Taxation Law United Kingdom Question Answer 2022

VerifiedAdded on 2022/10/13

|13

|2762

|10

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

TAXATION LAW

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to question 2:......................................................................................................................7

Reference.......................................................................................................................................11

TAXATION LAW

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to question 2:......................................................................................................................7

Reference.......................................................................................................................................11

2

TAXATION LAW

Answer to Question 1

Requirement a

The capital gain taxation rulings which are stated in the legislations makes its clear that if

an asset is sold for a profit than the same would be considered to be a capital gain for the

business. The regulations regarding the applicability of the capital gain taxes states that any

amount received would be treated as capital receipts if the individual sells or disposes off the

asset for a gain provided the transaction has taken place after 20th September 1985. It is also to be

noted that any purchases of assets before the specified date if sold would not be considered under

the purview of capital gains taxation (Bain and Boccabella 2019). In case a taxpayer sells off his

house which was his main dwelling than the same is disregarded under the capital gain taxation

system considering the conditions which are provided below:

The house which was sold was the main dwelling place for the taxpayer throughout the

ownership period.

The taxpayer is an individual

The ownership of the house which was sold was not transferred to the taxpayer due to

inheritance from a deceased estate.

As per the case, Jasmine has decided to move out of Australia where she is a resident and

shift to United Kingdom and therefore she is selling off her assets in Australia. Jasmine sold her

house for $ 650,000 which was originally purchased at $ 40,000 in 1981. The reason for non-

applicability of tax is that the house was purchased in 1981 which is earlier than the specified

date of applicability which is 20th September 1985. Therefore, it can be established that the assets

are Pre-CGT in nature and therefore not applicable to capital gains tax. Hence, no tax needs to be

paid by Jasmine in this regard.

TAXATION LAW

Answer to Question 1

Requirement a

The capital gain taxation rulings which are stated in the legislations makes its clear that if

an asset is sold for a profit than the same would be considered to be a capital gain for the

business. The regulations regarding the applicability of the capital gain taxes states that any

amount received would be treated as capital receipts if the individual sells or disposes off the

asset for a gain provided the transaction has taken place after 20th September 1985. It is also to be

noted that any purchases of assets before the specified date if sold would not be considered under

the purview of capital gains taxation (Bain and Boccabella 2019). In case a taxpayer sells off his

house which was his main dwelling than the same is disregarded under the capital gain taxation

system considering the conditions which are provided below:

The house which was sold was the main dwelling place for the taxpayer throughout the

ownership period.

The taxpayer is an individual

The ownership of the house which was sold was not transferred to the taxpayer due to

inheritance from a deceased estate.

As per the case, Jasmine has decided to move out of Australia where she is a resident and

shift to United Kingdom and therefore she is selling off her assets in Australia. Jasmine sold her

house for $ 650,000 which was originally purchased at $ 40,000 in 1981. The reason for non-

applicability of tax is that the house was purchased in 1981 which is earlier than the specified

date of applicability which is 20th September 1985. Therefore, it can be established that the assets

are Pre-CGT in nature and therefore not applicable to capital gains tax. Hence, no tax needs to be

paid by Jasmine in this regard.

3

TAXATION LAW

Requirement b

The provisions of “Section 108(5) of ITTA 1997” makes it clear that CGT assets can be

identified as any property which may be tangible or intangible in nature. CGT on asset sale takes

place according to the CGT event which takes place and the occurrence of the event is covered

under “Section 104 of ITTA 1997”. In case of “CGT event A1” there is a case of disposal of

asset for which capital gains tax is applicable considering the regulations.

The provisions of “Section 108(20) of ITTA 1997” includes those assets which are for

personal use and the same does not include assets which specifically used for private use and

entertainment of the taxpayer. In further analysis, “Section 108(20)(1) of ITTA 1997” states that

any loss which is made from sale of private assets which be not considered even if acquisition

price was paid.

