LAWS20060: Taxation Law of Australia Individual Assignment

VerifiedAdded on 2022/12/05

|17

|4200

|262

Homework Assignment

AI Summary

This document presents a detailed solution to a taxation law assignment, likely for an Australian law course. The assignment covers various aspects of taxation, including depreciation of assets, tax offsets, calculation of taxable income, and the difference between marginal and average tax rates. It delves into specific sections of the Income Tax Assessment Act 1997 (ITAA 1997) and relevant tax rulings, providing answers to questions regarding capital gains tax (CGT) events, main residence exemptions, and calculations of capital gains and losses. The assignment also examines allowable deductions, including business expenses, private use of assets, and losses. Furthermore, it explores topics such as CGT events and the application of relevant case law to support arguments. The document includes references to various legal sources, including legislation, cases, and tax rulings, adhering to the Australian Guide to Legal Citation (AGLC) referencing method. The solution provided is a comprehensive resource for students studying taxation law, offering insights into complex tax concepts and providing practical examples.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................5

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................6

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................7

Answer to E:...........................................................................................................................7

Answer to question 3:.................................................................................................................8

Answer A:..............................................................................................................................8

Answer B:...............................................................................................................................8

Answer C:...............................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................4

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................5

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................6

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................7

Answer to E:...........................................................................................................................7

Answer to question 3:.................................................................................................................8

Answer A:..............................................................................................................................8

Answer B:...............................................................................................................................8

Answer C:...............................................................................................................................9

2TAXATION LAW

Answer D:............................................................................................................................10

Answer to question 4:...............................................................................................................10

Answer A:............................................................................................................................10

Answer B:.............................................................................................................................11

Answer C:.............................................................................................................................11

Answer D:............................................................................................................................12

Answer E:.............................................................................................................................12

Answer to question 5:...............................................................................................................12

Issues:...................................................................................................................................12

Laws:....................................................................................................................................13

Application:..........................................................................................................................14

Conclusion:..........................................................................................................................15

References:...............................................................................................................................16

Answer D:............................................................................................................................10

Answer to question 4:...............................................................................................................10

Answer A:............................................................................................................................10

Answer B:.............................................................................................................................11

Answer C:.............................................................................................................................11

Answer D:............................................................................................................................12

Answer E:.............................................................................................................................12

Answer to question 5:...............................................................................................................12

Issues:...................................................................................................................................12

Laws:....................................................................................................................................13

Application:..........................................................................................................................14

Conclusion:..........................................................................................................................15

References:...............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Answer A:

Under the Taxation Ruling of TR 2018/14 the topic relating to a depreciating assets

effective life has been discussed within the legislation of “section 40-100, ITAA 1997”.

Answer B:

Details regarding the availability of the tax offset has been given under the “Division

13 of the ITAA 1997”1.

Answer C:

According to the ATO the highest amount of tax rate that is applied on the resident

tax payer for the year 2018-19 includes 54,097 + 45c for each $1 above $180,000.

Answer D:

“Section 108-20 (2)” defines the private use asset as something that is used for

private use satisfaction exclusive of the land and building. Any kind of capital gains that are

made from the private use asset that is bought for $10,000 or less must be disregarded under

the “section 118-10 (3), ITAA 1997”.

Answer E:

Under the “section 104-15 (1) of the ITAA 1997” the CGT events B1 happens when

a taxpayer enters into the covenant with the another entity on the conditions which includes2;

1 Gordon, Roger H. "The Rise of the Value-Added Tax. Cambridge Tax Law series." (2016):

243-246.

2 Lang, Michael, et al., eds. Introduction to European tax law on direct taxation. Linde

Verlag GmbH, 2018.

Answer to question 1:

Answer A:

Under the Taxation Ruling of TR 2018/14 the topic relating to a depreciating assets

effective life has been discussed within the legislation of “section 40-100, ITAA 1997”.

Answer B:

Details regarding the availability of the tax offset has been given under the “Division

13 of the ITAA 1997”1.

Answer C:

According to the ATO the highest amount of tax rate that is applied on the resident

tax payer for the year 2018-19 includes 54,097 + 45c for each $1 above $180,000.

Answer D:

“Section 108-20 (2)” defines the private use asset as something that is used for

private use satisfaction exclusive of the land and building. Any kind of capital gains that are

made from the private use asset that is bought for $10,000 or less must be disregarded under

the “section 118-10 (3), ITAA 1997”.

