Taxation Law Assignment: Fringe Benefits Tax, CGT, and Case Studies

VerifiedAdded on 2022/11/13

|11

|2502

|439

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation law assignment, focusing on fringe benefit tax (FBT) and capital gains tax (CGT). It begins by defining FBT and its application, including car fringe benefits, and provides detailed calculations using both statutory and operating cost methods. The assignment then delves into CGT, explaining what constitutes a CGT asset and the implications of CGT events. It analyzes several case studies, including the sale of a main residence, a painting, a luxury yacht, and shares, outlining the relevant tax consequences for each scenario. The analysis covers exemptions like the main residence exemption and the treatment of personal use assets, providing a clear understanding of the tax implications of various asset disposals. The assignment offers practical advice, such as utilizing the operating cost method to reduce FBT liability, and references relevant legislation, including the FBTAA 1986 and the ITAA 1997, to support its conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Facts of the case:........................................................................................................................3

Answer to question 2:.................................................................................................................6

Answer to A:..........................................................................................................................6

Case facts:..............................................................................................................................7

Sale of Main residence:..........................................................................................................7

Sale of Painting:.....................................................................................................................7

Sale of Luxury Yacht:............................................................................................................8

Sale of Shares:........................................................................................................................8

Answer to question B:............................................................................................................9

Answer to question C:............................................................................................................9

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Facts of the case:........................................................................................................................3

Answer to question 2:.................................................................................................................6

Answer to A:..........................................................................................................................6

Case facts:..............................................................................................................................7

Sale of Main residence:..........................................................................................................7

Sale of Painting:.....................................................................................................................7

Sale of Luxury Yacht:............................................................................................................8

Sale of Shares:........................................................................................................................8

Answer to question B:............................................................................................................9

Answer to question C:............................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

The fringe benefit tax is defined as the regime that is fundamentally treated as the tax

on the wide range of benefits that is provided to the employer or the employee. According to

the subsection 136 (1) FBTAA 1986 a fringe benefit tax is regarded as the benefit that is

provided to the employee by the employer during the taxation year in relation to the

employment of the employee (Barkoczy 2014). Section 136 (1)) explains that the word

benefit comprises of the any form of rights, privilege, service or the facilities that is provided

to the employee under the arrangement with respect to the performance of the work.

The court of law in “J & G Knowles & Associates Pty Ltd (2000) v FCT (2000)”

held that there should be adequate and material relationship to the benefits that is provided in

relation to the employment. There should be a casual relation with the employment to qualify

as the fringe benefit (Grange, Jover-Ledesma and Maydew 2015). The taxpayer should

denote that the benefit by reason or by virtue in respect of directly or indirectly to the

employment. As per “section 136 (1), FBTAA 1986” there are certain benefits that are

excluded or does not falls inside the purview of this act. This includes the salaries or wages,

payment for super funds, benefits in relation to employee share scheme and payment upon

the termination of the employment.

According to the “section 7 (1), FBTAA 1986” a car fringe benefit originates under a

situation where the employer offers the car to the employee for making private use of it.

Section 136 of the FBTAA 1986 explains that private usage of the car implies that the usage

of car is not the exclusively during the course of generating taxable earnings (Jover-Ledesma

2015). In addition to this, the original use is regarded immaterial, a fringe benefit originates

when the car is available for the usage such as the car is garaged at the home of the employee.

Answer to question 1:

The fringe benefit tax is defined as the regime that is fundamentally treated as the tax

on the wide range of benefits that is provided to the employer or the employee. According to

the subsection 136 (1) FBTAA 1986 a fringe benefit tax is regarded as the benefit that is

provided to the employee by the employer during the taxation year in relation to the

employment of the employee (Barkoczy 2014). Section 136 (1)) explains that the word

benefit comprises of the any form of rights, privilege, service or the facilities that is provided

to the employee under the arrangement with respect to the performance of the work.

The court of law in “J & G Knowles & Associates Pty Ltd (2000) v FCT (2000)”

held that there should be adequate and material relationship to the benefits that is provided in

relation to the employment. There should be a casual relation with the employment to qualify

as the fringe benefit (Grange, Jover-Ledesma and Maydew 2015). The taxpayer should

denote that the benefit by reason or by virtue in respect of directly or indirectly to the

employment. As per “section 136 (1), FBTAA 1986” there are certain benefits that are

excluded or does not falls inside the purview of this act. This includes the salaries or wages,

payment for super funds, benefits in relation to employee share scheme and payment upon

the termination of the employment.

According to the “section 7 (1), FBTAA 1986” a car fringe benefit originates under a

situation where the employer offers the car to the employee for making private use of it.

Section 136 of the FBTAA 1986 explains that private usage of the car implies that the usage

of car is not the exclusively during the course of generating taxable earnings (Jover-Ledesma

2015). In addition to this, the original use is regarded immaterial, a fringe benefit originates

when the car is available for the usage such as the car is garaged at the home of the employee.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

There are two methods that are employed in calculating the chargeable value of the

car fringe benefit. According to the section 10 (1), FBTA Act 1986 statutory method is

computed automatically except when the employer decides to use cost method of calculating

the car fringe benefit of the car. The employer is permitted to use either of the method for that

results in the fringe benefit. Subsection 10A and subsection 10B explains that the cost

method requires the records of log books and odometer record for calculating the car fringe

benefit.