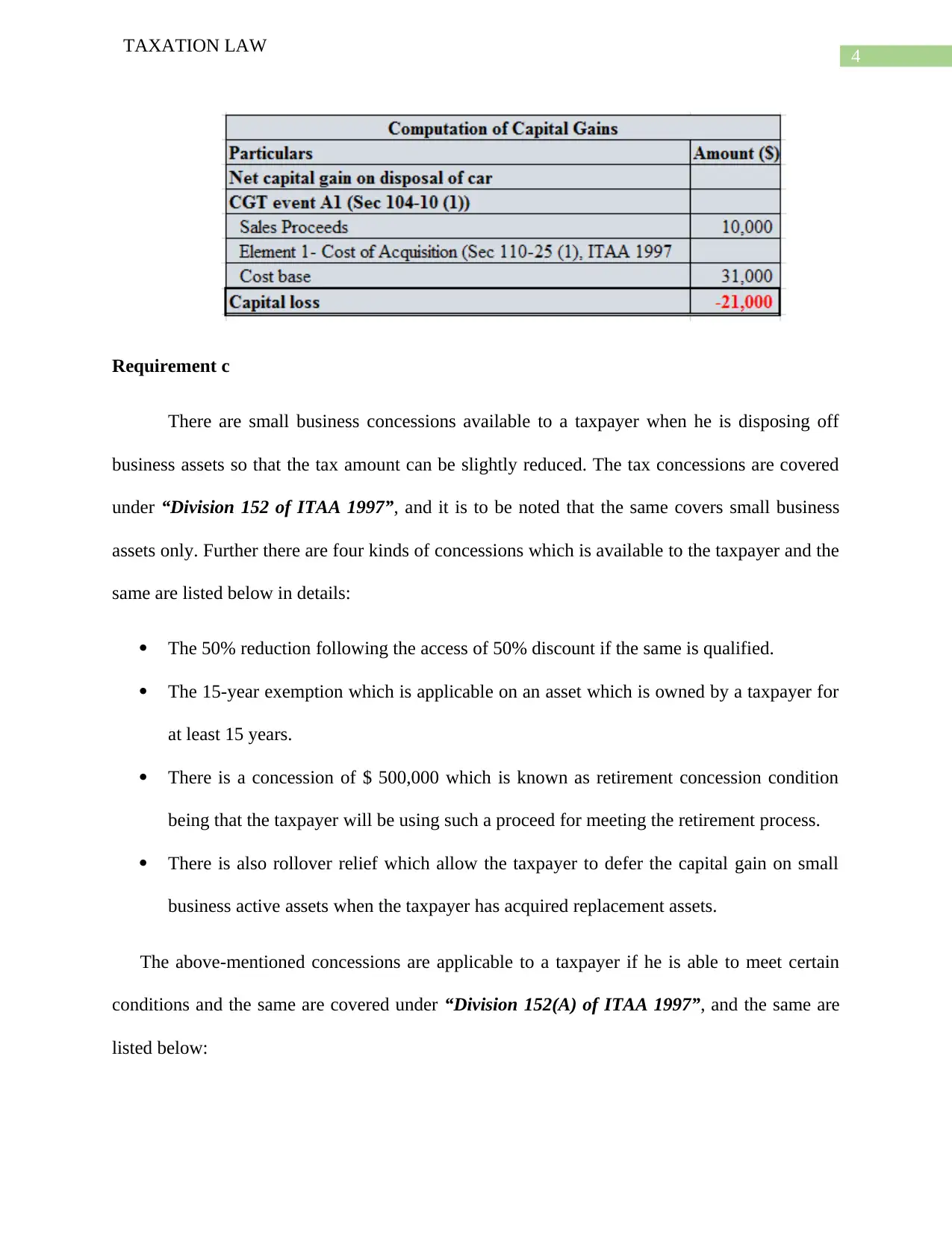

As per the case study, Jasmine is moving out of Australia and therefore she needs to

settle her affairs in terms of her assets. Jasmine wants to dispose off a car which she had

purchased for $ 31,000 and the same was valued at $ 10,000 at the time of its sale. The

provisions of “Section 108(5) of ITTA 1997” makes it clear that car is classified as a capital

asset. The car needs to be covered under “Section 108(20) of ITTA 1997” as Jasmine has

previously used the asset for her private use purposes (Brown, Ferguson and Sherry 2015). As

soon as the car is sold “CGT event A1” will be attracted but the capital loss which is made on the

car by Jasmine would be ignored under “Section 108(20)(1) of ITTA 1997”.

TAXATION LAW

Requirement b

The provisions of “Section 108(5) of ITTA 1997” makes it clear that CGT assets can be

identified as any property which may be tangible or intangible in nature. CGT on asset sale takes

place according to the CGT event which takes place and the occurrence of the event is covered

under “Section 104 of ITTA 1997”. In case of “CGT event A1” there is a case of disposal of

asset for which capital gains tax is applicable considering the regulations.

The provisions of “Section 108(20) of ITTA 1997” includes those assets which are for

personal use and the same does not include assets which specifically used for private use and

entertainment of the taxpayer. In further analysis, “Section 108(20)(1) of ITTA 1997” states that

any loss which is made from sale of private assets which be not considered even if acquisition

price was paid.

