Taxation of Timber Revenue in Australia

VerifiedAdded on 2020/03/28

|13

|2541

|38

AI Summary

This assignment delves into the taxation implications of earning income from cutting timber in Australia. It analyzes the Income Tax Assessment Act 1997 (ITAA 1997) and its provisions, particularly Section 6(1), which defines taxable income. The discussion considers the potential application of Subsection 26(f) regarding royalties received for timber harvesting rights.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW, THEORY AND PRACTICE

Taxation Law, Theory and Practice

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation Law, Theory and Practice

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW, THEORY AND PRACTICE

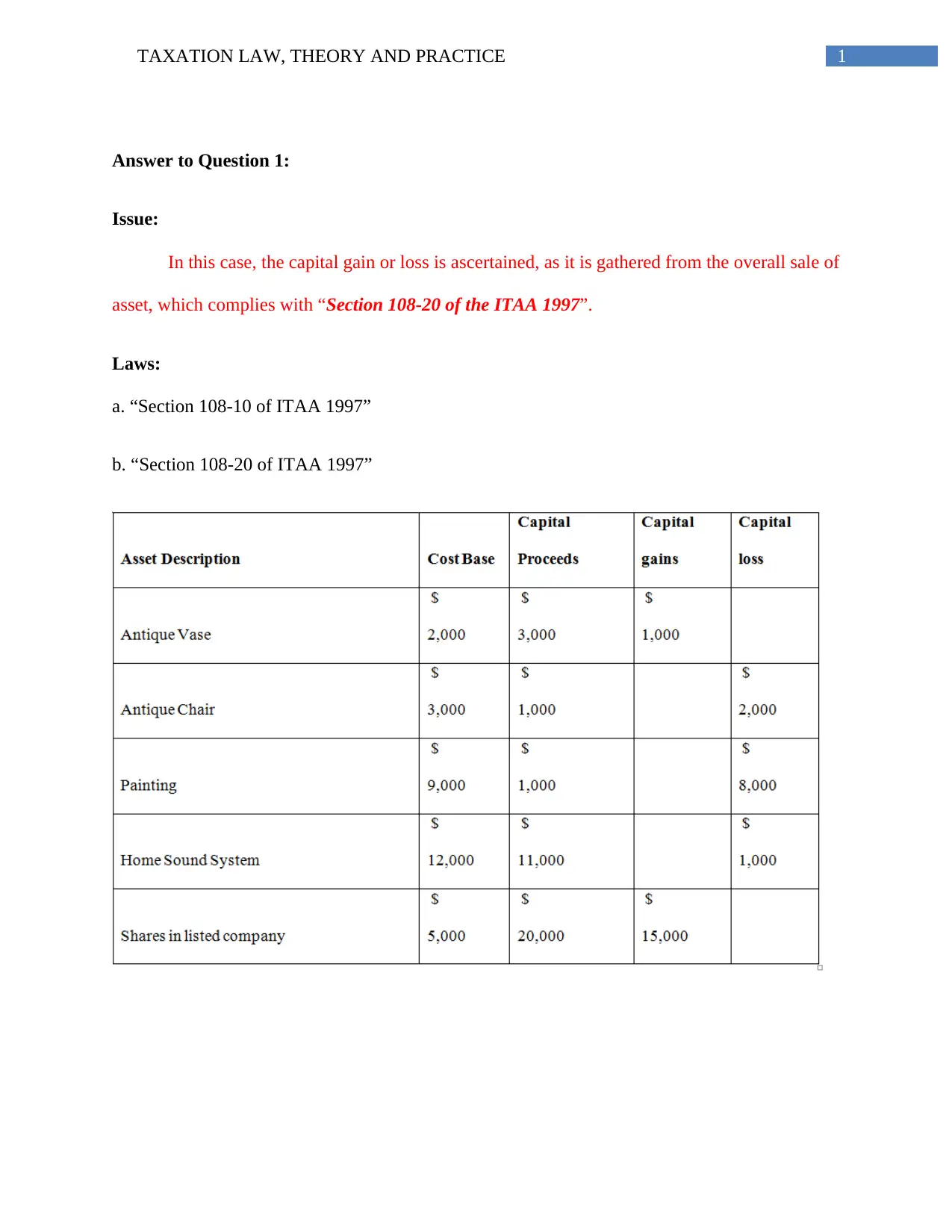

Answer to Question 1:

Issue:

In this case, the capital gain or loss is ascertained, as it is gathered from the overall sale of

asset, which complies with “Section 108-20 of the ITAA 1997”.