Facts of the case:

The case facts that is obtained suggest that Spiececo Pty Ltd has gave his employee

Lucinda the car for their private use. All through the year of 2018/19 Lucinda used the car

and incurred cost on the repairs that amounted to $3,300. In addition to this, expenses such as

Insurance and fuel costs were occurred by the taxpayer. The taxpayer here Lucinda also made

the contribution of $1,000 towards the price of the car.

The case study also provides that Lucinda used the car 70% of the time for the

business while the rest of the 30% of the car usage was dedicated towards the private use of

the car. By gauging into the situation of Lucinda it can be stated that under section 7 of the

FBTA Act 1986 car fringe benefit happens where the employer gives the car to Lucinda for

her private usage. This implies that Spiececo Pty Ltd has given the car to Lucinda for her

private usage and it is not exclusively limited to the production of the taxable under the

section 136 (Kenny 2013). In the situation of Lucinda it can be stated that the actual use of

the car is irrelevant for her because the car fringe benefit originates when Spiececo Pty Ltd

provided the car for her available use.

In addition to this, with reference to the case of “J & G Knowles & Associates Pty

Ltd (2000) v FCT (2000)” providing the car to Lucinda by Spiececo Pty Ltd clearly explains

There are two methods that are employed in calculating the chargeable value of the

car fringe benefit. According to the section 10 (1), FBTA Act 1986 statutory method is

computed automatically except when the employer decides to use cost method of calculating

the car fringe benefit of the car. The employer is permitted to use either of the method for that

results in the fringe benefit. Subsection 10A and subsection 10B explains that the cost

method requires the records of log books and odometer record for calculating the car fringe

benefit.

Facts of the case:

The case facts that is obtained suggest that Spiececo Pty Ltd has gave his employee

Lucinda the car for their private use. All through the year of 2018/19 Lucinda used the car

and incurred cost on the repairs that amounted to $3,300. In addition to this, expenses such as

Insurance and fuel costs were occurred by the taxpayer. The taxpayer here Lucinda also made

the contribution of $1,000 towards the price of the car.

The case study also provides that Lucinda used the car 70% of the time for the

business while the rest of the 30% of the car usage was dedicated towards the private use of

the car. By gauging into the situation of Lucinda it can be stated that under section 7 of the

FBTA Act 1986 car fringe benefit happens where the employer gives the car to Lucinda for

her private usage. This implies that Spiececo Pty Ltd has given the car to Lucinda for her

private usage and it is not exclusively limited to the production of the taxable under the

section 136 (Kenny 2013). In the situation of Lucinda it can be stated that the actual use of

the car is irrelevant for her because the car fringe benefit originates when Spiececo Pty Ltd

provided the car for her available use.

In addition to this, with reference to the case of “J & G Knowles & Associates Pty

Ltd (2000) v FCT (2000)” providing the car to Lucinda by Spiececo Pty Ltd clearly explains

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

the nexus with the employment (Krever 2013). In other words, the car was provided to

Lucinda in respect of the employment. The car qualifies as the fringe benefit in respect of

“section 136” as the benefit that is provided by virtue of or in relation to the direct or indirect

employment.