As per the case study, Jasmine is moving out of Australia and therefore she needs to

settle her affairs in terms of her assets. Jasmine wants to dispose off a car which she had

purchased for $ 31,000 and the same was valued at $ 10,000 at the time of its sale. The

provisions of “Section 108(5) of ITTA 1997” makes it clear that car is classified as a capital

asset. The car needs to be covered under “Section 108(20) of ITTA 1997” as Jasmine has

previously used the asset for her private use purposes (Brown, Ferguson and Sherry 2015). As

soon as the car is sold “CGT event A1” will be attracted but the capital loss which is made on the

car by Jasmine would be ignored under “Section 108(20)(1) of ITTA 1997”.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

TAXATION LAW

Requirement c

There are small business concessions available to a taxpayer when he is disposing off

business assets so that the tax amount can be slightly reduced. The tax concessions are covered

under “Division 152 of ITAA 1997”, and it is to be noted that the same covers small business

assets only. Further there are four kinds of concessions which is available to the taxpayer and the

same are listed below in details:

The 50% reduction following the access of 50% discount if the same is qualified.

The 15-year exemption which is applicable on an asset which is owned by a taxpayer for

at least 15 years.

There is a concession of $ 500,000 which is known as retirement concession condition

being that the taxpayer will be using such a proceed for meeting the retirement process.

There is also rollover relief which allow the taxpayer to defer the capital gain on small

business active assets when the taxpayer has acquired replacement assets.

The above-mentioned concessions are applicable to a taxpayer if he is able to meet certain

conditions and the same are covered under “Division 152(A) of ITAA 1997”, and the same are

listed below:

TAXATION LAW

Requirement c

There are small business concessions available to a taxpayer when he is disposing off

business assets so that the tax amount can be slightly reduced. The tax concessions are covered

under “Division 152 of ITAA 1997”, and it is to be noted that the same covers small business

assets only. Further there are four kinds of concessions which is available to the taxpayer and the

same are listed below in details:

The 50% reduction following the access of 50% discount if the same is qualified.

The 15-year exemption which is applicable on an asset which is owned by a taxpayer for

at least 15 years.

There is a concession of $ 500,000 which is known as retirement concession condition

being that the taxpayer will be using such a proceed for meeting the retirement process.

There is also rollover relief which allow the taxpayer to defer the capital gain on small

business active assets when the taxpayer has acquired replacement assets.

The above-mentioned concessions are applicable to a taxpayer if he is able to meet certain

conditions and the same are covered under “Division 152(A) of ITAA 1997”, and the same are

listed below:

5

TAXATION LAW

1. The nature of the business should be a small business meeting the criteria of having a

turnover of $ 2 million in the previous year or have a net asset value of $ 6 million and

not higher than this.

2. The CGT asset should be an active asset.

As per the case, Jasmine is moving out of Australia as she is retiring and wants to settle down

in United Kingdom. The business assets and goodwill which was owned by Jasmine was sold at

$ 65,000 and $ 60,000 respectively. Apply the provisions relating to concession, it can be said

that Jasmine would be eligible for small business concession as she has met the basic conditions

of the assets not being greater than $ 6 million in value. The concession which Jasmine can opt

for is the 15-year exemption for which she is totally applicable or she can also opt for retirement

concession of $ 500,000 as she is retiring from her business and can use the proceeds for the

same purpose.