Answer E:

Under the “section 104-15 (1) of the ITAA 1997” the CGT events B1 happens when

a taxpayer enters into the covenant with the another entity on the conditions which includes2;

1 Gordon, Roger H. "The Rise of the Value-Added Tax. Cambridge Tax Law series." (2016):

243-246.

2 Lang, Michael, et al., eds. Introduction to European tax law on direct taxation. Linde

Verlag GmbH, 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

a. The right of using the CGT asset that is owned by a person is passed to another entity

b. It also includes the title that are present in the asset will or might pass to another

entity at or prior to the conclusion of the agreement.

Answer F:

As it has been explained in “section 4-10 of the ITAA 1997” an individual taxpayer is

under obligation of paying tax each year. Additionally, in “section 4-10 (3), ITAA 1997” a

formula has been given for calculating the amount of income tax payable. The formula

includes;

Income tax = [Taxable Income x Rate] – Tax Offsets

Answer G:

As held in the case of “FC of T v Day 2008 ATC 20-064” the public servant was the

officer and the application of “section 8-1, ITAA 1997” was made relating to the deduction

of the legal expenditure which the taxpayer incurred because of numerous charges against

him3. The court held that the charges against the public servant was because of his own

consequences and hence the legal expenditure were not permissible for deductions in

“section 8-1 of ITAA 1997”.

Answer H:

The difference between the marginal and average tax is given below

a. The marginal tax is regarded as the amount that is paid on the additional dollar of

income. The average tax is paid as the percentage of an individual’s taxable income

that is effectively paid as tax.

3 Pogge, Thomas, and Krishen Mehta, eds. Global tax fairness. Oxford University Press,

2016.

a. The right of using the CGT asset that is owned by a person is passed to another entity

b. It also includes the title that are present in the asset will or might pass to another

entity at or prior to the conclusion of the agreement.

Answer F:

As it has been explained in “section 4-10 of the ITAA 1997” an individual taxpayer is

under obligation of paying tax each year. Additionally, in “section 4-10 (3), ITAA 1997” a

formula has been given for calculating the amount of income tax payable. The formula

includes;

Income tax = [Taxable Income x Rate] – Tax Offsets

Answer G:

As held in the case of “FC of T v Day 2008 ATC 20-064” the public servant was the

officer and the application of “section 8-1, ITAA 1997” was made relating to the deduction

of the legal expenditure which the taxpayer incurred because of numerous charges against

him3. The court held that the charges against the public servant was because of his own

consequences and hence the legal expenditure were not permissible for deductions in

“section 8-1 of ITAA 1997”.

Answer H:

The difference between the marginal and average tax is given below

a. The marginal tax is regarded as the amount that is paid on the additional dollar of

income. The average tax is paid as the percentage of an individual’s taxable income

that is effectively paid as tax.

3 Pogge, Thomas, and Krishen Mehta, eds. Global tax fairness. Oxford University Press,

2016.

5TAXATION LAW

b. The average tax rate represents the total amount of tax divided by the total earnings.

While the marginal tax is regarded as the incremental tax that is paid with the rise on

income.

Answer I:

The consumption tax is paid on the consumption spending of goods and services. The

tax base of such kind of tax is the amount of money that is spend on the consumption. It is

worth mentioning that consumption tax is indirect tax namely the sales tax and value added

tax.

Answer to question 2:

Answer to A:

As defined in the “Section 8-1, ITAA 1997” there are two positive limbs where the

taxpayer can obtain deduction4. This implies that a person can be entitled to allowable

deductions for the loss or outgoings that are incurred in generating the taxable earnings and

the outgoings that a taxpayer occurs in deriving his business income. The federal

commissioner in “Ronpibon Tin NL v FCT (1949)” held that the expenses are only

permitted for tax deduction when the outgoings are relevant in producing assessable income.

As understood Brett took out a loan against his home so that he can be pay the wages

of his employees. Referring to the case of “Ronpibon Tin NL v FCT (1949)” the interest on

loan that is occurred is permissible for deduction under “section 8-1, ITAA 1997” for the

reason that it is relevant in producing assessable income5.

