Taxation Law: Personal Income, Deductions, and Cooke & Sherden Case

VerifiedAdded on 2023/04/25

|9

|1821

|73

Case Study

AI Summary

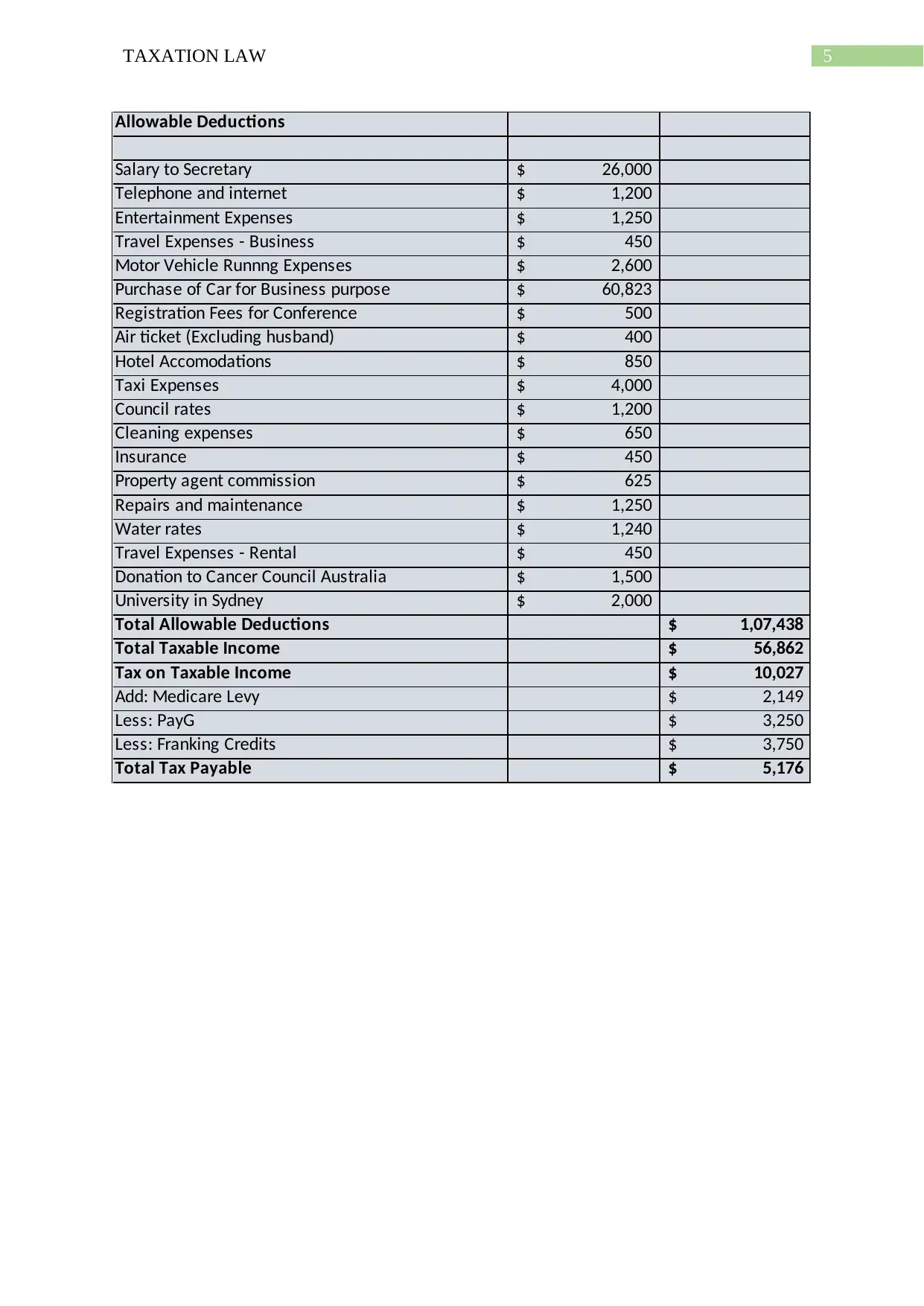

This case study delves into various aspects of taxation law, starting with the assessment of Jane's personal service income, including salary, bonuses, allowances, and awards, alongside deductible expenses. It applies relevant sections of the ITAA 1997 and ITAA 1936 to determine taxable income and allowable deductions, such as donations and business-related expenses. The study also addresses the tax treatment of franked dividends, capital gains/losses, and the application of earnings vs. receipts methods for business income. Furthermore, the case study analyzes the landmark FCT v Cooke and Sherden (1980) case, focusing on the principle that non-convertible, non-cash benefits are not considered ordinary income, referencing similar cases like Payne v FCT (1996). Desklib provides a platform for students to access this and other solved assignments for academic support.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.