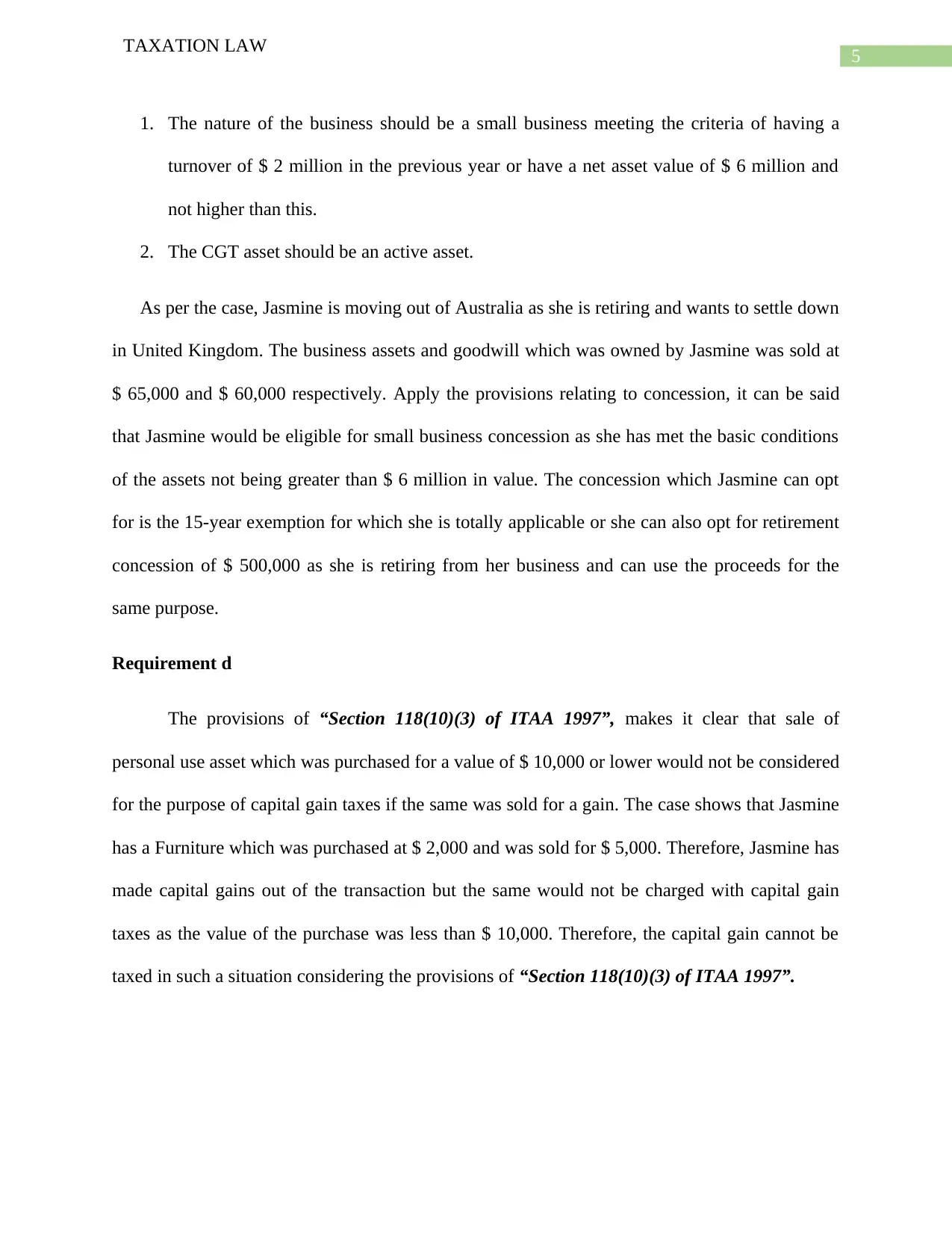

Requirement d

The provisions of “Section 118(10)(3) of ITAA 1997”, makes it clear that sale of

personal use asset which was purchased for a value of $ 10,000 or lower would not be considered

for the purpose of capital gain taxes if the same was sold for a gain. The case shows that Jasmine

has a Furniture which was purchased at $ 2,000 and was sold for $ 5,000. Therefore, Jasmine has

made capital gains out of the transaction but the same would not be charged with capital gain

taxes as the value of the purchase was less than $ 10,000. Therefore, the capital gain cannot be

taxed in such a situation considering the provisions of “Section 118(10)(3) of ITAA 1997”.

TAXATION LAW

1. The nature of the business should be a small business meeting the criteria of having a

turnover of $ 2 million in the previous year or have a net asset value of $ 6 million and

not higher than this.

2. The CGT asset should be an active asset.

As per the case, Jasmine is moving out of Australia as she is retiring and wants to settle down

in United Kingdom. The business assets and goodwill which was owned by Jasmine was sold at

$ 65,000 and $ 60,000 respectively. Apply the provisions relating to concession, it can be said

that Jasmine would be eligible for small business concession as she has met the basic conditions

of the assets not being greater than $ 6 million in value. The concession which Jasmine can opt

for is the 15-year exemption for which she is totally applicable or she can also opt for retirement

concession of $ 500,000 as she is retiring from her business and can use the proceeds for the

same purpose.

Requirement d

The provisions of “Section 118(10)(3) of ITAA 1997”, makes it clear that sale of

personal use asset which was purchased for a value of $ 10,000 or lower would not be considered

for the purpose of capital gain taxes if the same was sold for a gain. The case shows that Jasmine

has a Furniture which was purchased at $ 2,000 and was sold for $ 5,000. Therefore, Jasmine has

made capital gains out of the transaction but the same would not be charged with capital gain

taxes as the value of the purchase was less than $ 10,000. Therefore, the capital gain cannot be

taxed in such a situation considering the provisions of “Section 118(10)(3) of ITAA 1997”.

6

TAXATION LAW

Requirement e

The definition of the term Collectable is provided under “Section 118(10)(2) of ITAA

1997”, as some kind of artwork, jewellery or rare collection which is kept by people for private

usage and satisfaction or fun. Further the provisions of “Section 118(10)(3) of ITAA 1997”,

restricts recognition of any capital gain or losses upon sale of collectable if the same has been

purchased for $ 500 or lower value. However, if the value is greater than $ 500 than the gain

made would be taxable under CGT rulings while capital losses would be set off with capital

gains from other collectibles (Tran-Nam 2015).

