Taxation Law Report: Income Tax Calculation and Case Law Analysis

VerifiedAdded on 2023/04/23

|12

|2948

|101

Report

AI Summary

This taxation law report delves into the intricacies of income tax calculations, deductions, and relevant case law. The report begins with an analysis of personal exertion income, ordinary income, and the application of nexus tests, citing key legal precedents like 'Scott v CT' and 'Dean v FCT.' It then examines specific income sources, including salary, bonuses, clothing allowances, and awards, determining their taxability. The report also explores deductible and non-deductible expenses, such as clothing costs and seminar expenses, referencing cases like 'Mansfield v FCT.' Furthermore, it covers accounting methods, including the receipts and earnings methods, and applies them to Jane's taxation practice and investment property income. The report also includes the treatment of dividends, franking credits, and capital gains, referencing 'FCT v McNeil.' The report concludes with a detailed computation of Jane's net income and a case study analysis of 'FCT v Cooke and Sherden (1980)' which highlights the principles applied in determining taxable income from non-cash benefits.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part A:........................................................................................................................................2

Part B:.........................................................................................................................................7

Facts of the Case:...................................................................................................................7

Decisions and main principles applied in judgement:............................................................8

Relevance of Case and likely decision on similar facts:........................................................9

References:...............................................................................................................................10

Table of Contents

Part A:........................................................................................................................................2

Part B:.........................................................................................................................................7

Facts of the Case:...................................................................................................................7

Decisions and main principles applied in judgement:............................................................8

Relevance of Case and likely decision on similar facts:........................................................9

References:...............................................................................................................................10

2TAXATION LAW

Part A:

According to “section 6-1, ITAA 1936”, personal exertion income includes income

that is derived from wages, salaries, gratuities, superannuation allowance etc. by working as

the employee or from business activities. According to “section 6-5, ITAA 1997” most of

the income that is earned by the taxpayer is treated as ordinary income. According to the

taxation commissioner in “Scott v CT (1935)” income should be not be viewed as the word

of art instead the receipts must be determined based on in relation to the ordinary concepts

and usage (Maley, 2018). Jane reports the receipts of gross salary from her employment. The

gross salary amounts to income from personal exertion by Jane under “section 6-1, ITAA

1936”. Citing the court judgement in “Scott v CT (1935)” the gross salary is an ordinary

income based on the ordinary concepts of “section 6-5, ITAA 1997” and it is included for

taxation purpose.

As per the nexus test a sufficient relation should be present between the receipts and

provisions of services namely the reward or the ordinary incidence of service. The court in

“Dean v FCT (1997)” held that receipt of retention payment by employee to continue

employment for twelve more months following the takeover constitute an ordinary income

(Barnes, 2018). The performance bonus of $25,000 received by Jane is treated as taxable

income because the bonus holds adequate nexus with the occupation. She also received from

Milton Hotel her clothing allowance of $4,500. The amount has been included for assessment

as ordinary income under “section 6-5, ITAA 1997” as the sum is received by Jane during

the course of her employment by working in capacity of employee.

According to “Section 8-1, ITAA 1997” expenses occurred in purchasing ordinary clothing

items namely suits are non-deductible expenses. The court in “Mansfield v FCT (1996)”

stated that cost occurred on ordinary articles of apparel is not allowed for deduction

Part A:

According to “section 6-1, ITAA 1936”, personal exertion income includes income

that is derived from wages, salaries, gratuities, superannuation allowance etc. by working as

the employee or from business activities. According to “section 6-5, ITAA 1997” most of

the income that is earned by the taxpayer is treated as ordinary income. According to the

taxation commissioner in “Scott v CT (1935)” income should be not be viewed as the word

of art instead the receipts must be determined based on in relation to the ordinary concepts

and usage (Maley, 2018). Jane reports the receipts of gross salary from her employment. The

gross salary amounts to income from personal exertion by Jane under “section 6-1, ITAA

1936”. Citing the court judgement in “Scott v CT (1935)” the gross salary is an ordinary

income based on the ordinary concepts of “section 6-5, ITAA 1997” and it is included for

taxation purpose.

As per the nexus test a sufficient relation should be present between the receipts and

provisions of services namely the reward or the ordinary incidence of service. The court in

“Dean v FCT (1997)” held that receipt of retention payment by employee to continue

employment for twelve more months following the takeover constitute an ordinary income

(Barnes, 2018). The performance bonus of $25,000 received by Jane is treated as taxable

income because the bonus holds adequate nexus with the occupation. She also received from

Milton Hotel her clothing allowance of $4,500. The amount has been included for assessment

as ordinary income under “section 6-5, ITAA 1997” as the sum is received by Jane during

the course of her employment by working in capacity of employee.

