HI6028 Taxation Law: Analyzing Income, CGT, and Tax Legislation

VerifiedAdded on 2023/03/31

|8

|2324

|235

Homework Assignment

AI Summary

This assignment solution delves into various aspects of Australian taxation law, focusing on capital gains tax (CGT) and income tax principles. It analyzes scenarios involving the sale of assets like antique paintings, sculptures, jewellery, and pictures, referencing relevant sections of the ITAA 1997 to determine tax implications. Furthermore, it examines the concept of income from personal exertion, applying case law to determine the taxability of income earned by an economist from writing and selling a book. Lastly, the solution explores the tax treatment of interest income derived from a loan provided by a parent to their child, referencing relevant sections of the ITAA 1997 and relevant case laws. This document is helpful for students who are looking for solved assignments. You can find more material on Desklib.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer 1:......................................................................................................................2

Answer 2:......................................................................................................................3

Answer 3:......................................................................................................................5

Conclusion:...................................................................................................................6

References:..................................................................................................................7

Table of Contents

Answer 1:......................................................................................................................2

Answer 2:......................................................................................................................3

Answer 3:......................................................................................................................5

Conclusion:...................................................................................................................6

References:..................................................................................................................7

2TAXATION LAW

Answer 1:

Tax charged on Capital Gain for antique impressionism painting:

As per “sec 100-25 (1), ITAA 1997”, tax imposed on capital gains is

restricted on assets on which it is applied. Moreover, according to the section, the

tax is limited on those products which are bought on the 20th September, 1985. The

real gains, which are made, are applied only up to 21st September 1999, for tax

regarding the regimes of capital gains tax (Afonso and Alves 2018). For this reason,

the cost base related to assets of the capital gains tax was indexed for inflation when

the CGT asset, which was hold for more than 12 months, was sold. However, assets

that were bought before 20th September of 1985 and gained after that are not

accountable for CGT as these are exempted assets.

In this context, Helen purchased antique painting on February 1985 which

was before 20th September, 1985. Hence, the purchase was done before the

implementation of the capital gain tax regimes. On the other side, this painting was

sold in December 2018. The purchasing price of this painting was $4000 while it was

sold for $12000. Therefore, the sale of painting had helped Helen to experience

capital gain. The asset is known as pre CGT assets as it was bought before the

introduction day and consequently the capital gains for Helen was exempted in this

context.

Capital Gain Tax related to historical sculpture:

The CGT provision is on the realised or actual gains. As per “sec 102-5 (1)”,

the capital gains for a taxpayer are taxable in the form of statutory income and this is

included in the assessable earnings as well. On the other side, “Sec 104-10, ITAA

1997” is related with the disposable of CGT asset. The event A1 regarding CGT

happens when the CGT related assets are sold (Jacob 2018). Some listed items

under “sec 108-10 (2), ITAA 1997” are antiques, rare books, sculptures and

jewellery, which are used for the purpose of personal enjoyment.

