Taxation Law Report: Tax Treatments for Technology Computer Pty Ltd

VerifiedAdded on 2023/06/03

|13

|1670

|282

Report

AI Summary

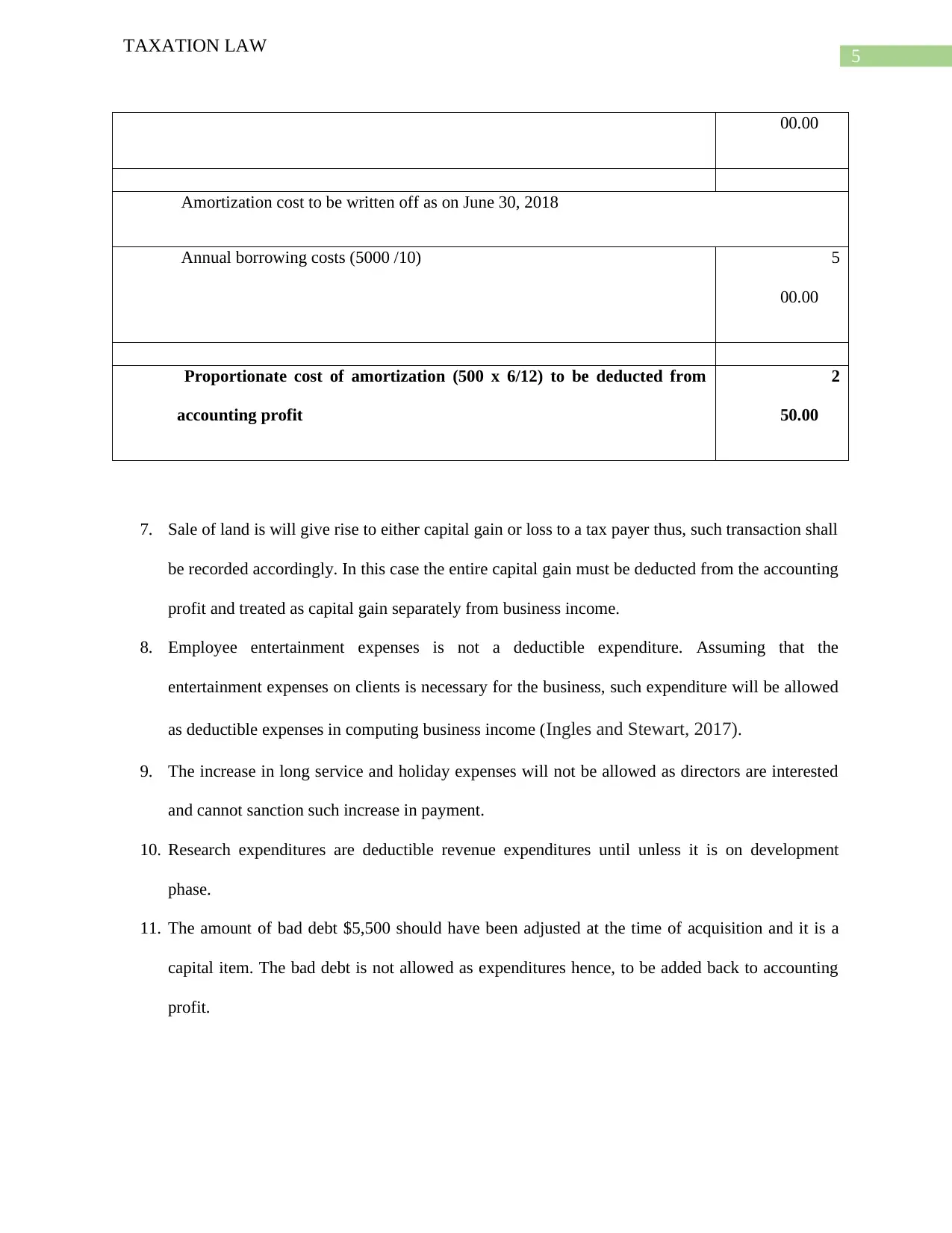

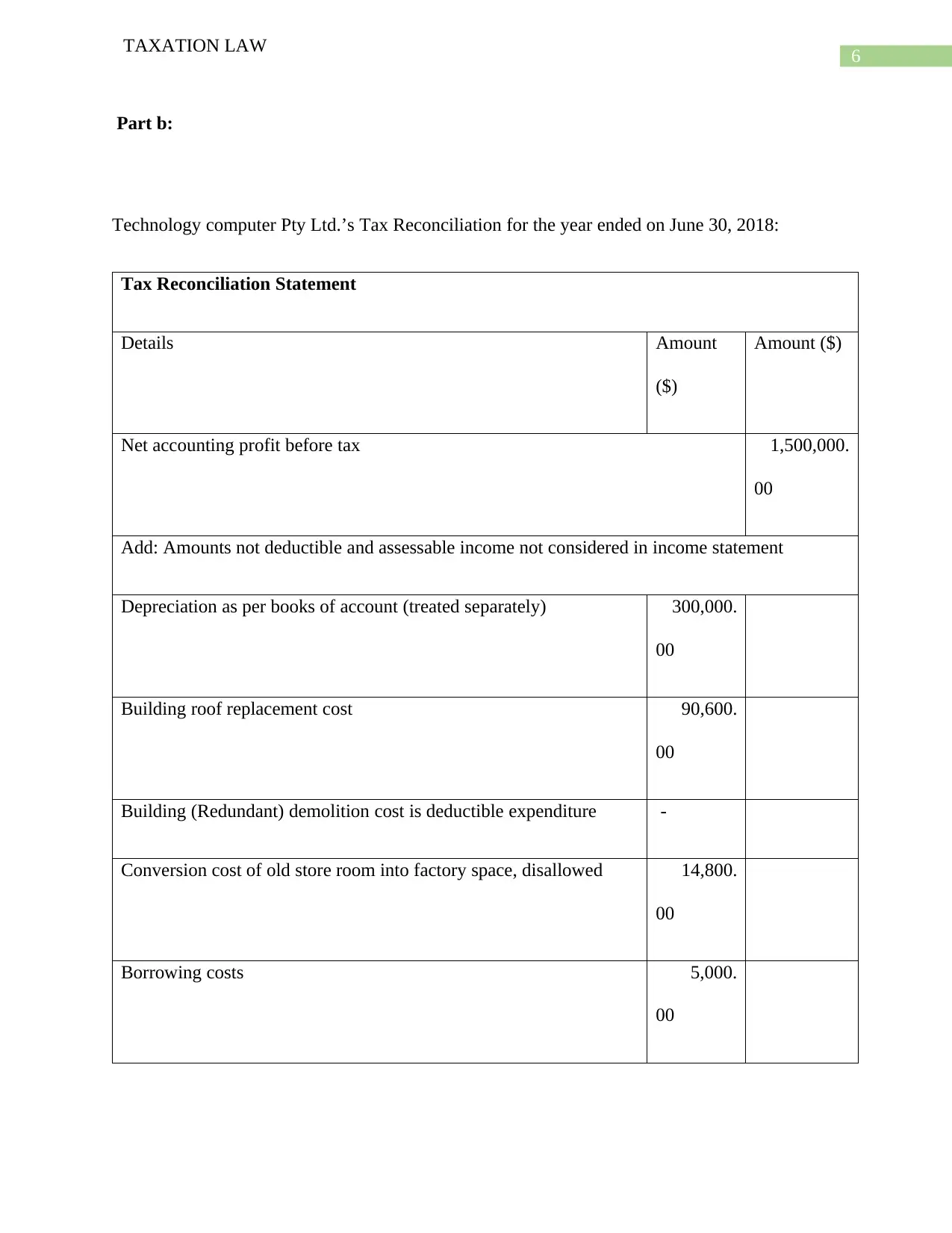

