ACC3TAX S1 2019 Group Report: Taxation Law for Chris Matthews

VerifiedAdded on 2022/11/29

|8

|1423

|426

Report

AI Summary

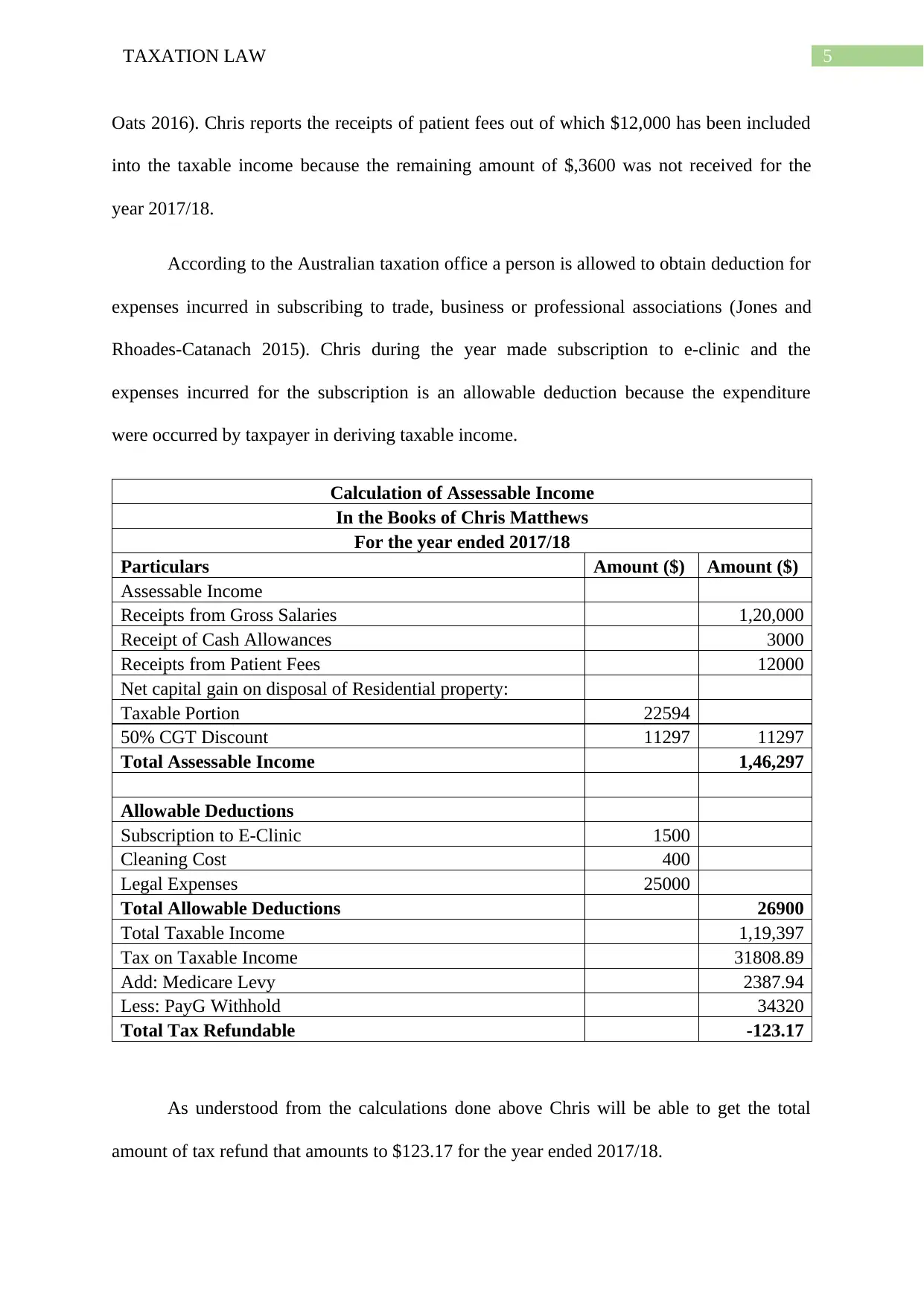

This report examines the tax implications for Chris Matthews, focusing on transactions related to his employment and personal consultancy business. It analyzes capital gains from the sale of his main residence, considering the partial main residence exemption due to business use of the property. The report also assesses the deductibility of legal fees incurred in defending negligence claims, referencing relevant legislation and case law. Furthermore, it calculates Chris's taxable income, incorporating salary, allowances, patient fees, and allowable deductions such as subscription fees and cleaning costs. The final computation determines his total tax liability and potential tax refund for the year 2017/18, providing a comprehensive overview of his tax position.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.