Laws:

a. “Section 108-10 of ITAA 1997”

b. “Section 108-20 of ITAA 1997”

Answer to Question 1:

Issue:

In this case, the capital gain or loss is ascertained, as it is gathered from the overall sale of

asset, which complies with “Section 108-20 of the ITAA 1997”.

Laws:

a. “Section 108-10 of ITAA 1997”

b. “Section 108-20 of ITAA 1997”

2TAXATION LAW, THEORY AND PRACTICE

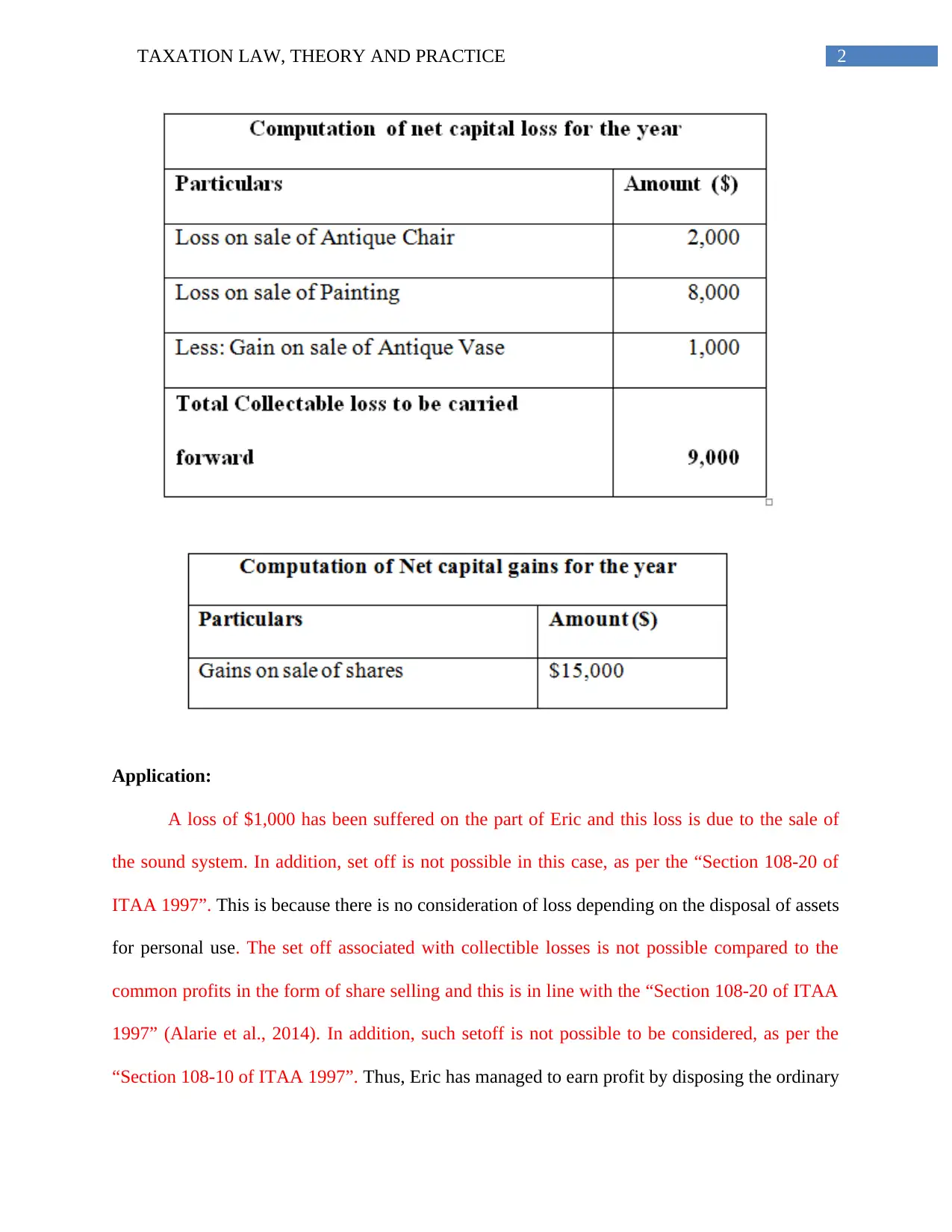

Application:

A loss of $1,000 has been suffered on the part of Eric and this loss is due to the sale of

the sound system. In addition, set off is not possible in this case, as per the “Section 108-20 of

ITAA 1997”. This is because there is no consideration of loss depending on the disposal of assets

for personal use. The set off associated with collectible losses is not possible compared to the

common profits in the form of share selling and this is in line with the “Section 108-20 of ITAA

1997” (Alarie et al., 2014). In addition, such setoff is not possible to be considered, as per the

“Section 108-10 of ITAA 1997”. Thus, Eric has managed to earn profit by disposing the ordinary

