LAW 6001: Taxation Law Case Study - Client Advice and Analysis

VerifiedAdded on 2023/03/17

|12

|3033

|55

Case Study

AI Summary

This case study, prepared for LAW 6001 Taxation Law, delves into various aspects of Australian taxation law, including the constitutional basis of taxation, double taxation agreements, capital gains tax (CGT), and tax deductions. It analyzes specific scenarios involving property subdivision, business cessation, and asset sales, providing detailed explanations of relevant legislation such as the Income Tax Assessment Act (ITAA) 1936 and 1997. The study further examines tax avoidance by multinational companies and the implications of franking credits. The assignment provides answers to specific questions related to tax law, including the treatment of capital gains, and the deductibility of expenses. It also incorporates analysis of relevant articles on multinational tax avoidance and franking credits, and offers a comprehensive overview of the application of tax laws in different contexts. The case study concludes with a detailed examination of the tax implications and provides recommendations based on the facts and analysis provided.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................3

Part 1:.....................................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................4

Answer to Part 2:....................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................6

Answer to question 6:.................................................................................................................7

Article 1: ATO Closing gap on multinational Tax Avoidance:.............................................7

Concise explanation of tax concepts:.....................................................................................8

Article 2: Removal of franking credit inequitable: Inquiry...................................................8

Answer to question 7:.................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................3

Part 1:.....................................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................4

Answer to Part 2:....................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................6

Answer to question 6:.................................................................................................................7

Article 1: ATO Closing gap on multinational Tax Avoidance:.............................................7

Concise explanation of tax concepts:.....................................................................................8

Article 2: Removal of franking credit inequitable: Inquiry...................................................8

Answer to question 7:.................................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Answer to A:

The constitutional basis of imposing tax in Australia is mainly found under the

“section 51 (ii)”, “section 90”, “section 53” and “section 96” of the Australian constitution.

The interpretation of the high court of Australia has been integral in the functioning as well

federalist in Australia (McCluskey & Franzsen, 2017). According to the “section 51 (ii)”, of

the Australian constitution, the power to impose tax is given under this section. The areas of

commonwealth power are given under the “section 51”. “Section 51 (ii)” permits the

commonwealth to impose law in relation to the taxation but not to discriminate among the

states and part of the states. The section 90, provides the commonwealth with the power of

imposing tax on the custom duties and excise.

Answer to B:

The development of government tax policy and its application is the responsibility of

the Treasury Ministers. An important role is played by the ATO to formulate the policy and

legislative process that portrays inter-dependence among the laws, policy and governmental

features of taxation system (Evans et al., 2017). The ATO is primarily responsible for the

managing the tax and superannuation laws which the parliament passes. To carry out this, the

administrative arrangements is developed by the ATO which is applied on the tax laws,

education and advising the taxpayers involving their duties and responsibilities.

The high court on the other hand is accountable for interpreting and applying tax in

Australia to make decision on cases that has special significances to the federal along with

the challenges of constitutional validity and hearing the appeals from state, federal and

territory courts (Woellner et al., 2016). The parliament usually is made up of upper and lower

houses. Bills must be passed from upper and lower house to be considered as law. Bills

Answer to question 1:

Answer to A:

The constitutional basis of imposing tax in Australia is mainly found under the

“section 51 (ii)”, “section 90”, “section 53” and “section 96” of the Australian constitution.

The interpretation of the high court of Australia has been integral in the functioning as well

federalist in Australia (McCluskey & Franzsen, 2017). According to the “section 51 (ii)”, of

the Australian constitution, the power to impose tax is given under this section. The areas of

commonwealth power are given under the “section 51”. “Section 51 (ii)” permits the

commonwealth to impose law in relation to the taxation but not to discriminate among the

states and part of the states. The section 90, provides the commonwealth with the power of

imposing tax on the custom duties and excise.

Answer to B:

The development of government tax policy and its application is the responsibility of

the Treasury Ministers. An important role is played by the ATO to formulate the policy and

legislative process that portrays inter-dependence among the laws, policy and governmental

features of taxation system (Evans et al., 2017). The ATO is primarily responsible for the

managing the tax and superannuation laws which the parliament passes. To carry out this, the

administrative arrangements is developed by the ATO which is applied on the tax laws,

education and advising the taxpayers involving their duties and responsibilities.