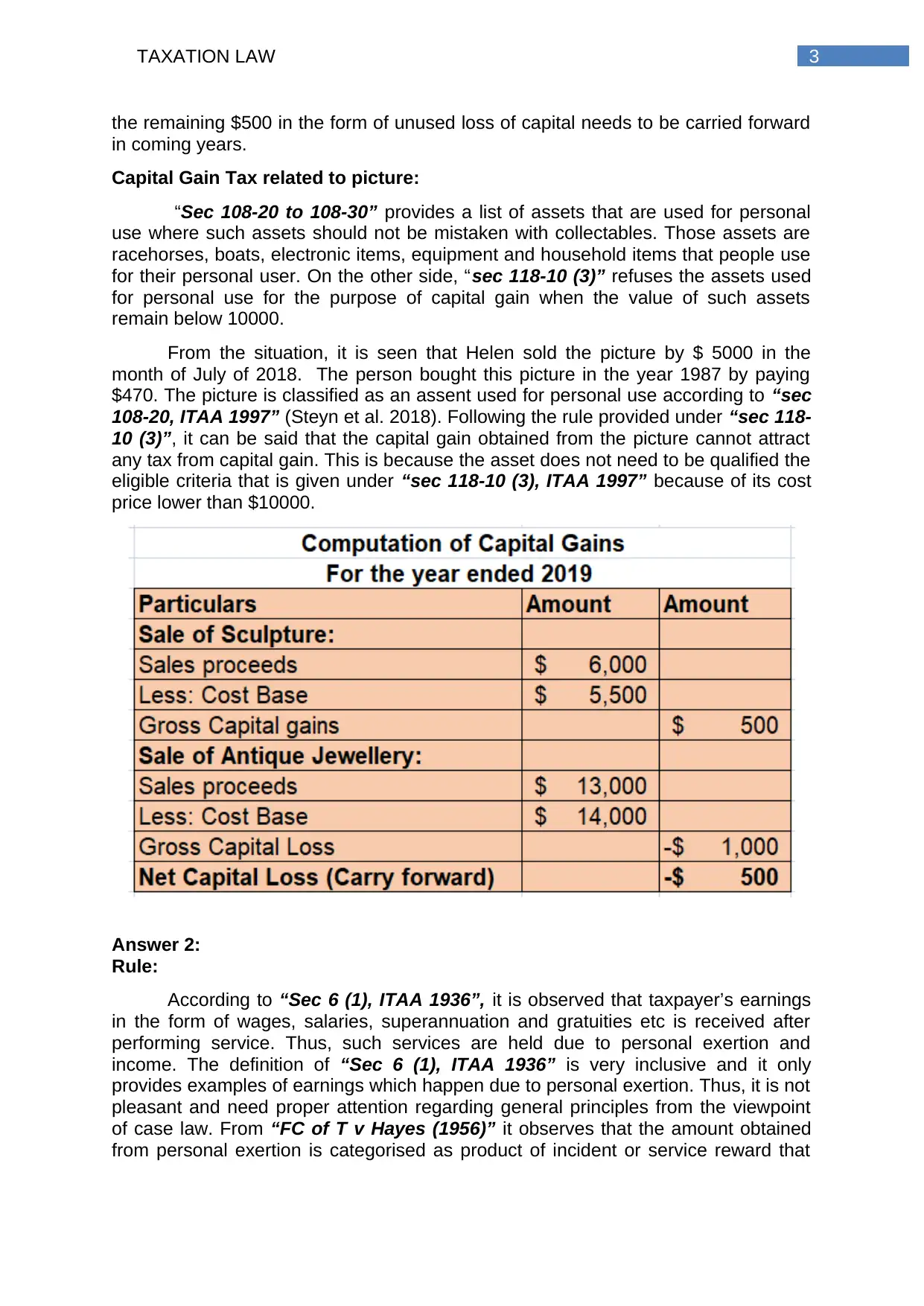

In 1993, a sculpture, which was an art work, was bought by $5500 by Helen,

who sold it again in 2018 for $6000. The sculpture is described as the collectable

item related to “sec 108-10 (2), ITAA 1997”. The selling process of the sculpture

has increased CGT event A1 based on “sec 104-10, ITAA 1997”. The capital gains,

which are made over here, are known as taxable in the form of statutory income

regarding “sec 6-10”. Depending on “sec 102-5 (1)”, this capital gains will be

considered as assessable income of Helen.

Tax on capital gain related to antique jewellery piece:

From “sec 108-10 (1), ITAA 1997”, it is seen that the capital loss happened

from any collectables are quarantined and this can e offset only against the capital

gains that happened from other collectables. This indictes that leftover amount from

capital loss can be carried forward for futures with the help of “sec 108-10 (4)”

(Bentley 2019). In this situation, Helen has purchased the jewellery by paying 14000

and sold it on 20 March 2018 by losing $1000 from the purchased price. By following

the quarantined rule under “sec 108-10 (1), ITAA 1997”, it is said that the capital

loss needs to be quarantined. Furthermore, such can be offset beside capital gain,

occurred from sculpture. Based on “sec 108-10 (4), ITAA 1997”, it is observed that

Answer 1:

Tax charged on Capital Gain for antique impressionism painting:

As per “sec 100-25 (1), ITAA 1997”, tax imposed on capital gains is

restricted on assets on which it is applied. Moreover, according to the section, the

tax is limited on those products which are bought on the 20th September, 1985. The

real gains, which are made, are applied only up to 21st September 1999, for tax

regarding the regimes of capital gains tax (Afonso and Alves 2018). For this reason,

the cost base related to assets of the capital gains tax was indexed for inflation when

the CGT asset, which was hold for more than 12 months, was sold. However, assets

that were bought before 20th September of 1985 and gained after that are not

accountable for CGT as these are exempted assets.