Application:

A loss of $1,000 has been suffered on the part of Eric and this loss is due to the sale of

the sound system. In addition, set off is not possible in this case, as per the “Section 108-20 of

ITAA 1997”. This is because there is no consideration of loss depending on the disposal of assets

for personal use. The set off associated with collectible losses is not possible compared to the

common profits in the form of share selling and this is in line with the “Section 108-20 of ITAA

1997” (Alarie et al., 2014). In addition, such setoff is not possible to be considered, as per the

“Section 108-10 of ITAA 1997”. Thus, Eric has managed to earn profit by disposing the ordinary

3TAXATION LAW, THEORY AND PRACTICE

assets and there is absence of existing year ordinary capital or other types of applicable

minimisations (Joseph, 2014). Moreover, the overall capital gain of Eric is obtained as $15,000.

Conclusion:

From the above evaluation, it could be inferred that Eric could not offset the overall loss

accumulated from collectibles, as the profit is made by disposing only the ordinary assets.

Answer to Question 2:

Issue:

The provided case study primarily suggests the issue pertaining to the ascertainment of

“Fringe Benefit Tax (FBT)” with special adherence to the “Taxation Ruling of TR 93/6”.

Laws:

a. Taxation Ruling of TR 93/6

Application:

Calculation of fringe tax benefits (FBT):

assets and there is absence of existing year ordinary capital or other types of applicable

minimisations (Joseph, 2014). Moreover, the overall capital gain of Eric is obtained as $15,000.

Conclusion:

From the above evaluation, it could be inferred that Eric could not offset the overall loss

accumulated from collectibles, as the profit is made by disposing only the ordinary assets.

Answer to Question 2:

Issue:

The provided case study primarily suggests the issue pertaining to the ascertainment of

“Fringe Benefit Tax (FBT)” with special adherence to the “Taxation Ruling of TR 93/6”.

Laws:

a. Taxation Ruling of TR 93/6

Application:

Calculation of fringe tax benefits (FBT):

