Taxation Law: Income, Deductions, and Legal Precedents Analysis

VerifiedAdded on 2023/04/21

|12

|2764

|378

Case Study

AI Summary

This assignment provides a detailed analysis of taxation law, focusing on the determination of assessable income and allowable deductions. It examines various income sources, including salary, bonuses, awards, and investment income, alongside deductible expenses such as business costs, travel, and donations. The study applies relevant sections of the ITAA 1936 and ITAA 1997, incorporating jurisdictional judgements like Scott v CT and FCT v Dean. Additionally, it delves into the FCT v Cooke and Sherden case, exploring the implications of non-cash benefits and their taxability, referencing section 21A and similar cases like Payne v FCT. The assignment concludes with a computation of net income and tax payable, offering a comprehensive overview of taxation principles. Desklib provides a platform to access similar solved assignments and study resources.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part A:........................................................................................................................................2

Part B:.........................................................................................................................................6

Facts of the Case:...................................................................................................................6

Decisions and main principles applied in judgement:............................................................7

Relevance of Case and likely decision on similar facts:........................................................7

References:.................................................................................................................................9

Table of Contents

Part A:........................................................................................................................................2

Part B:.........................................................................................................................................6

Facts of the Case:...................................................................................................................6

Decisions and main principles applied in judgement:............................................................7

Relevance of Case and likely decision on similar facts:........................................................7

References:.................................................................................................................................9

2TAXATION LAW

Part A:

As per “section 6, ITAA 1936”, income derived from the personal exertion denotes

the income involving earnings, wages, salaries, allowances, bonus, etc. that is received by the

taxpayer by working as employee for providing any service or proceeds from carrying on any

business (Barkoczy, 2014). Regularly a large of the income under that is earned by the

taxpayer is held as ordinary income under “section 6-5, ITAA 1997”. The jurisdictional

concept of ordinary income concepts is explained in “Scott v CT (1935)” which requires the

application of necessary principles to treat the receipts in accordance with ordinary earnings

(Deutsch, 2018). The receipt of gross salary by Jane is an income from personal exertion

under “section 6, ITAA 1936”. Citing the jurisdictional judgement of “Scott v CT (1935)”

the gross salary of Jane is included for taxation purpose since it is an ordinary income under

“section 6-5, ITAA 1997”.

There should be existence of nexus between the receipts and services. The decision in

“FC of T v Dean (1997)” stated that retention payment to key employees for agreeing to be

employed after acquisition was treated as income (Blackstone, 2013). The performance bonus

received by Jane is held for assessment based on the receipt basis even though it relates to

future earnings period of 5th July 2018. Jane also reports the receipt of clothing allowance

from her employer. The clothing allowance is taxable as ordinary income within “section 6-

5, ITAA 1997” since she received in course of employment.

Expenses for ordinary clothing item namely office suits is non-deductible under

“Section 8-1, ITAA 1997”. The court in “Mansfield v FCT (1996)” explained that expenses

on ordinary articles of attire is non-deductible irrespective of any adequate appearance in a

work (Jover-Ledesma, 2014). The jewellery expense by Jane is ordinary article of apparel

and formal office cloth is non-deductible under “section 8-1, ITAA 1997”.

Part A:

As per “section 6, ITAA 1936”, income derived from the personal exertion denotes

the income involving earnings, wages, salaries, allowances, bonus, etc. that is received by the

taxpayer by working as employee for providing any service or proceeds from carrying on any

business (Barkoczy, 2014). Regularly a large of the income under that is earned by the

taxpayer is held as ordinary income under “section 6-5, ITAA 1997”. The jurisdictional

concept of ordinary income concepts is explained in “Scott v CT (1935)” which requires the

application of necessary principles to treat the receipts in accordance with ordinary earnings

(Deutsch, 2018). The receipt of gross salary by Jane is an income from personal exertion

under “section 6, ITAA 1936”. Citing the jurisdictional judgement of “Scott v CT (1935)”

the gross salary of Jane is included for taxation purpose since it is an ordinary income under

“section 6-5, ITAA 1997”.