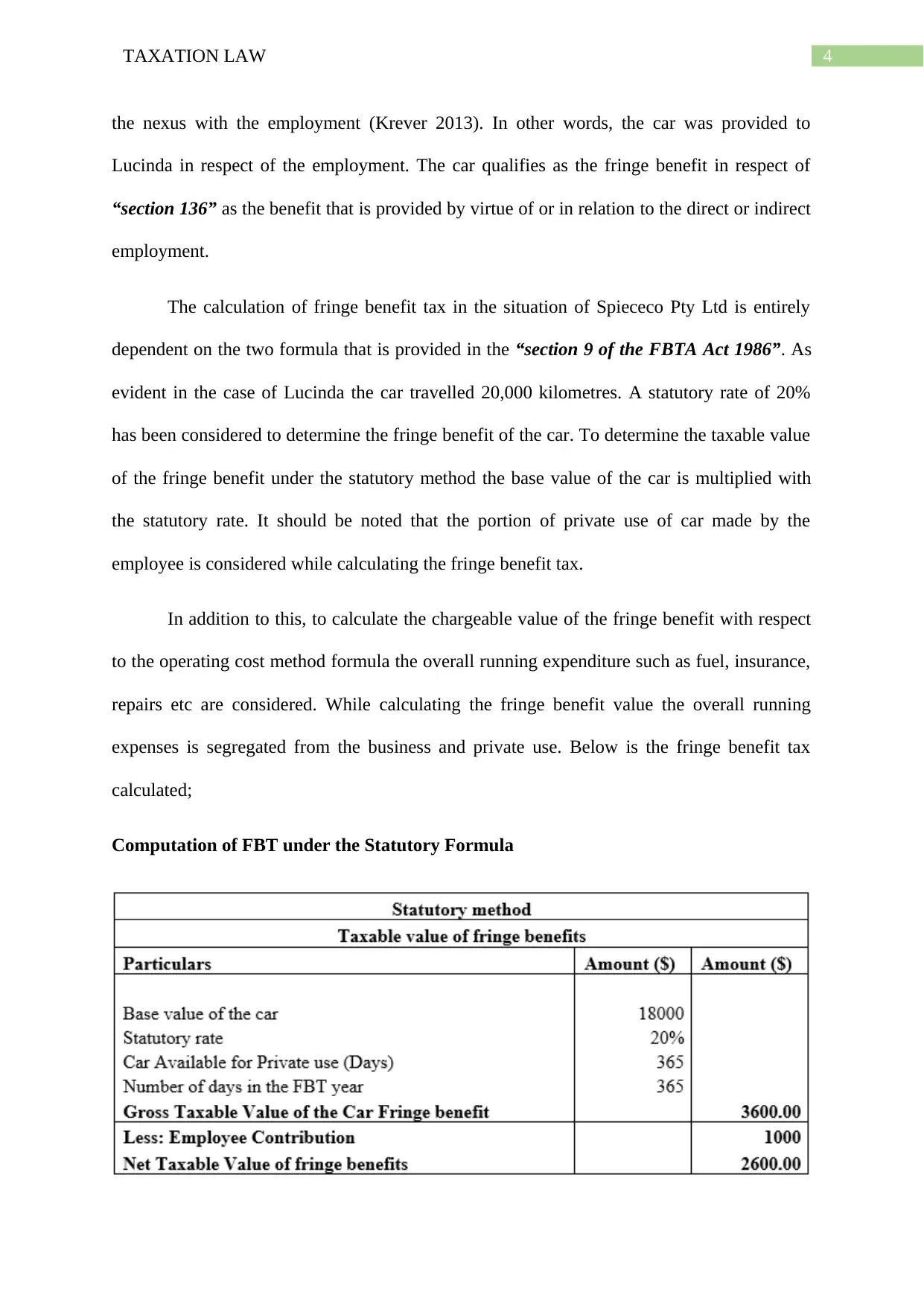

The calculation of fringe benefit tax in the situation of Spiececo Pty Ltd is entirely

dependent on the two formula that is provided in the “section 9 of the FBTA Act 1986”. As

evident in the case of Lucinda the car travelled 20,000 kilometres. A statutory rate of 20%

has been considered to determine the fringe benefit of the car. To determine the taxable value

of the fringe benefit under the statutory method the base value of the car is multiplied with

the statutory rate. It should be noted that the portion of private use of car made by the

employee is considered while calculating the fringe benefit tax.

In addition to this, to calculate the chargeable value of the fringe benefit with respect

to the operating cost method formula the overall running expenditure such as fuel, insurance,

repairs etc are considered. While calculating the fringe benefit value the overall running

expenses is segregated from the business and private use. Below is the fringe benefit tax

calculated;

Computation of FBT under the Statutory Formula

the nexus with the employment (Krever 2013). In other words, the car was provided to

Lucinda in respect of the employment. The car qualifies as the fringe benefit in respect of

“section 136” as the benefit that is provided by virtue of or in relation to the direct or indirect

employment.

The calculation of fringe benefit tax in the situation of Spiececo Pty Ltd is entirely

dependent on the two formula that is provided in the “section 9 of the FBTA Act 1986”. As

evident in the case of Lucinda the car travelled 20,000 kilometres. A statutory rate of 20%

has been considered to determine the fringe benefit of the car. To determine the taxable value

of the fringe benefit under the statutory method the base value of the car is multiplied with

the statutory rate. It should be noted that the portion of private use of car made by the

employee is considered while calculating the fringe benefit tax.

In addition to this, to calculate the chargeable value of the fringe benefit with respect

to the operating cost method formula the overall running expenditure such as fuel, insurance,

repairs etc are considered. While calculating the fringe benefit value the overall running

expenses is segregated from the business and private use. Below is the fringe benefit tax

calculated;