According to “Section 8-1, ITAA 1997” expenses occurred in purchasing ordinary clothing

items namely suits are non-deductible expenses. The court in “Mansfield v FCT (1996)”

stated that cost occurred on ordinary articles of apparel is not allowed for deduction

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

notwithstanding if the expenses are necessary to assure that a proper appearance is

maintained in a particular job (Braithwaite, 2017). The jewellery expense of $7,500 is non-

deductible under “section 8-1, ITAA 1997” for Jane since it is an ordinary item of apparel

which is not related to work.

A simple winning of prize is not held as income unless the receipts forms the part of

taxpayers income generating activities. The court in “FCT v Kelly (1985)” held that receipt

of award for being the fairest player was treated as taxable income since it was related to

employment and use of taxpayer’s skills (Miller & Oats, 2016). The receipt of award by Jane

for being best Australian financial controller is a taxable receipts since it is related to her

profession and work. Jane also received a computer in her award that valued $2,550. Citing

“Cooke and Sherden (1980)” gains which are non-convertible to cash is not held as ordinary

income. The computer received by Jane as an award is a gain which is easily convertible

cash. Therefore, it is included into the taxable income as ordinary income under “section 6-5,

ITAA 1997”.

If the employer gives an employee with the benefit then in such case the benefit will

be treated as non-taxable income for the employee under “section 23 L, ITAA 1936” whereas

for employer the value of benefit given to employee will be considered as FBT. Milton

Hotels Ltd paid Jane’s membership fees (Woellner et al., 2016). The amount will be treated

as non-taxable fringe benefit under “section 23 L, ITAA 1936” for Jane whereas Milton

Hotel Ltd will be liable for fringe benefit tax.

As stated by ATO a taxpayer is permitted to obtain a permissible deduction for

expenses that is occurred for attending seminars, conferences and workshop education that is

associated to work purpose (Awasthi, 2017). Any private part of the expenses must be

excluded that is occurred on trip. Jane with her husband attended a finance conference. The

notwithstanding if the expenses are necessary to assure that a proper appearance is

maintained in a particular job (Braithwaite, 2017). The jewellery expense of $7,500 is non-

deductible under “section 8-1, ITAA 1997” for Jane since it is an ordinary item of apparel

which is not related to work.

A simple winning of prize is not held as income unless the receipts forms the part of

taxpayers income generating activities. The court in “FCT v Kelly (1985)” held that receipt

of award for being the fairest player was treated as taxable income since it was related to

employment and use of taxpayer’s skills (Miller & Oats, 2016). The receipt of award by Jane

for being best Australian financial controller is a taxable receipts since it is related to her

profession and work. Jane also received a computer in her award that valued $2,550. Citing

“Cooke and Sherden (1980)” gains which are non-convertible to cash is not held as ordinary

income. The computer received by Jane as an award is a gain which is easily convertible

cash. Therefore, it is included into the taxable income as ordinary income under “section 6-5,

ITAA 1997”.

If the employer gives an employee with the benefit then in such case the benefit will

be treated as non-taxable income for the employee under “section 23 L, ITAA 1936” whereas

for employer the value of benefit given to employee will be considered as FBT. Milton

Hotels Ltd paid Jane’s membership fees (Woellner et al., 2016). The amount will be treated

as non-taxable fringe benefit under “section 23 L, ITAA 1936” for Jane whereas Milton

Hotel Ltd will be liable for fringe benefit tax.

As stated by ATO a taxpayer is permitted to obtain a permissible deduction for

expenses that is occurred for attending seminars, conferences and workshop education that is

associated to work purpose (Awasthi, 2017). Any private part of the expenses must be

excluded that is occurred on trip. Jane with her husband attended a finance conference. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

expenses consisted of registration, air fares, accommodation and visiting historical places.

Jane is permitted to claim deduction for the registration, accommodation and air fares for her

portion while the visit to historical places and air fare for husband is non-deductible expense

because it is a private expense.