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW, THEORY AND PRACTICE

5TAXATION LAW, THEORY AND PRACTICE

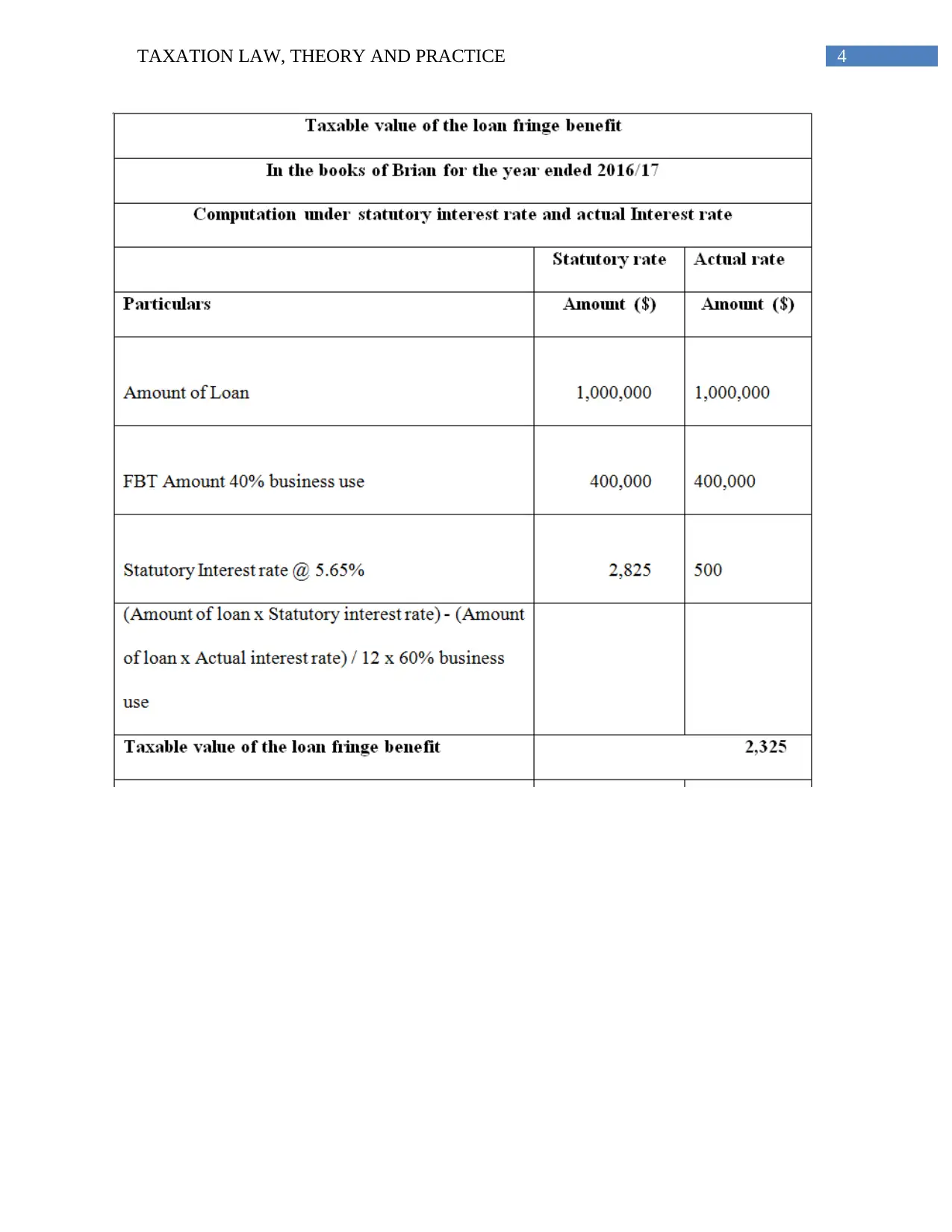

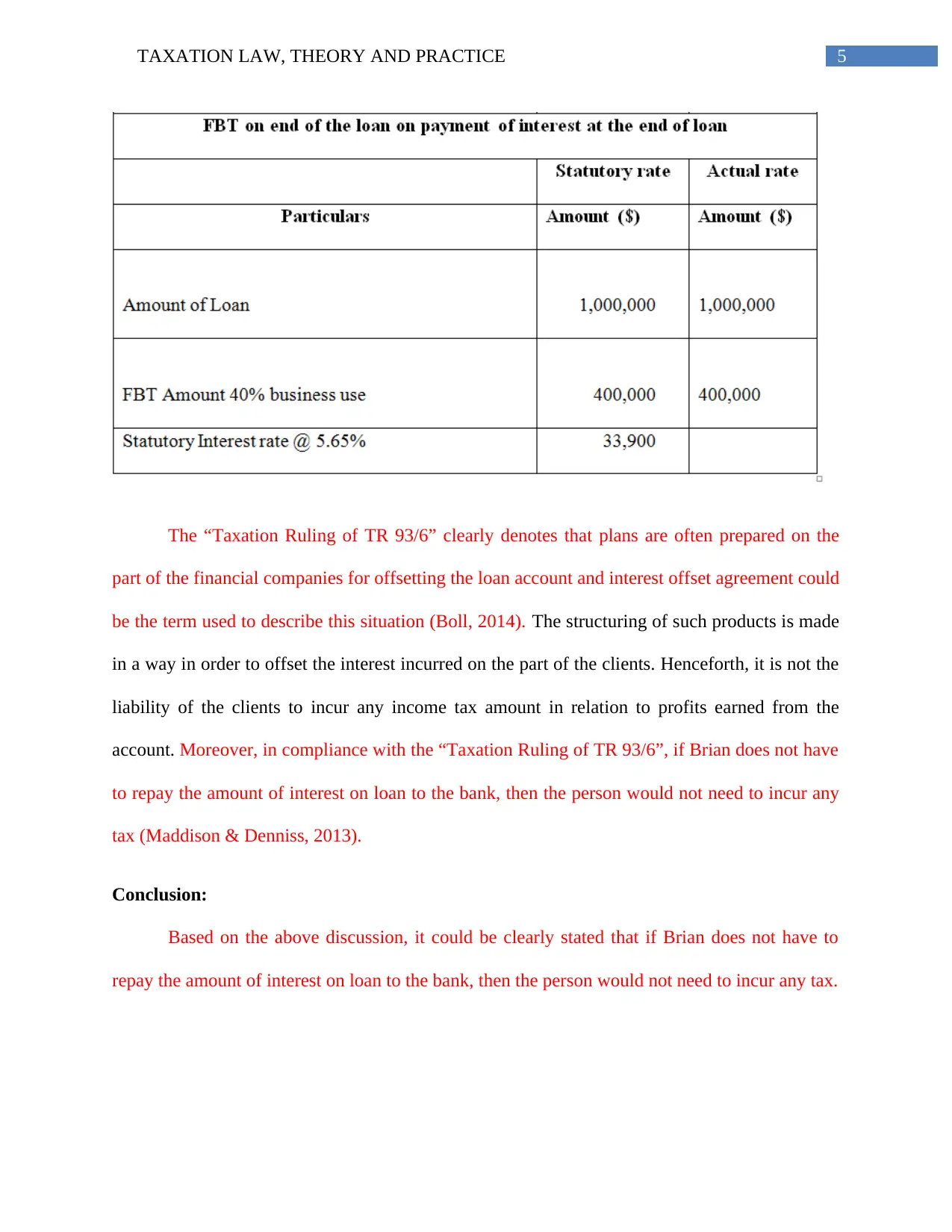

The “Taxation Ruling of TR 93/6” clearly denotes that plans are often prepared on the