In this context, Helen purchased antique painting on February 1985 which

was before 20th September, 1985. Hence, the purchase was done before the

implementation of the capital gain tax regimes. On the other side, this painting was

sold in December 2018. The purchasing price of this painting was $4000 while it was

sold for $12000. Therefore, the sale of painting had helped Helen to experience

capital gain. The asset is known as pre CGT assets as it was bought before the

introduction day and consequently the capital gains for Helen was exempted in this

context.

Capital Gain Tax related to historical sculpture:

The CGT provision is on the realised or actual gains. As per “sec 102-5 (1)”,

the capital gains for a taxpayer are taxable in the form of statutory income and this is

included in the assessable earnings as well. On the other side, “Sec 104-10, ITAA

1997” is related with the disposable of CGT asset. The event A1 regarding CGT

happens when the CGT related assets are sold (Jacob 2018). Some listed items

under “sec 108-10 (2), ITAA 1997” are antiques, rare books, sculptures and

jewellery, which are used for the purpose of personal enjoyment.

In 1993, a sculpture, which was an art work, was bought by $5500 by Helen,

who sold it again in 2018 for $6000. The sculpture is described as the collectable

item related to “sec 108-10 (2), ITAA 1997”. The selling process of the sculpture

has increased CGT event A1 based on “sec 104-10, ITAA 1997”. The capital gains,

which are made over here, are known as taxable in the form of statutory income

regarding “sec 6-10”. Depending on “sec 102-5 (1)”, this capital gains will be

considered as assessable income of Helen.

Tax on capital gain related to antique jewellery piece:

From “sec 108-10 (1), ITAA 1997”, it is seen that the capital loss happened

from any collectables are quarantined and this can e offset only against the capital

gains that happened from other collectables. This indictes that leftover amount from

capital loss can be carried forward for futures with the help of “sec 108-10 (4)”

(Bentley 2019). In this situation, Helen has purchased the jewellery by paying 14000

and sold it on 20 March 2018 by losing $1000 from the purchased price. By following

the quarantined rule under “sec 108-10 (1), ITAA 1997”, it is said that the capital

loss needs to be quarantined. Furthermore, such can be offset beside capital gain,

occurred from sculpture. Based on “sec 108-10 (4), ITAA 1997”, it is observed that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

the remaining $500 in the form of unused loss of capital needs to be carried forward

in coming years.

Capital Gain Tax related to picture:

“Sec 108-20 to 108-30” provides a list of assets that are used for personal

use where such assets should not be mistaken with collectables. Those assets are

racehorses, boats, electronic items, equipment and household items that people use

for their personal user. On the other side, “sec 118-10 (3)” refuses the assets used

for personal use for the purpose of capital gain when the value of such assets

remain below 10000.

From the situation, it is seen that Helen sold the picture by $ 5000 in the

month of July of 2018. The person bought this picture in the year 1987 by paying

$470. The picture is classified as an assent used for personal use according to “sec

108-20, ITAA 1997” (Steyn et al. 2018). Following the rule provided under “sec 118-

10 (3)”, it can be said that the capital gain obtained from the picture cannot attract

any tax from capital gain. This is because the asset does not need to be qualified the

eligible criteria that is given under “sec 118-10 (3), ITAA 1997” because of its cost

price lower than $10000.

Answer 2:

Rule:

According to “Sec 6 (1), ITAA 1936”, it is observed that taxpayer’s earnings

in the form of wages, salaries, superannuation and gratuities etc is received after

performing service. Thus, such services are held due to personal exertion and

income. The definition of “Sec 6 (1), ITAA 1936” is very inclusive and it only

provides examples of earnings which happen due to personal exertion. Thus, it is not

pleasant and need proper attention regarding general principles from the viewpoint

of case law. From “FC of T v Hayes (1956)” it observes that the amount obtained

from personal exertion is categorised as product of incident or service reward that

the remaining $500 in the form of unused loss of capital needs to be carried forward

in coming years.