The high court on the other hand is accountable for interpreting and applying tax in

Australia to make decision on cases that has special significances to the federal along with

the challenges of constitutional validity and hearing the appeals from state, federal and

territory courts (Woellner et al., 2016). The parliament usually is made up of upper and lower

houses. Bills must be passed from upper and lower house to be considered as law. Bills

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

relating to tax is forwarded by lower house to parliament and it is passed by upper house to

be considered as bill.

Answer to question 2:

Australia has the double taxation agreement with USA. The agreement explains that

profits made by the business of one contracting states will be considered taxable only under

that situation except when the company is carrying on the business in the other contracting

company with the help of permanent establishment located in that state (Duncan et al., 2018).

If the company under the double taxation agreement is performing the business as explained

above, then the business profits of the enterprise might be levied tax in the other state but

only to that extent that is attributable to that permanent establishment.

A company is treated as the resident of Australia if the company is performing its

business activities in Australia under the Australian controlled central management.

Generally, revenue derived by the business is held taxable where the source is located.

Accordingly, in “C of T (NSW) v Hillsdon Watts Ltd (1937)” business income is generally

held taxable where the business carries out its activities (Chardon, 2014). It is regarded as the

place where the contract is generally carried out and the only relevant factor in determining

sources. Taking into the account the double taxation agreement it can be stated that the profits

that are made by US company from selling its products in Australia will be considered

taxable in Australia because the sales will be sourced in Australia.

Answer to question 3:

Part 1:

Answer to A:

Assets purchased after 20th September 1985 is regarded for capital gains tax purpose.

While assets bought before this date is considered pre-CGT asset (Ingles, 2015). If Indiana

relating to tax is forwarded by lower house to parliament and it is passed by upper house to

be considered as bill.

Answer to question 2:

Australia has the double taxation agreement with USA. The agreement explains that

profits made by the business of one contracting states will be considered taxable only under

that situation except when the company is carrying on the business in the other contracting

company with the help of permanent establishment located in that state (Duncan et al., 2018).

If the company under the double taxation agreement is performing the business as explained

above, then the business profits of the enterprise might be levied tax in the other state but

only to that extent that is attributable to that permanent establishment.

A company is treated as the resident of Australia if the company is performing its

business activities in Australia under the Australian controlled central management.

Generally, revenue derived by the business is held taxable where the source is located.

Accordingly, in “C of T (NSW) v Hillsdon Watts Ltd (1937)” business income is generally

held taxable where the business carries out its activities (Chardon, 2014). It is regarded as the

place where the contract is generally carried out and the only relevant factor in determining

sources. Taking into the account the double taxation agreement it can be stated that the profits

that are made by US company from selling its products in Australia will be considered

taxable in Australia because the sales will be sourced in Australia.

Answer to question 3:

Part 1:

Answer to A:

Assets purchased after 20th September 1985 is regarded for capital gains tax purpose.

While assets bought before this date is considered pre-CGT asset (Ingles, 2015). If Indiana

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

considers subdividing the land to 80 units and dispose it then any capital gains will be

exempted because it is pre-CGT asset.

Answer to B:

Option 1:

If the property is purchased by Indiana on 1st November 1986 and then sells the

subdivided undeveloped block to the property developer, then the revenue provision must be

applied (Iskhakov et al., 2015). The land will not be treated as trading stock and the profits

will not be taxable under “section 6-5, ITAA 1997”.

Option 2:

In the second option if Indiana holds an auction of 80 block of land and sells it to the

highest bidder then those subdivided 80 blocks will be treated as trading stock for Indiana.

The profits made thereon by selling the 80 lots is a taxable as ordinary income under “section

6-5, ITAA 1997” (Cao et al., 2015).

Option 3:

If Indiana decides that she will not proceed forward with the subdivision of land and

directly sell the land to the property developer. Any gains derived will be considered taxable

as capital gains (Carling, 2015). The profits will be considered taxable as ordinary income

and will be subjected to GST.

Answer to Part 2:

Option A:

If the subdivision of land goes beyond mere realisation of capital asset, then it would

amount to carrying the business of land development by Indiana. The disposal of subdivided

considers subdividing the land to 80 units and dispose it then any capital gains will be

exempted because it is pre-CGT asset.

