Taxation Law Assignment: Residency, Income, Benefits, and Taxation

VerifiedAdded on 2023/04/21

|9

|1949

|445

Report

AI Summary

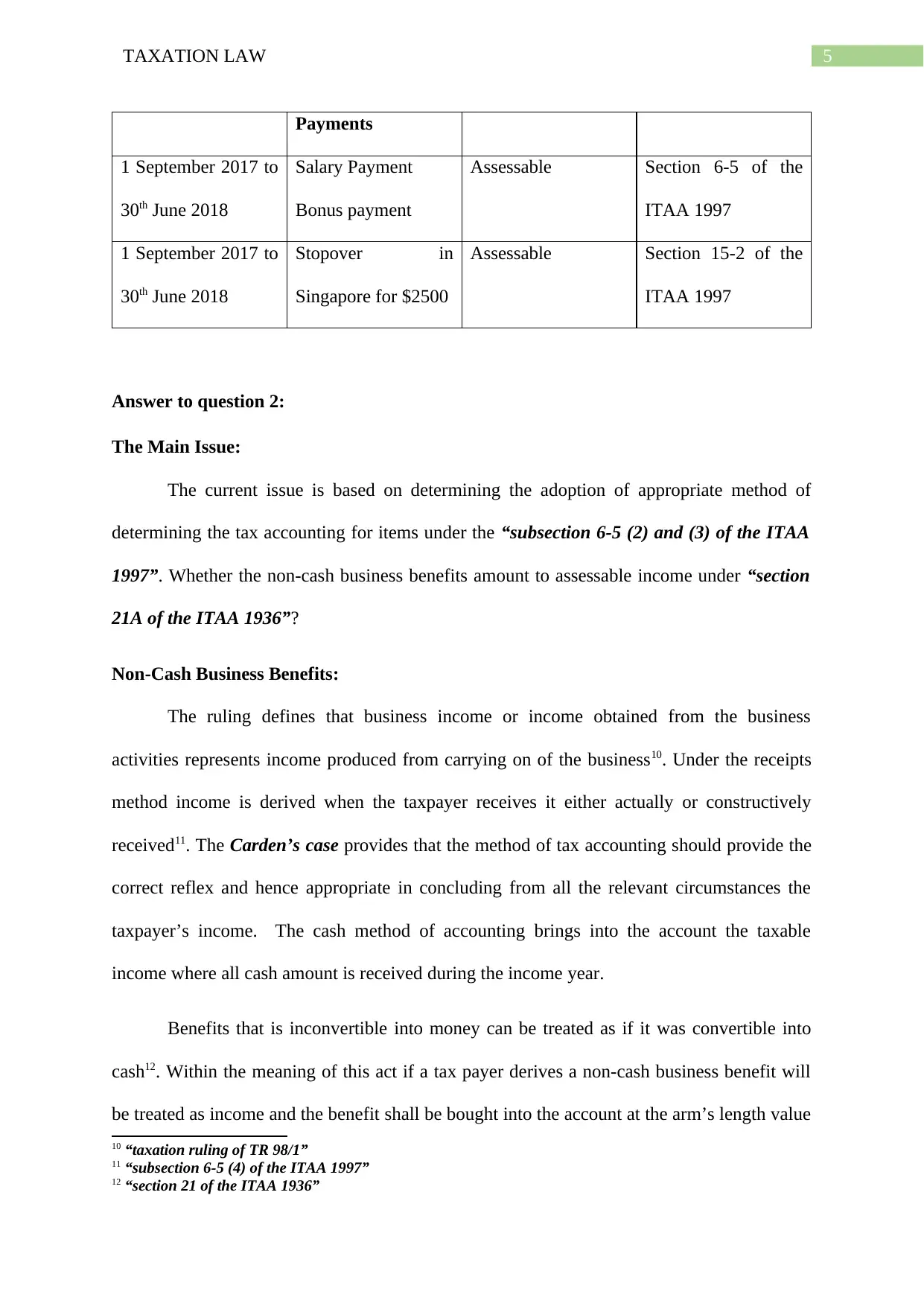

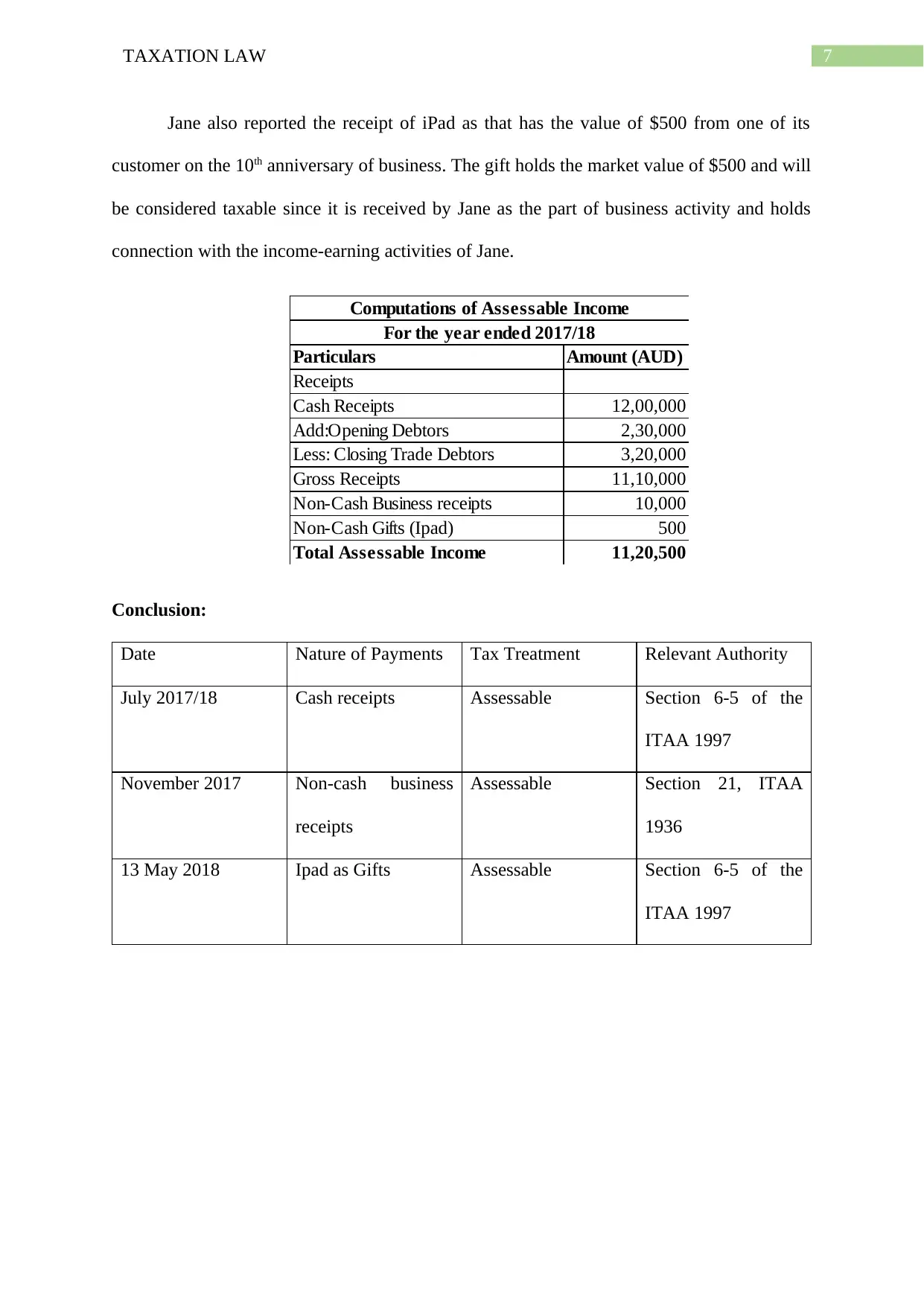

This assignment report analyzes two key taxation law questions. The first question examines Mary Joseph's residency status in Australia, considering the 183-day test, domicile, and her intention to reside in Australia for ten years. It assesses the assessability of her income, including salary, bonuses, and a stopover benefit, referencing relevant sections of the ITAA 1997 and case law. The report also addresses the Australia-UK Double Taxation Agreement concerning her rental and bank interest income. The second question investigates the tax treatment of non-cash business benefits, specifically focusing on the case of Jimmy and Jane's retail business. It explores the application of section 21 of the ITAA 1936 and the cash accounting method, determining whether free overseas holidays and gifts constitute assessable income. The report provides detailed computations of assessable income for both scenarios, citing relevant rulings and case law to support its conclusions.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.