The legislative response of “section 25-100, ITAA 1997” allows a taxpayer to obtain

deduction for expenses that is occurred relating to travel between two related work places

(Picciotto, 2015). The travel must be related directly amid the work place where the revenue

generating activities are carried on and none being taxpayers home. The court in “FCT v

Wiener”, held that the taxpayer was the teacher and her employment required her to travel

five different schools for teaching purpose (Schmalbeck et al., 2015). The commissioner

found that work duties of taxpayer was itinerant in nature and travel formed the part of her

employment duties, therefore a deduction was allowed. Travel expenditure reported by Jane

include traveling from Milton Hotel to her taxation practice place at Kingsford where the

income producing activities were performed. Therefore, a deduction is permitted for travel

under “section 8-1, ITAA 1997”.

According to “taxation ruling of TR 98/1” receipts and earnings basis of accounting

are two commonly used method for determining income during a relevant year. According to

“section 6-5 (4), ITAA 1997” income is derived as soon as it is received under receipts

method (Schenk, 2017). Under the earnings method income is derived as soon as it is earned.

The court in “Barratt v FCT (1992)” held that where payment comprises of extending the

credit and collection of debts then it is appropriate to follow the earnings method of

accounting.

Accordingly in case of Jane receipts from her taxation practice involved both the

billed and unbilled sum of $45,000 and $5,000. Furthermore, she also reported receipts from

expenses consisted of registration, air fares, accommodation and visiting historical places.

Jane is permitted to claim deduction for the registration, accommodation and air fares for her

portion while the visit to historical places and air fare for husband is non-deductible expense

because it is a private expense.

The legislative response of “section 25-100, ITAA 1997” allows a taxpayer to obtain

deduction for expenses that is occurred relating to travel between two related work places

(Picciotto, 2015). The travel must be related directly amid the work place where the revenue

generating activities are carried on and none being taxpayers home. The court in “FCT v

Wiener”, held that the taxpayer was the teacher and her employment required her to travel

five different schools for teaching purpose (Schmalbeck et al., 2015). The commissioner

found that work duties of taxpayer was itinerant in nature and travel formed the part of her

employment duties, therefore a deduction was allowed. Travel expenditure reported by Jane

include traveling from Milton Hotel to her taxation practice place at Kingsford where the

income producing activities were performed. Therefore, a deduction is permitted for travel

under “section 8-1, ITAA 1997”.

According to “taxation ruling of TR 98/1” receipts and earnings basis of accounting

are two commonly used method for determining income during a relevant year. According to

“section 6-5 (4), ITAA 1997” income is derived as soon as it is received under receipts

method (Schenk, 2017). Under the earnings method income is derived as soon as it is earned.

The court in “Barratt v FCT (1992)” held that where payment comprises of extending the

credit and collection of debts then it is appropriate to follow the earnings method of

accounting.

Accordingly in case of Jane receipts from her taxation practice involved both the

billed and unbilled sum of $45,000 and $5,000. Furthermore, she also reported receipts from

5TAXATION LAW

the investment property where she derived rent. The rental property receipts constituted

ordinary income and represented the concept of regular flow. Quoting the judgement of

“FCT v Barratt (1992)” the earnings method of accounting is appropriate method for

taxation purpose because it would help in providing a true reflex of Jane’s taxation practice

and investment property income. The income obtained from her taxation business and

investment property is included for taxation purpose on the basis of earnings method because

the income was derived as soon as it is earned by Jane in the relevant income year (Murphy

& Higgins, 2016). A point of derivation happened for Jane for both the taxation practice and

rental investment property when a recoverable debt was created by her for unbilled and

accrued value of business fees and rental receipts. While the expenses incurred for both

taxation practice business and investment property is allowed for deduction under “section 8-

1, ITAA 1997” as the expenses were incurred while generating taxable income.

Jane reports income from dividends. The dividends is considered for taxable purpose

under “section 44 (1) of the ITAA 1936”, while the franking credits attached with dividends

is included for taxable purpose under “section 207-20(1), ITAA 1997” as statutory income

(Deutsch, 2018). An income tax offset for the franking credits can be claimed by Jane to

reduce her tax liability.

Jane reported capital gains from the disposal of CBA share. Quoting “FCT v

McNeil” the capital gains obtained from CBA shares is treated as ordinary income for taxable

purpose (Jover-Ledesma, 2014). Whereas the disposal of BHP shares resulted in capital loss.

The capital gains from BHP shares is offset against the capital gains made from CBA shares.