Answer to B:

Option 1:

If the property is purchased by Indiana on 1st November 1986 and then sells the

subdivided undeveloped block to the property developer, then the revenue provision must be

applied (Iskhakov et al., 2015). The land will not be treated as trading stock and the profits

will not be taxable under “section 6-5, ITAA 1997”.

Option 2:

In the second option if Indiana holds an auction of 80 block of land and sells it to the

highest bidder then those subdivided 80 blocks will be treated as trading stock for Indiana.

The profits made thereon by selling the 80 lots is a taxable as ordinary income under “section

6-5, ITAA 1997” (Cao et al., 2015).

Option 3:

If Indiana decides that she will not proceed forward with the subdivision of land and

directly sell the land to the property developer. Any gains derived will be considered taxable

as capital gains (Carling, 2015). The profits will be considered taxable as ordinary income

and will be subjected to GST.

Answer to Part 2:

Option A:

If the subdivision of land goes beyond mere realisation of capital asset, then it would

amount to carrying the business of land development by Indiana. The disposal of subdivided

5TAXATION LAW

80 blocks of land is a revenue asset and the gains made thereon is taxable within the ordinary

concepts of “section 6-5, ITAA 1997”.

Option B:

If Indiana decides to do auction of subdivided 80 blocks of land, the she will be

assessed on the 80 lots as trading stock of business. She will be considered taxable for

adopting commercial approach and the capital gains will be taxable as ordinary income under

“section 6-5, ITAA 1997”.

Option C:

If no subdivision of land is done by Indiana and directly the property is sold to

development company, then the profits is taxable as ordinary income.

Answer to question 4:

Expenses occurred following the cessation of the business may be considered as tax

deductible expenses if the event of loss or outgoing is in the due course of business that is

carried on previously by the taxpayer with the purpose obtaining taxable income. The federal

commissioner in “FCT v Placer Pacific Management Pty Ltd (1995)” permitted the

taxpayer to obtain deduction from the outgoings that were occurred in settling the dispute for

supplying the faulty conveyor belt (Campbell, 2018). The respondent here incurred the

expenses for producing the assessable income from business activities. According to the

commissioner the instances of loss and expenditure should be viewed as business

arrangement which incurred was among the taxpayer and customers.

The court of law in “FCT v Brown (1999)” also held that the taxation commissioner

was permitted to claim deduction for the interest on loan which the taxpayer entered during

the course of partnership business for producing the taxable income (Datt & Keating, 2018).

80 blocks of land is a revenue asset and the gains made thereon is taxable within the ordinary

concepts of “section 6-5, ITAA 1997”.

Option B:

If Indiana decides to do auction of subdivided 80 blocks of land, the she will be

assessed on the 80 lots as trading stock of business. She will be considered taxable for

adopting commercial approach and the capital gains will be taxable as ordinary income under

“section 6-5, ITAA 1997”.

Option C:

If no subdivision of land is done by Indiana and directly the property is sold to

development company, then the profits is taxable as ordinary income.

Answer to question 4:

Expenses occurred following the cessation of the business may be considered as tax

deductible expenses if the event of loss or outgoing is in the due course of business that is

carried on previously by the taxpayer with the purpose obtaining taxable income. The federal

commissioner in “FCT v Placer Pacific Management Pty Ltd (1995)” permitted the

taxpayer to obtain deduction from the outgoings that were occurred in settling the dispute for

supplying the faulty conveyor belt (Campbell, 2018). The respondent here incurred the

expenses for producing the assessable income from business activities. According to the

commissioner the instances of loss and expenditure should be viewed as business

arrangement which incurred was among the taxpayer and customers.

The court of law in “FCT v Brown (1999)” also held that the taxation commissioner

was permitted to claim deduction for the interest on loan which the taxpayer entered during

the course of partnership business for producing the taxable income (Datt & Keating, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Evidently, Amity here occurred interest on loan following the cessation of business activities.

Therefore, the interest on loan was occurred by Amity for performing the business activity

and producing taxable income. As a result, the interest on loan will be considered as

allowable deduction under the section “section 8-1, ITAA 1997”.

Answer to question 5:

The capital gains tax regimes explain that the CGT event only arises when the asset

that is bought on or after the 20th September 1985. Under the “section 104-10 (1)) of the

ITAA 1997” a CGT event A1 happens when the asset is sold by the taxpayer. The main

residence of the taxpayer is generally considered as exempted from the capital gains tax

(White et al., 2019). However, a taxpayer is only allowed to claim exemption when the

property is wholly used by them for dwelling purpose and it is not used for producing

income. Here, Maurice purchased the house that costs $140,000 and eventually sold it on 1st

March 325,000. Maurice on no occasion used the house for generating income and as a result

the house will be considered as exempted asset for CGT purpose.

