Taxation Law Assignment: Income Tax Calculation for Sarah (2017/18)

VerifiedAdded on 2023/04/25

|10

|2233

|475

Homework Assignment

AI Summary

This assignment analyzes Sarah's tax liabilities for the 2017/18 income year, focusing on her income from employment and teaching, and her eligibility for various deductions. The solution examines the application of relevant sections of the ITAA 1997, including those related to assessable income, home office expenses, depreciation, membership fees, travel expenses, and self-education expenses. The assignment assesses whether Sarah can claim deductions for expenses such as home office costs, design equipment, and travel to client premises, while also considering the tax implications of selling personal assets. The solution includes a detailed computation of Sarah's taxable income and net tax payable, incorporating relevant case law and tax rulings to support the analysis. The assignment concludes with a summary of the findings, outlining Sarah's tax obligations and the deductions she is entitled to claim.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Headings:................................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Headings:................................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................8

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

Headings:

This is a taxation law problems related to the determination of the taxable income and

tax treatment of items occurred.

Issues:

The issues involved in the case is whether the receipts derived by the taxpayer is

liable for taxation within the ordinary concepts of “section 6-5, ITAA 1997”. Whether the

taxpayer is eligible for claiming allowable deduction for expenses occurred under the positive

limbs of “section 8-1, ITAA 1997”.

Rule:

“Section 6, ITAA 1936” states that income from personal exertion refers to the

income covering salaries, wages, allowances, bonuses etc. received working as employee for

the services rendered or any business proceeds derived from carrying on the business

activities. As per “section 6-5, ITAA 1997” regularly most of the income that is earned by the

taxpayer is held as ordinary income1. The commissioner in “Scott v CT (1935)” held that

income should not be viewed as an art and requires the necessary application of principles to

treat the receipts as income within the ordinary concepts and usage.

As per “taxation ruling of TR 93/30” where a taxpayer uses the home as their place of

business a relevant portion of occupancy and running expenses are allowed for deductions.

As held in “Swinford v FCT (1984) 15 ATR 1154” the commissioner allowed deduction to

the self-employed scriptwriter for the portion of flat rent where the taxpayer used the room of

her flat for writing scripts and did not any other separate business premises2.

1 Barkoczy, Stephen, Foundations Of Taxation Law 2014.

2 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business Taxation.

Answer to question 1:

Headings:

This is a taxation law problems related to the determination of the taxable income and

tax treatment of items occurred.

Issues:

The issues involved in the case is whether the receipts derived by the taxpayer is

liable for taxation within the ordinary concepts of “section 6-5, ITAA 1997”. Whether the

taxpayer is eligible for claiming allowable deduction for expenses occurred under the positive

limbs of “section 8-1, ITAA 1997”.

Rule:

“Section 6, ITAA 1936” states that income from personal exertion refers to the

income covering salaries, wages, allowances, bonuses etc. received working as employee for

the services rendered or any business proceeds derived from carrying on the business

activities. As per “section 6-5, ITAA 1997” regularly most of the income that is earned by the

taxpayer is held as ordinary income1. The commissioner in “Scott v CT (1935)” held that

income should not be viewed as an art and requires the necessary application of principles to

treat the receipts as income within the ordinary concepts and usage.

As per “taxation ruling of TR 93/30” where a taxpayer uses the home as their place of

business a relevant portion of occupancy and running expenses are allowed for deductions.

As held in “Swinford v FCT (1984) 15 ATR 1154” the commissioner allowed deduction to

the self-employed scriptwriter for the portion of flat rent where the taxpayer used the room of

her flat for writing scripts and did not any other separate business premises2.

1 Barkoczy, Stephen, Foundations Of Taxation Law 2014.

2 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business Taxation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

As per “section 40-25 (1), ITAA 1997” a taxpayer is allowed to claim deduction for

the amount that is equal to the decline in value for the income year of the depreciating asset

that is held during the year. Accordingly, under “section 40-25 (2), ITAA 1997” deduction

can be lowered where the decline in value of the assets is attributable to both private and

taxable purpose3. As per “section 25-55, ITAA 1997” a deduction is allowed to the taxpayer

for payments made relating to membership of trade, business or professional association.