There should be existence of nexus between the receipts and services. The decision in

“FC of T v Dean (1997)” stated that retention payment to key employees for agreeing to be

employed after acquisition was treated as income (Blackstone, 2013). The performance bonus

received by Jane is held for assessment based on the receipt basis even though it relates to

future earnings period of 5th July 2018. Jane also reports the receipt of clothing allowance

from her employer. The clothing allowance is taxable as ordinary income within “section 6-

5, ITAA 1997” since she received in course of employment.

Expenses for ordinary clothing item namely office suits is non-deductible under

“Section 8-1, ITAA 1997”. The court in “Mansfield v FCT (1996)” explained that expenses

on ordinary articles of attire is non-deductible irrespective of any adequate appearance in a

work (Jover-Ledesma, 2014). The jewellery expense by Jane is ordinary article of apparel

and formal office cloth is non-deductible under “section 8-1, ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Simple winning of prize is not an income but it may be an income if there is enough

relation with taxpayer income producing activity. In “FC of T v Kelly (1985)” the

professional footballer received an award for being the best player. The award constituted

taxable income because it was related to work and employment and was associated to use of

skills (McCouat, 2018). The award to Jane by ICA ANZ for being the best accountant is a

taxable income because it was related to work and was linked to use of Jane accounting

knowledge. While the computer received in award valued $2,550. Referring to “Cooke and

Sherden v FCT (1980)” gains that cannot be converted to income is treated as ordinary

income. The computer that is received by Jane is a taxable gain that can be converted to cash

and it is included for taxable purpose within the meaning of ordinary concept of income

under “section 6-5, ITAA 1997”.

Where an employer provides any kind of fringe benefit to an employee the benefit

will be treated as the non-taxable income for the employee under “section 23L of the ITAA

1936”. The employer however will be liable for fringe benefit tax on the value of the fringe

benefit (Kenny et al., 2018). The membership fees paid by the employer in respect of Jane

will be non-taxable for Jane under “section 23L, ITAA 1997” while her employer Milton

Hotels Ltd will be liable for FBT relating to value of benefit provided.

As per the ATO, the taxpayers are permitted to obtain an allowable income tax

deduction for expenses incurred in attending conferences, seminars or work related

educational workshop. Nevertheless, the personal portion of the expenses should be excluded

incurred during trip as they are non-deductible (Sadiq et al., 2014). Jane here will be allowed

to claim deduction for the registration fees, air tickets for her part and accommodation

expenses. She will be denied deduction for her husband air tickets and expenses occurred in

visiting historical place in Australia. These expenses are private in nature and not work

related.

Simple winning of prize is not an income but it may be an income if there is enough

relation with taxpayer income producing activity. In “FC of T v Kelly (1985)” the

professional footballer received an award for being the best player. The award constituted

taxable income because it was related to work and employment and was associated to use of

skills (McCouat, 2018). The award to Jane by ICA ANZ for being the best accountant is a

taxable income because it was related to work and was linked to use of Jane accounting

knowledge. While the computer received in award valued $2,550. Referring to “Cooke and

Sherden v FCT (1980)” gains that cannot be converted to income is treated as ordinary

income. The computer that is received by Jane is a taxable gain that can be converted to cash

and it is included for taxable purpose within the meaning of ordinary concept of income

under “section 6-5, ITAA 1997”.

Where an employer provides any kind of fringe benefit to an employee the benefit

will be treated as the non-taxable income for the employee under “section 23L of the ITAA

1936”. The employer however will be liable for fringe benefit tax on the value of the fringe

benefit (Kenny et al., 2018). The membership fees paid by the employer in respect of Jane

will be non-taxable for Jane under “section 23L, ITAA 1997” while her employer Milton

Hotels Ltd will be liable for FBT relating to value of benefit provided.

As per the ATO, the taxpayers are permitted to obtain an allowable income tax

deduction for expenses incurred in attending conferences, seminars or work related

educational workshop. Nevertheless, the personal portion of the expenses should be excluded

incurred during trip as they are non-deductible (Sadiq et al., 2014). Jane here will be allowed

to claim deduction for the registration fees, air tickets for her part and accommodation

expenses. She will be denied deduction for her husband air tickets and expenses occurred in

visiting historical place in Australia. These expenses are private in nature and not work

related.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

As per “section 25-100, ITAA 1997” deduction for travel is permitted to taxpayers

occurred for travelling between two work places. The travel should be related to work where

income producing activities is performed. Similarly in “FCT v Wiener (1978)” a teacher was

employed by education department was responsible for teaching in five different schools

during the week (Taylor et al., 2018). The court of law noticed that the employment of

taxpayer was travelling in nature and the travelling was made while performing her duties.

