Taxation Law: Income, Deductions, and Case Law Analysis - Year 2018

VerifiedAdded on 2023/04/25

|12

|2786

|487

Case Study

AI Summary

This case study provides a comprehensive analysis of taxation law, focusing on income assessment and allowable deductions. Part A involves calculating Jane's net income for the year ended June 30, 2018, considering various income sources like salary, bonuses, awards, rental income, and dividends, as well as deductible expenses related to her business and investments. The analysis also covers statutory income, franking credits, and capital gains/losses. Part B examines the case of FC of T v Cook and Sherden, discussing the facts, decision, and relevance of the case today, particularly concerning non-cash business benefits and their taxability. The study concludes with a detailed computation of Jane's net income, allowable deductions, and taxable income, including calculations for tax payable, Medicare levy, and franking credits.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part A:........................................................................................................................................2

Part B:.........................................................................................................................................8

Facts of the Case:...................................................................................................................8

Decision and main principles:................................................................................................8

Relevance of case today and likely decision on similar facts:...............................................9

References:...............................................................................................................................10

Table of Contents

Part A:........................................................................................................................................2

Part B:.........................................................................................................................................8

Facts of the Case:...................................................................................................................8

Decision and main principles:................................................................................................8

Relevance of case today and likely decision on similar facts:...............................................9

References:...............................................................................................................................10

2TAXATION LAW

Part A:

A receipt obtained from the employment and offering personal services will be

subjected to income tax for the employee. A relation or nexus with the receipts as the

outcome of taxpayer’s personal service is regarded as ordinary income. Ordinary income is

regarded as income based on the ordinary concepts and taxable under “section 6-5, ITAA

1997”. In “Scott v CT (1935)” income should be determined on the basis of ordinary

concepts and use of mankind (Grange et al., 2014). The gross cash salary of $50,000 is an

income from employment for offering personal service which will be subjected to taxation

under the ordinary concepts of “section 6-5, ITAA 1997”.

As per “taxation ruling TR 98/1” any income obtained from employment will be

subject to taxation based on receipts basis irrespective of whether such income relates to

future or past earnings (Deutsch, 2018). For instance, unanticipated or voluntary payments

that is received as the incidence of employment is regarded as ordinary income. In “Laidler v

Perry (1965)” the court held that Christmas bonus paid to employees as the redeemable gift

voucher was treated as income. The performance bonus received by Jane is the incidence of

employment and hence taxable as ordinary income under “section 6-5, ITAA 1997”. The

clothing allowance received from Milton Hotels by Jane is included for assessment as

ordinary taxable income.

When a taxpayer incurs expenses on the ordinary items of apparel namely formal suits

they are not allowed for deduction under “section 8-1”. As held in “Mansfield v FCT

(1996)” a deduction was denied to the taxpayer for expense on ordinary articles of apparel,

irrespective that such expenses is necessary to make sure that good appearance is maintained

in job (Barkoczy, 2014). Jane makes an expense of $7,500 on jewellery and office formal

Part A:

A receipt obtained from the employment and offering personal services will be

subjected to income tax for the employee. A relation or nexus with the receipts as the

outcome of taxpayer’s personal service is regarded as ordinary income. Ordinary income is

regarded as income based on the ordinary concepts and taxable under “section 6-5, ITAA

1997”. In “Scott v CT (1935)” income should be determined on the basis of ordinary

concepts and use of mankind (Grange et al., 2014). The gross cash salary of $50,000 is an

income from employment for offering personal service which will be subjected to taxation

under the ordinary concepts of “section 6-5, ITAA 1997”.

As per “taxation ruling TR 98/1” any income obtained from employment will be

subject to taxation based on receipts basis irrespective of whether such income relates to

future or past earnings (Deutsch, 2018). For instance, unanticipated or voluntary payments

that is received as the incidence of employment is regarded as ordinary income. In “Laidler v

Perry (1965)” the court held that Christmas bonus paid to employees as the redeemable gift

voucher was treated as income. The performance bonus received by Jane is the incidence of

employment and hence taxable as ordinary income under “section 6-5, ITAA 1997”. The

clothing allowance received from Milton Hotels by Jane is included for assessment as

ordinary taxable income.