Capital Gain Tax related to picture:

“Sec 108-20 to 108-30” provides a list of assets that are used for personal

use where such assets should not be mistaken with collectables. Those assets are

racehorses, boats, electronic items, equipment and household items that people use

for their personal user. On the other side, “sec 118-10 (3)” refuses the assets used

for personal use for the purpose of capital gain when the value of such assets

remain below 10000.

From the situation, it is seen that Helen sold the picture by $ 5000 in the

month of July of 2018. The person bought this picture in the year 1987 by paying

$470. The picture is classified as an assent used for personal use according to “sec

108-20, ITAA 1997” (Steyn et al. 2018). Following the rule provided under “sec 118-

10 (3)”, it can be said that the capital gain obtained from the picture cannot attract

any tax from capital gain. This is because the asset does not need to be qualified the

eligible criteria that is given under “sec 118-10 (3), ITAA 1997” because of its cost

price lower than $10000.

Answer 2:

Rule:

According to “Sec 6 (1), ITAA 1936”, it is observed that taxpayer’s earnings

in the form of wages, salaries, superannuation and gratuities etc is received after

performing service. Thus, such services are held due to personal exertion and

income. The definition of “Sec 6 (1), ITAA 1936” is very inclusive and it only

provides examples of earnings which happen due to personal exertion. Thus, it is not

pleasant and need proper attention regarding general principles from the viewpoint

of case law. From “FC of T v Hayes (1956)” it observes that the amount obtained

from personal exertion is categorised as product of incident or service reward that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

are rendered (Redonda et al. 2019). Thus, a sufficient relationship among the

activities related to income generation and amount can be observed.

In general, it is observed that the maximum form of earnings that taxpayer

receives, come in the form of ordinary earnings. Hence, the judicial concept related

to ordinary income related to “sec 6-5, ITAA 1997” considers ordinary types of

income. To provide support to the income done for personal exertion under income

case laws like “Brent v FCT (1971)” is suggested. This happens for gaining taxable

earnings, when Helen provided money to newspaper for telling her story based on

her life to in some exclusive publication.

Another example related to “Hobbs v Hussey (1942)”, in which the infamous

criminal earned £1,500 after selling the autobiography to a publisher. The criminal

did it in order to make an exclusive publication based on his story in the form of an

article in a newspaper. The payment amount that the taxpayer made cannot cover

the inconvenience or the cost.

Similarly, other instance related to “Housden v Marshall (1958)”, states that

the taxpayer paid the taxable amount when he sold out the Jockey related

experience. This also included the newspaper cutting as well as photographs. The

received amount was taxable and ordinary income where the meaning of ordinary

came from “sec 6-5, ITAA 1997”.

Application:

Barbara, the economist and a research commentator, was received $13000

from the publisher of Eco Books Ltd for writing a book of economics. After accepting

this offer, she wrote a book, named “Principle of Economics”. The provision of

services of Barbara was worth $13000. In addition to this, the example related to

“Brent v FCT (1971)” stated that the payment have huge amount of services which

are left for the earning activity (Kennedy et al. 2017). The payment character, which

Barbara received is the income earned after personal exertion as stated in “sec 6(1),

ITAA 1997”. Hence, the amount is taxable as ordinary earnings related to the

concept of judicial of “sec 6-5, ITAA 1997”.

Later, Barbara assigned the copyright for her book to her publisher, the Eco

Books Ltd. To sell the copyright, Barbara received the amount $13400. This similar

case example is discussed in “Hobbs v Hussey (1942)”. Barbara sold the copyright

of her economic book to the publisher and this is a taxable ordinary income as noted

in “sec 6-5, ITAA 1997”. Barbara received the amount as she needed to be

provided the personal service for obtaining the payment (Bentley 2019). It is

observed that she needed to write this book before receiving the payment from the

Eco Books Ltd. The chief importance of this payment that Barbara received was not

to cover up the outgoing that taxpayer incurred. Rather, in this case, taxpayer

motivates Barbara to make the service and her payment was the product of her

work.