The taxation commissioner allowed deduction for travelling between schools. Similarly, Jane

is permitted to claim an allowable deduction under “section 25-100 ITAA 1997” for

travelling from her employment place to her taxation practicing business as both the place

involved producing of income.

The “taxation ruling of TR 98/1” is related with receipts and earnings basis of

accounting. Within “subsection 6-5 (2) and (3) of the ITAA 1997” there are two commonly

used method of tax accounting of items related to income under the receipts and earnings

method (Woellner et al., 2018). As per the receipts tax accounting method income is obtained

when it is received under “subsection 6-5(4), ITAA 1997”. While under the earnings or

accruals method income is obtained when it is earned. As held in “Barratt v FCT (1992)”

where the business activities of the taxpayer involves formal process of extending the credit

and collection of debts, the earnings method is regarded as the most appropriate method of

tax accounting.

As evident Jane reports receipts from her taxation business that consisted of billed and

unbilled amount. She also received rent from the investment property where a sum of $500

remained due. Referring to “FCT v Barratt (1992)” the earnings method of accounting is

suitable for Jane because it is helpful in giving a true reflex of income from investment

property and taxation business (Jones, 2017). Whereas the expenses incurred for rental

property and business practices is allowed for deduction under “section 8-1, ITAA 1997”.

As per “section 25-100, ITAA 1997” deduction for travel is permitted to taxpayers

occurred for travelling between two work places. The travel should be related to work where

income producing activities is performed. Similarly in “FCT v Wiener (1978)” a teacher was

employed by education department was responsible for teaching in five different schools

during the week (Taylor et al., 2018). The court of law noticed that the employment of

taxpayer was travelling in nature and the travelling was made while performing her duties.

The taxation commissioner allowed deduction for travelling between schools. Similarly, Jane

is permitted to claim an allowable deduction under “section 25-100 ITAA 1997” for

travelling from her employment place to her taxation practicing business as both the place

involved producing of income.

The “taxation ruling of TR 98/1” is related with receipts and earnings basis of

accounting. Within “subsection 6-5 (2) and (3) of the ITAA 1997” there are two commonly

used method of tax accounting of items related to income under the receipts and earnings

method (Woellner et al., 2018). As per the receipts tax accounting method income is obtained

when it is received under “subsection 6-5(4), ITAA 1997”. While under the earnings or

accruals method income is obtained when it is earned. As held in “Barratt v FCT (1992)”

where the business activities of the taxpayer involves formal process of extending the credit

and collection of debts, the earnings method is regarded as the most appropriate method of

tax accounting.

As evident Jane reports receipts from her taxation business that consisted of billed and

unbilled amount. She also received rent from the investment property where a sum of $500

remained due. Referring to “FCT v Barratt (1992)” the earnings method of accounting is

suitable for Jane because it is helpful in giving a true reflex of income from investment

property and taxation business (Jones, 2017). Whereas the expenses incurred for rental

property and business practices is allowed for deduction under “section 8-1, ITAA 1997”.

5TAXATION LAW

The dividends received by Jane is taxable as statutory income under “section 44 (1)

of the ITAA 1936”, The franking credits is included for assessment under “section 207-

20(1), ITAA 1997” however an income tax offset can be claimed to reduce the tax liability of

Jane (Campbell, 2018).

The sale of CBA shares resulted in capital gains which is included for taxation

purpose within the ordinary concepts while the disposal of BHP shares yielded loss. The loss

can be offset by Jane against the capital gains made from CBA shares. The donation made to

cancer council and University of Sydney by Jane is deductible under “section 30-15 (2),

subdivision 30c, ITAA 1997”.