According to the “section 25-100, ITAA 1997”, a taxpayer is allowed to claim

deduction for the cost of travel between the workplaces. The travel should be directly

associated between two places where the income generating activities are conducted with

neither of the place is taxpayers home. This includes the traveling in the course of work such

as travelling as salesman, self-employed builder to provide quotes. As held in “FCT v Wiener

(1978) ATC 4006” the taxation commissioner permitted deduction to the taxpayer for travel

between schools and also the travel amid home and the first and last school attended by the

taxpayer each day4. The court noticed that the employment of taxpayer was itinerant and

travelling was done to perform duties.

On the other hand, travel between home and a person’s normal residence is non-

deductible. The court in “FCT v Payne (2001) ATC 4027” denied the taxpayer with the

deduction relating to the cost of travelling between the home and his employment place5. The

court held that no deduction is allowed under section 8-1, for travelling between two place

work places.

3 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury Publishing, 2016.

4 Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013).

5 Eliot, George, The Mill On The Floss (Open Road Integrated Media, 2016).

As per “section 40-25 (1), ITAA 1997” a taxpayer is allowed to claim deduction for

the amount that is equal to the decline in value for the income year of the depreciating asset

that is held during the year. Accordingly, under “section 40-25 (2), ITAA 1997” deduction

can be lowered where the decline in value of the assets is attributable to both private and

taxable purpose3. As per “section 25-55, ITAA 1997” a deduction is allowed to the taxpayer

for payments made relating to membership of trade, business or professional association.

According to the “section 25-100, ITAA 1997”, a taxpayer is allowed to claim

deduction for the cost of travel between the workplaces. The travel should be directly

associated between two places where the income generating activities are conducted with

neither of the place is taxpayers home. This includes the traveling in the course of work such

as travelling as salesman, self-employed builder to provide quotes. As held in “FCT v Wiener

(1978) ATC 4006” the taxation commissioner permitted deduction to the taxpayer for travel

between schools and also the travel amid home and the first and last school attended by the

taxpayer each day4. The court noticed that the employment of taxpayer was itinerant and

travelling was done to perform duties.

On the other hand, travel between home and a person’s normal residence is non-

deductible. The court in “FCT v Payne (2001) ATC 4027” denied the taxpayer with the

deduction relating to the cost of travelling between the home and his employment place5. The

court held that no deduction is allowed under section 8-1, for travelling between two place

work places.

3 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury Publishing, 2016.

4 Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013).

5 Eliot, George, The Mill On The Floss (Open Road Integrated Media, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The costs that is occurred on the ordinary items of clothing such as suits, is not

allowed for deduction under section 8-1. As held in “Mansfield v FCT 96 ATC 4001” the

court denied the deduction to the taxpayer for the cost incurred on the ordinary articles of

apparel, irrespective that the expenses were necessary in maintaining a suitable appearance

for a particular job or profession6.

Self-education expenses are usually allowed for deduction where the expenses

occurred by the taxpayer are for maintaining or increasing the skills of taxpayers in the

occupation in which one is currently engaged, particularly where expenses increases the

prospects and promotion of greater income. Whereas, a deduction is denied to the taxpayer

for the self-education expenses in which the taxpayer is not currently engaged in since the

nexus test is not satisfied.

A CGT event A1 happens under “section 104-10 (1)” when the taxpayer disposes a

CGT assets. Personal use assets are defined under “section 108-20(2)” that are mainly kept

or used for the personal enjoyment7. According to the “section 108-25 (2), ITAA 1997” the

set of personal use assets is considered as the single personal use asset and every disposal or

sale is the part of that asset.