When a taxpayer incurs expenses on the ordinary items of apparel namely formal suits

they are not allowed for deduction under “section 8-1”. As held in “Mansfield v FCT

(1996)” a deduction was denied to the taxpayer for expense on ordinary articles of apparel,

irrespective that such expenses is necessary to make sure that good appearance is maintained

in job (Barkoczy, 2014). Jane makes an expense of $7,500 on jewellery and office formal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

wear. No deduction is allowed to Jane under “section 8-1, ITAA 1997” because they are

ordinary items of apparel which is not related to work.

In “Moore v Griffiths (1972)” mere wining of prize was not an income. However,

prize may be treated as income on noting that a sufficient nexus is present with the income

earning activities of the taxpayer. In “Kelly v FCT (1985)” the receipt of award by the

professional footballer for being the best player was an income (Eliot, 2016). The amount

held nexus with the work and employment with the club. The receipt of award by Jane for

being the best financial controller in Australia should be considered as income because it is

related to her employment and work. She also received an HP computer that worth $2,550.

As held in “Cooke and Sherden v FCT (1980)” gains which is non-convertible to cash or

worth of money was not regarded as income (Edward, 2013). Nevertheless, the HP computer

received by Jane held the market value of $2,550 which can be converted into money’s

worth. With application of “section 26 (e)”, the HP computer received as an award will be

treated as ordinary income and the same is included for assessment.

As per the “section 23L ITAA 1936” if the employer provides the employee with the

fringe benefit then in such case the benefit will be considered as non-assessable income for

the employee and a fringe benefit tax will be imposed on the employer on the value of benefit

(Jover-Ledesma, 2014). The membership fees of $1,250 paid by Milton Hotel is non-

assessable benefit for Jane under “section 23L of ITAA 1936” while her employer will be

subject to fringe benefit tax on the value of benefit.

According to the ATO the taxpayers are allowed to claim a permissible deduction for

the expenses occurred on the conference, seminars and workshop which is associated to

work. The personal portion of the expenses are excluded from the deduction. Jane while

attending a conference can claim the cost of registration, air fares for her part and

wear. No deduction is allowed to Jane under “section 8-1, ITAA 1997” because they are

ordinary items of apparel which is not related to work.

In “Moore v Griffiths (1972)” mere wining of prize was not an income. However,

prize may be treated as income on noting that a sufficient nexus is present with the income

earning activities of the taxpayer. In “Kelly v FCT (1985)” the receipt of award by the

professional footballer for being the best player was an income (Eliot, 2016). The amount

held nexus with the work and employment with the club. The receipt of award by Jane for

being the best financial controller in Australia should be considered as income because it is

related to her employment and work. She also received an HP computer that worth $2,550.

As held in “Cooke and Sherden v FCT (1980)” gains which is non-convertible to cash or

worth of money was not regarded as income (Edward, 2013). Nevertheless, the HP computer

received by Jane held the market value of $2,550 which can be converted into money’s

worth. With application of “section 26 (e)”, the HP computer received as an award will be

treated as ordinary income and the same is included for assessment.

As per the “section 23L ITAA 1936” if the employer provides the employee with the

fringe benefit then in such case the benefit will be considered as non-assessable income for

the employee and a fringe benefit tax will be imposed on the employer on the value of benefit

(Jover-Ledesma, 2014). The membership fees of $1,250 paid by Milton Hotel is non-

assessable benefit for Jane under “section 23L of ITAA 1936” while her employer will be

subject to fringe benefit tax on the value of benefit.

According to the ATO the taxpayers are allowed to claim a permissible deduction for

the expenses occurred on the conference, seminars and workshop which is associated to

work. The personal portion of the expenses are excluded from the deduction. Jane while

attending a conference can claim the cost of registration, air fares for her part and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

accommodation. While she the air fares for her husband and visiting of historical importance

places will be non-deductible as they are private expenses.

In “Lunney v FCT” the travelling between home and person’s normal place of work

is non-deductible. But then the legislative response of “section 25-100 ITAA 1997” permits

the taxpayer to claim deduction on the cost of travel among the workplaces. Travel should

directly be between two place where revenue producing activities are performed and none of

them is home for the taxpayer. As held in “FCT v Wiener (1978)” the taxpayer was allowed

deduction for travelling between schools because the employment of the taxpayer required

travelling between schools to perform her duties (Krever, 2013). Similarly, Jane will be

permitted to claim deduction on the travelling expenses incurred from her place of

employment to taxation practice in Kingsford.