4 Motro, Shari. "The Income Tax Map: A Bird's-eye View of Federal Income Taxation for

Law Students." (2016): 1.

5 Gordon, Robert N. "REIT and MLP Taxation Under the New Tax Law." Journal of

Taxation of Investments 35.4 (2018).

b. The average tax rate represents the total amount of tax divided by the total earnings.

While the marginal tax is regarded as the incremental tax that is paid with the rise on

income.

Answer I:

The consumption tax is paid on the consumption spending of goods and services. The

tax base of such kind of tax is the amount of money that is spend on the consumption. It is

worth mentioning that consumption tax is indirect tax namely the sales tax and value added

tax.

Answer to question 2:

Answer to A:

As defined in the “Section 8-1, ITAA 1997” there are two positive limbs where the

taxpayer can obtain deduction4. This implies that a person can be entitled to allowable

deductions for the loss or outgoings that are incurred in generating the taxable earnings and

the outgoings that a taxpayer occurs in deriving his business income. The federal

commissioner in “Ronpibon Tin NL v FCT (1949)” held that the expenses are only

permitted for tax deduction when the outgoings are relevant in producing assessable income.

As understood Brett took out a loan against his home so that he can be pay the wages

of his employees. Referring to the case of “Ronpibon Tin NL v FCT (1949)” the interest on

loan that is occurred is permissible for deduction under “section 8-1, ITAA 1997” for the

reason that it is relevant in producing assessable income5.

4 Motro, Shari. "The Income Tax Map: A Bird's-eye View of Federal Income Taxation for

Law Students." (2016): 1.

5 Gordon, Robert N. "REIT and MLP Taxation Under the New Tax Law." Journal of

Taxation of Investments 35.4 (2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to B:

A taxpayer is usually permissible to get deduction for most of the business outlays. If

the expenditure having the mix of both the business and private use, then only the taxpayers

are allowable to get deduction for the portion of expenses that is associated to business. Julie

incurred an outgoing of $500 on mobile phone charges6. A portion of 60% calls are for

business purpose while the left over remains private use of mobile phone. Julie can only

claim business portion of mobile phone expenses as the expenses is associated to business

and derivation of assessable income.

Answer to C:

Taxpayers must denote that expenses of domestic or private character is not

deductible because if fails meet the positive limbs or non-deductible under the second

negative limbs of “section 8-1 (2(b)”. The federal commissioner conclusion in “Lodge v

FCT (1972)” held that the child care expenses was not allowed for deduction because these

are not relevant and incidental to the production of taxable income7.

Sally here occurs an expense of $1,200 where she is required to pay for her babysitter

so that her children can be looked after while she is attending work. Stating to conclusion

made in “Lodge v FCT (1972)” babysitter expenses is not permissible for deduction in the

second negative limbs of “section 8-1 (2(b)” because these are not appropriate and

supplementary to the production of taxable income.

6 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

7 Morini, Matteo, and Simone Pellegrino. "Personal income tax reforms: A genetic algorithm

approach." European Journal of Operational Research 264.3 (2018): 994-1004.

Answer to B:

A taxpayer is usually permissible to get deduction for most of the business outlays. If

the expenditure having the mix of both the business and private use, then only the taxpayers

are allowable to get deduction for the portion of expenses that is associated to business. Julie

incurred an outgoing of $500 on mobile phone charges6. A portion of 60% calls are for

business purpose while the left over remains private use of mobile phone. Julie can only

claim business portion of mobile phone expenses as the expenses is associated to business

and derivation of assessable income.

Answer to C:

Taxpayers must denote that expenses of domestic or private character is not

deductible because if fails meet the positive limbs or non-deductible under the second

negative limbs of “section 8-1 (2(b)”. The federal commissioner conclusion in “Lodge v

FCT (1972)” held that the child care expenses was not allowed for deduction because these

are not relevant and incidental to the production of taxable income7.

Sally here occurs an expense of $1,200 where she is required to pay for her babysitter

so that her children can be looked after while she is attending work. Stating to conclusion

made in “Lodge v FCT (1972)” babysitter expenses is not permissible for deduction in the

second negative limbs of “section 8-1 (2(b)” because these are not appropriate and

supplementary to the production of taxable income.