The donation to Sydney University and Cancer Council Australia is a deductible gift

recipients, therefore a deduction for the same has been claimed.

the investment property where she derived rent. The rental property receipts constituted

ordinary income and represented the concept of regular flow. Quoting the judgement of

“FCT v Barratt (1992)” the earnings method of accounting is appropriate method for

taxation purpose because it would help in providing a true reflex of Jane’s taxation practice

and investment property income. The income obtained from her taxation business and

investment property is included for taxation purpose on the basis of earnings method because

the income was derived as soon as it is earned by Jane in the relevant income year (Murphy

& Higgins, 2016). A point of derivation happened for Jane for both the taxation practice and

rental investment property when a recoverable debt was created by her for unbilled and

accrued value of business fees and rental receipts. While the expenses incurred for both

taxation practice business and investment property is allowed for deduction under “section 8-

1, ITAA 1997” as the expenses were incurred while generating taxable income.

Jane reports income from dividends. The dividends is considered for taxable purpose

under “section 44 (1) of the ITAA 1936”, while the franking credits attached with dividends

is included for taxable purpose under “section 207-20(1), ITAA 1997” as statutory income

(Deutsch, 2018). An income tax offset for the franking credits can be claimed by Jane to

reduce her tax liability.

Jane reported capital gains from the disposal of CBA share. Quoting “FCT v

McNeil” the capital gains obtained from CBA shares is treated as ordinary income for taxable

purpose (Jover-Ledesma, 2014). Whereas the disposal of BHP shares resulted in capital loss.

The capital gains from BHP shares is offset against the capital gains made from CBA shares.

The donation to Sydney University and Cancer Council Australia is a deductible gift

recipients, therefore a deduction for the same has been claimed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

