Taxation Law: Assessing Anna McCartney's Taxable Income and Deductions

VerifiedAdded on 2023/01/10

|11

|2481

|80

Report

AI Summary

This report provides a detailed analysis of Anna McCartney's tax situation, covering various aspects of Australian taxation law. It examines the assessability of her income, including a sign-on bonus, salary, and bonuses received during the financial year 2017-2018. The report delves into the tax treatment of her employer's superannuation contributions and Anna's own salary sacrifice contributions. It further explores the deductibility of work-related expenses, such as travel and conference fees, as well as car allowances. The report also addresses the tax implications of frequent flyer points and a compensation payment received due to workplace injuries. The analysis is supported by relevant case law, legislative references, and rulings, providing a comprehensive understanding of Anna's taxable income and allowable deductions. The report concludes with a summary of Anna's assessable income, allowable deductions, and total taxable income for the financial year.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1..................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................5

Conclusion:............................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Answer to question 1..................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................5

Conclusion:............................................................................................................................8

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1

Issues:

Is Anna held assessable for the numerous receipts that is received by her in the course

of her employment in accordance with the ordinary concepts of “section 6-5, ITAA 1997”? Is

Anna entitled to income tax deduction for outgoings occurred while gaining the taxable

income within the positive limbs of “section 8-1, ITAA 1997”?

Rule:

According to “section 6, ITAA 1936”, receipts that is earned from the employment

and providing personal services will be considered taxable in the hands the recipient. If the

receipts has sufficient connection with the taxpayer’s personal services then it will be treated

as income according to ordinary concepts1. Usually nexus is found with the common items of

personal exertion income. This includes the wages, salaries, commissions and bonus.

According to the “section 6-5 (1), ITAA 1997” the taxable income of the taxpayer commonly

includes the income from ordinary concepts. The commissioner in “Scott v CT (1935)” stated

that the income cannot be regarded as the simple word of art and necessarily requires the

implementation of the adequate principles to consider the receipts within the meaning of

ordinary concepts2.

Employers sometime to attract the candidates offers them with the sign-on fees.

Correspondingly, in “FCT v Pickford (1998)” the sign on fees which is received by

employee on joining was treated as payment made for the future services and was treated as

ordinary income. Income derived from personal services such as employment remuneration

1 LJ Nethercott, G Richardson and K Devos, Australian Taxation Study Manual, Questions and Suggested Solutions (28th

edn, Oxford University Press, 2018)

2 Woellner, Barkoczy, Murphy, Evans and Pinto, Australian Taxation Law (29th edn, Oxford University Press 2019)

Answer to question 1

Issues:

Is Anna held assessable for the numerous receipts that is received by her in the course

of her employment in accordance with the ordinary concepts of “section 6-5, ITAA 1997”? Is

Anna entitled to income tax deduction for outgoings occurred while gaining the taxable

income within the positive limbs of “section 8-1, ITAA 1997”?

Rule:

According to “section 6, ITAA 1936”, receipts that is earned from the employment

and providing personal services will be considered taxable in the hands the recipient. If the

receipts has sufficient connection with the taxpayer’s personal services then it will be treated

as income according to ordinary concepts1. Usually nexus is found with the common items of

personal exertion income. This includes the wages, salaries, commissions and bonus.

According to the “section 6-5 (1), ITAA 1997” the taxable income of the taxpayer commonly

includes the income from ordinary concepts. The commissioner in “Scott v CT (1935)” stated

that the income cannot be regarded as the simple word of art and necessarily requires the

implementation of the adequate principles to consider the receipts within the meaning of

ordinary concepts2.

Employers sometime to attract the candidates offers them with the sign-on fees.

Correspondingly, in “FCT v Pickford (1998)” the sign on fees which is received by

employee on joining was treated as payment made for the future services and was treated as

ordinary income. Income derived from personal services such as employment remuneration

1 LJ Nethercott, G Richardson and K Devos, Australian Taxation Study Manual, Questions and Suggested Solutions (28th

edn, Oxford University Press, 2018)

2 Woellner, Barkoczy, Murphy, Evans and Pinto, Australian Taxation Law (29th edn, Oxford University Press 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

are held taxable in the hands of recipient3. As held in “Dean & Anor v FCT (1997)”

employment remuneration paid to the employee for being employed following the acquisition

of the company was considered as income under ordinary concepts.