6 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

7 Morini, Matteo, and Simone Pellegrino. "Personal income tax reforms: A genetic algorithm

approach." European Journal of Operational Research 264.3 (2018): 994-1004.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to D:

Losses to the financial resources of the taxpayer that are diminished are permissible

for deduction under the provision of “section 8-1, ITAA 1997”. The federal commissioner

decision in “Charles Moore & Co Pty Ltd v FCT (1956)” explained that loss of financial

resources in the form of money stolen was permitted as deduction.

Similarly, the loss of $20,000 stole goods by the long term employee of Jerry should

be considered as the losses to the financial resources for Jerry that are diminished. Stating the

commissioner decision in “Charles Moore & Co Pty Ltd v FCT (1956)” the theft of $20,000

is an allowable deduction under provision of “section 8-1, ITAA 1997”.

Answer to E:

Conferring to the common provision of “section 8-1, ITAA 1997” expenditure that

are introductory to the start of revenue making acts or business is regarded as not occurred in

the course of such activity and hence non-deductible8. The federal commissioner judgement

in “FCT v Maddelena (1971)” held that expenditure to obtain new employment is not related

to generation of assessable income. The taxpayer was denied deduction for travel expense to

obtain new employment as it occurred at a point too soon.

The costs incurred in contesting the local government election is not allowable for

deduction under the common provision of “section 8-1, ITAA 1997” because they are

preliminary to income producing activities and not in the course of producing taxable

earning. The expenses were incurred at a point too soon9.

8 Butler, Daniel. "Who can provide taxation advice?." Taxation in Australia 53.7 (2019): 381.

9 Barkoczy, Stephen, Foundations Of Taxation Law 2014

Answer to D:

Losses to the financial resources of the taxpayer that are diminished are permissible

for deduction under the provision of “section 8-1, ITAA 1997”. The federal commissioner

decision in “Charles Moore & Co Pty Ltd v FCT (1956)” explained that loss of financial

resources in the form of money stolen was permitted as deduction.

Similarly, the loss of $20,000 stole goods by the long term employee of Jerry should

be considered as the losses to the financial resources for Jerry that are diminished. Stating the

commissioner decision in “Charles Moore & Co Pty Ltd v FCT (1956)” the theft of $20,000

is an allowable deduction under provision of “section 8-1, ITAA 1997”.

Answer to E:

Conferring to the common provision of “section 8-1, ITAA 1997” expenditure that

are introductory to the start of revenue making acts or business is regarded as not occurred in

the course of such activity and hence non-deductible8. The federal commissioner judgement

in “FCT v Maddelena (1971)” held that expenditure to obtain new employment is not related

to generation of assessable income. The taxpayer was denied deduction for travel expense to

obtain new employment as it occurred at a point too soon.

The costs incurred in contesting the local government election is not allowable for

deduction under the common provision of “section 8-1, ITAA 1997” because they are

preliminary to income producing activities and not in the course of producing taxable

earning. The expenses were incurred at a point too soon9.

8 Butler, Daniel. "Who can provide taxation advice?." Taxation in Australia 53.7 (2019): 381.

9 Barkoczy, Stephen, Foundations Of Taxation Law 2014

8TAXATION LAW

Answer to question 3:

Answer A:

As per the ATO CGT event F2 happens when the long term lease is renewed or

granted by the taxpayers. When the CGT event F2 is applied when the land owner is grants

any kind of sub-lease of land. Under such situations no CGT discount is provided to the

taxpayers.

A land is owned by Andy where he grants a five-year lease of the land on the

premium amount of $5,000. The Lease which is granted by Andy for a five-year period has

gave rise to CGT event F2 and as a result no CGT discount is applicable for Andy.

Answer B:

Where any kind of use and enjoyment of title is passed to another person then a CGT

event B1 transpires. Where the title of CGT asset title is passed and any capital gains thereof

following the subtraction of acquisition cost will result in CGT event B1. The use and

enjoyment of asset only happens when the title of the asset that is passed to another owner

and the person is allowed to deriving profits and rent the land10. Similarly, in the case of Farm

Ltd, the taxpayer was granted with an option of purchasing the farm for an amount of

$800,000. The grant of option gives rise to CGT event B1 and as result John can apply for the

CGT discount until the title of the asset is passed.