The dividends received by Jane is taxable as statutory income under “section 44 (1)

of the ITAA 1936”, The franking credits is included for assessment under “section 207-

20(1), ITAA 1997” however an income tax offset can be claimed to reduce the tax liability of

Jane (Campbell, 2018).

The sale of CBA shares resulted in capital gains which is included for taxation

purpose within the ordinary concepts while the disposal of BHP shares yielded loss. The loss

can be offset by Jane against the capital gains made from CBA shares. The donation made to

cancer council and University of Sydney by Jane is deductible under “section 30-15 (2),

subdivision 30c, ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

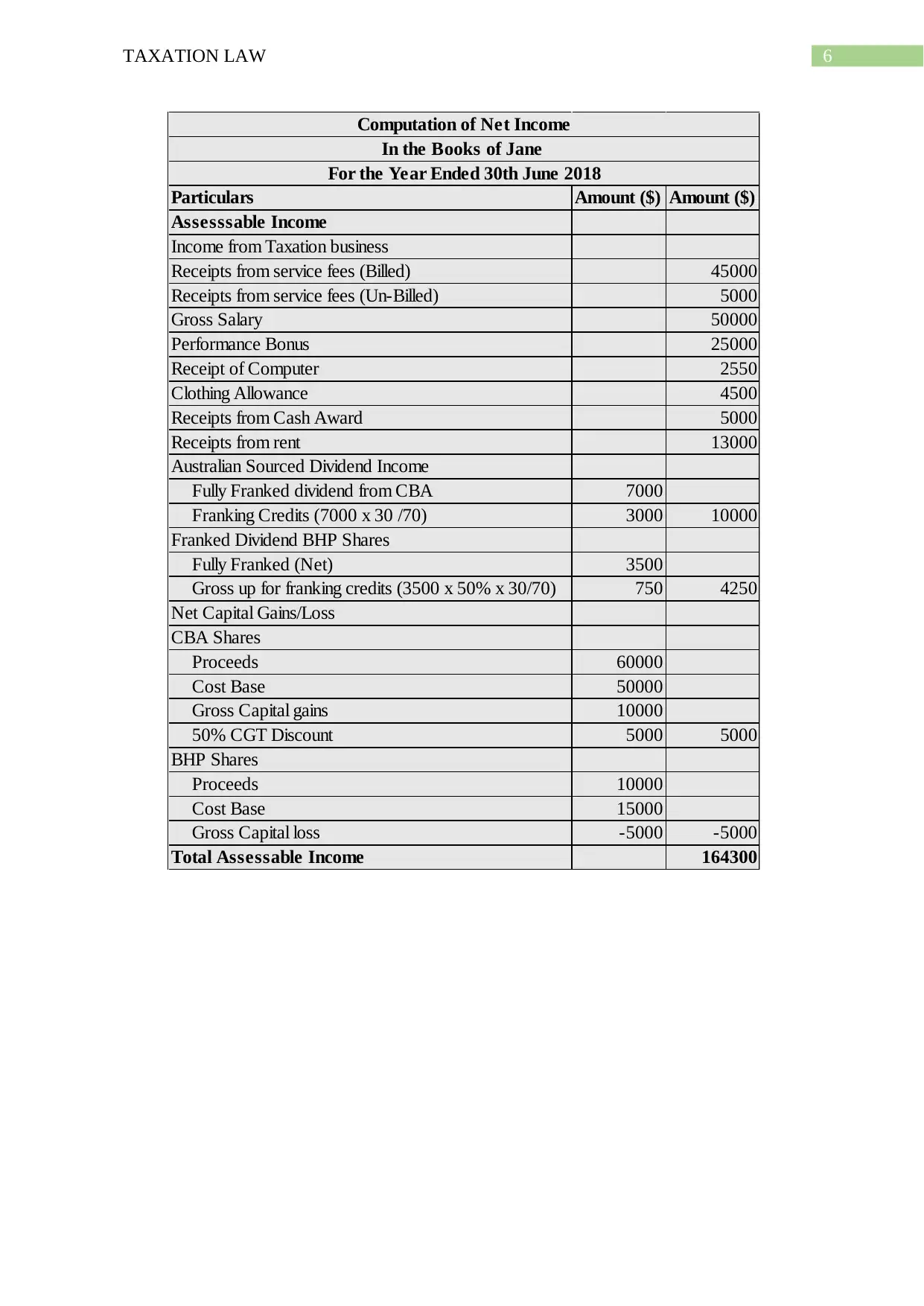

Particulars Amount ($) Amount ($)