part of the financial companies for offsetting the loan account and interest offset agreement could

be the term used to describe this situation (Boll, 2014). The structuring of such products is made

in a way in order to offset the interest incurred on the part of the clients. Henceforth, it is not the

liability of the clients to incur any income tax amount in relation to profits earned from the

account. Moreover, in compliance with the “Taxation Ruling of TR 93/6”, if Brian does not have

to repay the amount of interest on loan to the bank, then the person would not need to incur any

tax (Maddison & Denniss, 2013).

Conclusion:

Based on the above discussion, it could be clearly stated that if Brian does not have to

repay the amount of interest on loan to the bank, then the person would not need to incur any tax.

The “Taxation Ruling of TR 93/6” clearly denotes that plans are often prepared on the

part of the financial companies for offsetting the loan account and interest offset agreement could

be the term used to describe this situation (Boll, 2014). The structuring of such products is made

in a way in order to offset the interest incurred on the part of the clients. Henceforth, it is not the

liability of the clients to incur any income tax amount in relation to profits earned from the

account. Moreover, in compliance with the “Taxation Ruling of TR 93/6”, if Brian does not have

to repay the amount of interest on loan to the bank, then the person would not need to incur any

tax (Maddison & Denniss, 2013).

Conclusion:

Based on the above discussion, it could be clearly stated that if Brian does not have to

repay the amount of interest on loan to the bank, then the person would not need to incur any tax.

6TAXATION LAW, THEORY AND PRACTICE

Answer to Question 3:

Issue:

The current case study primarily denotes that such issue is concerned with the loss

distribution gathered from the rental property as joint ownership and the partners include Jack

and Jill.

Laws:

a. Taxation Ruling of TR 93/32

b. Section 51 of ITAA 1997

c. F.C. of T v McDonald (1987)

Application:

Based on the “Taxation Ruling of TR 93/32”, it comprises of the description of the

divisionary net gain or loss from the rental property between the joint owners of the stated

property (Braithwaite, 2016). Along with this, the ruling is adjudged primarily with the analysis

of the taxable position of the joint owners, which are not accountable for conducting the values

within actions. The existing situation of Jill and Jack takes into account the dissection of taxable

position of the above-stated property. 10% of the overall property belongs to Jack and the

remaining 90% of the property belongs to Jill.

As per the “Taxation Ruling TR 92/32”, the joint ownership of rental property is

considered as a partnership for income tax. However, this is not taken into account as a single

partnership at the common low besides the accounts of ownership for conducting value for any

business practice. In this case, the joint ownership is adjudged as the partnership to satisfy the

Answer to Question 3:

Issue:

The current case study primarily denotes that such issue is concerned with the loss

distribution gathered from the rental property as joint ownership and the partners include Jack

and Jill.

Laws:

a. Taxation Ruling of TR 93/32

b. Section 51 of ITAA 1997

c. F.C. of T v McDonald (1987)

Application:

Based on the “Taxation Ruling of TR 93/32”, it comprises of the description of the

divisionary net gain or loss from the rental property between the joint owners of the stated

property (Braithwaite, 2016). Along with this, the ruling is adjudged primarily with the analysis

of the taxable position of the joint owners, which are not accountable for conducting the values

within actions. The existing situation of Jill and Jack takes into account the dissection of taxable

position of the above-stated property. 10% of the overall property belongs to Jack and the

remaining 90% of the property belongs to Jill.

As per the “Taxation Ruling TR 92/32”, the joint ownership of rental property is

considered as a partnership for income tax. However, this is not taken into account as a single

partnership at the common low besides the accounts of ownership for conducting value for any

business practice. In this case, the joint ownership is adjudged as the partnership to satisfy the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW, THEORY AND PRACTICE

income tax purpose solely (Braithwaite, 2017). The loss incurred from the rental property is

handled through the joint ownership of the rental property along with from the allocation of

profits obtained from partnership and losses. The existing scenario of Jill and Jack depicts the

joint ownership between them in relation to the rental property depending on income tax purpose

and this could not be adjudged in the form of partnership in consideration with the common law

(Dafflon, 2015).

With special adherence to the “Taxation Ruling of TR 92/32”, the joint owners of the

rental property are not adjudged partners at common law. In this case, the agreement of

partnership has been either in verbal or written, which has no impact on the shared value related

to loss or income from the stated property. Henceforth, the joint owners of the rental property,

Jill and Jack, would stick on to the asset in the form of joint renters as a sole common factor

(Davis et al., 2015).