During the year 1984 also purchased the FUL shares at a cost of $15,000. However,

on 15th March 2018 Maurice sold the shares for $19,000 and makes a capital gain. Notably,

the capital gains from the FUL shares is exempted from the CGT because it is pre-CGT asset.

Furthermore, the personal use assets under the “section 108-20 (2), ITAA 1997” implies that

the asset which is kept by the taxpayers mainly for their own enjoyment and use (Duncan et

al., 2018). Conversely, “section 118-10 (3), ITAA 1997” requires the taxpayers to ignore

capital gains that are purchased for less than a cost of $10,000. Maurice later purchased

furniture for a cost of $9,500 and eventually sold it for $15,000 on 1st May for a cost of

$5,000. Consequently, the capital loss obtained from the sale of furniture must be ignored by

Maurice since the furniture cost base is less than $10,000.

Evidently, Amity here occurred interest on loan following the cessation of business activities.

Therefore, the interest on loan was occurred by Amity for performing the business activity

and producing taxable income. As a result, the interest on loan will be considered as

allowable deduction under the section “section 8-1, ITAA 1997”.

Answer to question 5:

The capital gains tax regimes explain that the CGT event only arises when the asset

that is bought on or after the 20th September 1985. Under the “section 104-10 (1)) of the

ITAA 1997” a CGT event A1 happens when the asset is sold by the taxpayer. The main

residence of the taxpayer is generally considered as exempted from the capital gains tax

(White et al., 2019). However, a taxpayer is only allowed to claim exemption when the

property is wholly used by them for dwelling purpose and it is not used for producing

income. Here, Maurice purchased the house that costs $140,000 and eventually sold it on 1st

March 325,000. Maurice on no occasion used the house for generating income and as a result

the house will be considered as exempted asset for CGT purpose.

During the year 1984 also purchased the FUL shares at a cost of $15,000. However,

on 15th March 2018 Maurice sold the shares for $19,000 and makes a capital gain. Notably,

the capital gains from the FUL shares is exempted from the CGT because it is pre-CGT asset.

Furthermore, the personal use assets under the “section 108-20 (2), ITAA 1997” implies that

the asset which is kept by the taxpayers mainly for their own enjoyment and use (Duncan et

al., 2018). Conversely, “section 118-10 (3), ITAA 1997” requires the taxpayers to ignore

capital gains that are purchased for less than a cost of $10,000. Maurice later purchased

furniture for a cost of $9,500 and eventually sold it for $15,000 on 1st May for a cost of

$5,000. Consequently, the capital loss obtained from the sale of furniture must be ignored by

Maurice since the furniture cost base is less than $10,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