According to the “section 23L, ITAA 1936”, if an employer provides any kind of

benefit of the employee then the benefit will not be considered as taxable for the employees.

If the employer pays the superannuation contribution to the employee, then the amount of

contribution paid to superfund cannot be considered as income for the employee. As stated by

the ATO salary sacrifice constitute a preparation which is usually treated as total

remuneration packages4. It is treated as arrangement between the employer and employee

given the employee decides to sacrifice a part of their future entitlements towards salary or

wages. If the employee makes a superannuation contribution on his own then the amount can

be claimed as deduction by the employee.

The ATO explains that employees that incurs cost of travelling to attend the seminars

or conference related to work then a deduction can be claimed for expenses incurred in

attending the seminars, conferences and education workshops. As stated in “section 15-2” an

employee during the course of employment may receive certain benefits. Such benefits may

be considered as taxable earnings together with the non-cash benefits that cannot be

converted into cash in accordance with ordinary meaning5. These amounts includes bonuses,

premium or allowances and gratuities.

As stated under the “Taxation Ruling of TR 1999/6” the taxpayers not required to

declare in their assessable the value of frequent flyer points which they accrued from frequent

3 Sadiq, Australian Taxation Law Cases (Thomson Reuters, 2019)

4 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

5 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

are held taxable in the hands of recipient3. As held in “Dean & Anor v FCT (1997)”

employment remuneration paid to the employee for being employed following the acquisition

of the company was considered as income under ordinary concepts.

According to the “section 23L, ITAA 1936”, if an employer provides any kind of

benefit of the employee then the benefit will not be considered as taxable for the employees.

If the employer pays the superannuation contribution to the employee, then the amount of

contribution paid to superfund cannot be considered as income for the employee. As stated by

the ATO salary sacrifice constitute a preparation which is usually treated as total

remuneration packages4. It is treated as arrangement between the employer and employee

given the employee decides to sacrifice a part of their future entitlements towards salary or

wages. If the employee makes a superannuation contribution on his own then the amount can

be claimed as deduction by the employee.

The ATO explains that employees that incurs cost of travelling to attend the seminars

or conference related to work then a deduction can be claimed for expenses incurred in

attending the seminars, conferences and education workshops. As stated in “section 15-2” an

employee during the course of employment may receive certain benefits. Such benefits may

be considered as taxable earnings together with the non-cash benefits that cannot be

converted into cash in accordance with ordinary meaning5. These amounts includes bonuses,

premium or allowances and gratuities.

As stated under the “Taxation Ruling of TR 1999/6” the taxpayers not required to

declare in their assessable the value of frequent flyer points which they accrued from frequent

3 Sadiq, Australian Taxation Law Cases (Thomson Reuters, 2019)

4 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

5 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

work trip during employment6. As defined in the “section 21A, 1936” non-cash benefit may

be having the nexus with the taxpayer’s income activities but not an income if it is non-

convertible to cash. A non-cash benefits might have relation with the personal services but if

it is not convertible into cash then it is not an income7. The federal commissioner in “Payne v

FCT (1996)” held that the redemption of frequent flyer points accrued from the work purpose

travel is not treated as income.

As per the “section 15-2, ITAA 1997” the taxpayers taxable earnings comprises of the

bonuses, gratuities, compensation and benefits that is provided to them in discharge of their

services by working as employee8.

Compensation generally holds the character that is intended to replace. If the

taxpayers receives the compensation relating to the loss of capital asset, the amount that is

received is regarded as capital in nature and not an ordinary income. On receiving

compensation relating to loss of earning income and sustaining personal injury then the

amount that is received is not treated income as it holds capital in character9. Receipt of lump

payment for the sustaining injuries that effects the earning ability in future is treated non-

taxable as ordinary income under the “section 6-5, ITAA 1997”. As per the ATO

compensation payment received either in lump sum or as the periodical payment does not

holds an income character.

6 Barkoczy, 2019 Core Tax Legislation and Study Guide, (22nd edition, Oxford University Press 2019)

7 Freudenberg, Brett, et al. "Tax literacy of Australian small businesses." J. Austl. Tax'n 19 (2017): 21.

8 Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian taxation law 2018. Oxford

University Press, 2018.