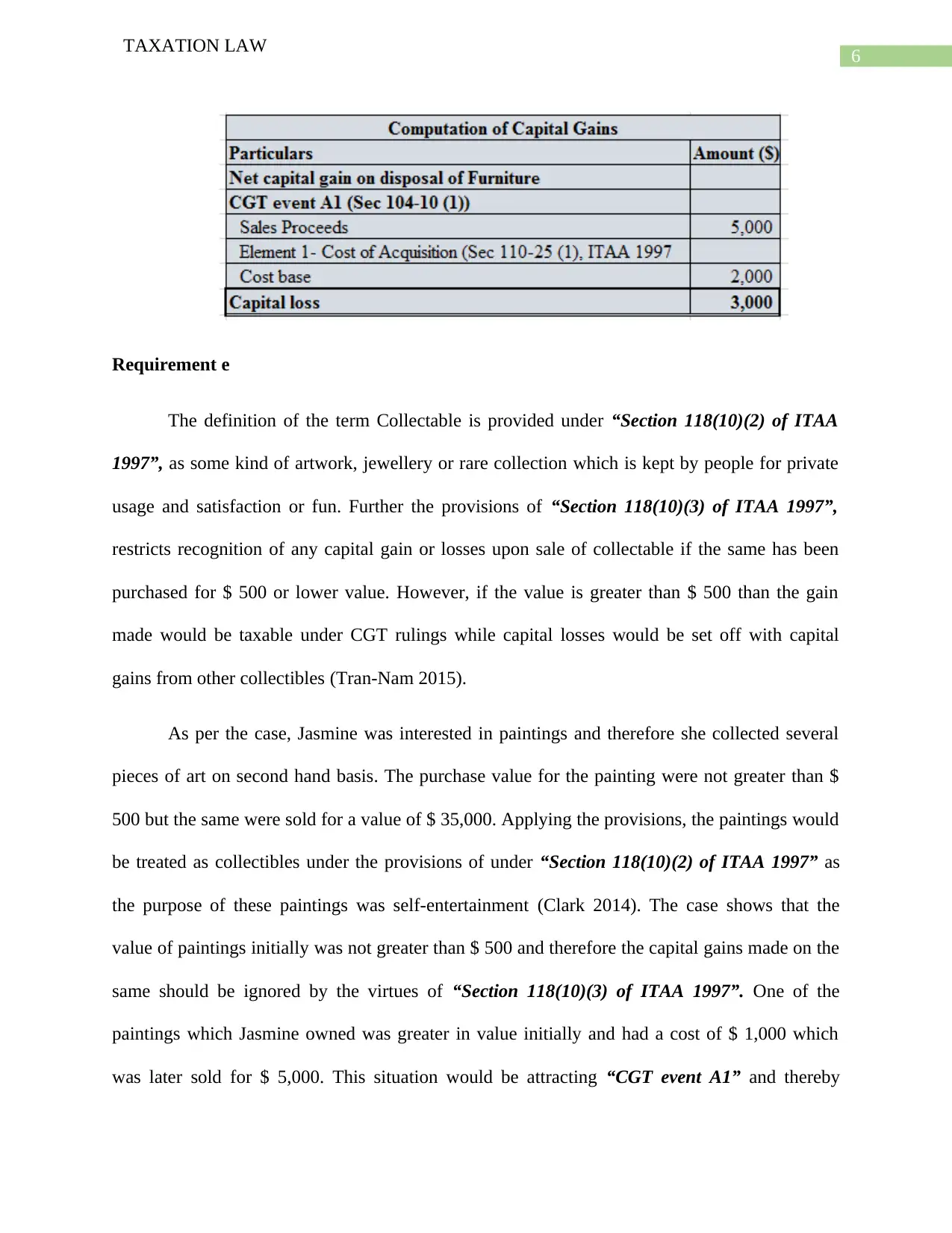

As per the case, Jasmine was interested in paintings and therefore she collected several

pieces of art on second hand basis. The purchase value for the painting were not greater than $

500 but the same were sold for a value of $ 35,000. Applying the provisions, the paintings would

be treated as collectibles under the provisions of under “Section 118(10)(2) of ITAA 1997” as

the purpose of these paintings was self-entertainment (Clark 2014). The case shows that the

value of paintings initially was not greater than $ 500 and therefore the capital gains made on the

same should be ignored by the virtues of “Section 118(10)(3) of ITAA 1997”. One of the

paintings which Jasmine owned was greater in value initially and had a cost of $ 1,000 which

was later sold for $ 5,000. This situation would be attracting “CGT event A1” and thereby

TAXATION LAW

Requirement e

The definition of the term Collectable is provided under “Section 118(10)(2) of ITAA

1997”, as some kind of artwork, jewellery or rare collection which is kept by people for private

usage and satisfaction or fun. Further the provisions of “Section 118(10)(3) of ITAA 1997”,

restricts recognition of any capital gain or losses upon sale of collectable if the same has been

purchased for $ 500 or lower value. However, if the value is greater than $ 500 than the gain

made would be taxable under CGT rulings while capital losses would be set off with capital

gains from other collectibles (Tran-Nam 2015).

