Macquarie University ACCG924 Taxation Law Case Study Report

VerifiedAdded on 2022/12/20

|8

|1906

|31

Report

AI Summary

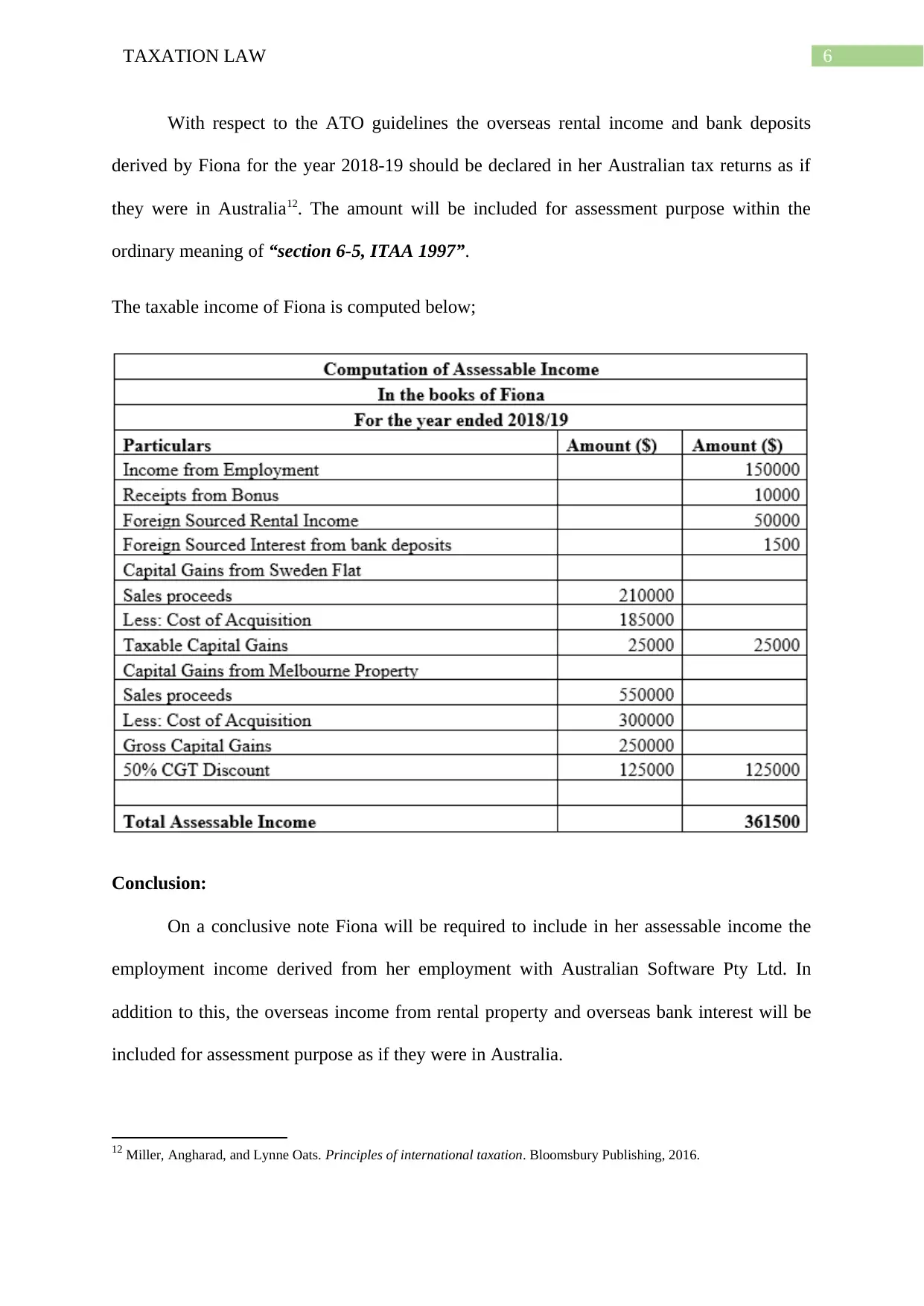

This report provides a comprehensive analysis of a taxation law case study, addressing various tax-related issues faced by an individual named Fiona. The report explores the concepts of assessable income, including income from employment, bonuses, and overseas income, referencing relevant legislation such as ITAA 1936 and ITAA 1997. It also examines capital gains tax (CGT) implications related to the sale of shares and property, considering pre-CGT assets and the CGT discount method. The analysis incorporates relevant case law, such as Scott v CT, Dean & Anor v CFT, and FCT v Payne, to support the conclusions. The report considers the tax treatment of different income sources and events, providing a detailed application of tax principles to Fiona's specific circumstances, including her employment, overseas investments, and capital gains. The report concludes with a summary of Fiona's assessable income and the tax implications of her various financial activities. The report also contains references to the sources used.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.