Computation of FBT under the Statutory Formula

5TAXATION LAW

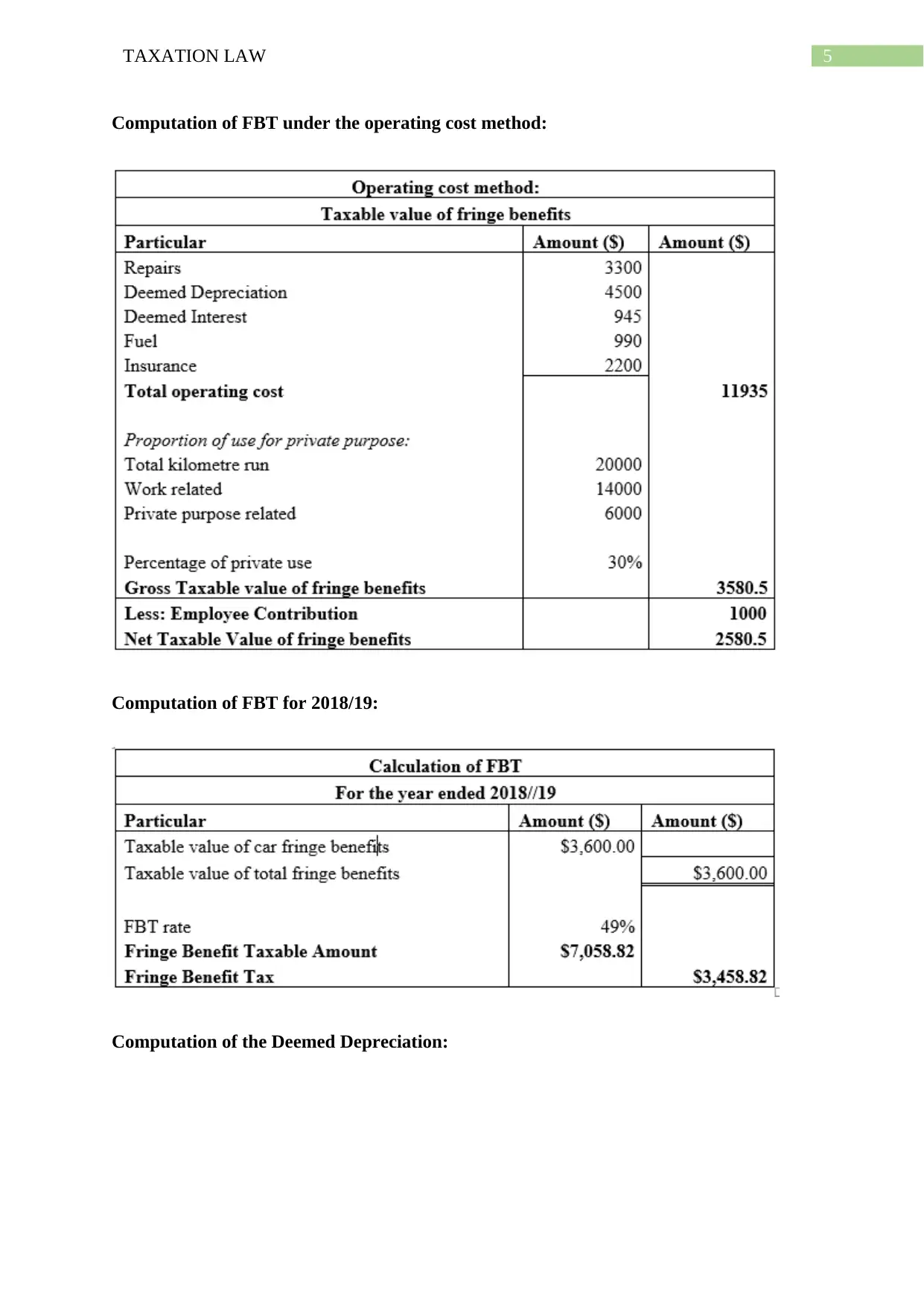

Computation of FBT under the operating cost method:

Computation of FBT for 2018/19:

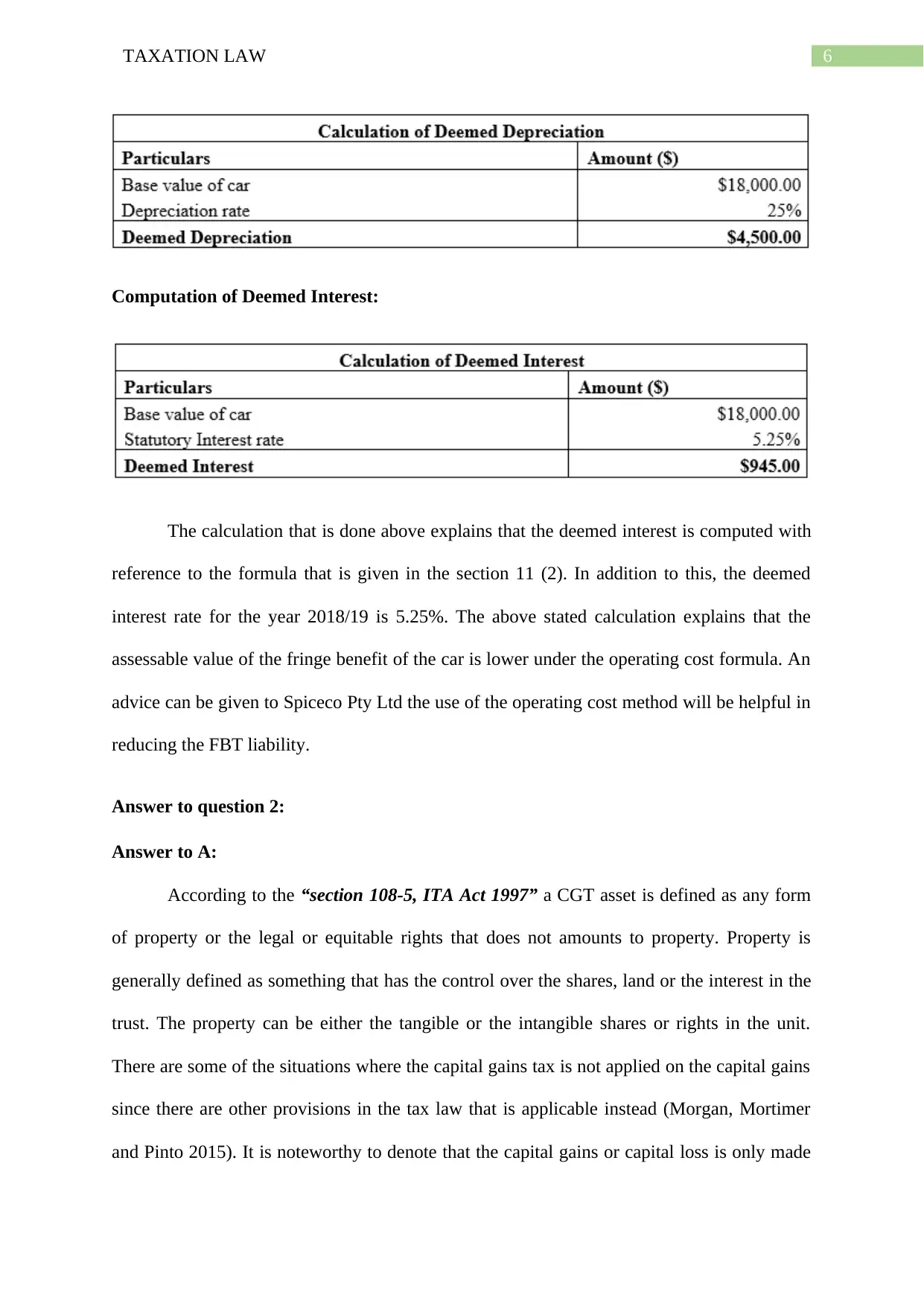

Computation of the Deemed Depreciation:

Computation of FBT under the operating cost method:

Computation of FBT for 2018/19:

Computation of the Deemed Depreciation:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

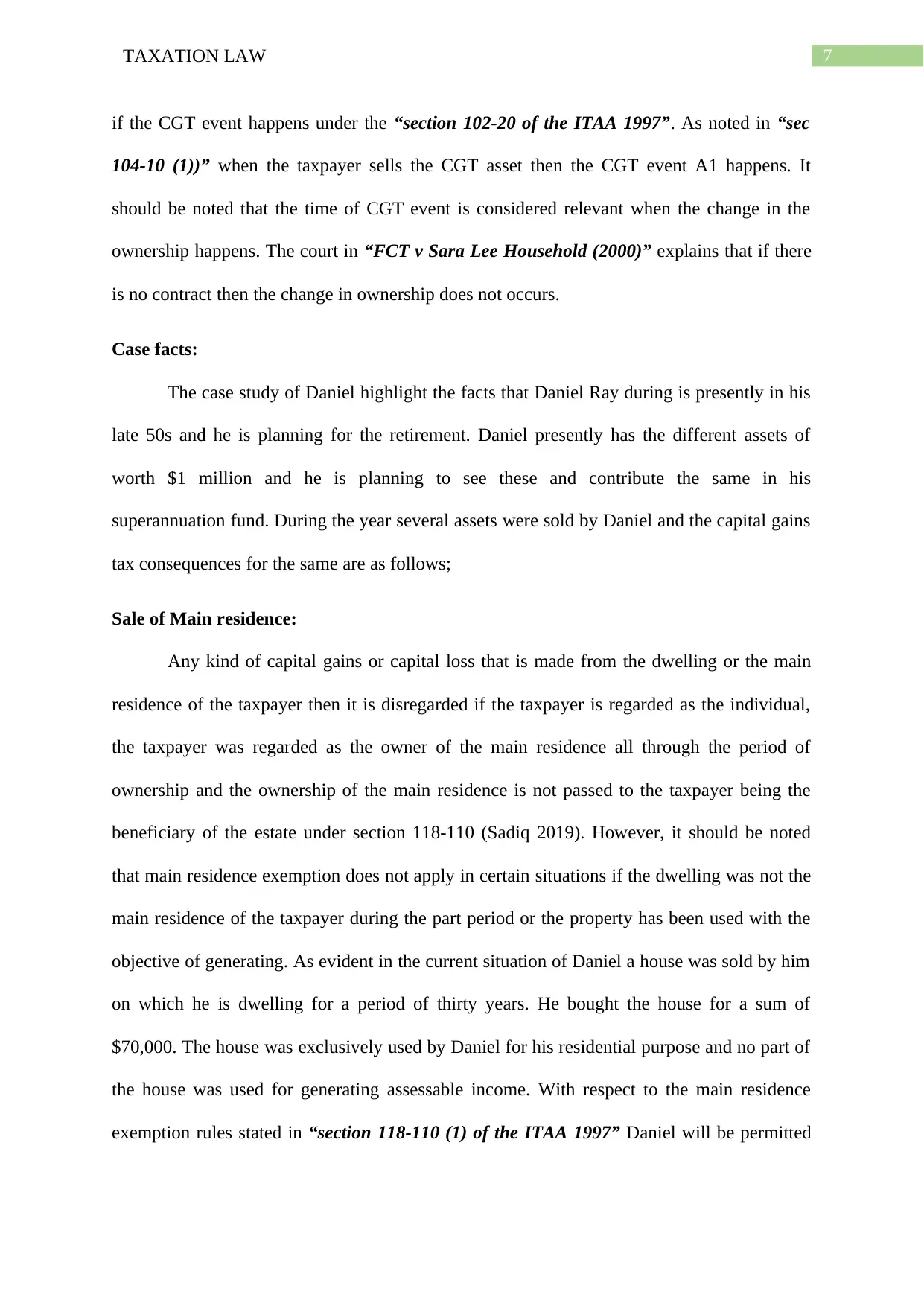

Computation of Deemed Interest:

The calculation that is done above explains that the deemed interest is computed with

reference to the formula that is given in the section 11 (2). In addition to this, the deemed

interest rate for the year 2018/19 is 5.25%. The above stated calculation explains that the

assessable value of the fringe benefit of the car is lower under the operating cost formula. An

advice can be given to Spiceco Pty Ltd the use of the operating cost method will be helpful in

reducing the FBT liability.

Answer to question 2:

Answer to A:

According to the “section 108-5, ITA Act 1997” a CGT asset is defined as any form

of property or the legal or equitable rights that does not amounts to property. Property is

generally defined as something that has the control over the shares, land or the interest in the

trust. The property can be either the tangible or the intangible shares or rights in the unit.