Application:

As evident from the case study Sarah worked as the full time interior design

consultant and derived a gross salary of $80,000 per annum. Citing “Section 6, ITAA 1936”

the salary received by Sarah from employment is an income from personal exertion8.

Denoting the decision made in “Scott v CT (1935)” the gross salary of Sarah received from

6 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014).

7 Krever, Richard E, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013).

8 Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian Taxation Law (CCH Australia, 2013).

The costs that is occurred on the ordinary items of clothing such as suits, is not

allowed for deduction under section 8-1. As held in “Mansfield v FCT 96 ATC 4001” the

court denied the deduction to the taxpayer for the cost incurred on the ordinary articles of

apparel, irrespective that the expenses were necessary in maintaining a suitable appearance

for a particular job or profession6.

Self-education expenses are usually allowed for deduction where the expenses

occurred by the taxpayer are for maintaining or increasing the skills of taxpayers in the

occupation in which one is currently engaged, particularly where expenses increases the

prospects and promotion of greater income. Whereas, a deduction is denied to the taxpayer

for the self-education expenses in which the taxpayer is not currently engaged in since the

nexus test is not satisfied.

A CGT event A1 happens under “section 104-10 (1)” when the taxpayer disposes a

CGT assets. Personal use assets are defined under “section 108-20(2)” that are mainly kept

or used for the personal enjoyment7. According to the “section 108-25 (2), ITAA 1997” the

set of personal use assets is considered as the single personal use asset and every disposal or

sale is the part of that asset.

Application:

As evident from the case study Sarah worked as the full time interior design

consultant and derived a gross salary of $80,000 per annum. Citing “Section 6, ITAA 1936”

the salary received by Sarah from employment is an income from personal exertion8.

Denoting the decision made in “Scott v CT (1935)” the gross salary of Sarah received from

6 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014).

7 Krever, Richard E, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013).

8 Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian Taxation Law (CCH Australia, 2013).

5TAXATION LAW

Design Co Ltd and teaching in community college constitute ordinary income within the

ordinary concepts of “section 6-5, ITAA 1997” which attracts tax liability.

Later it is noticed Design CoLtd does not provided Sarah with an office as a result she

used her house as her home office base for consulting work. With reference to “Swinford v

FCT (1984) 15 ATR 1154” Sarah can claim both the running and occupancy expenses

occurred in the form of interest on loan, insurance and electricity for her home office up to

60% of the home office expenses for her 20% floor space of the entire house.

Sarah also bought a new piece of design equipment for home office purpose and used

60% of the time for business purpose while remaining 40% was dedicated for personal

purpose. With reference to “section 40-25 (1), ITAA 1997” Sarah is allowed to claim

deduction for the amount that is equal to the decline in value for the income year of the new

design equipment that is held by her during the year9. Within the meaning of “section 40-25

(2), ITAA 1997” Sarah is only allowed to claim 60% of the decline in value of new

reassignment that is attributed for her work purpose. Meanwhile, Sarah can also claim

deduction under “section 25-55, ITAA 1997” for payments made relating to membership and

subscriptions for her interior designs.

Sarah also report an expense on travelling to the client premises for onsite advice and

building inspection. Within “section 25-100, ITAA 1997”, the travellig made by Sarah was in

the course of work10. Citing “FCT v Wiener (1978) ATC 4006” Sarah is allowed to claim

deduction for the cost of travel incurred for visiting client for on-site advice because it is

incurred for work purpose.

9 Sadiq, Kerrie et al, Principles Of Taxation Law (2014).

10 Tax, Law And Development (Edward Elgar, 2013).

Design Co Ltd and teaching in community college constitute ordinary income within the

ordinary concepts of “section 6-5, ITAA 1997” which attracts tax liability.

Later it is noticed Design CoLtd does not provided Sarah with an office as a result she

used her house as her home office base for consulting work. With reference to “Swinford v

FCT (1984) 15 ATR 1154” Sarah can claim both the running and occupancy expenses

occurred in the form of interest on loan, insurance and electricity for her home office up to

60% of the home office expenses for her 20% floor space of the entire house.

