Taxation Law Report: Assessing Income, Deductions, and Tax Liabilities

VerifiedAdded on 2021/05/31

|9

|1659

|21

Report

AI Summary

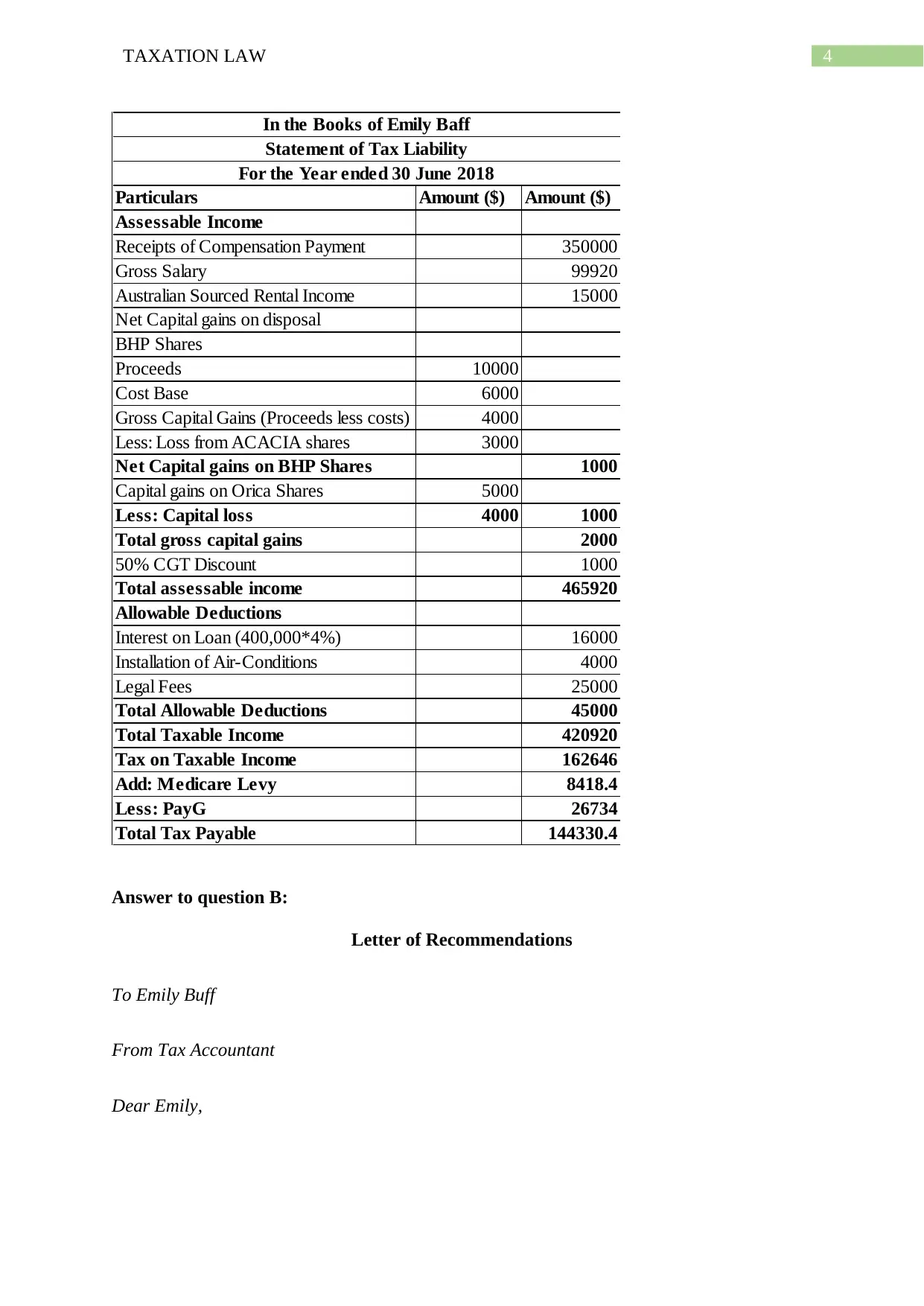

This report analyzes a taxation law assignment, addressing income assessment, deductions, and capital gains tax. It examines a scenario involving an individual's assessable income, allowable deductions (including interest expenses on investment property, capital works, and repairs), and capital gains from share sales, as well as losses. The report also includes a letter of advice concerning compensation payments and legal expenditure, addressing the taxation of compensation for lost earnings, discriminatory pay, and the deductibility of legal expenses incurred in pursuing claims against an employer. The analysis references relevant sections of the ITAA 1936 and ITAA 1997, along with case law such as Western Suburbs Cinemas v Federal Commissioner of Taxation and Hallstorm Pty Ltd v Federal Commissioner of Taxation, providing a comprehensive overview of taxation principles and their application in the given scenarios. The report concludes with a list of references.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.