It has been observed in the case of “F.C. of T v McDonald (1987) ATR 957”, the

taxpayer and his wife are the legal owners of two strata units of title in the form of joint renters.

There has been a confirmed agreement between them, which depicts that the net gain from the

rental property would be provided as 75% to Mrs McDonald and 25% to Mr McDonald. In this

case, the overall amount of loss would be incurred on the part of Mr McDonald (Mitchell et al.,

2016).

Conclusion:

From the above discussion, it could be stated that Jill and Jack need to allocate the loss

equally and joint ownership could not be considered as partnership business.

income tax purpose solely (Braithwaite, 2017). The loss incurred from the rental property is

handled through the joint ownership of the rental property along with from the allocation of

profits obtained from partnership and losses. The existing scenario of Jill and Jack depicts the

joint ownership between them in relation to the rental property depending on income tax purpose

and this could not be adjudged in the form of partnership in consideration with the common law

(Dafflon, 2015).

With special adherence to the “Taxation Ruling of TR 92/32”, the joint owners of the

rental property are not adjudged partners at common law. In this case, the agreement of

partnership has been either in verbal or written, which has no impact on the shared value related

to loss or income from the stated property. Henceforth, the joint owners of the rental property,

Jill and Jack, would stick on to the asset in the form of joint renters as a sole common factor

(Davis et al., 2015).

It has been observed in the case of “F.C. of T v McDonald (1987) ATR 957”, the

taxpayer and his wife are the legal owners of two strata units of title in the form of joint renters.

There has been a confirmed agreement between them, which depicts that the net gain from the

rental property would be provided as 75% to Mrs McDonald and 25% to Mr McDonald. In this

case, the overall amount of loss would be incurred on the part of Mr McDonald (Mitchell et al.,

2016).

Conclusion:

From the above discussion, it could be stated that Jill and Jack need to allocate the loss

equally and joint ownership could not be considered as partnership business.

8TAXATION LAW, THEORY AND PRACTICE

Answer to Question 4:

The occurrence of avoiding tax has been quoted in accordance with “IRC v Duke of

Westminster [1936] AC 1”. This case developed a principle, which denotes that each individual

is permitted for ordering the affairs to allow the taxation assignment made in the Fitting Act.

Such taxation allocation is less than the same (Dowling, 2014). Although it could not be

adjudged that such ruling has been attractive for others to seek the tax avoidance in relation to

the complex structures of law and the subsequent cases have weakened them, in which the courts

have viewed at the entire effect. Depicting an instance of the court in the future stages are highly

restrictive and these have been adopted under the “WT Ramsay v IRC principle”. There has been

artificial pre-arrangement of the transaction and the service is not provided for commercial

purpose (Halliday & Shaffer, 2015). The ideal regulation is to levy tax to extend the transaction

in the form of overall fact.

In the modern scenario, the doctrine within Australia signifies that in case; an individual

accomplishes success to secure the results, the Inland Revenue might be of the initiative and they

could not be compelled to incur any enhanced tax amount (Ivec & Braithwaite, 2015). Along

with this, it has been evaluated that such aspect enables the organisations and individuals to

structure the financial agreements in relation to the fixed goals of minimising the tax liabilities

depending on their structures within the law structure.

Answer to Question 5:

Issue:

In the existing scenario, the assessment of income from selling the felled timber is

evaluated under “Subsection 6(1) of the Income Tax Assessment Act 1936”.

Answer to Question 4:

The occurrence of avoiding tax has been quoted in accordance with “IRC v Duke of

Westminster [1936] AC 1”. This case developed a principle, which denotes that each individual

is permitted for ordering the affairs to allow the taxation assignment made in the Fitting Act.

Such taxation allocation is less than the same (Dowling, 2014). Although it could not be

adjudged that such ruling has been attractive for others to seek the tax avoidance in relation to

the complex structures of law and the subsequent cases have weakened them, in which the courts

have viewed at the entire effect. Depicting an instance of the court in the future stages are highly

restrictive and these have been adopted under the “WT Ramsay v IRC principle”. There has been

artificial pre-arrangement of the transaction and the service is not provided for commercial

purpose (Halliday & Shaffer, 2015). The ideal regulation is to levy tax to extend the transaction

in the form of overall fact.

In the modern scenario, the doctrine within Australia signifies that in case; an individual

accomplishes success to secure the results, the Inland Revenue might be of the initiative and they

could not be compelled to incur any enhanced tax amount (Ivec & Braithwaite, 2015). Along

with this, it has been evaluated that such aspect enables the organisations and individuals to

structure the financial agreements in relation to the fixed goals of minimising the tax liabilities

depending on their structures within the law structure.