Answer C:

Main residence is exempt from CGT. Though, a taxpayer is only allowed to get main

residence exception when the property is not used for producing income. however, on using

10 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of

Business Taxation

Answer to question 3:

Answer A:

As per the ATO CGT event F2 happens when the long term lease is renewed or

granted by the taxpayers. When the CGT event F2 is applied when the land owner is grants

any kind of sub-lease of land. Under such situations no CGT discount is provided to the

taxpayers.

A land is owned by Andy where he grants a five-year lease of the land on the

premium amount of $5,000. The Lease which is granted by Andy for a five-year period has

gave rise to CGT event F2 and as a result no CGT discount is applicable for Andy.

Answer B:

Where any kind of use and enjoyment of title is passed to another person then a CGT

event B1 transpires. Where the title of CGT asset title is passed and any capital gains thereof

following the subtraction of acquisition cost will result in CGT event B1. The use and

enjoyment of asset only happens when the title of the asset that is passed to another owner

and the person is allowed to deriving profits and rent the land10. Similarly, in the case of Farm

Ltd, the taxpayer was granted with an option of purchasing the farm for an amount of

$800,000. The grant of option gives rise to CGT event B1 and as result John can apply for the

CGT discount until the title of the asset is passed.

Answer C:

Main residence is exempt from CGT. Though, a taxpayer is only allowed to get main

residence exception when the property is not used for producing income. however, on using

10 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of

Business Taxation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

the property for producing income then an individual is permissible to get partial main

residence exemption11.

A property was purchased by Jamie and Olivia which they rented out for two years.

However, from the year 2008, the property was used as main residence by Jamie and Olivia

before it was finally sold in 2018. As the property was used by Jamie and Olivia for making

income. They can only get partial main house exemption and a 50% CGT discount is

applicable in this case.