As per the case, Jasmine was interested in paintings and therefore she collected several

pieces of art on second hand basis. The purchase value for the painting were not greater than $

500 but the same were sold for a value of $ 35,000. Applying the provisions, the paintings would

be treated as collectibles under the provisions of under “Section 118(10)(2) of ITAA 1997” as

the purpose of these paintings was self-entertainment (Clark 2014). The case shows that the

value of paintings initially was not greater than $ 500 and therefore the capital gains made on the

same should be ignored by the virtues of “Section 118(10)(3) of ITAA 1997”. One of the

paintings which Jasmine owned was greater in value initially and had a cost of $ 1,000 which

was later sold for $ 5,000. This situation would be attracting “CGT event A1” and thereby

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

making the provisions of “Section 104(10) of ITAA 1997” applicable. Therefore, capital gain

taxes would be applicable for this painting and the computation for the same is shown below:

Answer to question 2:

Issues

The issue which arises is related to the applicability of “Division 40 of ITAA 1997”

which deals with deduction offered on deprecation charged on business assets.

Rule

The provisions which is stated under “Division 40 of ITAA 1997” provides a deduction

for a decline in value for a depreciating asset and the same usually allowed as a uniformed

capital allowance (Boll 2014). As per the provisions stated in “Division 40(25) of ITAA 1997”

deduction is allowable for decline in the value of a depreciating asset if the asset is under the

ownership of the taxpayer or being utilized for use purposes (Burkhauser, Hahn and Wilkins

2015). In case of further move in with the rulings, the definition of depreciating asset which is

covered under “Division 40(30) of ITAA 1997” stating that it is an asset which has a useful life

and the usefulness of the asset is said to fall as time passes based on the period of use for the

TAXATION LAW

making the provisions of “Section 104(10) of ITAA 1997” applicable. Therefore, capital gain

taxes would be applicable for this painting and the computation for the same is shown below:

Answer to question 2:

Issues

The issue which arises is related to the applicability of “Division 40 of ITAA 1997”

which deals with deduction offered on deprecation charged on business assets.

Rule

The provisions which is stated under “Division 40 of ITAA 1997” provides a deduction

for a decline in value for a depreciating asset and the same usually allowed as a uniformed

capital allowance (Boll 2014). As per the provisions stated in “Division 40(25) of ITAA 1997”

deduction is allowable for decline in the value of a depreciating asset if the asset is under the

ownership of the taxpayer or being utilized for use purposes (Burkhauser, Hahn and Wilkins

2015). In case of further move in with the rulings, the definition of depreciating asset which is

covered under “Division 40(30) of ITAA 1997” stating that it is an asset which has a useful life

and the usefulness of the asset is said to fall as time passes based on the period of use for the

8

TAXATION LAW

same. The word asset involves all tangible and intangible assets and thereby a simple plant can

also be considered as an asset. In the case of “FCT v Wangaratta Woollen Mills Ltd (1969)” a

structure dye house was considered to be a plant

The assets should be under the ownership of the taxpayer or used for an assessable

purpose. The provisions which is stated under “Section 40(25)(7) of ITAA 1997” clearly that an

asset should be used for the purpose of generating business income while there is a deduction

which is allowable on the lower base which is other than the tax base applicable (Faccio and Xu

2015). The provisions of “Section 40(60) of ITAA 1997” covers that decline in value starts when

the asset is first installed and put for use and deduction applicable to such assets is based on the

effective life of the asset.

The provision of “Sub-Division 40(C ) of ITAA 1997” shows that the depreciation on the

use of the asset is allowed on the basis of the cost base of the asset. The cost of the asset

comprises of two elements which are:

The time frame during which the taxpayer first holds the assets or used the same.

It includes amounts which is paid for the assets by the taxpayer.

“Section 40(190) of ITAA 1997” is concerned with the second element of the cost of the

asset and the same covers the amount which is incurred by the taxpayer to bring the asset in a

usable state.

Application

As per the case which is provided in the assessment, John is an owner of a manufacturing

automobile company and the company is engaged in production of motor vehicles. The company

had to purchase and implement a machinery for BMW parts productions which was done on 1st

TAXATION LAW

same. The word asset involves all tangible and intangible assets and thereby a simple plant can

also be considered as an asset. In the case of “FCT v Wangaratta Woollen Mills Ltd (1969)” a

structure dye house was considered to be a plant

The assets should be under the ownership of the taxpayer or used for an assessable

purpose. The provisions which is stated under “Section 40(25)(7) of ITAA 1997” clearly that an

asset should be used for the purpose of generating business income while there is a deduction

which is allowable on the lower base which is other than the tax base applicable (Faccio and Xu

2015). The provisions of “Section 40(60) of ITAA 1997” covers that decline in value starts when

the asset is first installed and put for use and deduction applicable to such assets is based on the

effective life of the asset.