As per the “taxation ruling of TR 98/1” when the income is earned in one year of tax

and received in another year of tax the it is necessary to adopt right method of determining

when the income is earned under “section 6-5 (2) and (3)”. There are two method for

determining income (Morgan et al., 2013). Namely the earnings method and receipts method.

Under “sub-section 6-5(4), ITAA 1997” in receipts method income is derived when it is

received. While under earnings method income is derived when it is earned.

As held in “Barratt v FCT (1992)” where the taxpayers formal business activities

includes the extending credit and collecting of debts, the earnings method is regarded as the

most appropriate method of accounting (Kenny, 2013). Jane reports income from her

business and investment property. She received fees from business practices that included

unbilled fees as well. While her rental property included unearned or accrued rent during the

year. Mentioning the case of “Barratt v FCT (1992)” Jane must follow the earnings method

of accounting as it is more appropriate method of substantially providing true reflex of her

accommodation. While she the air fares for her husband and visiting of historical importance

places will be non-deductible as they are private expenses.

In “Lunney v FCT” the travelling between home and person’s normal place of work

is non-deductible. But then the legislative response of “section 25-100 ITAA 1997” permits

the taxpayer to claim deduction on the cost of travel among the workplaces. Travel should

directly be between two place where revenue producing activities are performed and none of

them is home for the taxpayer. As held in “FCT v Wiener (1978)” the taxpayer was allowed

deduction for travelling between schools because the employment of the taxpayer required

travelling between schools to perform her duties (Krever, 2013). Similarly, Jane will be

permitted to claim deduction on the travelling expenses incurred from her place of

employment to taxation practice in Kingsford.

As per the “taxation ruling of TR 98/1” when the income is earned in one year of tax

and received in another year of tax the it is necessary to adopt right method of determining

when the income is earned under “section 6-5 (2) and (3)”. There are two method for

determining income (Morgan et al., 2013). Namely the earnings method and receipts method.

Under “sub-section 6-5(4), ITAA 1997” in receipts method income is derived when it is

received. While under earnings method income is derived when it is earned.

As held in “Barratt v FCT (1992)” where the taxpayers formal business activities

includes the extending credit and collecting of debts, the earnings method is regarded as the

most appropriate method of accounting (Kenny, 2013). Jane reports income from her

business and investment property. She received fees from business practices that included

unbilled fees as well. While her rental property included unearned or accrued rent during the

year. Mentioning the case of “Barratt v FCT (1992)” Jane must follow the earnings method

of accounting as it is more appropriate method of substantially providing true reflex of her

5TAXATION LAW

income. Whereas the expenses incurred for her business and investment property are allowed

as deduction under “section 8-1, ITAA 1997” because they were incurred in earning taxable

income.

The assessable income also includes the statutory income. Dividends are regarded as

statutory income under “section 44 ITAA 1936”. The franking credits that are related with

the franked dividends are included for assessment under “section 201-20 (1), ITAA 1997” as

the statutory income, however an income tax offset can be claimed for the franking credits to

reduce income tax liability (Sadiq et al., 2014). Jane reports the receipts of franked dividend

from CBA and BHP shares. These dividends are included for assessment as statutory income.

The franking credits are also included for assessment as statutory income under “section

201-20 (1), ITAA 1997”. Jane can claim tax offset for the franking credits associated to

franked dividends.

During the year Jane reports the capital gains from the sale of CBA shares while her

BHP shares yielded capital loss. Jane can offset the capital loss from BHP shares against the

gains made from CBA shares. Furthermore, the donation to Cancer Council Australia and

Sydney University can be claimed as income deduction by Jane under “section 30-15 (2),

subdivision 30c, ITAA 1997”.

income. Whereas the expenses incurred for her business and investment property are allowed

as deduction under “section 8-1, ITAA 1997” because they were incurred in earning taxable

income.