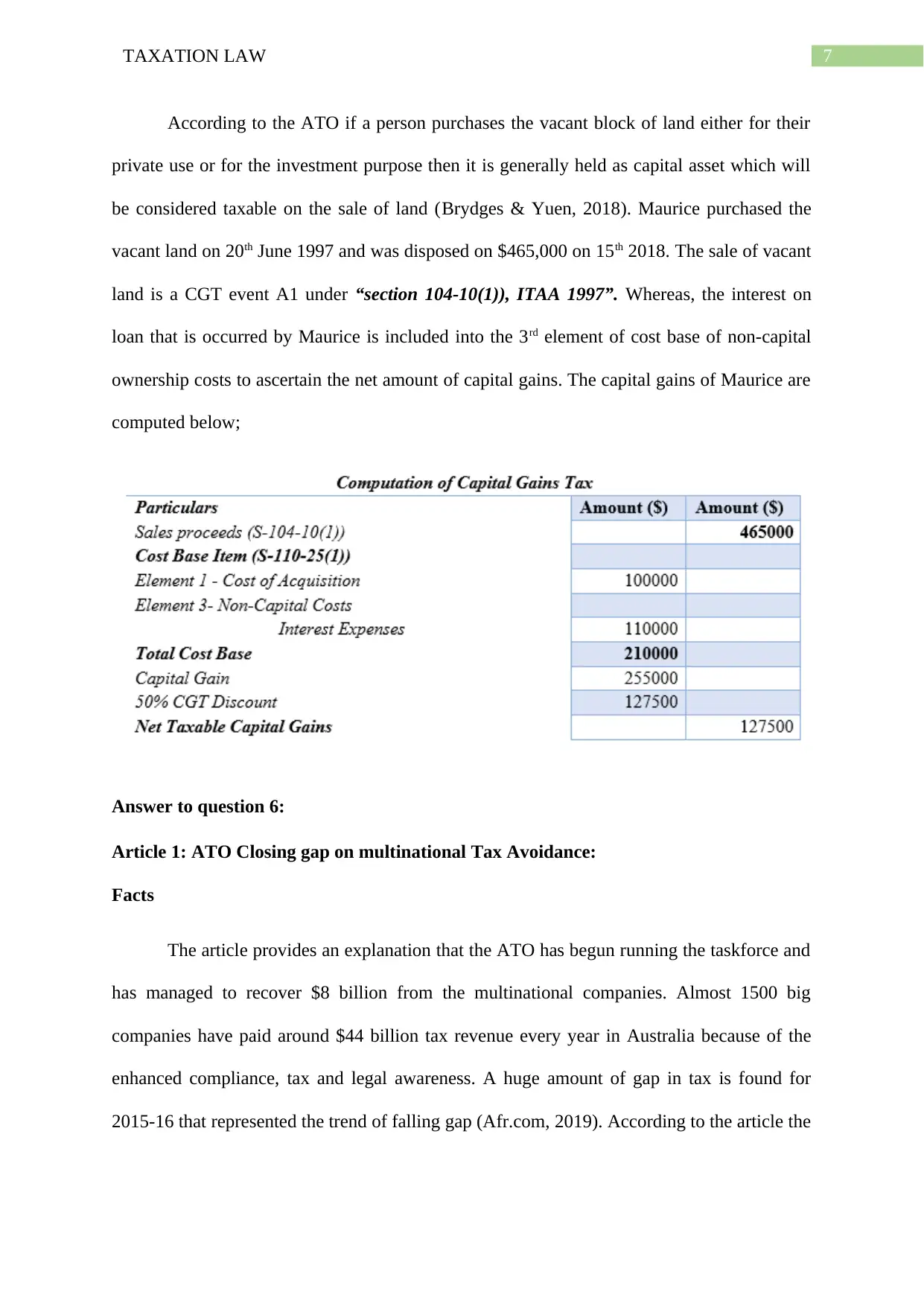

According to the ATO if a person purchases the vacant block of land either for their

private use or for the investment purpose then it is generally held as capital asset which will

be considered taxable on the sale of land (Brydges & Yuen, 2018). Maurice purchased the

vacant land on 20th June 1997 and was disposed on $465,000 on 15th 2018. The sale of vacant

land is a CGT event A1 under “section 104-10(1)), ITAA 1997”. Whereas, the interest on

loan that is occurred by Maurice is included into the 3rd element of cost base of non-capital

ownership costs to ascertain the net amount of capital gains. The capital gains of Maurice are

computed below;

Answer to question 6:

Article 1: ATO Closing gap on multinational Tax Avoidance:

Facts

The article provides an explanation that the ATO has begun running the taskforce and

has managed to recover $8 billion from the multinational companies. Almost 1500 big

companies have paid around $44 billion tax revenue every year in Australia because of the

enhanced compliance, tax and legal awareness. A huge amount of gap in tax is found for

2015-16 that represented the trend of falling gap (Afr.com, 2019). According to the article the

According to the ATO if a person purchases the vacant block of land either for their

private use or for the investment purpose then it is generally held as capital asset which will

be considered taxable on the sale of land (Brydges & Yuen, 2018). Maurice purchased the

vacant land on 20th June 1997 and was disposed on $465,000 on 15th 2018. The sale of vacant

land is a CGT event A1 under “section 104-10(1)), ITAA 1997”. Whereas, the interest on

loan that is occurred by Maurice is included into the 3rd element of cost base of non-capital

ownership costs to ascertain the net amount of capital gains. The capital gains of Maurice are

computed below;

Answer to question 6:

Article 1: ATO Closing gap on multinational Tax Avoidance:

Facts

The article provides an explanation that the ATO has begun running the taskforce and

has managed to recover $8 billion from the multinational companies. Almost 1500 big

companies have paid around $44 billion tax revenue every year in Australia because of the

enhanced compliance, tax and legal awareness. A huge amount of gap in tax is found for

2015-16 that represented the trend of falling gap (Afr.com, 2019). According to the article the

8TAXATION LAW

compliance among the multinational companies have been met and there is a rise of around

95% in tax performance.