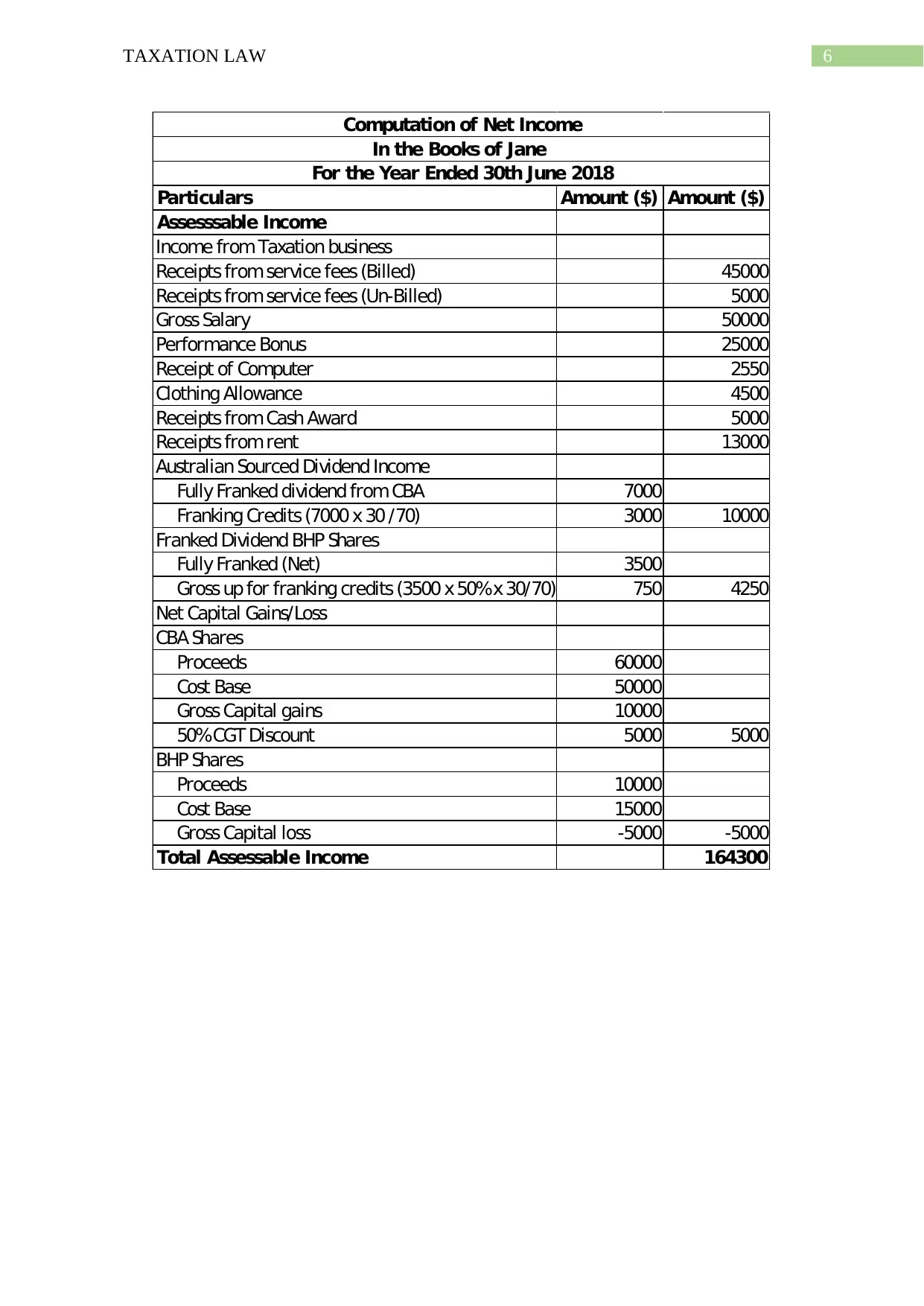

Particulars Amount ($) Amount ($)

Assesssable Income

Income from Taxation business

Receipts from service fees (Billed) 45000

Receipts from service fees (Un-Billed) 5000

Gross Salary 50000

Performance Bonus 25000

Receipt of Computer 2550

Clothing Allowance 4500

Receipts from Cash Award 5000

Receipts from rent 13000

Australian Sourced Dividend Income

Fully Franked dividend from CBA 7000

Franking Credits (7000 x 30 /70) 3000 10000

Franked Dividend BHP Shares

Fully Franked (Net) 3500

Gross up for franking credits (3500 x 50%x 30/70) 750 4250

Net Capital Gains/Loss

CBA Shares

Proceeds 60000

Cost Base 50000

Gross Capital gains 10000

50%CGT Discount 5000 5000

BHP Shares

Proceeds 10000

Cost Base 15000

Gross Capital loss -5000 -5000

Total Assessable Income 164300

Computation of Net Income

In the Books of Jane

For the Year Ended 30th June 2018

Particulars Amount ($) Amount ($)

Assesssable Income

Income from Taxation business

Receipts from service fees (Billed) 45000

Receipts from service fees (Un-Billed) 5000

Gross Salary 50000

Performance Bonus 25000

Receipt of Computer 2550

Clothing Allowance 4500

Receipts from Cash Award 5000

Receipts from rent 13000

Australian Sourced Dividend Income

Fully Franked dividend from CBA 7000

Franking Credits (7000 x 30 /70) 3000 10000

Franked Dividend BHP Shares

Fully Franked (Net) 3500

Gross up for franking credits (3500 x 50%x 30/70) 750 4250

Net Capital Gains/Loss

CBA Shares

Proceeds 60000

Cost Base 50000

Gross Capital gains 10000

50%CGT Discount 5000 5000

BHP Shares

Proceeds 10000

Cost Base 15000

Gross Capital loss -5000 -5000

Total Assessable Income 164300

Computation of Net Income

In the Books of Jane

For the Year Ended 30th June 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