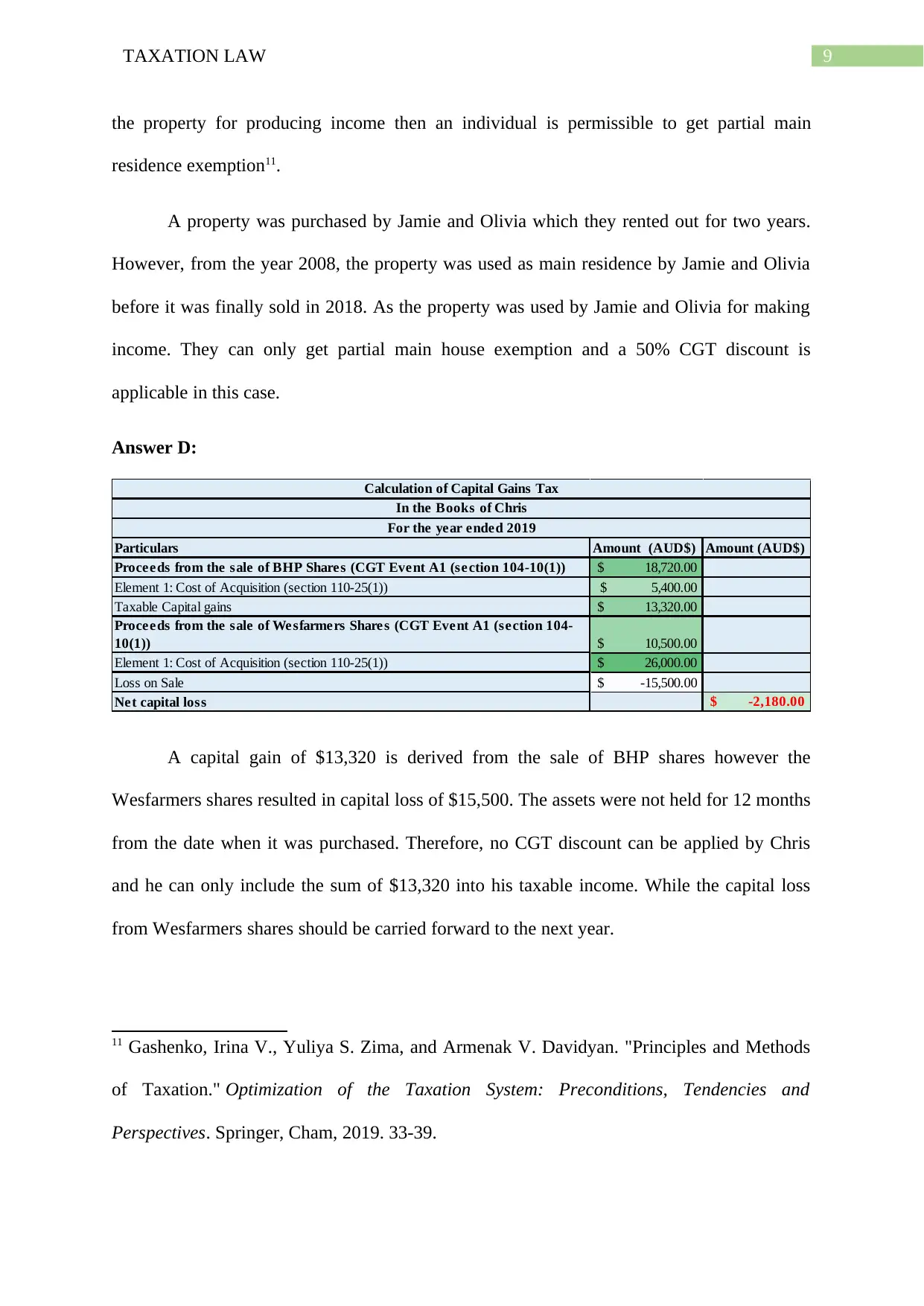

Answer D:

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18,720.00$

Element 1: Cost of Acquisition (section 110-25(1)) 5,400.00$

Taxable Capital gains 13,320.00$

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10,500.00$

Element 1: Cost of Acquisition (section 110-25(1)) 26,000.00$

Loss on Sale -15,500.00$

Net capital loss -2,180.00$

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

A capital gain of $13,320 is derived from the sale of BHP shares however the

Wesfarmers shares resulted in capital loss of $15,500. The assets were not held for 12 months

from the date when it was purchased. Therefore, no CGT discount can be applied by Chris

and he can only include the sum of $13,320 into his taxable income. While the capital loss

from Wesfarmers shares should be carried forward to the next year.

11 Gashenko, Irina V., Yuliya S. Zima, and Armenak V. Davidyan. "Principles and Methods

of Taxation." Optimization of the Taxation System: Preconditions, Tendencies and

Perspectives. Springer, Cham, 2019. 33-39.

the property for producing income then an individual is permissible to get partial main

residence exemption11.

A property was purchased by Jamie and Olivia which they rented out for two years.

However, from the year 2008, the property was used as main residence by Jamie and Olivia

before it was finally sold in 2018. As the property was used by Jamie and Olivia for making

income. They can only get partial main house exemption and a 50% CGT discount is

applicable in this case.

Answer D:

Particulars Amount (AUD$) Amount (AUD$)

Proceeds from the sale of BHP Shares (CGT Event A1 (section 104-10(1)) 18,720.00$

Element 1: Cost of Acquisition (section 110-25(1)) 5,400.00$

Taxable Capital gains 13,320.00$

Proceeds from the sale of Wesfarmers Shares (CGT Event A1 (section 104-

10(1)) 10,500.00$

Element 1: Cost of Acquisition (section 110-25(1)) 26,000.00$

Loss on Sale -15,500.00$

Net capital loss -2,180.00$

Calculation of Capital Gains Tax

In the Books of Chris

For the year ended 2019

A capital gain of $13,320 is derived from the sale of BHP shares however the

Wesfarmers shares resulted in capital loss of $15,500. The assets were not held for 12 months

from the date when it was purchased. Therefore, no CGT discount can be applied by Chris

and he can only include the sum of $13,320 into his taxable income. While the capital loss

from Wesfarmers shares should be carried forward to the next year.

11 Gashenko, Irina V., Yuliya S. Zima, and Armenak V. Davidyan. "Principles and Methods

of Taxation." Optimization of the Taxation System: Preconditions, Tendencies and

Perspectives. Springer, Cham, 2019. 33-39.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Answer to question 4:

Answer A:

The federal commissioner in “Moore v Griffiths (1972)” held that the simple prize

should not be considered as income12. However, it is treated as income where there is

sufficient link with income earning events of taxpayer. The federal commissioner in “FCT v

Stone (2005)” held that the taxpayer was assessable for the prize winnings because it was

connected to her revenue making activities.

The prize winnings for being the best advertisement of the year will be considered.