Answer to Question 5:

Issue:

In the existing scenario, the assessment of income from selling the felled timber is

evaluated under “Subsection 6(1) of the Income Tax Assessment Act 1936”.

9TAXATION LAW, THEORY AND PRACTICE

Laws:

a. “Subsection 6(1) of the Income Tax Assessment Act 1936”

b. “McCauley v The Federal Commissioner of Taxation”

Application:

In the current situation, it has been found that Bill is the owner of a large land, in which

there are diverse pine trees. Bill intended to utilise the land for grazing sheep and the person

wanted to clear the same. The person has invented a logging organisation, which is ready to pay

$1,000 for each 100 metres of timber. The organisation could grab a portion from the land of

Bill. The “Taxation Ruling TR 95/6” lays down the consequences of income tax generating the

primary production activities and forestry (Parker, 2013). This ruling provides the limit to which

the receipts ate obtained from the overall timber sale. This aspect comprises of assessable

income to ascertain whether the tax payers are involved into the forestry sector activities. In

accordance with “Subsection 6 (1) of the Income Tax Assessment Act 1936”, the taxpayers are

involved into the forest operation activities, which are adjudged as the primary creator.

According to “Subsection 6 (1) of the Income Tax Assessment Act 1936”, the initial

production is described commonly as the tree planting within plantation needed for felling forest

(Taylor & Richardson, 2013). It has been observed from the provided case that Bill is adjudged

as a basic producer, as he has been involved into the primary production procedures in

accordance with the “Subsection 6 (1) of the Income Tax Assessment Act 1936”. The forestry

operations take into account the fall of trees in the plantation or forest; however, there is no

concern on the part of the taxpayers regarding the planted trees.

Laws:

a. “Subsection 6(1) of the Income Tax Assessment Act 1936”

b. “McCauley v The Federal Commissioner of Taxation”

Application:

In the current situation, it has been found that Bill is the owner of a large land, in which

there are diverse pine trees. Bill intended to utilise the land for grazing sheep and the person

wanted to clear the same. The person has invented a logging organisation, which is ready to pay

$1,000 for each 100 metres of timber. The organisation could grab a portion from the land of

Bill. The “Taxation Ruling TR 95/6” lays down the consequences of income tax generating the

primary production activities and forestry (Parker, 2013). This ruling provides the limit to which

the receipts ate obtained from the overall timber sale. This aspect comprises of assessable

income to ascertain whether the tax payers are involved into the forestry sector activities. In

accordance with “Subsection 6 (1) of the Income Tax Assessment Act 1936”, the taxpayers are

involved into the forest operation activities, which are adjudged as the primary creator.

According to “Subsection 6 (1) of the Income Tax Assessment Act 1936”, the initial

production is described commonly as the tree planting within plantation needed for felling forest

(Taylor & Richardson, 2013). It has been observed from the provided case that Bill is adjudged

as a basic producer, as he has been involved into the primary production procedures in

accordance with the “Subsection 6 (1) of the Income Tax Assessment Act 1936”. The forestry

operations take into account the fall of trees in the plantation or forest; however, there is no

concern on the part of the taxpayers regarding the planted trees.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW, THEORY AND PRACTICE

As evaluated above, Bill is the owner of a large land; however, the person has not planted

the trees. The entire receipt amount obtained from the part of Bill through selling the felled

timber comprises assessable income of the taxpayers disposing regarding the trees not

necessarily planted on the part of the taxpayers along with rendering for the objective of sale.

This develops the portion of assessable income (Vatn, 2015). Despite such facts, the sales

combine either full or partial business assets, in which the trees are undertaken as assessable

income of the taxpayers in accordance with “Subsection 6 (1) of the Income Tax Assessment Act

1936”.

On the other hand, if the taxpayer has incurred an amount of $50,000 through surrender

of the obligation to the logging organisation in order to remove the needed amount of timber. In

that case, the receipt amount would be taken into account in the form of royalties. According to

the “Section 26 (f) receipt of royalties from the taxpayer to grant, the right of falling the timber

on land obtained on the part of the taxpayer (Yan & Luo, 2016).

Conclusion:

It could be inferred that the receiving income from cutting timber would be adjudged as

taxable proceeds in accordance with “Subsection 6 (1) of the ITAA 1997”.

As evaluated above, Bill is the owner of a large land; however, the person has not planted

the trees. The entire receipt amount obtained from the part of Bill through selling the felled

timber comprises assessable income of the taxpayers disposing regarding the trees not

necessarily planted on the part of the taxpayers along with rendering for the objective of sale.