Assesssable Income

Income from Taxation business

Receipts from service fees (Billed) 45000

Receipts from service fees (Un-Billed) 5000

Gross Salary 50000

Performance Bonus 25000

Receipt of Computer 2550

Clothing Allowance 4500

Receipts from Cash Award 5000

Receipts from rent 13000

Australian Sourced Dividend Income

Fully Franked dividend from CBA 7000

Franking Credits (7000 x 30 /70) 3000 10000

Franked Dividend BHP Shares

Fully Franked (Net) 3500

Gross up for franking credits (3500 x 50% x 30/70) 750 4250

Net Capital Gains/Loss

CBA Shares

Proceeds 60000

Cost Base 50000

Gross Capital gains 10000

50% CGT Discount 5000 5000

BHP Shares

Proceeds 10000

Cost Base 15000

Gross Capital loss -5000 -5000

Total Assessable Income 164300

Computation of Net Income

In the Books of Jane

For the Year Ended 30th June 2018

Particulars Amount ($) Amount ($)

Assesssable Income

Income from Taxation business

Receipts from service fees (Billed) 45000

Receipts from service fees (Un-Billed) 5000

Gross Salary 50000

Performance Bonus 25000

Receipt of Computer 2550

Clothing Allowance 4500

Receipts from Cash Award 5000

Receipts from rent 13000

Australian Sourced Dividend Income

Fully Franked dividend from CBA 7000

Franking Credits (7000 x 30 /70) 3000 10000

Franked Dividend BHP Shares

Fully Franked (Net) 3500

Gross up for franking credits (3500 x 50% x 30/70) 750 4250

Net Capital Gains/Loss

CBA Shares

Proceeds 60000

Cost Base 50000

Gross Capital gains 10000

50% CGT Discount 5000 5000

BHP Shares

Proceeds 10000

Cost Base 15000

Gross Capital loss -5000 -5000

Total Assessable Income 164300

Computation of Net Income

In the Books of Jane

For the Year Ended 30th June 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