The assessable income also includes the statutory income. Dividends are regarded as

statutory income under “section 44 ITAA 1936”. The franking credits that are related with

the franked dividends are included for assessment under “section 201-20 (1), ITAA 1997” as

the statutory income, however an income tax offset can be claimed for the franking credits to

reduce income tax liability (Sadiq et al., 2014). Jane reports the receipts of franked dividend

from CBA and BHP shares. These dividends are included for assessment as statutory income.

The franking credits are also included for assessment as statutory income under “section

201-20 (1), ITAA 1997”. Jane can claim tax offset for the franking credits associated to

franked dividends.

During the year Jane reports the capital gains from the sale of CBA shares while her

BHP shares yielded capital loss. Jane can offset the capital loss from BHP shares against the

gains made from CBA shares. Furthermore, the donation to Cancer Council Australia and

Sydney University can be claimed as income deduction by Jane under “section 30-15 (2),

subdivision 30c, ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

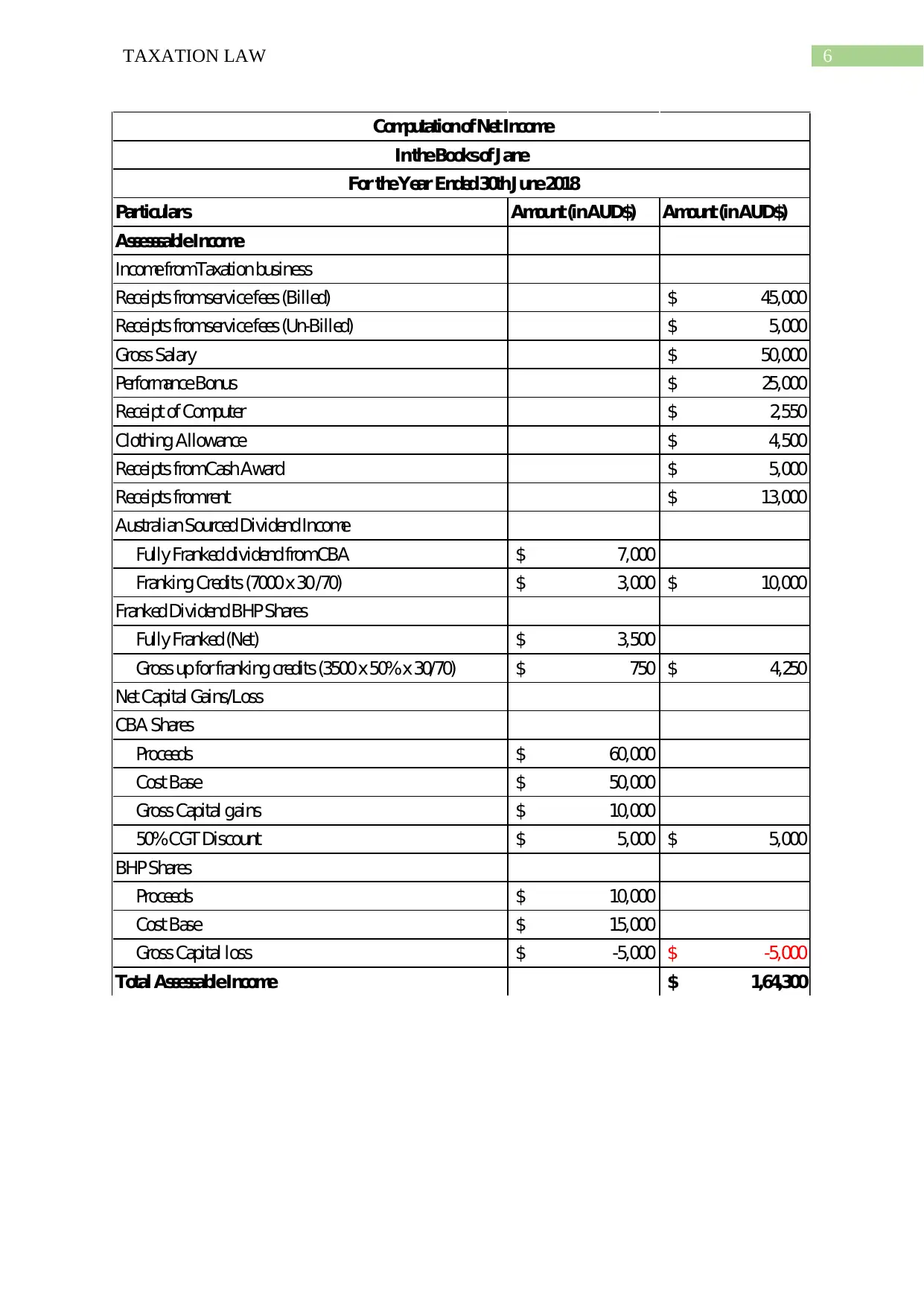

Particulars Amount(inAUD$) Amount(inAUD$)