The provision of “Sub-Division 40(C ) of ITAA 1997” shows that the depreciation on the

use of the asset is allowed on the basis of the cost base of the asset. The cost of the asset

comprises of two elements which are:

The time frame during which the taxpayer first holds the assets or used the same.

It includes amounts which is paid for the assets by the taxpayer.

“Section 40(190) of ITAA 1997” is concerned with the second element of the cost of the

asset and the same covers the amount which is incurred by the taxpayer to bring the asset in a

usable state.

Application

As per the case which is provided in the assessment, John is an owner of a manufacturing

automobile company and the company is engaged in production of motor vehicles. The company

had to purchase and implement a machinery for BMW parts productions which was done on 1st

9

TAXATION LAW

Nov 2014. Applying the case laws of “FCT v Wangaratta Woollen Mills Ltd (1969)”, the

machinery would be considered as a deprecating asset under the meaning of “Section 40(25) of

ITAA 1997”. The machine would likely decline in value with the years to come and accordingly

deduction is to be applied (Chardon, Freudenberg and Brimble 2016). Therefore, the business

can claim deduction under “Section 40(25)(7) of ITAA 1997” as the same is a depreciable asset.

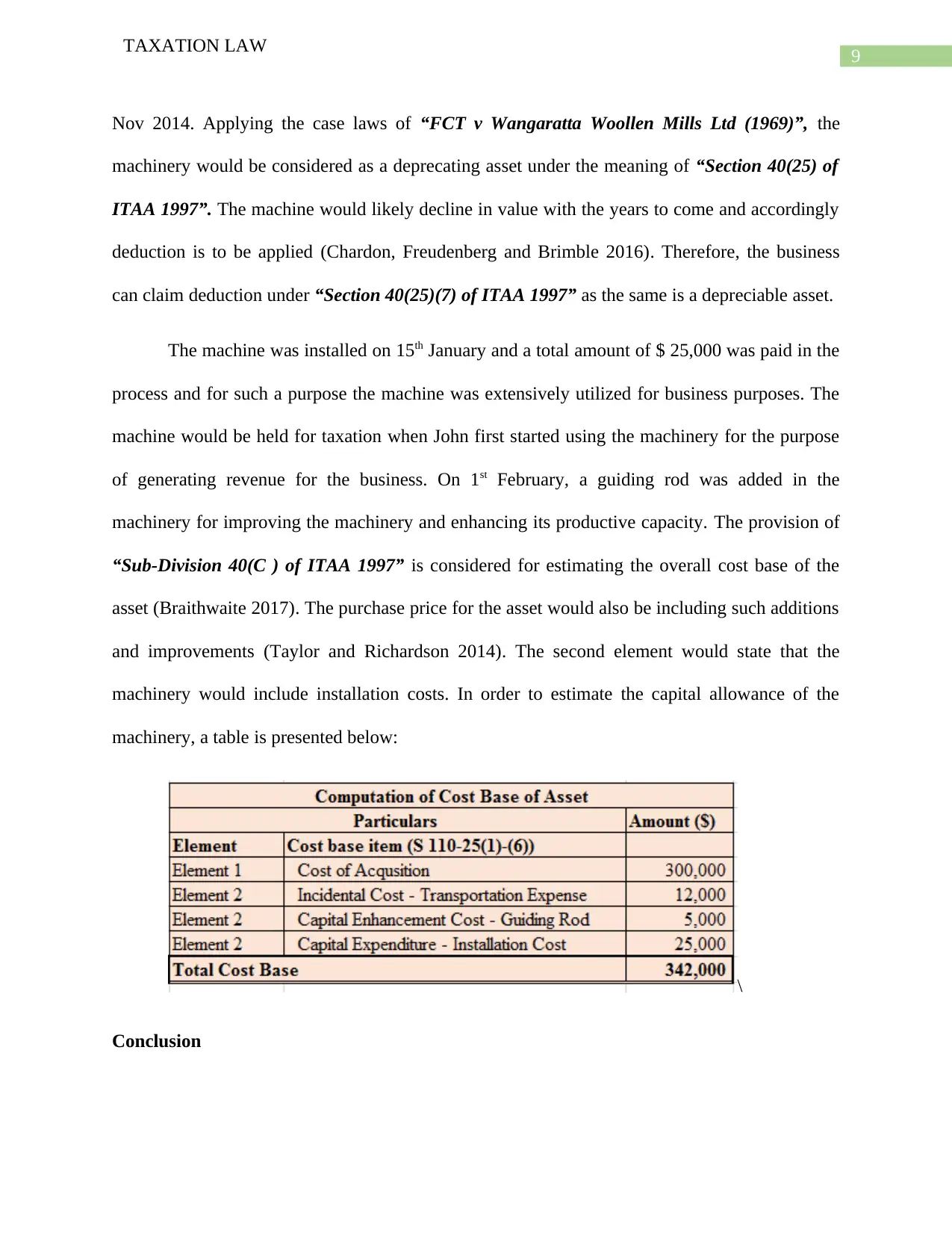

The machine was installed on 15th January and a total amount of $ 25,000 was paid in the

process and for such a purpose the machine was extensively utilized for business purposes. The

machine would be held for taxation when John first started using the machinery for the purpose

of generating revenue for the business. On 1st February, a guiding rod was added in the

machinery for improving the machinery and enhancing its productive capacity. The provision of

