). Australian taxation

law 2014.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.