AssesssableIncome

IncomefromTaxationbusiness

Receipts fromservicefees (Billed) 45,000$

Receipts fromservicefees (Un-Billed) 5,000$

Gross Salary 50,000$

PerformanceBonus 25,000$

Receipt of Computer 2,550$

Clothing Allowance 4,500$

Receipts fromCashAward 5,000$

Receipts fromrent 13,000$

AustralianSourcedDividendIncome

Fully FrankeddividendfromCBA 7,000$

Franking Credits (7000 x30/70) 3,000$ 10,000$

FrankedDividendBHP Shares

Fully Franked(Net) 3,500$

Gross upforfranking credits (3500x50%x 30/70) 750$ 4,250$

Net Capital Gains/Loss

CBA Shares

Proceeds 60,000$

Cost Base 50,000$

Gross Capital gains 10,000$

50%CGT Discount 5,000$ 5,000$

BHP Shares

Proceeds 10,000$

Cost Base 15,000$

Gross Capital loss -5,000$ -5,000$

Total AssessableIncome 1,64,300$

ComputationofNetIncome

IntheBooksofJane

For theYear Ended30thJune2018

Particulars Amount(inAUD$) Amount(inAUD$)

AssesssableIncome

IncomefromTaxationbusiness

Receipts fromservicefees (Billed) 45,000$

Receipts fromservicefees (Un-Billed) 5,000$

Gross Salary 50,000$

PerformanceBonus 25,000$

Receipt of Computer 2,550$

Clothing Allowance 4,500$

Receipts fromCashAward 5,000$

Receipts fromrent 13,000$

AustralianSourcedDividendIncome

Fully FrankeddividendfromCBA 7,000$

Franking Credits (7000 x30/70) 3,000$ 10,000$

FrankedDividendBHP Shares

Fully Franked(Net) 3,500$

Gross upforfranking credits (3500x50%x 30/70) 750$ 4,250$

Net Capital Gains/Loss

CBA Shares

Proceeds 60,000$

Cost Base 50,000$

Gross Capital gains 10,000$

50%CGT Discount 5,000$ 5,000$

BHP Shares

Proceeds 10,000$

Cost Base 15,000$

Gross Capital loss -5,000$ -5,000$

Total AssessableIncome 1,64,300$

ComputationofNetIncome

IntheBooksofJane