At the end, Barbara sold the manuscript of her book along with the

manuscripts of interview to the library. These activities helped her to earn money. As

referred in “Housden v Marshall (1958)”, selling manuscripts of interview and

books as well as the income receipt hence is considered as taxable ordinary income

that occur under “sec 6-5, ITAA 1997”.

are rendered (Redonda et al. 2019). Thus, a sufficient relationship among the

activities related to income generation and amount can be observed.

In general, it is observed that the maximum form of earnings that taxpayer

receives, come in the form of ordinary earnings. Hence, the judicial concept related

to ordinary income related to “sec 6-5, ITAA 1997” considers ordinary types of

income. To provide support to the income done for personal exertion under income

case laws like “Brent v FCT (1971)” is suggested. This happens for gaining taxable

earnings, when Helen provided money to newspaper for telling her story based on

her life to in some exclusive publication.

Another example related to “Hobbs v Hussey (1942)”, in which the infamous

criminal earned £1,500 after selling the autobiography to a publisher. The criminal

did it in order to make an exclusive publication based on his story in the form of an

article in a newspaper. The payment amount that the taxpayer made cannot cover

the inconvenience or the cost.

Similarly, other instance related to “Housden v Marshall (1958)”, states that

the taxpayer paid the taxable amount when he sold out the Jockey related

experience. This also included the newspaper cutting as well as photographs. The

received amount was taxable and ordinary income where the meaning of ordinary

came from “sec 6-5, ITAA 1997”.

Application:

Barbara, the economist and a research commentator, was received $13000

from the publisher of Eco Books Ltd for writing a book of economics. After accepting

this offer, she wrote a book, named “Principle of Economics”. The provision of

services of Barbara was worth $13000. In addition to this, the example related to

“Brent v FCT (1971)” stated that the payment have huge amount of services which

are left for the earning activity (Kennedy et al. 2017). The payment character, which

Barbara received is the income earned after personal exertion as stated in “sec 6(1),

ITAA 1997”. Hence, the amount is taxable as ordinary earnings related to the

concept of judicial of “sec 6-5, ITAA 1997”.

Later, Barbara assigned the copyright for her book to her publisher, the Eco

Books Ltd. To sell the copyright, Barbara received the amount $13400. This similar

case example is discussed in “Hobbs v Hussey (1942)”. Barbara sold the copyright

of her economic book to the publisher and this is a taxable ordinary income as noted

in “sec 6-5, ITAA 1997”. Barbara received the amount as she needed to be

provided the personal service for obtaining the payment (Bentley 2019). It is

observed that she needed to write this book before receiving the payment from the

Eco Books Ltd. The chief importance of this payment that Barbara received was not

to cover up the outgoing that taxpayer incurred. Rather, in this case, taxpayer

motivates Barbara to make the service and her payment was the product of her

work.

At the end, Barbara sold the manuscript of her book along with the

manuscripts of interview to the library. These activities helped her to earn money. As

referred in “Housden v Marshall (1958)”, selling manuscripts of interview and

books as well as the income receipt hence is considered as taxable ordinary income

that occur under “sec 6-5, ITAA 1997”.

5TAXATION LAW

On the other side, if Barbara wrote the book simply during her leisure time

and after that she sold those to the book publisher for further publication then the

amount derived from her work would be known as income (Chardon, Freudenberg

and Brimble 2016). Such income coming from the exertion of personal service would

be taxable under the “sec 6-5, ITAA 1997”.

Thus, the amount of money received by Barbara is relayed exclusively with

her personal exertion. Under the judicial concept of “sec 6-5, ITAA 1997”, the

amount will be referred as taxable in the form of ordinary earnings.

Answer 3:

Rule:

The taxable income considers both the ordinary income as well the statutory

income. Thus, ordinary income is known as income which the courts generally

ascertain by implementing the income definition. Such definition of income depends

on the ordinary concept of “Sec 6-5 (1)” and measures the tax related ordinary

income. The taxable income related to the taxpayer includes the income related with

the concept of ordinary earnings. In order to characterise such income, it is essential

to consider the required characteristics related to it (Castro 2018). This considers

whether the earned receipt can be convertible easily into case. Featuring the

receipts as income generally involves the ascertainment. This implies whether the

receipts hold recurrence, periodicity and regularity. The receipts obtaining from the

activities related to income generation are normally known as ordinary earnings.