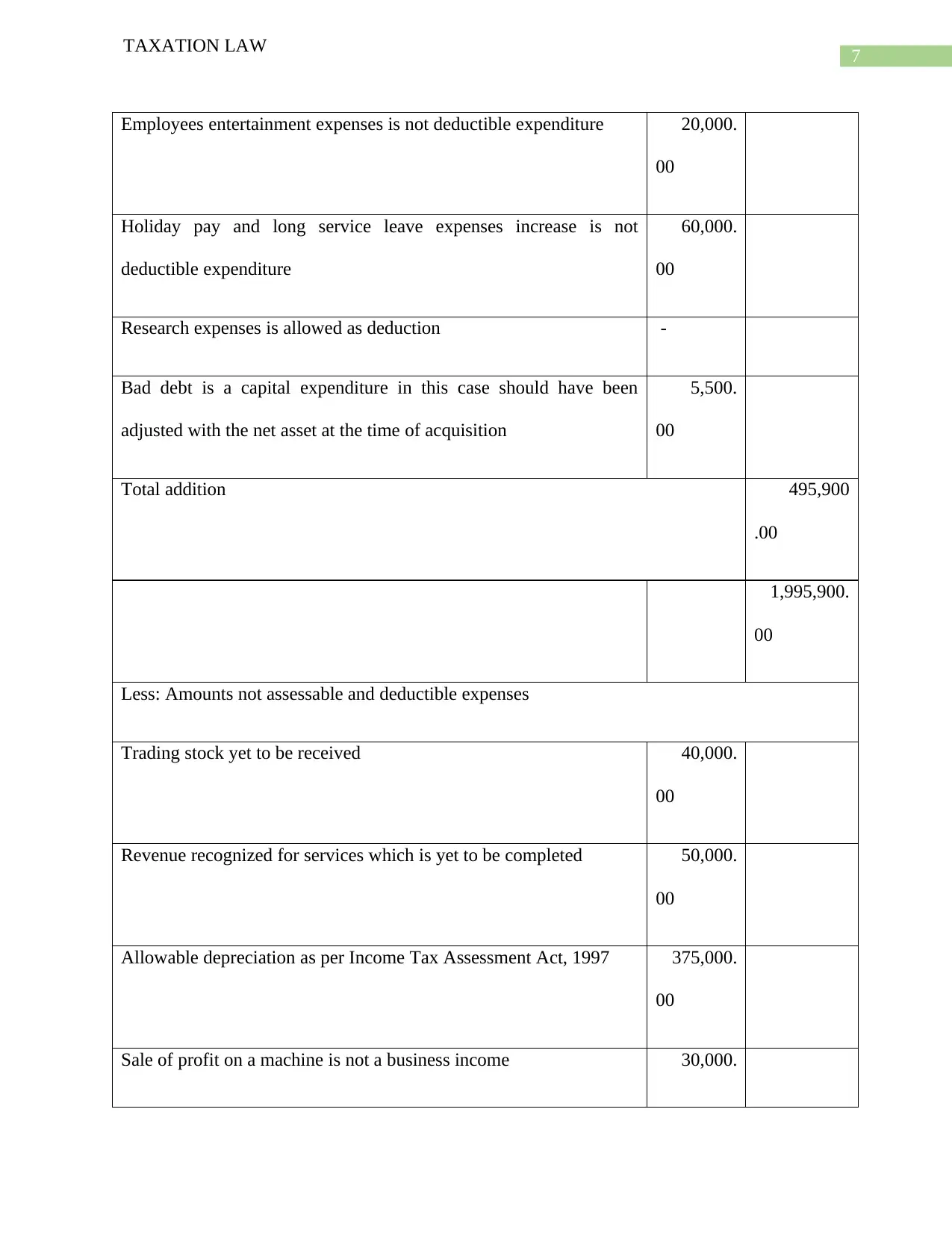

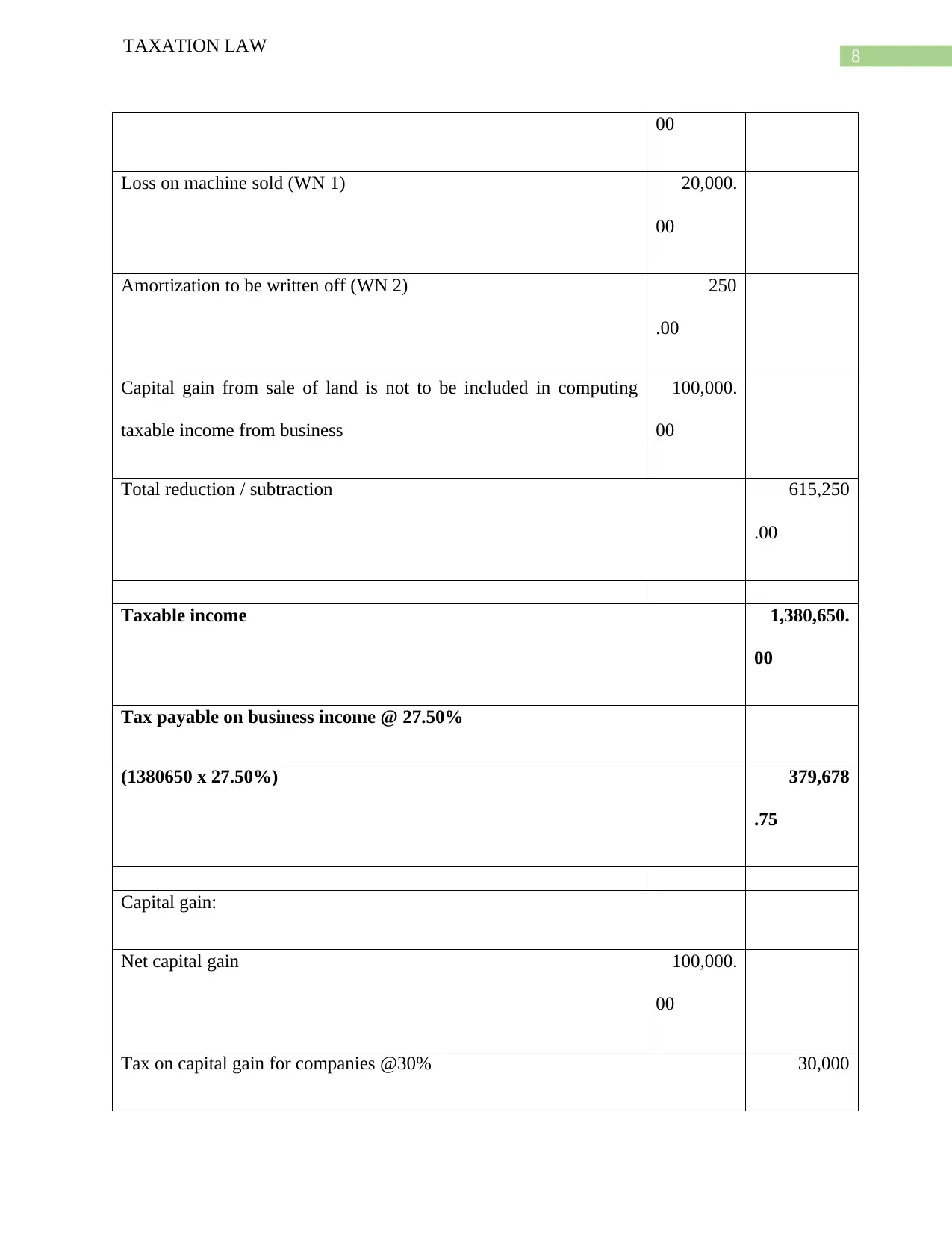

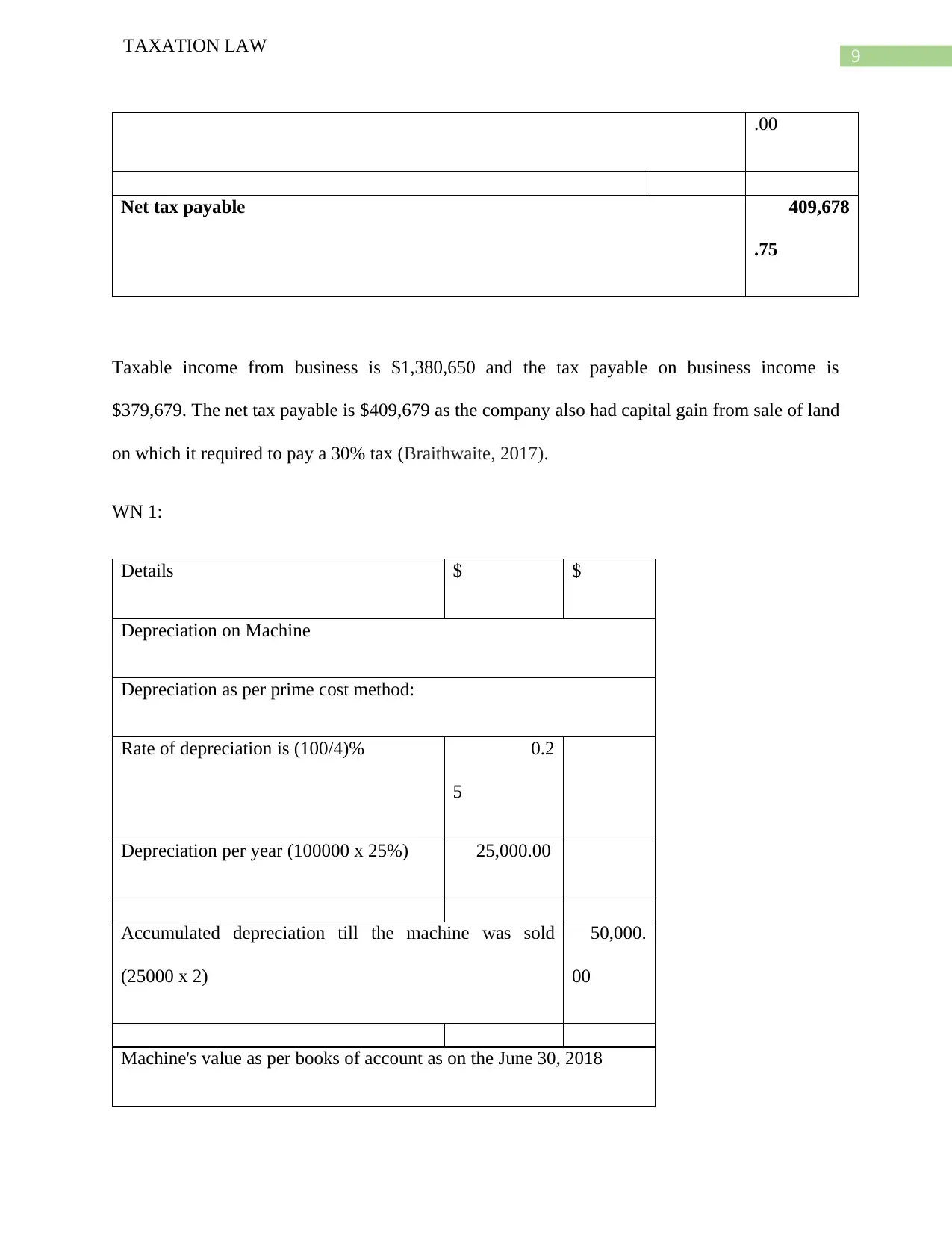

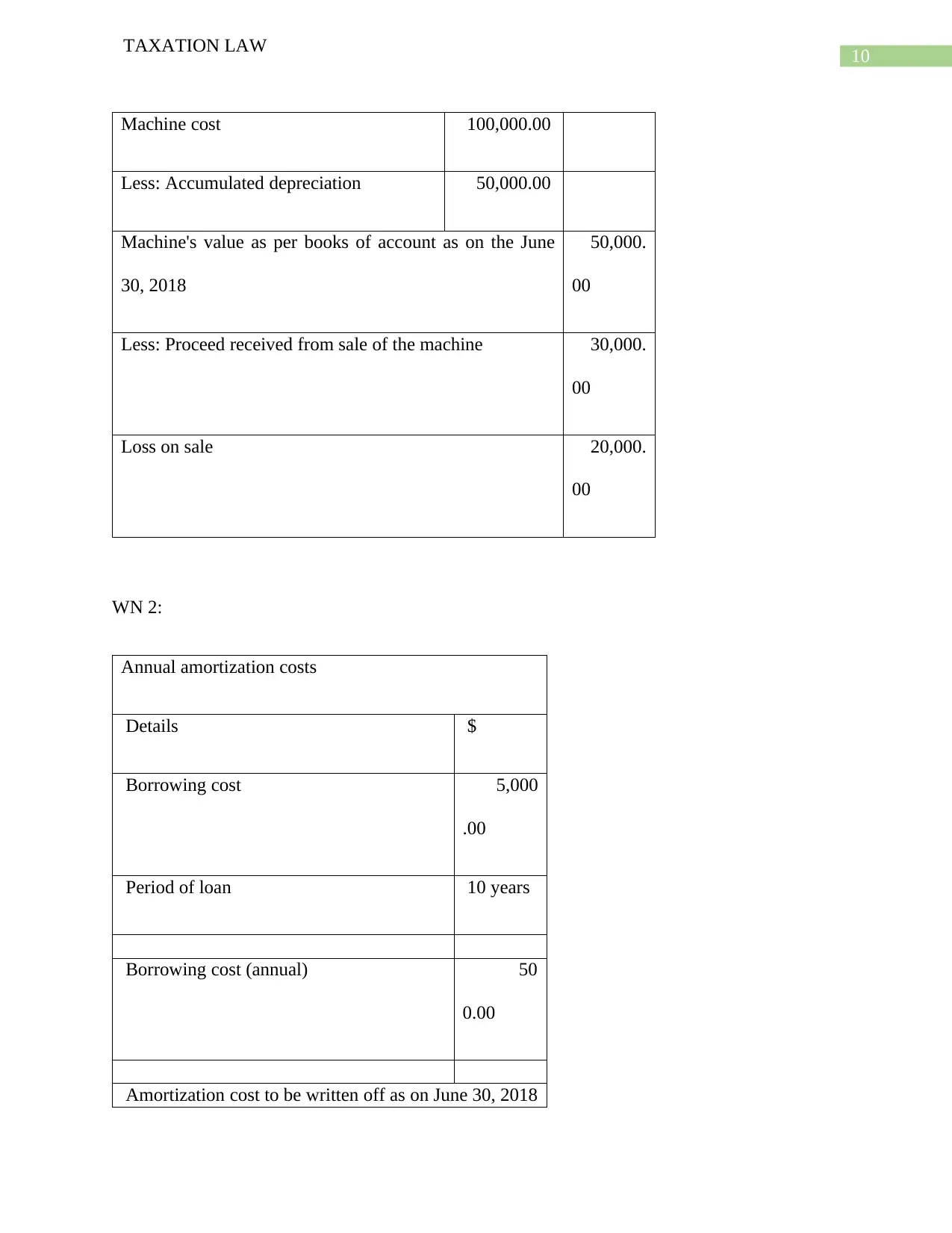

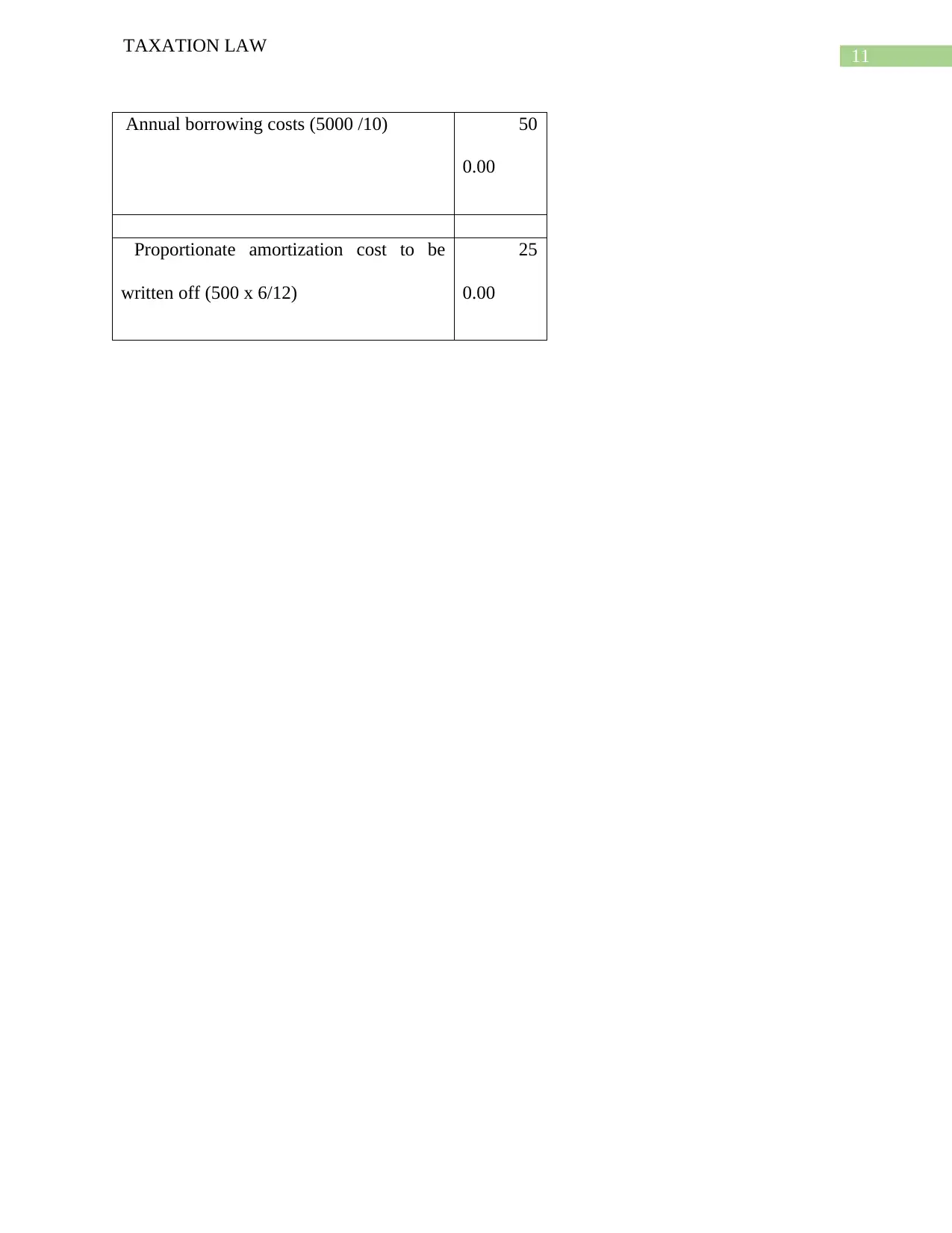

This report provides a detailed analysis of Australian taxation law, specifically focusing on the tax treatments for Technology Computer Pty Ltd for the income year ending June 30, 2018. The report examines various financial transactions, including trading stock, service revenue, depreciation, sale of assets, repair and maintenance costs, borrowing costs, sale of land, employee entertainment expenses, and research expenditures, along with bad debts. The analysis is based on the provisions of the Income Tax Assessment Act 1997 (ITAA 1997) and relevant Australian Taxation Office (ATO) guidelines. Part A of the report details the tax treatments for each item, while Part B presents a tax reconciliation statement, calculating taxable income and the tax payable. The report also includes detailed workings for depreciation and borrowing costs. The net tax payable is calculated considering both business income and capital gains. The report is a comprehensive guide to understanding taxation law in the Australian context.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.