For theYear Ended30thJune2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

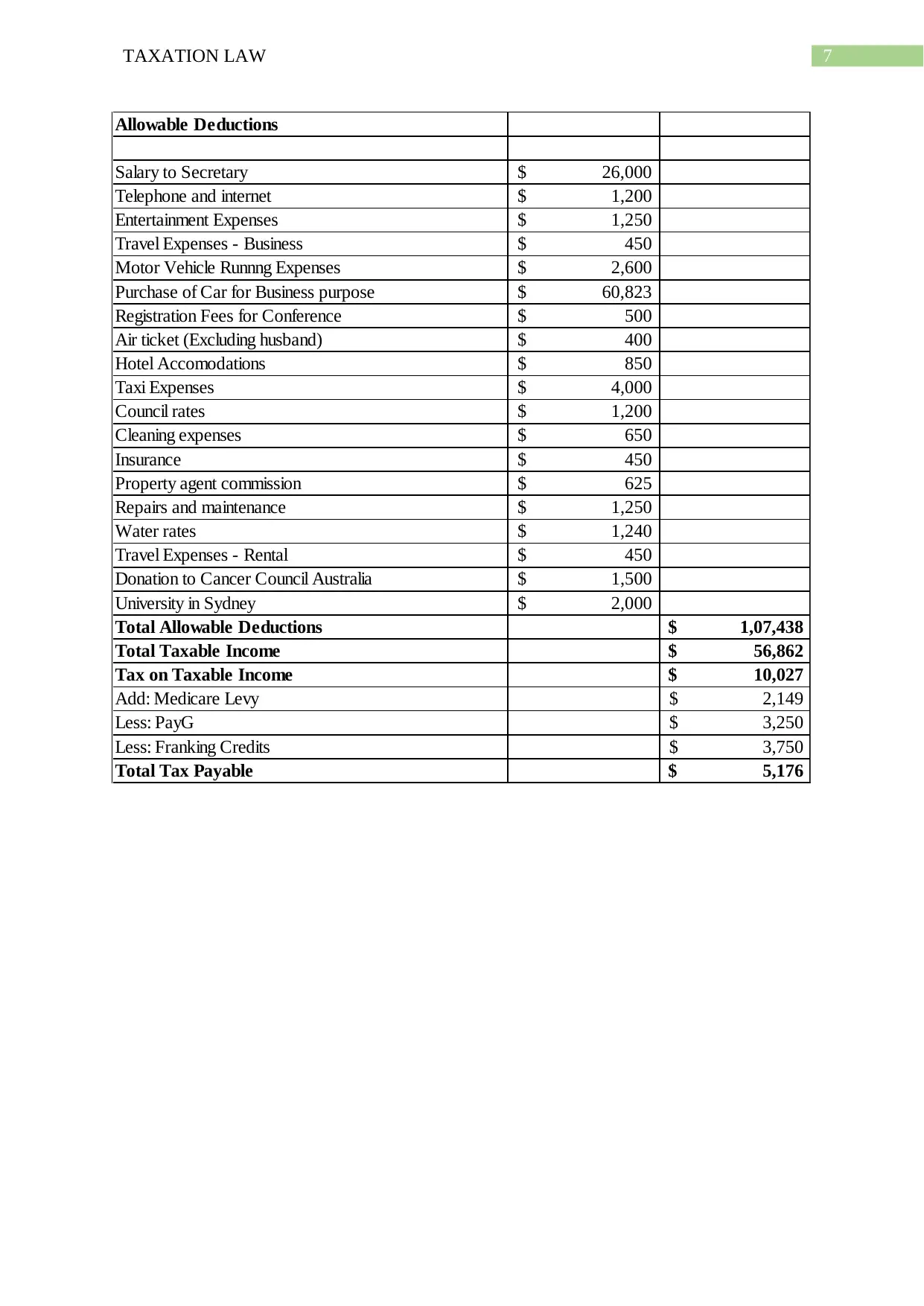

Allowable Deductions

Salary to Secretary 26,000$

Telephone and internet 1,200$

Entertainment Expenses 1,250$

Travel Expenses - Business 450$

Motor Vehicle Runnng Expenses 2,600$

Purchase of Car for Business purpose 60,823$

Registration Fees for Conference 500$

Air ticket (Excluding husband) 400$

Hotel Accomodations 850$

Taxi Expenses 4,000$

Council rates 1,200$

Cleaning expenses 650$

Insurance 450$

Property agent commission 625$

Repairs and maintenance 1,250$

Water rates 1,240$

Travel Expenses - Rental 450$

Donation to Cancer Council Australia 1,500$

University in Sydney 2,000$

Total Allowable Deductions 1,07,438$

Total Taxable Income 56,862$

Tax on Taxable Income 10,027$

Add: Medicare Levy 2,149$

Less: PayG 3,250$

Less: Franking Credits 3,750$

Total Tax Payable 5,176$

Allowable Deductions

Salary to Secretary 26,000$

Telephone and internet 1,200$

Entertainment Expenses 1,250$

Travel Expenses - Business 450$

Motor Vehicle Runnng Expenses 2,600$

Purchase of Car for Business purpose 60,823$

Registration Fees for Conference 500$

Air ticket (Excluding husband) 400$

Hotel Accomodations 850$

Taxi Expenses 4,000$

Council rates 1,200$

Cleaning expenses 650$

Insurance 450$

Property agent commission 625$

Repairs and maintenance 1,250$

Water rates 1,240$

Travel Expenses - Rental 450$

Donation to Cancer Council Australia 1,500$

University in Sydney 2,000$

Total Allowable Deductions 1,07,438$

Total Taxable Income 56,862$

Tax on Taxable Income 10,027$

Add: Medicare Levy 2,149$

Less: PayG 3,250$

Less: Franking Credits 3,750$

Total Tax Payable 5,176$

8TAXATION LAW

Part B:

Facts of the Case:

In “FC of T v Cook and Sherden, 80 ATC 4140” the taxpayer operated a business

under partnership. The taxpayer separately went on door-to-door for distribution of soft

drinks based on the franchise agreement with the manufacturer of soft drink (Woellner,

2013). An incentive scheme was sponsored by the manufacturer which allowed their

distributors each year to win prizes such as free trips of holidays either in local or overseas

resorts. The trips were non-transferable and cannot be converted into the cash or any other

type of property. if the winners does not take the trips then no further rewards are provided.

The taxpayer’s each won the holiday trips. The commissioner assessed the taxpayer on the

amounts that is equivalent to the costs of assessable income.

To support the taxation, an argument followed that the value of holiday trips was

taxable under “section 25 (1), ITAA 1977” within the ordinary income concepts (Christians,

2017). However, in the unanimous decision it was held that no part of the value of trips were

taxable.

Decision and main principles:

The decision of the court held that the gratuitous benefits in the form of kind under

“section 25 (1)”, that could not be converted in cash or any other property will not be treated

as income based on the ordinary concepts. In the view of court, benefit or gift of type will be

only taxable if the benefit is received either in money or it is capable of being converting into

the money’s worth or money (Sheffrin, 2018). The decision of the law court also included

that it was of no importance that the taxpayers were able to save the expenditure which would

have occurred if they have paid themselves for the holiday, therefore, such savings is not

treated as income.

Part B:

Facts of the Case:

In “FC of T v Cook and Sherden, 80 ATC 4140” the taxpayer operated a business

under partnership. The taxpayer separately went on door-to-door for distribution of soft

drinks based on the franchise agreement with the manufacturer of soft drink (Woellner,

2013). An incentive scheme was sponsored by the manufacturer which allowed their

distributors each year to win prizes such as free trips of holidays either in local or overseas

resorts. The trips were non-transferable and cannot be converted into the cash or any other

type of property. if the winners does not take the trips then no further rewards are provided.

The taxpayer’s each won the holiday trips. The commissioner assessed the taxpayer on the

amounts that is equivalent to the costs of assessable income.

To support the taxation, an argument followed that the value of holiday trips was

taxable under “section 25 (1), ITAA 1977” within the ordinary income concepts (Christians,

2017). However, in the unanimous decision it was held that no part of the value of trips were

taxable.

Decision and main principles:

The decision of the court held that the gratuitous benefits in the form of kind under

“section 25 (1)”, that could not be converted in cash or any other property will not be treated

as income based on the ordinary concepts. In the view of court, benefit or gift of type will be

only taxable if the benefit is received either in money or it is capable of being converting into

the money’s worth or money (Sheffrin, 2018). The decision of the law court also included

that it was of no importance that the taxpayers were able to save the expenditure which would

have occurred if they have paid themselves for the holiday, therefore, such savings is not

treated as income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

The law court also observed that if the taxpayers received the benefit that cannot be

converted into pecuniary account, then no income is received by the taxpayer within the

ordinary concepts. As a result the court also referred to illustration of “Abbott v Philbin

(1961)” where the option for purchasing of shares were involved (Miller & Oats, 2016). The

court held that even if the options for shares cannot be assigned but the call for shares was

having the money’s worth because it can be used as security for borrowing money.

By referring to “section 26 (e)”, the decision held that no kind of services were

performed by the taxpayers to the manufacturers (Krever, 2013). The taxpayers only

performed their business activities on their behalf for their benefit. Therefore, no room for

application of “section 26 (e)”, was available.

Relevance of case today and likely decision on similar facts:

The decision made in “FC of T v Cook and Sherden, 80 ATC 4140” is considered

relevant because the judgement of court resulted in the adoption of section 21A that dealt

with the non-cash business benefits which is convertible to cash (Christians, 2017)). Within

the meaning of this act, if the non-cash business benefits is received notwithstanding whether

it can be converted to cash, it will be treated as income derived by the taxpayer. The benefit

which is non-convertible shall be considered as if they were convertible to cash.