There are some of the situations where the capital gains tax is not applied on the capital gains

since there are other provisions in the tax law that is applicable instead (Morgan, Mortimer

and Pinto 2015). It is noteworthy to denote that the capital gains or capital loss is only made

Computation of Deemed Interest:

The calculation that is done above explains that the deemed interest is computed with

reference to the formula that is given in the section 11 (2). In addition to this, the deemed

interest rate for the year 2018/19 is 5.25%. The above stated calculation explains that the

assessable value of the fringe benefit of the car is lower under the operating cost formula. An

advice can be given to Spiceco Pty Ltd the use of the operating cost method will be helpful in

reducing the FBT liability.

Answer to question 2:

Answer to A:

According to the “section 108-5, ITA Act 1997” a CGT asset is defined as any form

of property or the legal or equitable rights that does not amounts to property. Property is

generally defined as something that has the control over the shares, land or the interest in the

trust. The property can be either the tangible or the intangible shares or rights in the unit.

There are some of the situations where the capital gains tax is not applied on the capital gains

since there are other provisions in the tax law that is applicable instead (Morgan, Mortimer

and Pinto 2015). It is noteworthy to denote that the capital gains or capital loss is only made

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

if the CGT event happens under the “section 102-20 of the ITAA 1997”. As noted in “sec

104-10 (1))” when the taxpayer sells the CGT asset then the CGT event A1 happens. It

should be noted that the time of CGT event is considered relevant when the change in the

ownership happens. The court in “FCT v Sara Lee Household (2000)” explains that if there

is no contract then the change in ownership does not occurs.

Case facts:

The case study of Daniel highlight the facts that Daniel Ray during is presently in his

late 50s and he is planning for the retirement. Daniel presently has the different assets of

worth $1 million and he is planning to see these and contribute the same in his

superannuation fund. During the year several assets were sold by Daniel and the capital gains

tax consequences for the same are as follows;

Sale of Main residence:

Any kind of capital gains or capital loss that is made from the dwelling or the main

residence of the taxpayer then it is disregarded if the taxpayer is regarded as the individual,

the taxpayer was regarded as the owner of the main residence all through the period of

ownership and the ownership of the main residence is not passed to the taxpayer being the

beneficiary of the estate under section 118-110 (Sadiq 2019). However, it should be noted

that main residence exemption does not apply in certain situations if the dwelling was not the

main residence of the taxpayer during the part period or the property has been used with the

objective of generating. As evident in the current situation of Daniel a house was sold by him

on which he is dwelling for a period of thirty years. He bought the house for a sum of

$70,000. The house was exclusively used by Daniel for his residential purpose and no part of

the house was used for generating assessable income. With respect to the main residence

exemption rules stated in “section 118-110 (1) of the ITAA 1997” Daniel will be permitted

if the CGT event happens under the “section 102-20 of the ITAA 1997”. As noted in “sec

104-10 (1))” when the taxpayer sells the CGT asset then the CGT event A1 happens. It

should be noted that the time of CGT event is considered relevant when the change in the

ownership happens. The court in “FCT v Sara Lee Household (2000)” explains that if there

is no contract then the change in ownership does not occurs.

Case facts:

The case study of Daniel highlight the facts that Daniel Ray during is presently in his

late 50s and he is planning for the retirement. Daniel presently has the different assets of

worth $1 million and he is planning to see these and contribute the same in his

superannuation fund. During the year several assets were sold by Daniel and the capital gains

tax consequences for the same are as follows;

Sale of Main residence:

Any kind of capital gains or capital loss that is made from the dwelling or the main

residence of the taxpayer then it is disregarded if the taxpayer is regarded as the individual,

the taxpayer was regarded as the owner of the main residence all through the period of

ownership and the ownership of the main residence is not passed to the taxpayer being the

beneficiary of the estate under section 118-110 (Sadiq 2019). However, it should be noted

that main residence exemption does not apply in certain situations if the dwelling was not the

main residence of the taxpayer during the part period or the property has been used with the

objective of generating. As evident in the current situation of Daniel a house was sold by him

on which he is dwelling for a period of thirty years. He bought the house for a sum of

$70,000. The house was exclusively used by Daniel for his residential purpose and no part of

the house was used for generating assessable income. With respect to the main residence

exemption rules stated in “section 118-110 (1) of the ITAA 1997” Daniel will be permitted

8TAXATION LAW

to obtain the main residence exemption from the capital gains that will be made from the

disposal of house.

Sale of Painting:

As explained in section 108-10, ITAA 1997 collectable can be defined as the asset

that are mainly used by the taxpayer or kept by the taxpayer for their private usage and

enjoyment of the taxpayer. Accordingly in sec 108-10 (2), collectables mainly include the

antiques and jewellery, art work, rare stamps, coins etc. As understood in the current state of

Daniel it is understood that he bought an artistic painting during 20th September 1985.

Accordingly, it can be explained that the painting is a post-CGT asset that is bought

following the introduction of CGT regime (Woellner et al. 2014). The sale of painting has

resulted in CGT event A1 under section 104-10 (1), ITAA 1997. The capital gains that is

made by Daniel following the sale of painting is the taxable gains and under the section 102-

5, ITAA 1997 the gains will be included into the net income of Daniel.