Sarah also bought a new piece of design equipment for home office purpose and used

60% of the time for business purpose while remaining 40% was dedicated for personal

purpose. With reference to “section 40-25 (1), ITAA 1997” Sarah is allowed to claim

deduction for the amount that is equal to the decline in value for the income year of the new

design equipment that is held by her during the year9. Within the meaning of “section 40-25

(2), ITAA 1997” Sarah is only allowed to claim 60% of the decline in value of new

reassignment that is attributed for her work purpose. Meanwhile, Sarah can also claim

deduction under “section 25-55, ITAA 1997” for payments made relating to membership and

subscriptions for her interior designs.

Sarah also report an expense on travelling to the client premises for onsite advice and

building inspection. Within “section 25-100, ITAA 1997”, the travellig made by Sarah was in

the course of work10. Citing “FCT v Wiener (1978) ATC 4006” Sarah is allowed to claim

deduction for the cost of travel incurred for visiting client for on-site advice because it is

incurred for work purpose.

9 Sadiq, Kerrie et al, Principles Of Taxation Law (2014).

10 Tax, Law And Development (Edward Elgar, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

The clothing expenses incurred by Sarah is non-deductible under “section 8-1, ITAA

1997”. Citing the “Mansfield v FCT 96 ATC 4001” Sarah cannot deduction expenses for

ordinary articles of apparel, irrespective that the expenses were necessary in maintaining a

suitable appearance for a particular profession.

Sarah also incurred travelling expenses for travelling from her home to art classes at

community college. With reference to “FCT v Payne (2001) ATC 4027” no deduction will be

allowed to Sarah under “section 8-1, ITAA 1997” for travelling between the home and her

community college as it is a private travel11.

Sarah later reports self-education expenses on MBA course fees and textbooks. The

self-education course undertaken by Sarah is not related to the work or profession in which

she is currently employed12. Therefore, she will be denied deduction for self-education

expenses since the nexus test is not satisfied.

The disposal of bedroom furniture set by Sarah constitutes “CGT event A1” under

“section 104-10 (1)”. Based on “section 108-25 (2), ITAA 1997” the disposal of personal use

assets made by Sarah is in single set and every disposal that is made by Sarah represents the

part of asset. However, the asset was bought in January and only held for six months before it

was sold by Sarah. Therefore, no discounting method will be applicable while computing

capital gains for Sarah.