An identical decision was followed in the example of “Payne v FCT (1986) ATC

4407” where the commissioner of taxation imposed tax on the taxpayer based on the market

value of the tickets (Woellner, 2013). The decision of federal court held that frequent flyer

points will not be treated as income because it was not money. The points were non-

convertible or non-transferable and if it sold then they were subjected to cancellation.

The law court also observed that if the taxpayers received the benefit that cannot be

converted into pecuniary account, then no income is received by the taxpayer within the

ordinary concepts. As a result the court also referred to illustration of “Abbott v Philbin

(1961)” where the option for purchasing of shares were involved (Miller & Oats, 2016). The

court held that even if the options for shares cannot be assigned but the call for shares was

having the money’s worth because it can be used as security for borrowing money.

By referring to “section 26 (e)”, the decision held that no kind of services were

performed by the taxpayers to the manufacturers (Krever, 2013). The taxpayers only

performed their business activities on their behalf for their benefit. Therefore, no room for

application of “section 26 (e)”, was available.

Relevance of case today and likely decision on similar facts:

The decision made in “FC of T v Cook and Sherden, 80 ATC 4140” is considered

relevant because the judgement of court resulted in the adoption of section 21A that dealt

with the non-cash business benefits which is convertible to cash (Christians, 2017)). Within

the meaning of this act, if the non-cash business benefits is received notwithstanding whether

it can be converted to cash, it will be treated as income derived by the taxpayer. The benefit

which is non-convertible shall be considered as if they were convertible to cash.

An identical decision was followed in the example of “Payne v FCT (1986) ATC

4407” where the commissioner of taxation imposed tax on the taxpayer based on the market

value of the tickets (Woellner, 2013). The decision of federal court held that frequent flyer

points will not be treated as income because it was not money. The points were non-

convertible or non-transferable and if it sold then they were subjected to cancellation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Barkoczy, S. (2014). Foundations of taxation law 2014.

Christians, A. (2017). Hard Law, Soft Law, and International Taxation. Wis. Int'l LJ, 25, 325.

Deutsch, R. (2018). Australian tax handbook 2018: THOMSON REUTERS AUSTRALIA.

Edward E. (2013). Tax, law and development. Cheltenham, UK.

Eliot, G. (2016). The mill on the Floss: Open Road Integrated Media.

Grange, J., Jover-Ledesma, G., & Maydew, G. (2014). principles of business taxation.

Jover-Ledesma, G. (2014). Principles of business taxation 2015: Cch Incorporated.

Kenny, P. (2013). Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. (2013). Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian

taxation law. North Ryde [N.S.W.]: CCH Australia.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., & Ting, A. (2014).

Principles of taxation law 2014.

Sheffrin, S. M. (2018). The Domain of Desert Principles for Taxation. Erasmus Journal for

Philosophy and Economics, 11(2), 220-244.

Woellner, R. (2013). Australian taxation law 2012. North Ryde [N.S.W.]: CCH Australia.

References:

Barkoczy, S. (2014). Foundations of taxation law 2014.

Christians, A. (2017). Hard Law, Soft Law, and International Taxation. Wis. Int'l LJ, 25, 325.

Deutsch, R. (2018). Australian tax handbook 2018: THOMSON REUTERS AUSTRALIA.

Edward E. (2013). Tax, law and development. Cheltenham, UK.

Eliot, G. (2016). The mill on the Floss: Open Road Integrated Media.

Grange, J., Jover-Ledesma, G., & Maydew, G. (2014). principles of business taxation.

Jover-Ledesma, G. (2014). Principles of business taxation 2015: Cch Incorporated.

Kenny, P. (2013). Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. (2013). Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian

taxation law. North Ryde [N.S.W.]: CCH Australia.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., & Ting, A. (2014).

Principles of taxation law 2014.

Sheffrin, S. M. (2018). The Domain of Desert Principles for Taxation. Erasmus Journal for

Philosophy and Economics, 11(2), 220-244.

Woellner, R. (2013). Australian taxation law 2012. North Ryde [N.S.W.]: CCH Australia.

11TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.