This develops the portion of assessable income (Vatn, 2015). Despite such facts, the sales

combine either full or partial business assets, in which the trees are undertaken as assessable

income of the taxpayers in accordance with “Subsection 6 (1) of the Income Tax Assessment Act

1936”.

On the other hand, if the taxpayer has incurred an amount of $50,000 through surrender

of the obligation to the logging organisation in order to remove the needed amount of timber. In

that case, the receipt amount would be taken into account in the form of royalties. According to

the “Section 26 (f) receipt of royalties from the taxpayer to grant, the right of falling the timber

on land obtained on the part of the taxpayer (Yan & Luo, 2016).

Conclusion:

It could be inferred that the receiving income from cutting timber would be adjudged as

taxable proceeds in accordance with “Subsection 6 (1) of the ITAA 1997”.

11TAXATION LAW, THEORY AND PRACTICE

References:

Alarie, B., Datt, K. H., Sawyer, A. J., & Weeks, G. (2014). Advance tax rulings in perspective: a

theoretical and comparative analysis.

Boll, K. (2014). Mapping tax compliance: Assemblages, distributed action and practices: A new

way of doing tax research. Critical Perspectives on Accounting, 25(4), 293-303.

Braithwaite, J. B. (2016). Restorative Justice and Responsive Regulation: The Question of

Evidence.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Dafflon, B. (2015). The assignment of functions to decentralized government: from theory to

practice. Handbook of multilevel finance, Edward Elgar, Cheltenham, 163-199.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), 47-68.

Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), 173-184.

Halliday, T. C., & Shaffer, G. (Eds.). (2015). Transnational legal orders. Cambridge University

Press.

Ivec, M., & Braithwaite, V. (2015). Applications of responsive regulatory theory in Australia and

overseas: Update.

References:

Alarie, B., Datt, K. H., Sawyer, A. J., & Weeks, G. (2014). Advance tax rulings in perspective: a

theoretical and comparative analysis.

Boll, K. (2014). Mapping tax compliance: Assemblages, distributed action and practices: A new

way of doing tax research. Critical Perspectives on Accounting, 25(4), 293-303.

Braithwaite, J. B. (2016). Restorative Justice and Responsive Regulation: The Question of

Evidence.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Dafflon, B. (2015). The assignment of functions to decentralized government: from theory to

practice. Handbook of multilevel finance, Edward Elgar, Cheltenham, 163-199.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially responsible

firms pay more taxes?. The Accounting Review, 91(1), 47-68.

Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), 173-184.

Halliday, T. C., & Shaffer, G. (Eds.). (2015). Transnational legal orders. Cambridge University

Press.

Ivec, M., & Braithwaite, V. (2015). Applications of responsive regulatory theory in Australia and

overseas: Update.

12TAXATION LAW, THEORY AND PRACTICE

Joseph, S. A. (2014). The polluter pays principle and land remediation: A comparison of the

United Kingdom and Australian approaches. AJEL, 1, 24.

Maddison, S., & Denniss, R. (2013). An introduction to Australian public policy: theory and

practice. Cambridge University Press.

Mitchell, R., O'Donnell, A., Marshall, S., & Ramsay, I. (2016). Law, corporate governance and

partnerships at work: a study of australian regulatory style and business practice.

Routledge.

Parker, C. (2013). Twenty years of responsive regulation: An appreciation and

appraisal. Regulation & Governance, 7(1), 2-13.

Taylor, G., & Richardson, G. (2013). The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting,

Auditing and Taxation, 22(1), 12-25.

Vatn, A. (2015). Markets in environmental governance. From theory to practice. Ecological

Economics, 117, 225-233.

Yan, A., & Luo, Y. (2016). International joint ventures: Theory and practice. Routledge.

Joseph, S. A. (2014). The polluter pays principle and land remediation: A comparison of the

United Kingdom and Australian approaches. AJEL, 1, 24.

Maddison, S., & Denniss, R. (2013). An introduction to Australian public policy: theory and

practice. Cambridge University Press.

Mitchell, R., O'Donnell, A., Marshall, S., & Ramsay, I. (2016). Law, corporate governance and

partnerships at work: a study of australian regulatory style and business practice.

Routledge.

Parker, C. (2013). Twenty years of responsive regulation: An appreciation and

appraisal. Regulation & Governance, 7(1), 2-13.

Taylor, G., & Richardson, G. (2013). The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting,

Auditing and Taxation, 22(1), 12-25.

Vatn, A. (2015). Markets in environmental governance. From theory to practice. Ecological

Economics, 117, 225-233.

Yan, A., & Luo, Y. (2016). International joint ventures: Theory and practice. Routledge.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.