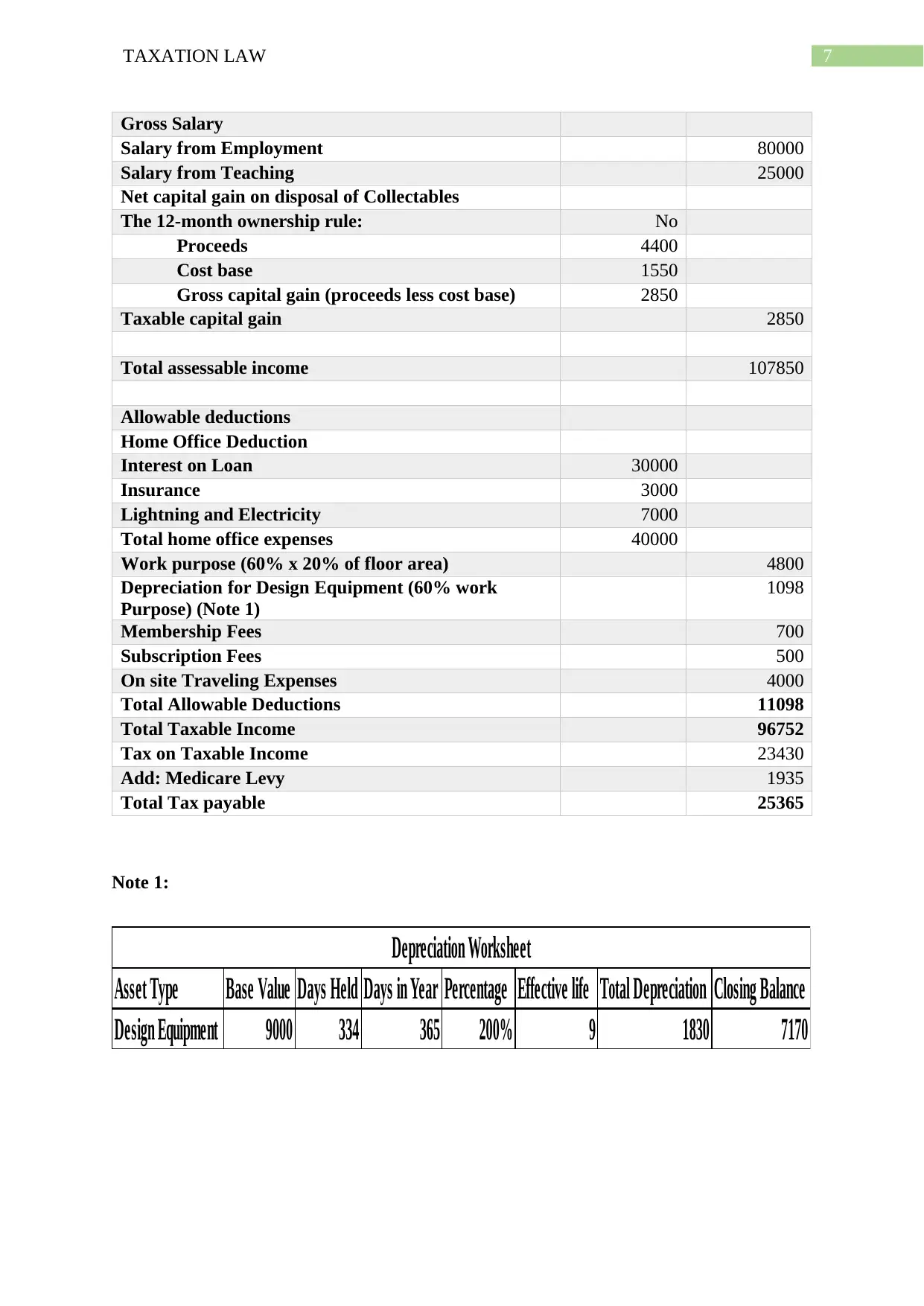

Computation of Taxable Income and Net Tax Payable

In the Books of Sarah

For the Year ended 2017/18

Particulars Amount

($AUD)

Amount

($AUD)

Assessable Income

11 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

12 Woellner, R. H, Australian Taxation Law 2012 (CCH Australia, 2013).

The clothing expenses incurred by Sarah is non-deductible under “section 8-1, ITAA

1997”. Citing the “Mansfield v FCT 96 ATC 4001” Sarah cannot deduction expenses for

ordinary articles of apparel, irrespective that the expenses were necessary in maintaining a

suitable appearance for a particular profession.

Sarah also incurred travelling expenses for travelling from her home to art classes at

community college. With reference to “FCT v Payne (2001) ATC 4027” no deduction will be

allowed to Sarah under “section 8-1, ITAA 1997” for travelling between the home and her

community college as it is a private travel11.

Sarah later reports self-education expenses on MBA course fees and textbooks. The

self-education course undertaken by Sarah is not related to the work or profession in which

she is currently employed12. Therefore, she will be denied deduction for self-education

expenses since the nexus test is not satisfied.

The disposal of bedroom furniture set by Sarah constitutes “CGT event A1” under

“section 104-10 (1)”. Based on “section 108-25 (2), ITAA 1997” the disposal of personal use

assets made by Sarah is in single set and every disposal that is made by Sarah represents the

part of asset. However, the asset was bought in January and only held for six months before it

was sold by Sarah. Therefore, no discounting method will be applicable while computing

capital gains for Sarah.