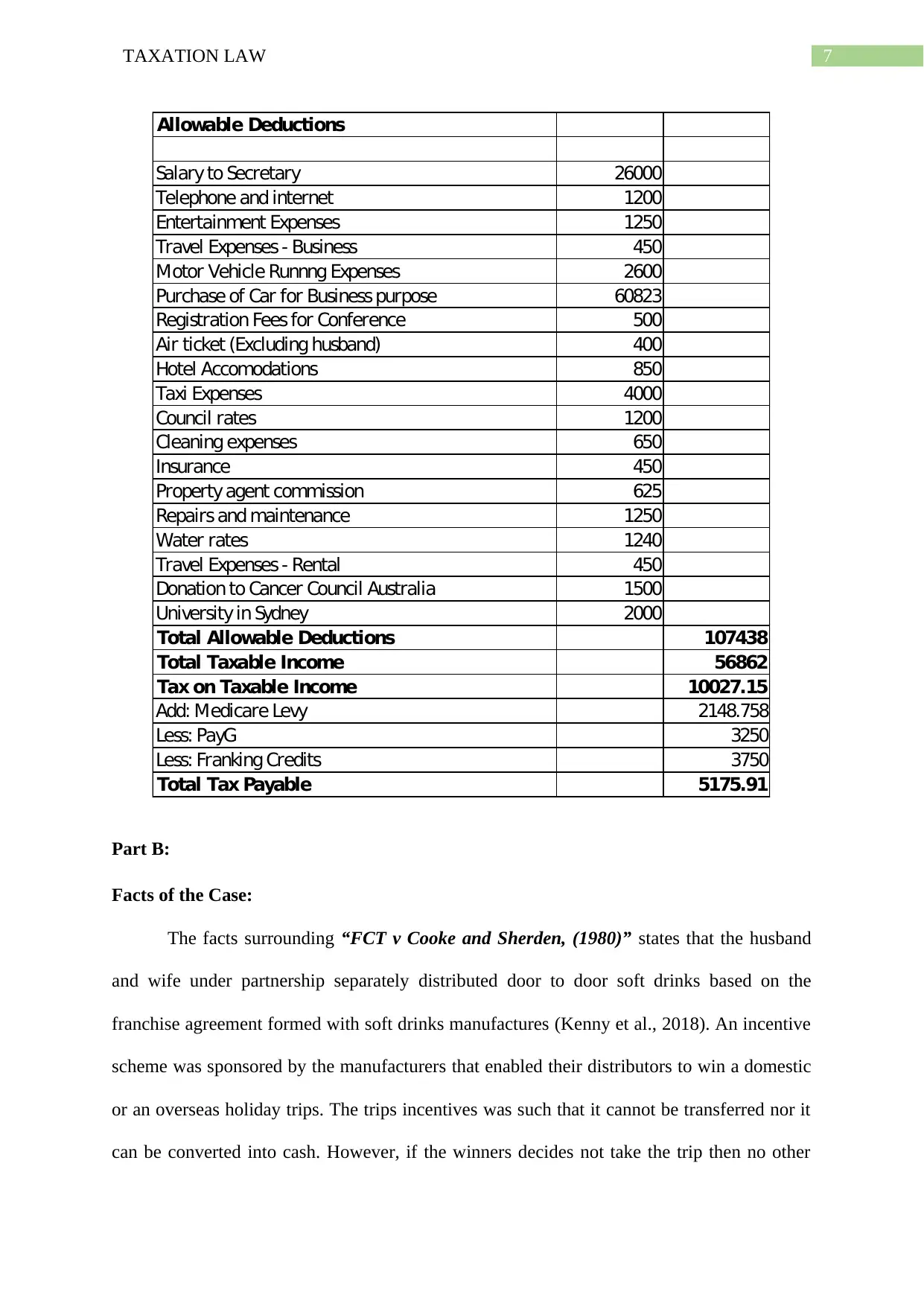

Allowable Deductions

Salary to Secretary 26000

Telephone and internet 1200

Entertainment Expenses 1250

Travel Expenses - Business 450

Motor Vehicle Runnng Expenses 2600

Purchase of Car for Business purpose 60823

Registration Fees for Conference 500

Air ticket (Excluding husband) 400

Hotel Accomodations 850

Taxi Expenses 4000

Council rates 1200

Cleaning expenses 650

Insurance 450

Property agent commission 625

Repairs and maintenance 1250

Water rates 1240

Travel Expenses - Rental 450

Donation to Cancer Council Australia 1500

University in Sydney 2000

Total Allowable Deductions 107438

Total Taxable Income 56862

Tax on Taxable Income 10027.15

Add: Medicare Levy 2148.758

Less: PayG 3250

Less: Franking Credits 3750

Total Tax Payable 5175.91

Part B:

Facts of the Case:

The facts surrounding “FCT v Cooke and Sherden, (1980)” states that the husband

and wife under partnership separately distributed door to door soft drinks based on the

franchise agreement formed with soft drinks manufactures (Kenny et al., 2018). An incentive

scheme was sponsored by the manufacturers that enabled their distributors to win a domestic

or an overseas holiday trips. The trips incentives was such that it cannot be transferred nor it

can be converted into cash. However, if the winners decides not take the trip then no other

Allowable Deductions

Salary to Secretary 26000

Telephone and internet 1200

Entertainment Expenses 1250

Travel Expenses - Business 450

Motor Vehicle Runnng Expenses 2600

Purchase of Car for Business purpose 60823

Registration Fees for Conference 500

Air ticket (Excluding husband) 400

Hotel Accomodations 850

Taxi Expenses 4000

Council rates 1200

Cleaning expenses 650

Insurance 450

Property agent commission 625

Repairs and maintenance 1250

Water rates 1240

Travel Expenses - Rental 450

Donation to Cancer Council Australia 1500

University in Sydney 2000

Total Allowable Deductions 107438

Total Taxable Income 56862

Tax on Taxable Income 10027.15

Add: Medicare Levy 2148.758

Less: PayG 3250

Less: Franking Credits 3750

Total Tax Payable 5175.91

Part B:

Facts of the Case:

The facts surrounding “FCT v Cooke and Sherden, (1980)” states that the husband

and wife under partnership separately distributed door to door soft drinks based on the

franchise agreement formed with soft drinks manufactures (Kenny et al., 2018). An incentive

scheme was sponsored by the manufacturers that enabled their distributors to win a domestic

or an overseas holiday trips. The trips incentives was such that it cannot be transferred nor it

can be converted into cash. However, if the winners decides not take the trip then no other

8TAXATION LAW

benefits was given to the distributors. The taxpayer here won several holiday trips during the

past number of years. The commissioner of taxation considered the amount of trips relevant

to the taxable income for the taxpayers. The court however in its unanimous decisions stated

that the trips cannot be considered as taxable income.

For taxation purpose, an argument was raised which stated that the value of overseas

holiday trips won by the taxpayer will be considered as taxable income under “section 25 (1),

ITAA 1997” as the ordinary income (McCouat, 2018). The court decided that the holiday

trips was received by the taxpayers as the outcome for providing services to the

manufacturers and on applying “section 26 (e)” the holiday trips may be treated as taxable

income.

Decisions and main principles applied in judgement:

As per “section 25 (1)” the court held that gratuitous benefits received in kind which

is non-convertible to cash is non-assessable ordinary income. As per the law court gifts or

benefits of such type is only treated for taxation purpose given the benefit is acquired in cash

or can be converted to cash (Sadiq et al., 2018). The court also stated that it was regardless

whether the expenses that might have incurred given the taxpayer had to pay for the trips and

the same cannot be treated as ordinary income.

As per the law court it may not often happen that the benefit that is to be enjoyed by

the taxpayers cannot be converted into pecuniary account, if the benefit is surrendered or the

same is used in acquire some sort of right of commodity (Taylor et al., 2018). Where the

claims of benefit is non-convertible to cash, cautious evaluation should be made to determine

if any type of indirect attempt of obtaining the benefit is made such as money or money’s

worth. By citing the example of “Abott v Philbin (1961)” the commissioner stated where the

benefits was given to the distributors. The taxpayer here won several holiday trips during the

past number of years. The commissioner of taxation considered the amount of trips relevant

to the taxable income for the taxpayers. The court however in its unanimous decisions stated

that the trips cannot be considered as taxable income.

For taxation purpose, an argument was raised which stated that the value of overseas

holiday trips won by the taxpayer will be considered as taxable income under “section 25 (1),

ITAA 1997” as the ordinary income (McCouat, 2018). The court decided that the holiday

trips was received by the taxpayers as the outcome for providing services to the

manufacturers and on applying “section 26 (e)” the holiday trips may be treated as taxable

income.

Decisions and main principles applied in judgement:

As per “section 25 (1)” the court held that gratuitous benefits received in kind which

is non-convertible to cash is non-assessable ordinary income. As per the law court gifts or

benefits of such type is only treated for taxation purpose given the benefit is acquired in cash

or can be converted to cash (Sadiq et al., 2018). The court also stated that it was regardless

whether the expenses that might have incurred given the taxpayer had to pay for the trips and

the same cannot be treated as ordinary income.

As per the law court it may not often happen that the benefit that is to be enjoyed by

the taxpayers cannot be converted into pecuniary account, if the benefit is surrendered or the

same is used in acquire some sort of right of commodity (Taylor et al., 2018). Where the

claims of benefit is non-convertible to cash, cautious evaluation should be made to determine

if any type of indirect attempt of obtaining the benefit is made such as money or money’s

worth. By citing the example of “Abott v Philbin (1961)” the commissioner stated where the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

option was not provided however the right for calling of shares was held as having the worth

of money because the same can be used as a means of borrowing money.

Referring to “section 26 (e)”, the commissioner stated that no kind of services was

rendered to the manufacturers by the taxpayers. Rather the taxpayer distributed soft drinks

and were conducting their business activities for their personal benefit. Therefore, the benefit

of free holiday trips could be treated as income under the ordinary concepts as it was non-

convertible into cash.

Relevance of Case and likely decision on similar facts:

The case of “FCT v Cooke and Sherden, (1980)” is still treated as relevant case since

the verdict announced resulted in the enactment of “section 21A” (Sadiq et al., 2018). As per

“section 21A” non-cash business benefits received as a result of business relation which is

non-convertible to cash will be treated as convertible into money and such benefits will be

bought under the purview of taxable income, provided such benefits is having income

character.