9 Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J. Australasian Tax Tchrs. Ass'n 13

(2018): 307.

work trip during employment6. As defined in the “section 21A, 1936” non-cash benefit may

be having the nexus with the taxpayer’s income activities but not an income if it is non-

convertible to cash. A non-cash benefits might have relation with the personal services but if

it is not convertible into cash then it is not an income7. The federal commissioner in “Payne v

FCT (1996)” held that the redemption of frequent flyer points accrued from the work purpose

travel is not treated as income.

As per the “section 15-2, ITAA 1997” the taxpayers taxable earnings comprises of the

bonuses, gratuities, compensation and benefits that is provided to them in discharge of their

services by working as employee8.

Compensation generally holds the character that is intended to replace. If the

taxpayers receives the compensation relating to the loss of capital asset, the amount that is

received is regarded as capital in nature and not an ordinary income. On receiving

compensation relating to loss of earning income and sustaining personal injury then the

amount that is received is not treated income as it holds capital in character9. Receipt of lump

payment for the sustaining injuries that effects the earning ability in future is treated non-

taxable as ordinary income under the “section 6-5, ITAA 1997”. As per the ATO

compensation payment received either in lump sum or as the periodical payment does not

holds an income character.

6 Barkoczy, 2019 Core Tax Legislation and Study Guide, (22nd edition, Oxford University Press 2019)

7 Freudenberg, Brett, et al. "Tax literacy of Australian small businesses." J. Austl. Tax'n 19 (2017): 21.

8 Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian taxation law 2018. Oxford

University Press, 2018.

9 Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J. Australasian Tax Tchrs. Ass'n 13

(2018): 307.

5TAXATION LAW

Application:

Anna began working from 1st August 2017 and soon when she joined, a joining bonus

of $5,000 was given to Anna. With reference to “FCT v Pickford (1998)” the sign on fees

which is received by Anna on joining is treated as payment made for the future services and

under “section 6-5 (1), ITAA 1997” it constitute an ordinary income10.

During her employment period she was given the salaries and additional bonus that

were subjected to market conditions. Quoting the decision made in “Dean & Anor v FCT

(1997)” employment remuneration and bonuses paid to Anna should be considered as income

under ordinary concepts of “section 6-5 (1), ITAA 1997”11. The receipts has sufficient nexus

with the income producing activities of Anna and is earned during her course of employment.

While the second bonus of $15,000 was paid to her during 12th July 2018 which is in the next

income year cycle. So the amount will not be included for assessment purpose for the year

ended 30th June 2018.

During the year employer contributed an amount of $13,500 into the personal

superannuation fund of Anna. Taking into the account the “section 23L, ITAA 1936” the

superannuation contribution paid by employer on behalf of Anna constitutes non-assessable

benefit for Anna. Later Anna also made a salary sacrifice to personally contribute in her

superannuation fund. The amount of $5,000 can be claimed as deduction by the Anna since it

was related to derivation of her assessable income.

During the year Anna reported the expenses that were incurred while travelling to

attend the conference on finance. Under the positive limbs of “section 8-1, ITAA 1997” the

10 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

11 Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law Select 2019: Legislation And

Commentary. Oxford University Press, 2019.

Application:

Anna began working from 1st August 2017 and soon when she joined, a joining bonus

of $5,000 was given to Anna. With reference to “FCT v Pickford (1998)” the sign on fees

which is received by Anna on joining is treated as payment made for the future services and

under “section 6-5 (1), ITAA 1997” it constitute an ordinary income10.

During her employment period she was given the salaries and additional bonus that

were subjected to market conditions. Quoting the decision made in “Dean & Anor v FCT

(1997)” employment remuneration and bonuses paid to Anna should be considered as income

under ordinary concepts of “section 6-5 (1), ITAA 1997”11. The receipts has sufficient nexus

with the income producing activities of Anna and is earned during her course of employment.

While the second bonus of $15,000 was paid to her during 12th July 2018 which is in the next

income year cycle. So the amount will not be included for assessment purpose for the year

ended 30th June 2018.

During the year employer contributed an amount of $13,500 into the personal

superannuation fund of Anna. Taking into the account the “section 23L, ITAA 1936” the

superannuation contribution paid by employer on behalf of Anna constitutes non-assessable

benefit for Anna. Later Anna also made a salary sacrifice to personally contribute in her

superannuation fund. The amount of $5,000 can be claimed as deduction by the Anna since it

was related to derivation of her assessable income.