Sale of Luxury Yacht:

As explained in sec 108-20, ITAA 1997, CGT asset is regarded namely the personal

use asset that are mainly used or kept for the private enjoyment of the taxpayer under sec

108-20 of the ITA Act 1997. There are some kinds of special rules that is applied on the

private use assets (Sadiq 2019). Any kind of capital gains that is made for the asset that is

purchased for less than the $10,000 then the capital gains should be ignored. On the other

hand section 108-20 (1), explains that the capital loss that are made from the sale of the

private use assets should be regularly ignored.

The case study explains that a luxury yacht was purchased by the Daniel for a cost of

$110,000. However on the 1st June 2019 the Yacht was eventually sold by Daniel for a sale

value of $60,000. As understood that there has been a loss from the sale of yacht. Making the

to obtain the main residence exemption from the capital gains that will be made from the

disposal of house.

Sale of Painting:

As explained in section 108-10, ITAA 1997 collectable can be defined as the asset

that are mainly used by the taxpayer or kept by the taxpayer for their private usage and

enjoyment of the taxpayer. Accordingly in sec 108-10 (2), collectables mainly include the

antiques and jewellery, art work, rare stamps, coins etc. As understood in the current state of

Daniel it is understood that he bought an artistic painting during 20th September 1985.

Accordingly, it can be explained that the painting is a post-CGT asset that is bought

following the introduction of CGT regime (Woellner et al. 2014). The sale of painting has

resulted in CGT event A1 under section 104-10 (1), ITAA 1997. The capital gains that is

made by Daniel following the sale of painting is the taxable gains and under the section 102-

5, ITAA 1997 the gains will be included into the net income of Daniel.

Sale of Luxury Yacht:

As explained in sec 108-20, ITAA 1997, CGT asset is regarded namely the personal

use asset that are mainly used or kept for the private enjoyment of the taxpayer under sec

108-20 of the ITA Act 1997. There are some kinds of special rules that is applied on the

private use assets (Sadiq 2019). Any kind of capital gains that is made for the asset that is

purchased for less than the $10,000 then the capital gains should be ignored. On the other

hand section 108-20 (1), explains that the capital loss that are made from the sale of the

private use assets should be regularly ignored.

The case study explains that a luxury yacht was purchased by the Daniel for a cost of

$110,000. However on the 1st June 2019 the Yacht was eventually sold by Daniel for a sale

value of $60,000. As understood that there has been a loss from the sale of yacht. Making the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

reference of section 108-20 (1) the capital loss derived from the personal use asset should be

simply ignored by Daniel.