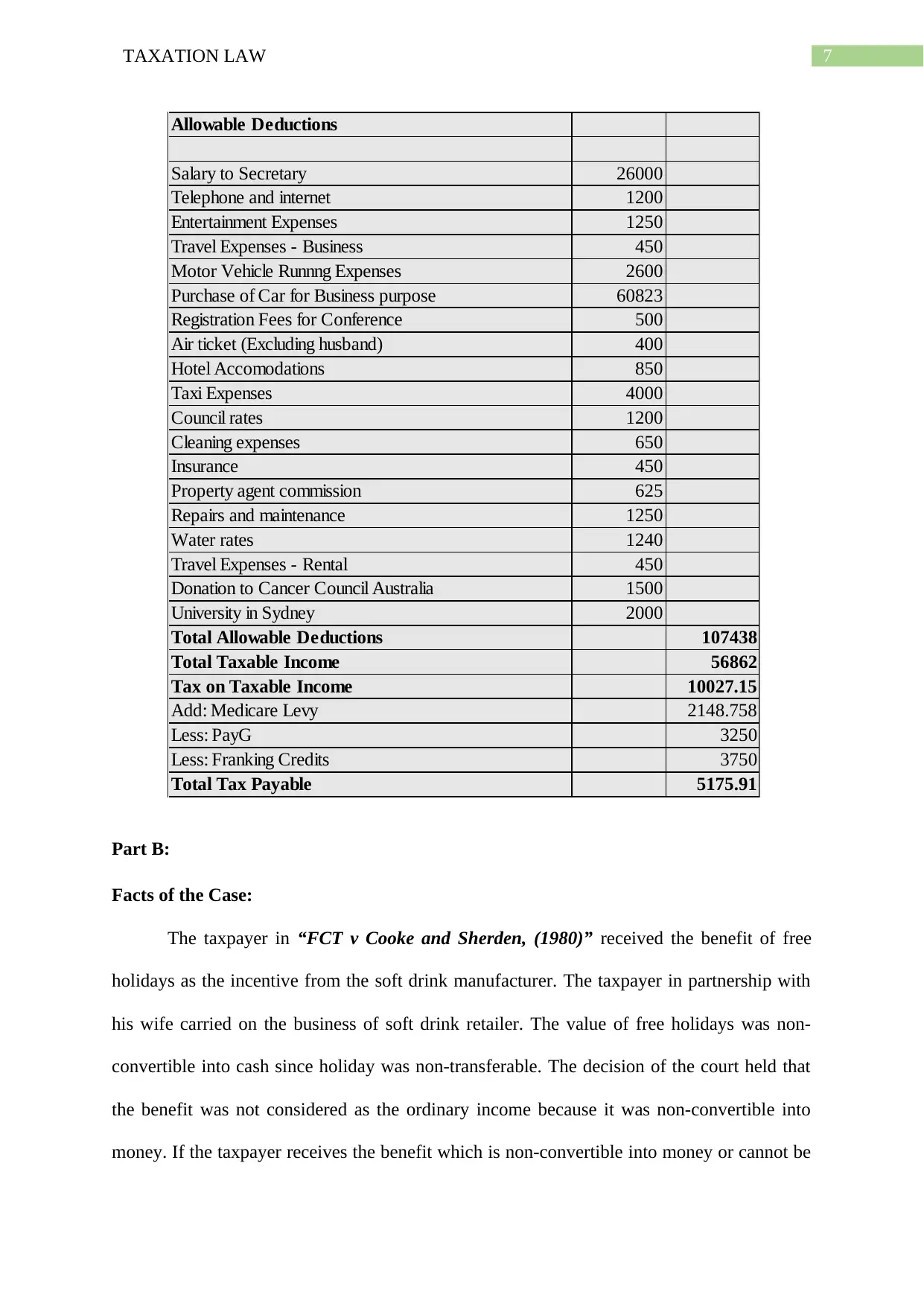

Allowable Deductions

Salary to Secretary 26000

Telephone and internet 1200

Entertainment Expenses 1250

Travel Expenses - Business 450

Motor Vehicle Runnng Expenses 2600

Purchase of Car for Business purpose 60823

Registration Fees for Conference 500

Air ticket (Excluding husband) 400

Hotel Accomodations 850

Taxi Expenses 4000

Council rates 1200

Cleaning expenses 650

Insurance 450

Property agent commission 625

Repairs and maintenance 1250

Water rates 1240

Travel Expenses - Rental 450

Donation to Cancer Council Australia 1500

University in Sydney 2000

Total Allowable Deductions 107438

Total Taxable Income 56862

Tax on Taxable Income 10027.15

Add: Medicare Levy 2148.758

Less: PayG 3250

Less: Franking Credits 3750

Total Tax Payable 5175.91

Part B:

Facts of the Case:

The taxpayer in “FCT v Cooke and Sherden, (1980)” received the benefit of free

holidays as the incentive from the soft drink manufacturer. The taxpayer in partnership with

his wife carried on the business of soft drink retailer. The value of free holidays was non-

convertible into cash since holiday was non-transferable. The decision of the court held that

the benefit was not considered as the ordinary income because it was non-convertible into

money. If the taxpayer receives the benefit which is non-convertible into money or cannot be

Allowable Deductions

Salary to Secretary 26000

Telephone and internet 1200

Entertainment Expenses 1250

Travel Expenses - Business 450

Motor Vehicle Runnng Expenses 2600

Purchase of Car for Business purpose 60823

Registration Fees for Conference 500

Air ticket (Excluding husband) 400

Hotel Accomodations 850

Taxi Expenses 4000

Council rates 1200

Cleaning expenses 650

Insurance 450

Property agent commission 625

Repairs and maintenance 1250

Water rates 1240

Travel Expenses - Rental 450

Donation to Cancer Council Australia 1500

University in Sydney 2000

Total Allowable Deductions 107438

Total Taxable Income 56862

Tax on Taxable Income 10027.15

Add: Medicare Levy 2148.758

Less: PayG 3250

Less: Franking Credits 3750

Total Tax Payable 5175.91

Part B:

Facts of the Case:

The taxpayer in “FCT v Cooke and Sherden, (1980)” received the benefit of free

holidays as the incentive from the soft drink manufacturer. The taxpayer in partnership with

his wife carried on the business of soft drink retailer. The value of free holidays was non-

convertible into cash since holiday was non-transferable. The decision of the court held that

the benefit was not considered as the ordinary income because it was non-convertible into

money. If the taxpayer receives the benefit which is non-convertible into money or cannot be

8TAXATION LAW

turned into the pecuniary account, then no income is received by the taxpayer within the

ordinary concepts of income under “section 6-5, ITAA 1997”.

Decisions and main principles applied in judgement:

In respect of “section 25 (1)”, the decision of court stated that gratuitous benefits in

kind which cannot be convertible to cash or property is not held as income under the ordinary

concepts (Datt & Keating, 2018). The federal court through illustration of “Abbott v Philbin

(1961)” stated that even though the options of shares was unassignable however the right for

calling of shares was treated as having the money’s worth since it could be employed as the

medium of borrowing money (King, 2016). The view of court stated that benefits or gifts of

this type is taxable given it is converted to cash or money’s worth. The court also stated that

it was irrelevant that the taxpayers saved the expenditure which might have occurred if they

had paid themselves for the holiday and such savings could not be held as income.

The law court perceived that it would not regularly happen that a benefit that is to be

enjoyed by the taxpayer could not be turned into pecuniary account given the benefit is

surrendered or used in acquiring some other rights. In accordance with “section 26 (e)”, the

court stated that no service in relevant sense was rendered by the taxpayer to manufacturers.

While distributing the soft drinks the taxpayer only performed business activities for their

own benefit (Burton, 2017). The fact that the successful business operations led to holiday

trips which does not change the basic relation between the buyer and seller that the court held

be present among the manufacturers and taxpayers. Based on this facts there was no options

for application of “section 26 (e)”. The judgement of federal court does not impose any

restraints on this section.

turned into the pecuniary account, then no income is received by the taxpayer within the

ordinary concepts of income under “section 6-5, ITAA 1997”.

Decisions and main principles applied in judgement:

In respect of “section 25 (1)”, the decision of court stated that gratuitous benefits in

kind which cannot be convertible to cash or property is not held as income under the ordinary

concepts (Datt & Keating, 2018). The federal court through illustration of “Abbott v Philbin

(1961)” stated that even though the options of shares was unassignable however the right for

calling of shares was treated as having the money’s worth since it could be employed as the

medium of borrowing money (King, 2016). The view of court stated that benefits or gifts of

this type is taxable given it is converted to cash or money’s worth. The court also stated that

it was irrelevant that the taxpayers saved the expenditure which might have occurred if they

had paid themselves for the holiday and such savings could not be held as income.

The law court perceived that it would not regularly happen that a benefit that is to be

enjoyed by the taxpayer could not be turned into pecuniary account given the benefit is

surrendered or used in acquiring some other rights. In accordance with “section 26 (e)”, the

court stated that no service in relevant sense was rendered by the taxpayer to manufacturers.

While distributing the soft drinks the taxpayer only performed business activities for their

own benefit (Burton, 2017). The fact that the successful business operations led to holiday

trips which does not change the basic relation between the buyer and seller that the court held

be present among the manufacturers and taxpayers. Based on this facts there was no options

for application of “section 26 (e)”. The judgement of federal court does not impose any

restraints on this section.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Relevance of Case and likely decision on similar facts:

The example of “FCT v Cooke and Sherden, (1980)” is yet considered as the

relevant case because jurisdictional judgement resulted in the adoption of “section 21A”.

According to “section 21A” non-cash business benefits that is received by the taxpayer

which cannot be converted into will be treated as if they can be converted to cash (Miller &

Oats, 2016). Within the meaning of this Act, if the non-cash business benefits whether or not

it can be converted into cash is treated as income derived by taxpayer.

A similar example of “Payne v FCT (1996)” was followed where the commissioner

measured the taxpayer in terms of the market value of the tickets (Fleurbaey & Maniquet,

2015). The court of law held that the frequent flyer points were not treated as income since it

was not the income. The frequent flyer points cannot be converted or transferred and will be

cancelled if sold.