In this context, it is essential to mention that ordinary earnings mainly have

two prerequisites. This considers whether the receipts can be converted into cash

and a receiver’s real gain or not. As per “Hochstrasser v Mayes (1960)”, the court

law has explained that the ordinary income will not occur until the receipt are

considered as the genuine gain (Steyn et al. 2018). The gains will be described as

ordinary income if the prerequisites related to the ordinary income will be satisfied. In

this situation, the gains will be known as the ordinary income that will consider the

sufficient characteristics related to income. Most importantly, the one-off receives are

not considered as the ordinary income. Likewise, the lump sum gains can be

considered as the ordinary income if the interest related to one-ff receipt under the

loan agreement will be held as ordinary income.

Applications:

Hence, rules, which are analysed in the above discussion, can be applied in

the context of Patrick and David. Patrick provided a loan to his son, David for five

years. However, Patrick also paid the loan where the amount of interest was $6000.

David paid the amount of loan by with the help of cheque. Furthermore, on the total

amount of borrowing, he also paid 5% in the form of the interest.

In this context, the interest amount earned by Patrick can be considered as

the real gain of the taxpayer and consequently it is denoted as income. The interest

receipt covers up the prerequisite as it can be converted easily into cash and this is

also a real gain (Torgler 2016). As mentioned in “Hochstrasser v Mayes (1960)”,

the one-off receipt related to interest obtained from the loan agreement is considered

as the real gain which is considered as an ordinary income as mentioned in “sec 6-

5, ITAA 1997”.

On the other side, if Barbara wrote the book simply during her leisure time

and after that she sold those to the book publisher for further publication then the

amount derived from her work would be known as income (Chardon, Freudenberg

and Brimble 2016). Such income coming from the exertion of personal service would

be taxable under the “sec 6-5, ITAA 1997”.

Thus, the amount of money received by Barbara is relayed exclusively with

her personal exertion. Under the judicial concept of “sec 6-5, ITAA 1997”, the

amount will be referred as taxable in the form of ordinary earnings.

Answer 3:

Rule:

The taxable income considers both the ordinary income as well the statutory

income. Thus, ordinary income is known as income which the courts generally

ascertain by implementing the income definition. Such definition of income depends

on the ordinary concept of “Sec 6-5 (1)” and measures the tax related ordinary

income. The taxable income related to the taxpayer includes the income related with

the concept of ordinary earnings. In order to characterise such income, it is essential

to consider the required characteristics related to it (Castro 2018). This considers

whether the earned receipt can be convertible easily into case. Featuring the

receipts as income generally involves the ascertainment. This implies whether the

receipts hold recurrence, periodicity and regularity. The receipts obtaining from the

activities related to income generation are normally known as ordinary earnings.

In this context, it is essential to mention that ordinary earnings mainly have

two prerequisites. This considers whether the receipts can be converted into cash

and a receiver’s real gain or not. As per “Hochstrasser v Mayes (1960)”, the court

law has explained that the ordinary income will not occur until the receipt are

considered as the genuine gain (Steyn et al. 2018). The gains will be described as

ordinary income if the prerequisites related to the ordinary income will be satisfied. In

this situation, the gains will be known as the ordinary income that will consider the

sufficient characteristics related to income. Most importantly, the one-off receives are

not considered as the ordinary income. Likewise, the lump sum gains can be

considered as the ordinary income if the interest related to one-ff receipt under the

loan agreement will be held as ordinary income.

Applications:

Hence, rules, which are analysed in the above discussion, can be applied in

the context of Patrick and David. Patrick provided a loan to his son, David for five

years. However, Patrick also paid the loan where the amount of interest was $6000.

David paid the amount of loan by with the help of cheque. Furthermore, on the total

amount of borrowing, he also paid 5% in the form of the interest.

In this context, the interest amount earned by Patrick can be considered as

the real gain of the taxpayer and consequently it is denoted as income. The interest

receipt covers up the prerequisite as it can be converted easily into cash and this is

also a real gain (Torgler 2016). As mentioned in “Hochstrasser v Mayes (1960)”,

the one-off receipt related to interest obtained from the loan agreement is considered

as the real gain which is considered as an ordinary income as mentioned in “sec 6-

5, ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

At the end, to measure the tax liability related to the interest, the payment

mode, which the son utilises, cannot influence the tax position.