Concise explanation of tax concepts:

The article provides the explanation that the tax avoidance is regarded as the lawful

concept which uses the tax regimes in the single territory in the advantage of multinationals

to reduce their amount of tax that is payable inside the law.

Explanation of connection between concepts and indicators of good tax policy:

The article provides the explanation the ATO has projected that the taskforce will

continue to work in the direct of good tax policy by emphasising on the tax impact of the

entire system (Afr.com, 2019). It reflects that there is an enhancement in the tax gap more

generally.

Article 2: Removal of franking credit inequitable: Inquiry

Facts:

This article is associated with the proposal of labor regarding the removal of franking

credit for both the super funds and individuals. However, removing the franking credits is

considered highly flawed following parliamentary inquiry. The committee has considered

that abolition of the franking credits for both the individuals and the SMSF policy is highly

unequal.

Concise explanation of taxation concepts:

As per the article the imputation credits would enable the Australian firms to pass the

tax at the company level and finally to the shareholders. The parliamentary budget projects

that policy would cost budget around $5.2 billion in 2020-21 and may increase to $48.6

billion by 2027-28.

compliance among the multinational companies have been met and there is a rise of around

95% in tax performance.

Concise explanation of tax concepts:

The article provides the explanation that the tax avoidance is regarded as the lawful

concept which uses the tax regimes in the single territory in the advantage of multinationals

to reduce their amount of tax that is payable inside the law.

Explanation of connection between concepts and indicators of good tax policy:

The article provides the explanation the ATO has projected that the taskforce will

continue to work in the direct of good tax policy by emphasising on the tax impact of the

entire system (Afr.com, 2019). It reflects that there is an enhancement in the tax gap more

generally.

Article 2: Removal of franking credit inequitable: Inquiry

Facts:

This article is associated with the proposal of labor regarding the removal of franking

credit for both the super funds and individuals. However, removing the franking credits is

considered highly flawed following parliamentary inquiry. The committee has considered

that abolition of the franking credits for both the individuals and the SMSF policy is highly

unequal.

Concise explanation of taxation concepts:

As per the article the imputation credits would enable the Australian firms to pass the

tax at the company level and finally to the shareholders. The parliamentary budget projects

that policy would cost budget around $5.2 billion in 2020-21 and may increase to $48.6

billion by 2027-28.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Explanation of connection between concepts and indicators of good tax policy:

The removal of the refundable franking credits for the SMSF and individuals is highly

inequitable and comprises of the flaws. Abolishing the refundable franking credit may be

unfair for most of the moderate income group that are retired.

Answer to question 7:

The tax agent or the tax advisor has the vital role of ensuring that the clients follow

the compliance procedure with all relevant taxation laws. This includes;

a. The tax agent must assist the clients in managing their tax affairs by assuring their

clients that they have understood the rights and obligations (Igt.gov.au, 2019).

b. The tax agent to promote compliance among the clients with tax laws should improve

the risk and compliance strategies with the help of better focussed information request

and conversation with the customers.

c. The tax advisors play a vital role in acting as the important leverage point for the

clients. They act as the key intermediate for taxation and superannuation system.

Explanation of connection between concepts and indicators of good tax policy:

The removal of the refundable franking credits for the SMSF and individuals is highly

inequitable and comprises of the flaws. Abolishing the refundable franking credit may be

unfair for most of the moderate income group that are retired.

Answer to question 7:

The tax agent or the tax advisor has the vital role of ensuring that the clients follow

the compliance procedure with all relevant taxation laws. This includes;

a. The tax agent must assist the clients in managing their tax affairs by assuring their

clients that they have understood the rights and obligations (Igt.gov.au, 2019).

b. The tax agent to promote compliance among the clients with tax laws should improve

the risk and compliance strategies with the help of better focussed information request

and conversation with the customers.

c. The tax advisors play a vital role in acting as the important leverage point for the

clients. They act as the key intermediate for taxation and superannuation system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Brydges, N., & Yuen, K. (2018). A matter of trusts: Trusts, income tax, CGT and foreign

residents. Taxation in Australia, 53(2), 80.