Relevance of Case and likely decision on similar facts:

The example of “FCT v Cooke and Sherden, (1980)” is yet considered as the

relevant case because jurisdictional judgement resulted in the adoption of “section 21A”.

According to “section 21A” non-cash business benefits that is received by the taxpayer

which cannot be converted into will be treated as if they can be converted to cash (Miller &

Oats, 2016). Within the meaning of this Act, if the non-cash business benefits whether or not

it can be converted into cash is treated as income derived by taxpayer.

A similar example of “Payne v FCT (1996)” was followed where the commissioner

measured the taxpayer in terms of the market value of the tickets (Fleurbaey & Maniquet,

2015). The court of law held that the frequent flyer points were not treated as income since it

was not the income. The frequent flyer points cannot be converted or transferred and will be

cancelled if sold.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Barkoczy, S. (2014). Foundations of taxation law 2014.

Blackstone, S. (2013). Commentaries on the laws of england.: Gale, Making Of Modern La.

Burton, M. (2017). A Review of Judicial References to the Dictum of Jordan CJ, Expressed

in Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n, 19, 50.

Campbell, S. (2018). Personal liability of a trustee to tax on trust income: Part 2. Taxation in

Australia, 53(6), 322.

Datt, K. H., & Keating, M. (2018, April). The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New Zealand.

In Australian Tax Forum (Vol. 33, No. 3).

Deutsch, R. (2018). Australian tax handbook 2018.: THOMSON REUTERS AUSTRALIA.

Fleurbaey, M., & Maniquet, F. (2015). Optimal taxation theory and principles of

fairness (No. 2015005). Université catholique de Louvain, Center for Operations

Research and Econometrics (CORE).

Jones, D. (2017). Tax and accounting income-Worlds apart?. Taxation in Australia, 52(1),

14.

Jover-Ledesma, G. (2014). Principles of business taxation 2015.: Cch Incorporated.

Kenny, P., Blissenden, M., & Villios, S. (2018). Australian Tax 2018.

King, A. (2016). Mid market focus: The new attribution tax regime for MITs: Part

2. Taxation in Australia, 51(1), 12.

McCouat, P. (2018) Australian master GST guide 2018.

References:

Barkoczy, S. (2014). Foundations of taxation law 2014.

Blackstone, S. (2013). Commentaries on the laws of england.: Gale, Making Of Modern La.

Burton, M. (2017). A Review of Judicial References to the Dictum of Jordan CJ, Expressed

in Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n, 19, 50.

Campbell, S. (2018). Personal liability of a trustee to tax on trust income: Part 2. Taxation in

Australia, 53(6), 322.

Datt, K. H., & Keating, M. (2018, April). The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New Zealand.

In Australian Tax Forum (Vol. 33, No. 3).

Deutsch, R. (2018). Australian tax handbook 2018.: THOMSON REUTERS AUSTRALIA.

Fleurbaey, M., & Maniquet, F. (2015). Optimal taxation theory and principles of

fairness (No. 2015005). Université catholique de Louvain, Center for Operations

Research and Econometrics (CORE).

Jones, D. (2017). Tax and accounting income-Worlds apart?. Taxation in Australia, 52(1),

14.

Jover-Ledesma, G. (2014). Principles of business taxation 2015.: Cch Incorporated.

Kenny, P., Blissenden, M., & Villios, S. (2018). Australian Tax 2018.

King, A. (2016). Mid market focus: The new attribution tax regime for MITs: Part

2. Taxation in Australia, 51(1), 12.

McCouat, P. (2018) Australian master GST guide 2018.

11TAXATION LAW

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., & Ting, A. (2014).

Principles of taxation law 2014.

Taylor, C., Walpole, M., Burton, M., Ciro, T., & Murray, I. Understanding taxation law

(2018).

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2018). Australian taxation

law 2018.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., & Ting, A. (2014).

Principles of taxation law 2014.

Taylor, C., Walpole, M., Burton, M., Ciro, T., & Murray, I. Understanding taxation law

(2018).

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2018). Australian taxation

law 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.