During the year Anna reported the expenses that were incurred while travelling to

attend the conference on finance. Under the positive limbs of “section 8-1, ITAA 1997” the

10 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

11 Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law Select 2019: Legislation And

Commentary. Oxford University Press, 2019.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

travelling cost and conferences fees can be claimed as allowable deduction since the expenses

were occurred in the process of earning assessable income. Anna also received a sum of

$2,000 as the allowance to defray the incidental expenditure. With respect to the “section 15-

2” the allowance received is in relation to the course of employment and holds clear nexus

with the personal service income. Therefore, it is a statutory income which attracts tax

liability.

As the part of the work-related travel Anna accrued frequent flyer points with Qantas.

With reference to the example of “Payne v FCT (1996)” the redemption of frequent flyer

points accrued from the work purpose travel is not treated as income under ordinary concepts

of “section 6-5, ITAA 1997”12. Under “section 21A, ITAA 1936”, the frequent flyer points

are a non-cash benefit for Anna since it is non-convertible cash. As a general rule the

frequent flyer points were regarded as the employer paid expenditure despite the fact that it

had connection with the employment service of Anna but the amount was non-convertible to

cash and therefore not an income in accordance with ordinary concepts.

In order to travel to work, Anna used her personal car. The employer paid Anna with

the 80 cents for the total kilometres that were travelled for work purpose. A work related car

allowances was provided to Anna by her employer that amounted to $2,250. Citing “section

15-2, ITAA 1997”, the car allowances that is received by Anna should be included in the

assessable income as statutory income because it was paid to Anna during the course of her

employment for rendering the services by working as the employee.

In the mid-June a compensation payment of $130,000 was paid to Anna from her

previous employer relating to the injuries suffered at work place. It should be noted that the

compensation that was paid to Anna was for the injuries suffered at the work place. The

12 Kenny, P. Australian tax. Chatswood, N.S.W.: (LexisNexis Butterworths 2013).

travelling cost and conferences fees can be claimed as allowable deduction since the expenses

were occurred in the process of earning assessable income. Anna also received a sum of

$2,000 as the allowance to defray the incidental expenditure. With respect to the “section 15-

2” the allowance received is in relation to the course of employment and holds clear nexus

with the personal service income. Therefore, it is a statutory income which attracts tax

liability.

As the part of the work-related travel Anna accrued frequent flyer points with Qantas.

With reference to the example of “Payne v FCT (1996)” the redemption of frequent flyer

points accrued from the work purpose travel is not treated as income under ordinary concepts

of “section 6-5, ITAA 1997”12. Under “section 21A, ITAA 1936”, the frequent flyer points

are a non-cash benefit for Anna since it is non-convertible cash. As a general rule the

frequent flyer points were regarded as the employer paid expenditure despite the fact that it

had connection with the employment service of Anna but the amount was non-convertible to

cash and therefore not an income in accordance with ordinary concepts.

In order to travel to work, Anna used her personal car. The employer paid Anna with

the 80 cents for the total kilometres that were travelled for work purpose. A work related car

allowances was provided to Anna by her employer that amounted to $2,250. Citing “section

15-2, ITAA 1997”, the car allowances that is received by Anna should be included in the

assessable income as statutory income because it was paid to Anna during the course of her

employment for rendering the services by working as the employee.

In the mid-June a compensation payment of $130,000 was paid to Anna from her

previous employer relating to the injuries suffered at work place. It should be noted that the

compensation that was paid to Anna was for the injuries suffered at the work place. The

12 Kenny, P. Australian tax. Chatswood, N.S.W.: (LexisNexis Butterworths 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

compensation payment which is received by Anna is associated to the loss of income earning

ability and sustaining injuries at workplace. Therefore, the amount is a capital receipt and not

an income. Since the amount is treated as capital in nature, the sum of $130,000 is not an

ordinary income under the meaning of “section 6-5, ITAA 1997”. In an alternative situation

if Anna decides to accept the lesser amount of $75,000 notwithstanding of any agreed basis,

the compensation amount will be considered as the capital payment because the amount was

received by Anna as the settlement of the workplace injury.