“Sub-Division 40(C ) of ITAA 1997” is considered for estimating the overall cost base of the

asset (Braithwaite 2017). The purchase price for the asset would also be including such additions

and improvements (Taylor and Richardson 2014). The second element would state that the

machinery would include installation costs. In order to estimate the capital allowance of the

machinery, a table is presented below:

\

Conclusion

TAXATION LAW

Nov 2014. Applying the case laws of “FCT v Wangaratta Woollen Mills Ltd (1969)”, the

machinery would be considered as a deprecating asset under the meaning of “Section 40(25) of

ITAA 1997”. The machine would likely decline in value with the years to come and accordingly

deduction is to be applied (Chardon, Freudenberg and Brimble 2016). Therefore, the business

can claim deduction under “Section 40(25)(7) of ITAA 1997” as the same is a depreciable asset.

The machine was installed on 15th January and a total amount of $ 25,000 was paid in the

process and for such a purpose the machine was extensively utilized for business purposes. The

machine would be held for taxation when John first started using the machinery for the purpose

of generating revenue for the business. On 1st February, a guiding rod was added in the

machinery for improving the machinery and enhancing its productive capacity. The provision of

“Sub-Division 40(C ) of ITAA 1997” is considered for estimating the overall cost base of the

asset (Braithwaite 2017). The purchase price for the asset would also be including such additions

and improvements (Taylor and Richardson 2014). The second element would state that the

machinery would include installation costs. In order to estimate the capital allowance of the

machinery, a table is presented below:

\

Conclusion

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

TAXATION LAW

The discussion above reveals that John would be allowed to claim deduction on

depreciation under decline in value of machinery estimate under “Section 40(25) of ITAA 1997”

which is mainly due to the fact that the machinery was purchased for generating more income.

TAXATION LAW

The discussion above reveals that John would be allowed to claim deduction on

depreciation under decline in value of machinery estimate under “Section 40(25) of ITAA 1997”

which is mainly due to the fact that the machinery was purchased for generating more income.

11

TAXATION LAW

Reference

Bain, K and Boccabella, D, 2019. The age of the home worker - part 2: Calculation of home

occupancy expense deductions, deduction apportionment and partial loss of CGT main residence

exemption. Australian Tax Forum, 34(1), pp.65–93.

Boll, K., 2014. Mapping tax compliance: Assemblages, distributed action and practices: A new

way of doing tax research. Critical Perspectives on Accounting, 25(4-5), pp.293-303.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion. Routledge.

Brown, P., Ferguson, A. and Sherry, S., 2015. Investor behaviour in response to Australia’s

capital gains tax. Accounting & Finance, 50(4), pp.783–808.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.

Clark, J., 2014. Capital gains tax: historical trends and forecasting frameworks. Economic

Round-up, (2), p.35.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), pp.277-300.

Taylor, G. and Richardson, G., 2014. Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting & Economics, 10(1),

pp.1-15.

TAXATION LAW

Reference

Bain, K and Boccabella, D, 2019. The age of the home worker - part 2: Calculation of home

occupancy expense deductions, deduction apportionment and partial loss of CGT main residence

exemption. Australian Tax Forum, 34(1), pp.65–93.

Boll, K., 2014. Mapping tax compliance: Assemblages, distributed action and practices: A new

way of doing tax research. Critical Perspectives on Accounting, 25(4-5), pp.293-303.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion. Routledge.

Brown, P., Ferguson, A. and Sherry, S., 2015. Investor behaviour in response to Australia’s

capital gains tax. Accounting & Finance, 50(4), pp.783–808.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.

Clark, J., 2014. Capital gains tax: historical trends and forecasting frameworks. Economic

Round-up, (2), p.35.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), pp.277-300.

Taylor, G. and Richardson, G., 2014. Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting & Economics, 10(1),

pp.1-15.

12

TAXATION LAW

Tran-Nam, B., 2015. Tax compliance as a red tape to businesses: Conceptual issues and

empirical evidence from Australia. Journal of Business & Economic Policy, 2(4), pp.76-87.

TAXATION LAW

Tran-Nam, B., 2015. Tax compliance as a red tape to businesses: Conceptual issues and

empirical evidence from Australia. Journal of Business & Economic Policy, 2(4), pp.76-87.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.