Campbell, S. (2018). Personal liability of a trustee to tax on trust income: Part 1. Taxation in

Australia, 53(5), 263.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury.

Carling, R. G. (2015). Right or rort? Dissecting Australia's tax concessions. Centre for

Independent Studies.

Chapter 7: Tax practitioners and advisors | Inspector-General of Taxation. (2019). Retrieved

from http://igt.gov.au/publications/reports-of-reviews/use-of-compliance-risk-

assessment-tools/chapter-7-tax-practitioners-and-advisors/#P2035_307929

Chardon, T. (2014). Taxation and superannuation literacy in Australia: What do people know

(or think they know)?. JASSA, (1), 42.

Datt, K. H., & Keating, M. (2018, April). The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New Zealand.

In Australian Tax Forum (Vol. 33, No. 3).

Duncan, A., Hodgson, H., Minas, J., Ong, R., & Seymour, R. G. (2018). The income tax

treatment of housing assets: an assessment of proposed reform arrangements.

Duncan, A., Hodgson, H., Minas, J., Ong, R., & Seymour, R. G. (2018). The income tax

treatment of housing assets: an assessment of proposed reform arrangements.

References:

Brydges, N., & Yuen, K. (2018). A matter of trusts: Trusts, income tax, CGT and foreign

residents. Taxation in Australia, 53(2), 80.

Campbell, S. (2018). Personal liability of a trustee to tax on trust income: Part 1. Taxation in

Australia, 53(5), 263.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury.

Carling, R. G. (2015). Right or rort? Dissecting Australia's tax concessions. Centre for

Independent Studies.

Chapter 7: Tax practitioners and advisors | Inspector-General of Taxation. (2019). Retrieved

from http://igt.gov.au/publications/reports-of-reviews/use-of-compliance-risk-

assessment-tools/chapter-7-tax-practitioners-and-advisors/#P2035_307929

Chardon, T. (2014). Taxation and superannuation literacy in Australia: What do people know

(or think they know)?. JASSA, (1), 42.

Datt, K. H., & Keating, M. (2018, April). The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New Zealand.

In Australian Tax Forum (Vol. 33, No. 3).

Duncan, A., Hodgson, H., Minas, J., Ong, R., & Seymour, R. G. (2018). The income tax

treatment of housing assets: an assessment of proposed reform arrangements.

Duncan, A., Hodgson, H., Minas, J., Ong, R., & Seymour, R. G. (2018). The income tax

treatment of housing assets: an assessment of proposed reform arrangements.

11TAXATION LAW

Evans, C., Minas, J., & Lim, Y. (2015). Taxing personal capital gains in Australia: an

alternative way forward. Austl. Tax F., 30, 735.

Franking credit removal 'inequitable': inquiry. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/franking-credit-removal-inequitable-and-

deeply-flawed-inquiry-20190404-p51az9

Ingles, D., 2015. Should capital income be taxed? And if so, how?. And If So, How.

Iskhakov, F., Thorp, S., & Bateman, H. (2015). Optimal annuity purchases for Australian

retirees. Economic Record, 91(293), 139-154.

McCluskey, W. J., & Franzsen, R. C. (2017). Land value taxation: An applied analysis.

Routledge.

White, A., Blackwood, C., & Cooper, G. (2019). Taxing private trusts-A moving

target. Taxation in Australia, 53(7), 372.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

Evans, C., Minas, J., & Lim, Y. (2015). Taxing personal capital gains in Australia: an

alternative way forward. Austl. Tax F., 30, 735.

Franking credit removal 'inequitable': inquiry. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/franking-credit-removal-inequitable-and-

deeply-flawed-inquiry-20190404-p51az9

Ingles, D., 2015. Should capital income be taxed? And if so, how?. And If So, How.

Iskhakov, F., Thorp, S., & Bateman, H. (2015). Optimal annuity purchases for Australian

retirees. Economic Record, 91(293), 139-154.

McCluskey, W. J., & Franzsen, R. C. (2017). Land value taxation: An applied analysis.

Routledge.

White, A., Blackwood, C., & Cooper, G. (2019). Taxing private trusts-A moving

target. Taxation in Australia, 53(7), 372.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.