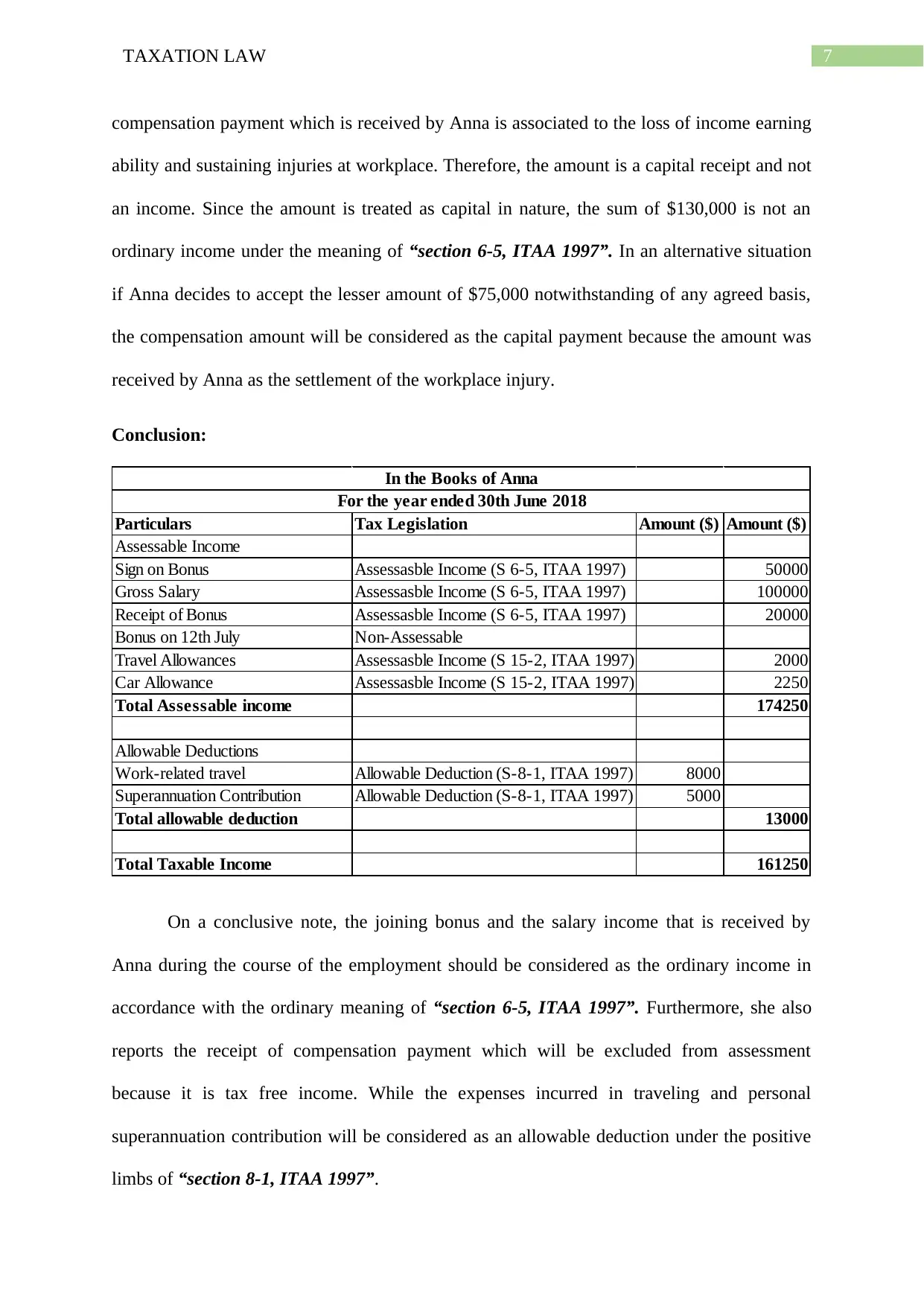

Conclusion:

Particulars Tax Legislation Amount ($) Amount ($)

Assessable Income

Sign on Bonus Assessasble Income (S 6-5, ITAA 1997) 50000

Gross Salary Assessasble Income (S 6-5, ITAA 1997) 100000

Receipt of Bonus Assessasble Income (S 6-5, ITAA 1997) 20000

Bonus on 12th July Non-Assessable

Travel Allowances Assessasble Income (S 15-2, ITAA 1997) 2000

Car Allowance Assessasble Income (S 15-2, ITAA 1997) 2250

Total Assessable income 174250

Allowable Deductions

Work-related travel Allowable Deduction (S-8-1, ITAA 1997) 8000

Superannuation Contribution Allowable Deduction (S-8-1, ITAA 1997) 5000

Total allowable deduction 13000

Total Taxable Income 161250

In the Books of Anna

For the year ended 30th June 2018

On a conclusive note, the joining bonus and the salary income that is received by