Conclusion:

In this section, it can be concluded that the interest related to loan, which the

father has provided will be referred as the taxable income obtained from “sec 6-5,

ITAA 1997”. This is because for a taxpayer it is a real gain.

At the end, to measure the tax liability related to the interest, the payment

mode, which the son utilises, cannot influence the tax position.

Conclusion:

In this section, it can be concluded that the interest related to loan, which the

father has provided will be referred as the taxable income obtained from “sec 6-5,

ITAA 1997”. This is because for a taxpayer it is a real gain.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

References:

Afonso, A. and Alves, J., 2018. Optimal tax structure for consumption and income

inequality: an empirical assessment. REM Working Paper, pp.051-2018.

Bentley, D., 2019. Does A Capital Gains Tax Work? The Australian Experience

Eleven Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Bentley, D., 2019. Does A Capital Gains Tax Work? The Australian Experience

Eleven Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Castro, J.A., 2018. US Tax Treatment of Australian Superannuation. In Nevada Law

Journal Forum (Vol. 2, No. 1, p. 6).

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not

knowing your deduction from your offset. Austl. Tax F., 31, p.321.

Jacob, M., 2018. Tax regimes and capital gains realizations. European Accounting

Review, 27(1), pp.1-21.

Kennedy, T., Smyth, R., Valadkhani, A. and Chen, G., 2017. Does income inequality

hinder economic growth? New evidence using Australian taxation

statistics. Economic Modelling, 65, pp.119-128.

Redonda, A., de Sarralde, S.D., Hallerberg, M., Johnson, L., Melamud, A.,

Rozemberg, R., Schwab, J. and von Haldenwang, C., 2019. Tax expenditure and the

treatment of tax incentives for investment. Economics: The Open-Access, Open-

Assessment E-Journal, 13(2019-12), pp.1-11.

Steyn, T., Smulders, S., Stark, K. and Penning, I., 2018. Capital gains tax research:

an initial synthesis of the literature. eJTR, 16, p.278.

Steyn, T., Smulders, S., Stark, K. and Penning, I., 2018. Capital gains tax research:

an initial synthesis of the literature. eJTR, 16, p.278.

Torgler, B., 2016. Tax compliance and data: What is available and what is

needed. Australian Economic Review, 49(3), pp.352-364.

References:

Afonso, A. and Alves, J., 2018. Optimal tax structure for consumption and income

inequality: an empirical assessment. REM Working Paper, pp.051-2018.

Bentley, D., 2019. Does A Capital Gains Tax Work? The Australian Experience

Eleven Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Bentley, D., 2019. Does A Capital Gains Tax Work? The Australian Experience

Eleven Years On. Journal of Malaysian and Comparative Law, 23, pp.13-36.

Castro, J.A., 2018. US Tax Treatment of Australian Superannuation. In Nevada Law

Journal Forum (Vol. 2, No. 1, p. 6).

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not

knowing your deduction from your offset. Austl. Tax F., 31, p.321.

Jacob, M., 2018. Tax regimes and capital gains realizations. European Accounting

Review, 27(1), pp.1-21.

Kennedy, T., Smyth, R., Valadkhani, A. and Chen, G., 2017. Does income inequality

hinder economic growth? New evidence using Australian taxation

statistics. Economic Modelling, 65, pp.119-128.

Redonda, A., de Sarralde, S.D., Hallerberg, M., Johnson, L., Melamud, A.,

Rozemberg, R., Schwab, J. and von Haldenwang, C., 2019. Tax expenditure and the

treatment of tax incentives for investment. Economics: The Open-Access, Open-

Assessment E-Journal, 13(2019-12), pp.1-11.

Steyn, T., Smulders, S., Stark, K. and Penning, I., 2018. Capital gains tax research:

an initial synthesis of the literature. eJTR, 16, p.278.

Steyn, T., Smulders, S., Stark, K. and Penning, I., 2018. Capital gains tax research:

an initial synthesis of the literature. eJTR, 16, p.278.

Torgler, B., 2016. Tax compliance and data: What is available and what is

needed. Australian Economic Review, 49(3), pp.352-364.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.