An identical verdict was made in “FCT v Payne (1996)” where the frequent flyer

points was not held as ordinary income because it was non-convertible to money. The points

were neither transferable nor convertible and was subjected to cancellation if it is sold.

option was not provided however the right for calling of shares was held as having the worth

of money because the same can be used as a means of borrowing money.

Referring to “section 26 (e)”, the commissioner stated that no kind of services was

rendered to the manufacturers by the taxpayers. Rather the taxpayer distributed soft drinks

and were conducting their business activities for their personal benefit. Therefore, the benefit

of free holiday trips could be treated as income under the ordinary concepts as it was non-

convertible into cash.

Relevance of Case and likely decision on similar facts:

The case of “FCT v Cooke and Sherden, (1980)” is still treated as relevant case since

the verdict announced resulted in the enactment of “section 21A” (Sadiq et al., 2018). As per

“section 21A” non-cash business benefits received as a result of business relation which is

non-convertible to cash will be treated as convertible into money and such benefits will be

bought under the purview of taxable income, provided such benefits is having income

character.

An identical verdict was made in “FCT v Payne (1996)” where the frequent flyer

points was not held as ordinary income because it was non-convertible to money. The points

were neither transferable nor convertible and was subjected to cancellation if it is sold.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Awasthi, A. (2017). Transformation of Tax Laws: A Global Perspective. Intertax, 45(2), 175-

181.

Barnes, J., (2018). On the ground and on tap—law reform, Australian style. The Theory and

Practice of Legislation, pp.1-32.

Braithwaite, V. (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

DEUTSCH, R. (2018). Australian tax handbook 2018. [Place of publication not identified]:

THOMSON REUTERS AUSTRALIA.

Jover-Ledesma, G. (2014). Principles of business taxation 2015. [Place of publication not

identified]: Cch Incorporated.

Kenny, P., Blissenden, M., & Villios, S. (2018). Australian Tax 2018.

Maley, M. N. (2018). Australian Taxation Office Guidance on the Diverted Profits Tax.

McCouat, P. (2018). Australian master GST guide 2018.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Murphy, K. E., & Higgins, M. (2016). Concepts in Federal Taxation 2017. Cengage

Learning.

Picciotto, S. (2015). Indeterminacy, complexity, technocracy and the reform of international

corporate taxation. Social & Legal Studies, 24(2), 165-184.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., & Obst, W. et al.

(2018). Principles of taxation law 2018.

References:

Awasthi, A. (2017). Transformation of Tax Laws: A Global Perspective. Intertax, 45(2), 175-

181.

Barnes, J., (2018). On the ground and on tap—law reform, Australian style. The Theory and

Practice of Legislation, pp.1-32.

Braithwaite, V. (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

DEUTSCH, R. (2018). Australian tax handbook 2018. [Place of publication not identified]:

THOMSON REUTERS AUSTRALIA.

Jover-Ledesma, G. (2014). Principles of business taxation 2015. [Place of publication not

identified]: Cch Incorporated.

Kenny, P., Blissenden, M., & Villios, S. (2018). Australian Tax 2018.

Maley, M. N. (2018). Australian Taxation Office Guidance on the Diverted Profits Tax.

McCouat, P. (2018). Australian master GST guide 2018.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Murphy, K. E., & Higgins, M. (2016). Concepts in Federal Taxation 2017. Cengage

Learning.

Picciotto, S. (2015). Indeterminacy, complexity, technocracy and the reform of international

corporate taxation. Social & Legal Studies, 24(2), 165-184.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., & Obst, W. et al.

(2018). Principles of taxation law 2018.

11TAXATION LAW

Schenk, D. H. (2017). Federal Taxation of S Corporations. Law Journal Press.

Schmalbeck, R., Zelenak, L., & Lawsky, S. B. (2015). Federal Income Taxation. Wolters

Kluwer Law & Business.

Taylor, C., Walpole, M., Burton, M., Ciro, T., & Murray, I. (2018). Understanding taxation

law 2018.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

Schenk, D. H. (2017). Federal Taxation of S Corporations. Law Journal Press.

Schmalbeck, R., Zelenak, L., & Lawsky, S. B. (2015). Federal Income Taxation. Wolters

Kluwer Law & Business.

Taylor, C., Walpole, M., Burton, M., Ciro, T., & Murray, I. (2018). Understanding taxation

law 2018.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.