Anna during the course of the employment should be considered as the ordinary income in

accordance with the ordinary meaning of “section 6-5, ITAA 1997”. Furthermore, she also

reports the receipt of compensation payment which will be excluded from assessment

because it is tax free income. While the expenses incurred in traveling and personal

superannuation contribution will be considered as an allowable deduction under the positive

limbs of “section 8-1, ITAA 1997”.

compensation payment which is received by Anna is associated to the loss of income earning

ability and sustaining injuries at workplace. Therefore, the amount is a capital receipt and not

an income. Since the amount is treated as capital in nature, the sum of $130,000 is not an

ordinary income under the meaning of “section 6-5, ITAA 1997”. In an alternative situation

if Anna decides to accept the lesser amount of $75,000 notwithstanding of any agreed basis,

the compensation amount will be considered as the capital payment because the amount was

received by Anna as the settlement of the workplace injury.

Conclusion:

Particulars Tax Legislation Amount ($) Amount ($)

Assessable Income

Sign on Bonus Assessasble Income (S 6-5, ITAA 1997) 50000

Gross Salary Assessasble Income (S 6-5, ITAA 1997) 100000

Receipt of Bonus Assessasble Income (S 6-5, ITAA 1997) 20000

Bonus on 12th July Non-Assessable

Travel Allowances Assessasble Income (S 15-2, ITAA 1997) 2000

Car Allowance Assessasble Income (S 15-2, ITAA 1997) 2250

Total Assessable income 174250

Allowable Deductions

Work-related travel Allowable Deduction (S-8-1, ITAA 1997) 8000

Superannuation Contribution Allowable Deduction (S-8-1, ITAA 1997) 5000

Total allowable deduction 13000

Total Taxable Income 161250

In the Books of Anna

For the year ended 30th June 2018

On a conclusive note, the joining bonus and the salary income that is received by

Anna during the course of the employment should be considered as the ordinary income in

accordance with the ordinary meaning of “section 6-5, ITAA 1997”. Furthermore, she also

reports the receipt of compensation payment which will be excluded from assessment

because it is tax free income. While the expenses incurred in traveling and personal

superannuation contribution will be considered as an allowable deduction under the positive

limbs of “section 8-1, ITAA 1997”.

8TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Barkoczy, 2019 Core Tax Legislation and Study Guide, (22nd edition, Oxford University

Press 2019)

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Freudenberg, Brett, et al. "Tax literacy of Australian small businesses." J. Austl. Tax'n 19

(2017): 21.

Kenny, P. Australian tax. Chatswood, N.S.W.: (LexisNexis Butterworths 2013).

LJ Nethercott, G Richardson and K Devos, Australian Taxation Study Manual, Questions and

Suggested Solutions (28th edn, Oxford University Press, 2018)

Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J.

Australasian Tax Tchrs. Ass'n 13 (2018): 307.

Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law

Select 2019: Legislation And Commentary. Oxford University Press, 2019.

Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

Sadiq, Australian Taxation Law Cases (Thomson Reuters, 2019)

Woellner, Barkoczy, Murphy, Evans and Pinto, Australian Taxation Law (29th edn, Oxford

University Press 2019)

Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

References:

Barkoczy, 2019 Core Tax Legislation and Study Guide, (22nd edition, Oxford University

Press 2019)

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Freudenberg, Brett, et al. "Tax literacy of Australian small businesses." J. Austl. Tax'n 19

(2017): 21.

Kenny, P. Australian tax. Chatswood, N.S.W.: (LexisNexis Butterworths 2013).

LJ Nethercott, G Richardson and K Devos, Australian Taxation Study Manual, Questions and

Suggested Solutions (28th edn, Oxford University Press, 2018)

Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J.

Australasian Tax Tchrs. Ass'n 13 (2018): 307.

Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law

Select 2019: Legislation And Commentary. Oxford University Press, 2019.

Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

Sadiq, Australian Taxation Law Cases (Thomson Reuters, 2019)

Woellner, Barkoczy, Murphy, Evans and Pinto, Australian Taxation Law (29th edn, Oxford

University Press 2019)

Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.