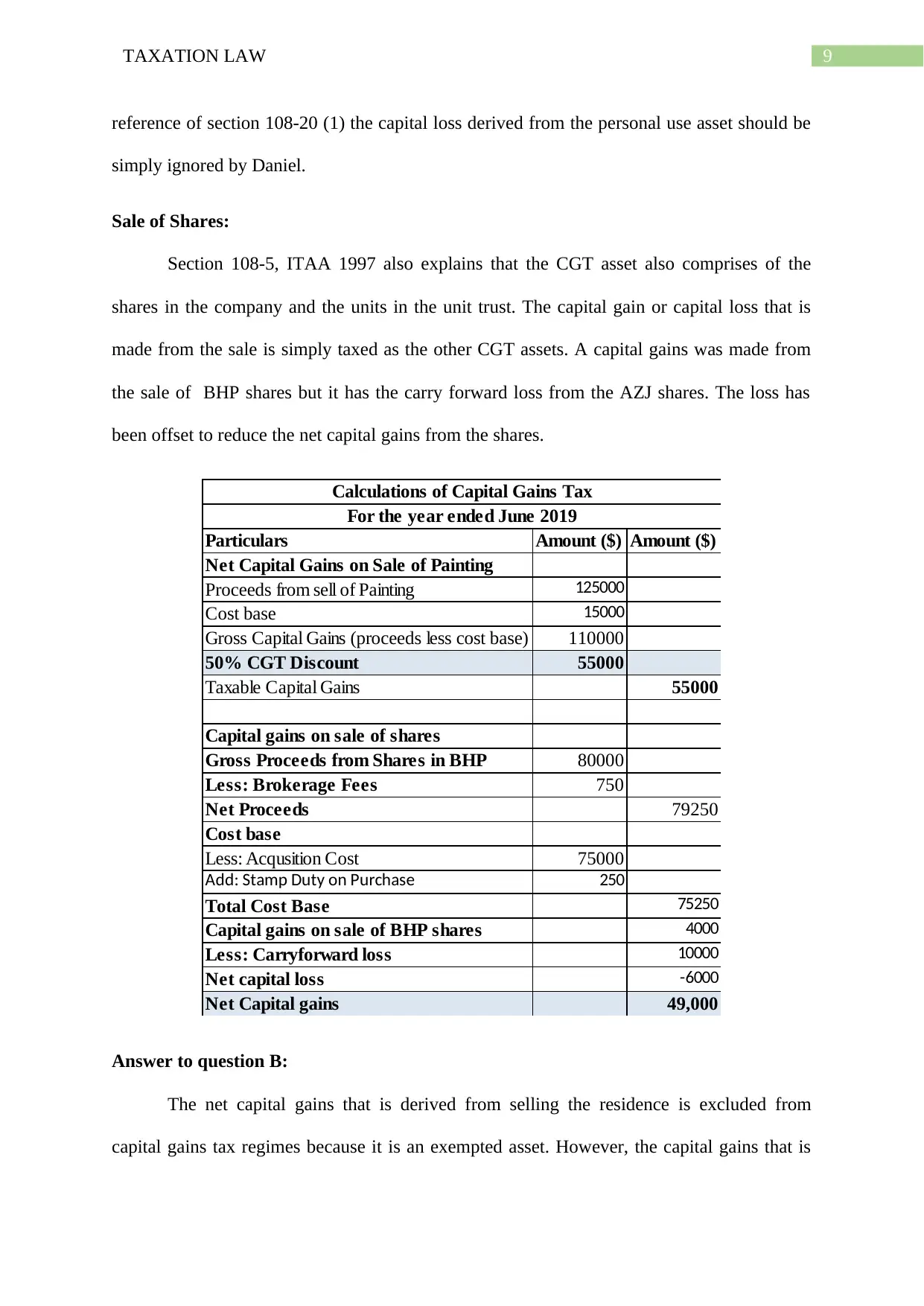

Sale of Shares:

Section 108-5, ITAA 1997 also explains that the CGT asset also comprises of the

shares in the company and the units in the unit trust. The capital gain or capital loss that is

made from the sale is simply taxed as the other CGT assets. A capital gains was made from

the sale of BHP shares but it has the carry forward loss from the AZJ shares. The loss has

been offset to reduce the net capital gains from the shares.

Particulars Amount ($) Amount ($)

Net Capital Gains on Sale of Painting

Proceeds from sell of Painting 125000

Cost base 15000

Gross Capital Gains (proceeds less cost base) 110000

50% CGT Discount 55000

Taxable Capital Gains 55000

Capital gains on sale of shares

Gross Proceeds from Shares in BHP 80000

Less: Brokerage Fees 750

Net Proceeds 79250

Cost base

Less: Acqusition Cost 75000

Add: Stamp Duty on Purchase 250

Total Cost Base 75250

Capital gains on sale of BHP shares 4000

Less: Carryforward loss 10000

Net capital loss -6000

Net Capital gains 49,000

Calculations of Capital Gains Tax

For the year ended June 2019

Answer to question B:

The net capital gains that is derived from selling the residence is excluded from

capital gains tax regimes because it is an exempted asset. However, the capital gains that is

reference of section 108-20 (1) the capital loss derived from the personal use asset should be

simply ignored by Daniel.

Sale of Shares:

Section 108-5, ITAA 1997 also explains that the CGT asset also comprises of the

shares in the company and the units in the unit trust. The capital gain or capital loss that is

made from the sale is simply taxed as the other CGT assets. A capital gains was made from

the sale of BHP shares but it has the carry forward loss from the AZJ shares. The loss has

been offset to reduce the net capital gains from the shares.

Particulars Amount ($) Amount ($)

Net Capital Gains on Sale of Painting

Proceeds from sell of Painting 125000

Cost base 15000

Gross Capital Gains (proceeds less cost base) 110000

50% CGT Discount 55000

Taxable Capital Gains 55000

Capital gains on sale of shares

Gross Proceeds from Shares in BHP 80000

Less: Brokerage Fees 750

Net Proceeds 79250

Cost base

Less: Acqusition Cost 75000

Add: Stamp Duty on Purchase 250

Total Cost Base 75250

Capital gains on sale of BHP shares 4000

Less: Carryforward loss 10000

Net capital loss -6000

Net Capital gains 49,000

Calculations of Capital Gains Tax

For the year ended June 2019

Answer to question B:

The net capital gains that is derived from selling the residence is excluded from

capital gains tax regimes because it is an exempted asset. However, the capital gains that is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

derived from the disposal of painting can be used by Daniel to fund it in his superannuation

fund.

Answer to question C:

A capital loss is also reported from the disposal of Yacht and a carry forward loss of

AZJ shares has been used to offset the gains from BHP shares. An advice can be given to

David that capital loss can be carried forward by Daniel to subsequent years as no capital

gains has been reported from personal use asset.

References:

Barkoczy, S. 2014. Foundations of taxation law 2014.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2015. Principles of business taxation.

Jover-Ledesma, G. 2015. Principles of business taxation 2015. [Place of publication not

identified]: Cch Incorporated.

Kenny, P. 2013. Australian tax. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. 2013. Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Morgan, A., Mortimer, C. and Pinto, D. 2015. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Sadiq, K. 2019. Principles of taxation law 2019.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D. 2014. Australian taxation

law 2014.

derived from the disposal of painting can be used by Daniel to fund it in his superannuation

fund.

Answer to question C:

A capital loss is also reported from the disposal of Yacht and a carry forward loss of

AZJ shares has been used to offset the gains from BHP shares. An advice can be given to

David that capital loss can be carried forward by Daniel to subsequent years as no capital

gains has been reported from personal use asset.

References:

Barkoczy, S. 2014. Foundations of taxation law 2014.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2015. Principles of business taxation.

Jover-Ledesma, G. 2015. Principles of business taxation 2015. [Place of publication not

identified]: Cch Incorporated.

Kenny, P. 2013. Australian tax. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. 2013. Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Morgan, A., Mortimer, C. and Pinto, D. 2015. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Sadiq, K. 2019. Principles of taxation law 2019.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D. 2014. Australian taxation

law 2014.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.