Computation of Taxable Income and Net Tax Payable

In the Books of Sarah

For the Year ended 2017/18

Particulars Amount

($AUD)

Amount

($AUD)

Assessable Income

11 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

12 Woellner, R. H, Australian Taxation Law 2012 (CCH Australia, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Gross Salary

Salary from Employment 80000

Salary from Teaching 25000

Net capital gain on disposal of Collectables

The 12-month ownership rule: No

Proceeds 4400

Cost base 1550

Gross capital gain (proceeds less cost base) 2850

Taxable capital gain 2850

Total assessable income 107850

Allowable deductions

Home Office Deduction

Interest on Loan 30000

Insurance 3000

Lightning and Electricity 7000

Total home office expenses 40000

Work purpose (60% x 20% of floor area) 4800

Depreciation for Design Equipment (60% work

Purpose) (Note 1)

1098

Membership Fees 700

Subscription Fees 500

On site Traveling Expenses 4000

Total Allowable Deductions 11098

Total Taxable Income 96752

Tax on Taxable Income 23430

Add: Medicare Levy 1935

Total Tax payable 25365

Note 1:

Asset Type Base Value Days Held Days in Year Percentage Effective life Total Depreciation Closing Balance

Design Equipment 9000 334 365 200% 9 1830 7170

Depreciation Worksheet

Gross Salary

Salary from Employment 80000

Salary from Teaching 25000

Net capital gain on disposal of Collectables

The 12-month ownership rule: No

Proceeds 4400

Cost base 1550

Gross capital gain (proceeds less cost base) 2850

Taxable capital gain 2850

Total assessable income 107850

Allowable deductions

Home Office Deduction

Interest on Loan 30000

Insurance 3000

Lightning and Electricity 7000

Total home office expenses 40000

Work purpose (60% x 20% of floor area) 4800

Depreciation for Design Equipment (60% work

Purpose) (Note 1)

1098

Membership Fees 700

Subscription Fees 500

On site Traveling Expenses 4000

Total Allowable Deductions 11098

Total Taxable Income 96752

Tax on Taxable Income 23430

Add: Medicare Levy 1935

Total Tax payable 25365

Note 1:

Asset Type Base Value Days Held Days in Year Percentage Effective life Total Depreciation Closing Balance

Design Equipment 9000 334 365 200% 9 1830 7170

Depreciation Worksheet

8TAXATION LAW

Conclusion:

Conclusively, Sarah will be liable for taxation for her gross salary from employment

within the ordinary concepts of “section 6-5”. While she will be denied deduction for cost of

travelling, ordinary clothing and self-education expenses under “section 8-1”.

Conclusion:

Conclusively, Sarah will be liable for taxation for her gross salary from employment

within the ordinary concepts of “section 6-5”. While she will be denied deduction for cost of

travelling, ordinary clothing and self-education expenses under “section 8-1”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Barkoczy, Stephen, Foundations Of Taxation Law 2014.

Eliot, George, The Mill On The Floss (Open Road Integrated Media, 2016).

Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business

Taxation.

Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014).

Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013).

Krever, Richard E, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013).

Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law (CCH Australia, 2013).

Sadiq, Kerrie et al, Principles Of Taxation Law (2014).

Tax, Law And Development (Edward Elgar, 2013).

Woellner, R. H, Australian Taxation Law 2012 (CCH Australia, 2013).

Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

References:

Barkoczy, Stephen, Foundations Of Taxation Law 2014.

Eliot, George, The Mill On The Floss (Open Road Integrated Media, 2016).

Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business

Taxation.

Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014).

Kenny, Paul, Australian Tax 2013 (LexisNexis Butterworths, 2013).

Krever, Richard E, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013).

Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

Morgan, Annette, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law (CCH Australia, 2013).

Sadiq, Kerrie et al, Principles Of Taxation Law (2014).

Tax, Law And Development (Edward Elgar, 2013).

Woellner, R. H, Australian Taxation Law 2012 (CCH Australia, 2013).

Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.