The amount of $2,000 constitute taxable income under the ordinary concepts of “section 6-5,

ITAA 1997” because it is associated to the income producing activities of the taxpayer.

Answer B:

Where an employee is reimbursed for the expenditure occurred is not regarded as

income. It should be noted that the employee here incurred an expenditure of $500 for

travelling to Sydney was related to work13. But the employee only occurred an amount of

$120 for the whole trip. As a result, the remaining amount of $380 will be regarded as gain to

the employee and the sum will be treated as income in the ordinary conceptions of “section

6-5, ITAA 1997”.

Answer C:

Gains that are simple gifts received by the individual taxpayer should be treated as

having the nature of income. Similarly, the federal court decision in “Hayes v FCT (1956)”

12 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

13 Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013)

Answer to question 4:

Answer A:

The federal commissioner in “Moore v Griffiths (1972)” held that the simple prize

should not be considered as income12. However, it is treated as income where there is

sufficient link with income earning events of taxpayer. The federal commissioner in “FCT v

Stone (2005)” held that the taxpayer was assessable for the prize winnings because it was

connected to her revenue making activities.

The prize winnings for being the best advertisement of the year will be considered.

The amount of $2,000 constitute taxable income under the ordinary concepts of “section 6-5,

ITAA 1997” because it is associated to the income producing activities of the taxpayer.

Answer B:

Where an employee is reimbursed for the expenditure occurred is not regarded as

income. It should be noted that the employee here incurred an expenditure of $500 for

travelling to Sydney was related to work13. But the employee only occurred an amount of

$120 for the whole trip. As a result, the remaining amount of $380 will be regarded as gain to

the employee and the sum will be treated as income in the ordinary conceptions of “section

6-5, ITAA 1997”.

Answer C:

Gains that are simple gifts received by the individual taxpayer should be treated as

having the nature of income. Similarly, the federal court decision in “Hayes v FCT (1956)”

12 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

13 Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013)

11TAXATION LAW

receipt of gift in the form of shares in the company by the previous employer was not treated

as having the character of income14.

The taxpayer here is given a gift of iphone by a client that amounted to $1000.

Mentioning the decision in “Hayes v FCT (1956)” the amount will be considered as gift

which is not a taxable income.

Answer D:

As defined under the “paragraph 118-37 (1), (b), ITAA 1997” if a taxpayer receives

a personal injury claim and they agree to the settlement or the court orders in the favour of

taxpayer, then the taxpayer may receive the compensation payment in the form of periodic or

lump sum15. Such kind of payment are not considered for tax because it does not amount to

income.

In the present case, the taxpayer is given a personal injury compensation of $10,000

suffered from the car accident. Under the provision of “paragraph 118-37 (1), (b), ITAA

1997” the payment of $10,000 are not considered for tax because it does not amount to

income.

Answer E:

The taxpayer here is the owner of shares that were purchased for a cost of $5. While

on 30th June, the taxpayer still owned the shares which is presently trending at greater than

the acquisition price of $7.50. The taxpayer in this circumstances is anticipating to earn

14 Krever, Richard E, Australian Taxation Law Cases 2014

15 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

receipt of gift in the form of shares in the company by the previous employer was not treated

as having the character of income14.

The taxpayer here is given a gift of iphone by a client that amounted to $1000.

Mentioning the decision in “Hayes v FCT (1956)” the amount will be considered as gift

which is not a taxable income.

Answer D:

As defined under the “paragraph 118-37 (1), (b), ITAA 1997” if a taxpayer receives

a personal injury claim and they agree to the settlement or the court orders in the favour of

taxpayer, then the taxpayer may receive the compensation payment in the form of periodic or

lump sum15. Such kind of payment are not considered for tax because it does not amount to

income.

In the present case, the taxpayer is given a personal injury compensation of $10,000

suffered from the car accident. Under the provision of “paragraph 118-37 (1), (b), ITAA

1997” the payment of $10,000 are not considered for tax because it does not amount to

income.

Answer E:

The taxpayer here is the owner of shares that were purchased for a cost of $5. While

on 30th June, the taxpayer still owned the shares which is presently trending at greater than

the acquisition price of $7.50. The taxpayer in this circumstances is anticipating to earn

14 Krever, Richard E, Australian Taxation Law Cases 2014

15 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.